PRMRF - Occidental Petroleum: The Next Step

Summary

- The Anadarko acquisition has faced unexpected challenges from the start.

- Good management will have in place a "just in case" plan that was likely used in the last couple of years.

- Operational improvements take time for a large acquisition.

- The second quarter report combined with a robust commodity price outlook takes some pressure off management about the acquisition outlook.

- There are about 10 million unexplored acres that had zero value on the reserve report that could make this acquisition quite a bargain at a very low average value.

(Note: This article appeared in the newsletter on August 14, 2022, and has been updated as needed.)

Occidental Petroleum Corporation ( OXY ) made the acquisition of Anadarko Petroleum ((APC)) and then endured probably one of the worst futures possible after the acquisition. Still, many companies will plan for that "just in case emergency" precisely because they happen often enough that managers need to have a plan. Occidental managed to sell assets while using the currently strong commodity price market to repay debt faster than expected. Still, Mr. Market wants more after the fiscal year 2020 events. That more may well be on the way.

There was a general feeling that the reason that Occidental management bid more than anyone else for the assets is that they felt they could run these assets better than anyone else bidding to justify the price they bid. Just running the assets better was not a real high bar considering the "goings on" that many of us covered at Anadarko. The real unknown for many of us is the operational improvement that Occidental management can produce.

Any acquirer with plans to operate the assets better has to put up with things they cannot change. Incorrect well spacing or even antique completion designs are not something that can be easily fixed (for example). Therefore, operational improvements including better drilling and completion practices will become apparent to shareholders only after there is a significant amount of the new (and better) practices to show on the financial statements. For an acquisition of the size made, that could take a few years.

Such improvements and management changes undoubtedly began the minute Occidental gained control of the acquisition. Clearly, the center stage was on the asset sales of the past and the challenges of the coronavirus demand destruction. Management likely worked overtime to whip operations into shape even as oil prices fell through the floor while Mr. Market was losing hope on the situation.

The higher prices have provided welcome financial relief to what was clearly a beleaguered company. Now the question is how management can prove to the market that those better operations have provided a financial benefit to shareholders. Occidental used a very normal acquisition and post-acquisition strategy that I have covered many times with several different companies. Without fiscal year 2020, the improvement or lack thereof probably would be obvious. Now, I think management will have a harder sell.

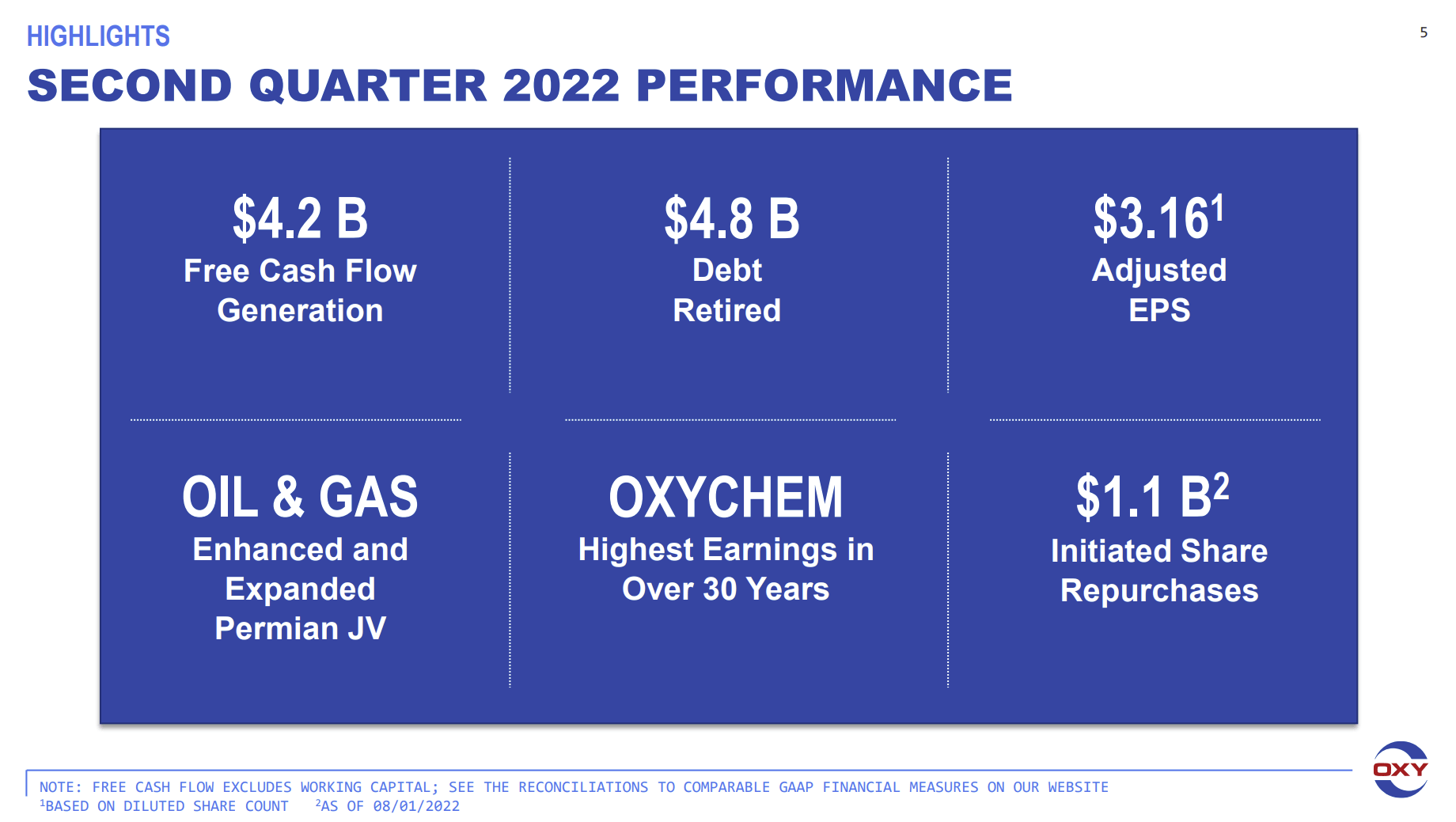

OXY's Second Quarter Report

Still, rising commodity prices make many managements look good to the market. In this case, the rising prices have provided a welcome relief from the criticism brought on by the unexpected challenges of fiscal year 2020 that sent the stock price through the floor. Had any of us seen the fiscal year 2020 challenges before they happened, we would have all done things very differently.

Occidental Petroleum Second Quarter 2022, Results Summary (Occidental Petroleum Second Quarter 2022, Conference Call Slides)

{kind=link}

The market is going to expect record earnings and cash flow generation at lower prices. The management's pace of improving operations will clearly speed-up during a time of record prices because there is more cash available to get things done.

In the meantime, management is reducing financial risk by getting that debt reduced. For many, the current announced level of $20 billion in long-term debt (approximately) was a great initial goal. It will probably need to go lower for common shareholders because common shareholders will likely add the preferred stock to the long-term debt to get the financial ratio. Currently, high commodity prices actually allow lower leverage goals to be achieved much faster than any of us thought possible.

There is also a general perception that demand exceeds supplies. That should fuel further optimism about reshaping the balance sheet. Still, the stock is likely to make progress only as fast as the financial leverage reduction proceeds.

Currently

Price earnings ratios throughout the industry appear to be at historical lows, even if a lower selling commodity price projection is taken into account. That should imply some decent long-term capital gains as some faith is restored to an industry that took a considerable financial beating since the end of 2015.

Just as Mr. Market was sure in 2014 that the good times would last forever, that same Mr. Market is now convinced (as shown by low price-earnings ratios) that the good times will again abort as they did in 2018 before the industry really had anything close to the usual upcycle financial benefits.

The Future

But this industry has extremely low visibility and is full of surprises. The rush into the market by a lot of money that had no experience and wanted to make a quick buck because "it was going to be easy" is just not there. That kind of investor and lender lost a lot of money both in 2016 and again after 2018. Right now, that appears to be enough to keep that money away from the industry.

Many think that the industry lost access to lenders. Yet, the debt market and banks that know the industry are still there as they always have been. What is not happening is the unrealistic buyouts (that had no chance) and funding that led to a lot of write-offs and bankruptcies over the last five years.

Many quickly forget that what looked like a reasonable loan in 2014 (under the assumption that $90 per barrel prices would last "forever") quickly became a very foolish loan in the 2015-2016 time period. Similarly, those same investors and lenders hoping for a return to the good times in 2018 were quickly disappointed in 2019. That same crew had major financial challenges in a very unexpected fiscal year 2020.

But the experienced crowd largely escaped the headlines of fiscal year 2020. That crowd remains with the industry doing sound deals. Contrary to popular belief, the debt market and the capital market never close. But the cost of doing business can climb to levels unacceptable to many managements. Maybe that looks like a closed market to some. But the difference is in how costs can come back down when conditions change appropriately (as opposed to a formal reopening).

Managements that considered their stock price undervalued and therefore refused to do accretive transactions that lowered debt levels often had very predictable results that could have been avoided.

On the other hand, managements that took what they could get (Paramount Resources ( PRMRF , POU:CA), Earthstone Energy ( ESTE ), Laredo Petroleum ( LPI ) and many more) climb out of the challenging times to participate in the recovery. There is an old saying that "your first loss is your best loss." Many managements learned that the hard way.

Occidental management managed to sell assets to reduce debt as promised through some very challenging times. By and large, management kept the promises and guidance made after the acquisition that could be kept.

Probably the largest asset that was on the books with no value was about 10 (depending upon how you count) million unexplored acres that were part of the acquisition. Since the acquisition, management has gone through that acreage and dealt with at least some of it. But those acres do not have to average out to a lot of money to make the acquisition a real bargain.

An average price of say $500 an acre for that acreage already changes the deal for the other parts of the company in a material way. Good times like this offer management the best time and financial resources to explore that asset for value. There are likely to be some announcements about that acreage from time to time over the next several years. Let's see what happens.

For further details see:

Occidental Petroleum: The Next Step