VAL - Occidental Petroleum: Good Risk-Reward In The Energy Sector

Summary

- Occidental Petroleum is set to report Q4 earnings in coming weeks, and shares are still attractive despite a massive run over the last couple years.

- Berkshire Hathaway now owns over 20% of OXY's shares, with the authorization to increase their stake up to 50% ownership.

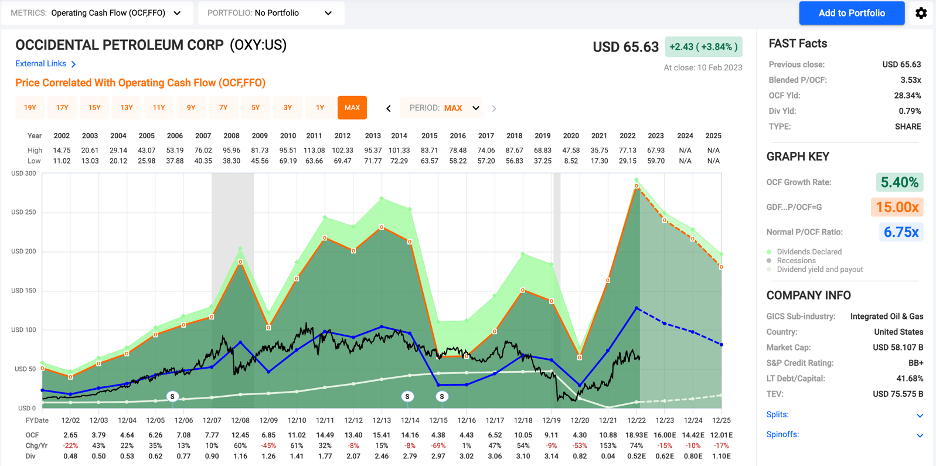

- Shares are cheap today at 3.5x cash flow and are cheap relative to oil majors like Chevron and Exxon Mobil.

- OXY is expected to focus on buybacks this year and could potentially redeem Berkshire's preferred shares.

- I also talk briefly about the offshore sector, where I find the risk/reward to be very attractive today.

It has been almost a year since I wrote an article covering Occidental Petroleum ( OXY ) and I think now is a decent time to write an update as their year-end earnings approaches in the next couple weeks. In my last article I talked about the Berkshire Hathaway ( BRK.A ) ( BRK.B ) stake, which has since grown to more than 20%. They have permission to buy up to 50% of the outstanding stock, and if shares drop, I think we will see continued buying, which will probably support OXY’s share price. While I still think energy is an attractive sector to invest in, I think the outperformance for the large energy companies over the last couple years might not continue in 2023.

Investment Thesis

Occidental Petroleum has had an interesting couple of years, where their ill-timed Anadarko acquisition led to an overleveraged balance sheet and a dividend cut in 2020. Since then, they have repaired their balance sheet and are set to post impressive year end results for 2022 in coming weeks. Shares are still cheap at 3.5x cash flows, and they look cheaper than oil majors like Chevron ( CVX ) and Exxon Mobil ( XOM ), which recently announced large buyback programs. OXY looks like they will follow suit with an increased focus on buybacks in 2023 and the potential redemption of Berkshire’s preferred shares.

I have been putting money to work in the energy sector in recent months, but I have been focused on the offshore sector, where the risk/reward looks very attractive in my opinion. I’ll be the first to admit that I missed the boat on the energy trade in 2021 in stocks like OXY, Chevron, and Exxon Mobil, but I think stocks in the offshore sector are poised for an impressive run in the next couple years. I think OXY is likely to raise their dividend with their year-end results, and the company will probably follow it up with a solid 2023, especially if energy prices increase. If I had to pick an oil major to buy today it would be OXY, and I think any dip near $60 would provide investors with a margin of safety.

Why I Like Offshore Today

Over the last three months, I have been focused on the offshore sector because I think some of the most attractive opportunities in the whole stock market can be found in this long out of favor sector. This includes Transocean ( RIG ) and Tidewater ( TDW ), but I also like Valaris ( VAL ) as well. Day rates have continued to increase, the supply and demand setup for offshore is very attractive, and I think investors looking for a speculation in the energy sector might want to take a closer look at these companies.

I still find OXY attractive at current levels, but I think offshore companies are still mispriced relative to their assets and the prospects for the sector over the next couple years. OXY still has fantastic assets, and like other oil majors, they are planning to emphasize buybacks over production growth in 2023. This brings me to a short rant on buybacks in the energy industry, which have received widespread criticism from politicians and talking heads.

Buybacks: Only A Problem For The Energy Sector

One of the things I find hypocritical about the criticism of energy company buybacks is that we have seen companies in other sectors buying back more stock without so much as a peep from the political establishment. Tech giants like Apple ( AAPL ), Microsoft ( MSFT ), and Google ( GOOG ) ( GOOGL ) have dumped billions into buybacks for years. The energy sector limped along for years until 2021 when rising oil prices lifted all boats and provided huge returns for investors. For managements in energy, there is no reason to invest in production growth when politicians are threatening windfall profits taxes and other policies that restrict the energy sector.

Balance sheets across the sector have improved dramatically, and Chevron announced a $75B buyback recently with Exxon Mobil announcing a $35B program . While OXY won’t have a buyback program of that size, I think investors can expect significant buybacks over the next 12 months. One of the other things that would be a positive for investors is the potential redemption of Berkshire’s $10B of preferred shares. I also think OXY is a bit cheaper than giants like Chevron and Exxon, which will make the buybacks more attractive.

Valuation

OXY is one of the companies that used 2022 to improve its balance sheet, reducing debt by about $8B in the first nine months of the year. They already earned well over $10 per share in the first nine months, and I would guess that they will add another dollar or two to that total in Q4. Their results for 2023 is going to be tied to oil prices, which have come off in recent months, but I think we will see energy prices trend higher this year.

{kind=link}

OXY’s operating cash flows should still be impressive for 2023, even if they don’t match 2022’s results. Shares are trading at a price/cash flow of 3.5x, which is still well below the average multiple. While shares aren’t as cheap as they were a couple years ago, I still think they are attractive today and will likely provide solid returns for investors. Shares can be volatile, but for investors looking to add to their position, buying shares at or below $60 looks like a good risk/reward to me. On top of the improved balance sheet and increasing buybacks, OXY should be able to provide investors with another dividend hike in 2023.

The Dividend

OXY was forced to cut their dividend in 2020 to a token payout of $0.01, but they have since raised the quarterly payout to $0.13. My guess is that they will increase the payout with their year-end results, but they have already stated that they intend to focus on buybacks, so I wouldn’t count on a massive increase. The yield isn’t much to write home about at 0.8%, but I think that their payout should grow over the next couple years.

Conclusion

Earlier I mentioned that I think the large oil companies might not outperform like they have over the last couple years. This is more due to the cyclical nature of markets, and I still think energy will be a good place to be invested, even if we don’t see the massive outperformance continue. For those buying today, I think the risk/reward is the most attractive in the offshore sector, but I still think OXY will provide solid returns over the next couple years due to its low valuation, improved balance sheet, and continued focus on buybacks. I also think OXY is more attractive than oil giants like Chevron and Exxon, which are more richly valued, but do offer larger dividends. Investors looking at adding to their energy holdings might want to add shares of Occidental Petroleum, especially if shares dip below $60 in coming weeks.

For further details see:

Occidental Petroleum: Good Risk-Reward In The Energy Sector