OCFCP - OceanFirst Financial: A 10.5% Yield To Call On The Preferred Shares

2023-08-11 11:44:48 ET

Summary

- OceanFirst Financial's Q2 results showed stable performance, with a slight decrease in net interest income and higher non-interest expenses.

- The bank's loan portfolio is robust, with a low amount of past due and non-accruing loans.

- The preferred shares offer a 7.41% yield and may be called in 2025.

Introduction

Back in May, I wrote an article on the preferred shares of OceanFirst Financial ( OCFC ), a regional bank headquartered in New Jersey with exposure to New Jersey, New York, and Pennsylvania . Although I wasn't planning on buying the preferred shares right away, one of my orders was filled shortly after publication and I now have a (relatively small) long position in OceanFirst's preferred shares , so I plan to keep an eye on the bank's financial performance on a quarterly basis to make sure I take appropriate action when necessary.

The Q2 Results: Stable

As explained before, I focus on two very specific elements when I try to determine if a preferred share is a good fit for my portfolio. The preferred dividends need to be very well covered and there should be plenty of junior equity on the balance sheet.

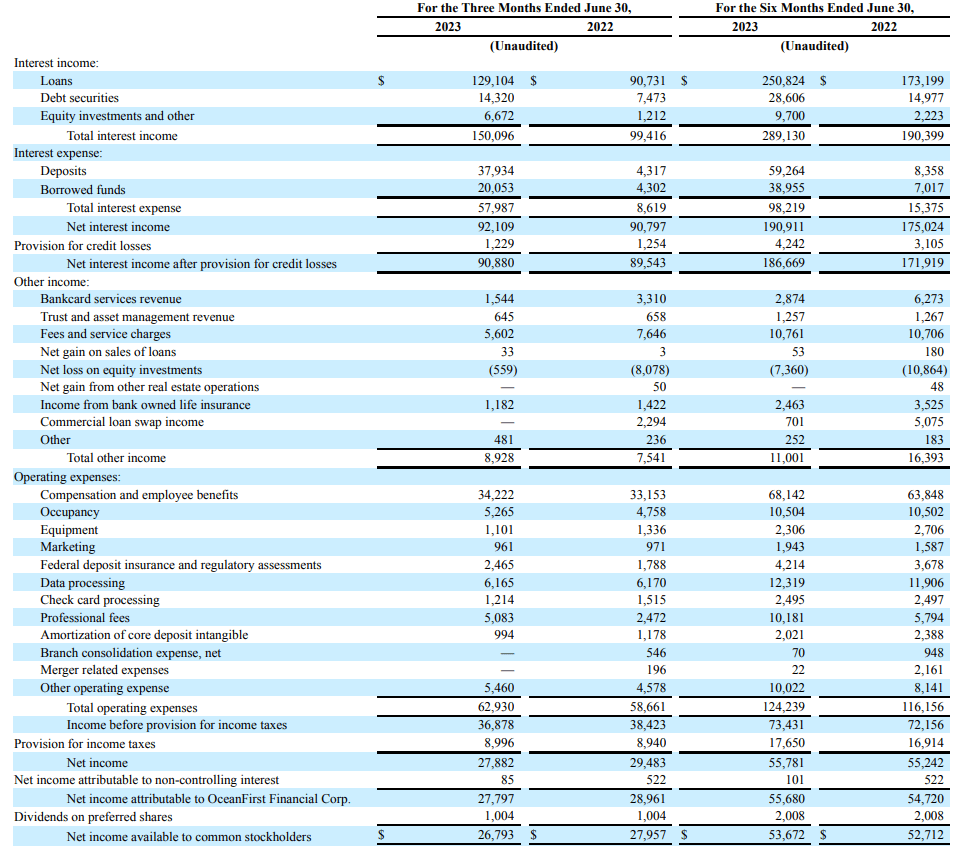

To determine the dividend coverage ratio, we obviously need to have a look at the financial results of the bank. OceanFirst saw its interest income increase by just over $10M compared to the first quarter of this year, but the interest expenses increased at a faster pace (by about 10%) which meant the net interest income decreased on a QoQ basis, but still came in slightly higher on a YoY comparison.

{kind=link}

The bank also reported higher non-interest expenses (up $4.25M) and was only able to compensate a portion by the higher non-interest income. This resulted in a pre-tax income of approximately $38M before taking loan loss provisions into account. Those provisions decreased on a QoQ basis as the bank recorded a $3M provision in Q1. And as you can see in the image above, a $1.23M provision was deemed to be sufficient in the second quarter of the year. The total reported pre-tax income was $36.9M and this resulted in a net income of $27.9M of which $28.8M was attributable to OceanFirst Financial.

That's the net income before taking the preferred dividend payments into account. The preferred shares have a fixed preferred dividend payment (I'll discuss the details later in this article), and as you can see in the income statement, the bank needs about $1M per quarter to cover those preferred dividend payments. The net income attributable to the common shareholders of OceanFirst was $26.8M, which is approximately 45 cents per share. The H1 EPS was approximately $0.91 and the Q1 and Q2 bottom line results were very similar, which means the required payout ratio was rather stable at around 3.5-3.7% of the net income attributable to OceanFirst. Although the preferred shares are non-cumulative, the low payout ratio makes them relatively attractive.

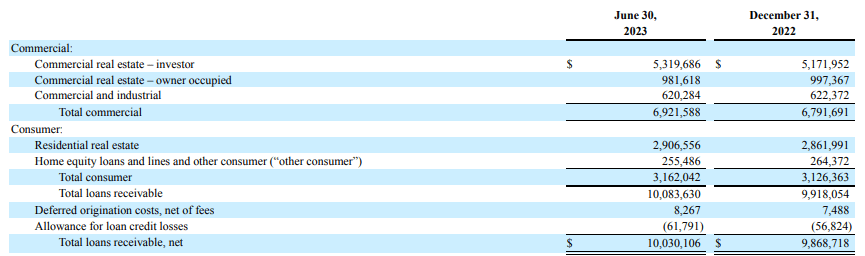

The income statement also shows OCFC can easily increase the total amount of loan loss provisions it's recording in any given quarter. And although a quarterly provision of just over $1M appears pretty low given the total size of the loan book of in excess of $10B, OceanFirst's loan portfolio is quite robust.

{kind=link}

As you can see above, just over 30% of the loans consists of residential real estate related loans but about 63% of the loan book consists of commercial real estate. While that may be a red flag at first, the details of the loan book indicate that in excess of 60% of the total amount of loans past due occurs in the residential real estate portfolio, which represents just about 30% of the total portfolio size.

{kind=link}

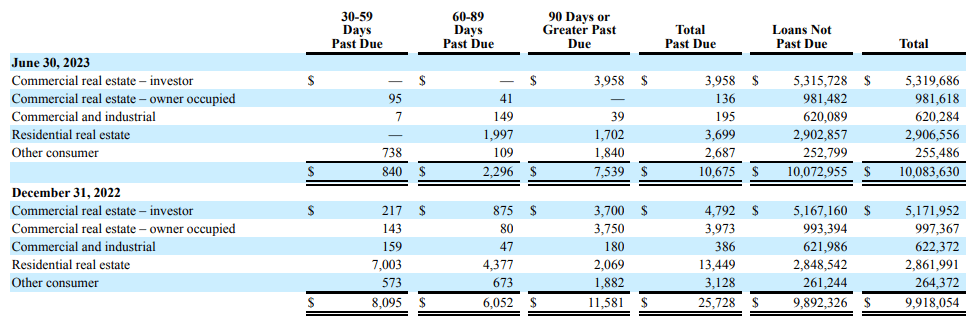

As you can see above, the vast majority of CRE loans are perfectly up-to-date. And the total amount of non-accruing loans stood at $22.8M as of the end of June, which is even lower than the total at the end of 2022. This means that both the total amount of loans past due as well as the non-accruing loans has decreased in the first semester.

OCFC Investor Relations

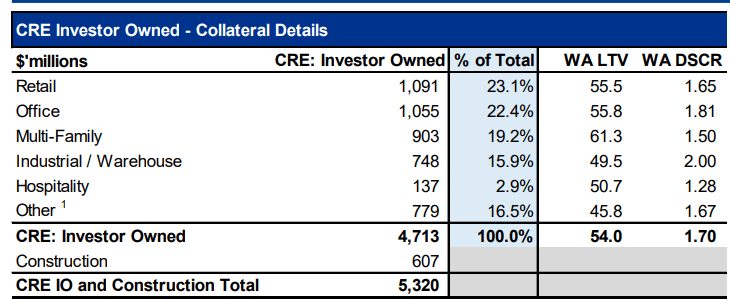

It will be important to keep an eye on the office portfolio which accounts for just over $1.05B of the loan book but with an LTV ratio in the mid-50s and very limited exposure to the CBD offices, OceanFirst should be able to navigate through the current choppy waters.

{kind=link}

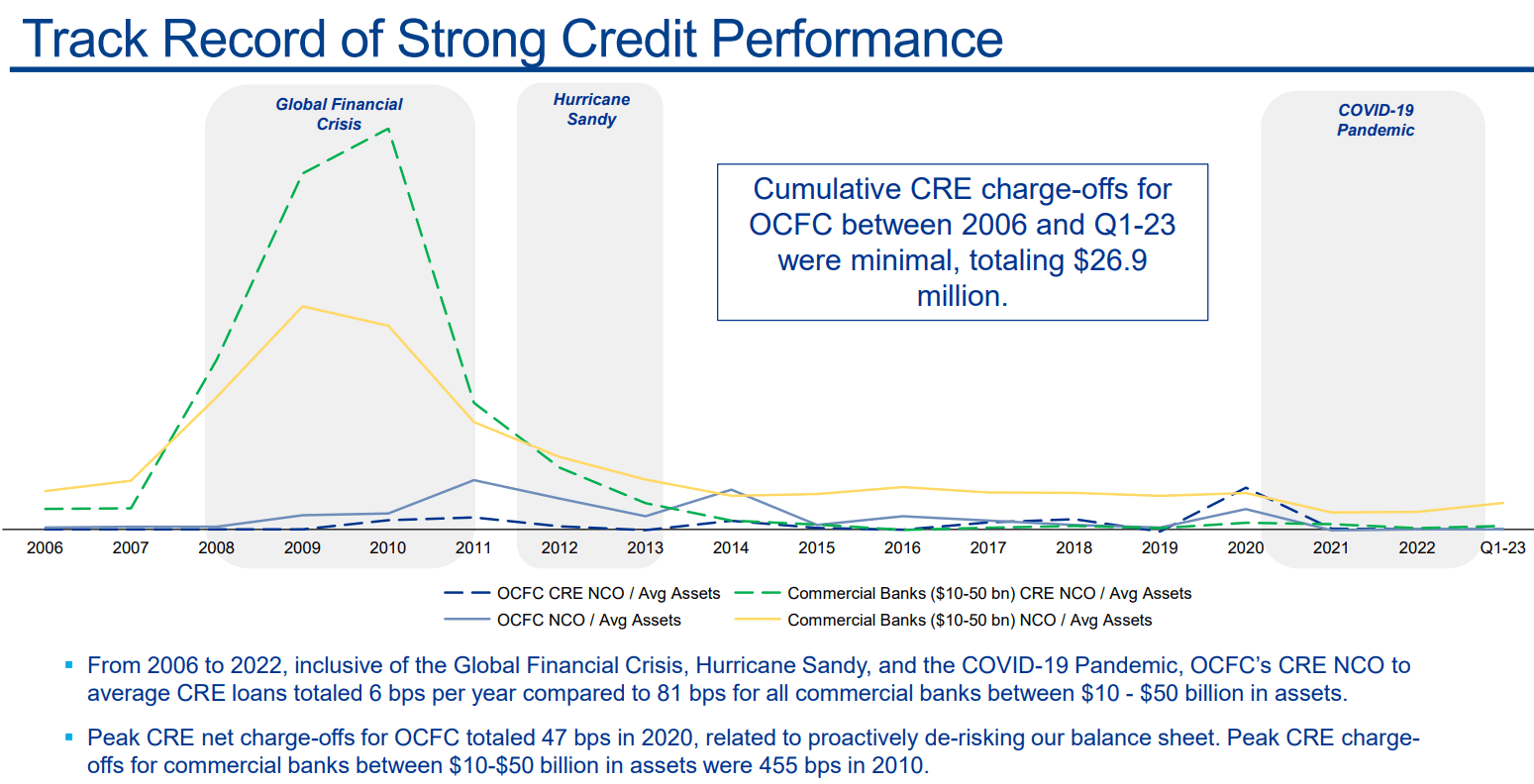

The most convincing argument is probably the bank's history in dealing with market disruptions. As you can see below, the bank has outperformed its peers when it comes to credit quality.

{kind=link}

The common shares of the bank are still attractive at 1.05x the tangible book value (and about 1.15x TBV if you'd include the unrealized losses on the HTM securities portfolio) and offering a 4.35% yield thanks to a quarterly dividend of $0.20 , but I'm interested in the private shares for the income portion of my portfolio.

The preferred shares have a non-cumulative preferred dividend of $1.75 per year (payable in four equal quarterly tranches) and as the preferred share is currently trading at $23.60, the current yield is approximately 7.41%. An additional bonus is that these preferred shares will move to a floating rate in May 2025. The new floating rate will be the 3-month SOFR + 684.5 basis points per year. With the 3-month SOFR currently at 5.36% , the pro forma floating preferred dividend rate would increase by just over $3/share per year. And based on the current share price, the yield would increase to 12.7%.

I doubt the bank will want to pay double-digit yields, and given the relatively small issue (less than $60M on a total equity of in excess of $1.6B), I think the odds to see the bank calling these preferred shares are increasing. The yield to call still exceeds 10% making it an interesting security to both speculate on a call, and if a call option doesn't happen, the preferred dividend will likely increase substantially upon a reset in 2025.

Investment Thesis

The bank has guided for its net interest margin to remain flat or show a "nominal decline" in the third quarter, which seems to indicate the worst of the rate hike impact is now behind us. Additionally, the run-rate of the operating expenses should decrease to about $58-59M (this was in excess of $62M in the second quarter) and the combination of both could result in an earnings boost in 2024.

But from the perspective of a preferred shareholder, I'm happy to hold my position. I'll keep an eye on the quality of the loan book to see if the situation deteriorates dramatically, but without any unforeseen circumstances, I expect the preferred shares to be called in 2025.

For further details see:

OceanFirst Financial: A 10.5% Yield To Call On The Preferred Shares