VTI - October CPI Preview: Downside Miss Likely

2023-11-10 12:00:36 ET

Summary

- Recent jobs report shows moderating job growth, easing wage pressures, and positive productivity.

- Consensus expectations for CPI to drop and monthly increase to be half of last month's increase.

- I predict a downside miss in the upcoming CPI report due to factors such as supply-side drivers and a steep drop in energy prices.

What to expect from the October CPI report?

"These young guys are playing checkers (chess) . I'm out there playing chess (Bughouse) ." - Kobe Bryant (Jay Powell).

The October jobs report was so good that I'd use a saying my dad uses in golf to describe a perfectly hit drive in golf. If you hit such a drive, he will say, "You couldn't have walked it out there any better." The report was convincing evidence that a soft landing is transpiring. Furthermore, recent Cleveland Nowcast Inflation projections show that progress is likely. The jobs report showed:

- Job growth is moderating at a pace that doesn't yet indicate a recession.

- Easing wage pressures.

- Productivity continues to be positive.

Many in the Wall Street consensus now think that the inflation number will show dogged persistence in the face of tightening and that the Fed's job will be hard. To be sure, they have some compelling evidence in their corner. However, I think we're primely positioned for a downside upset of consensus expectations.

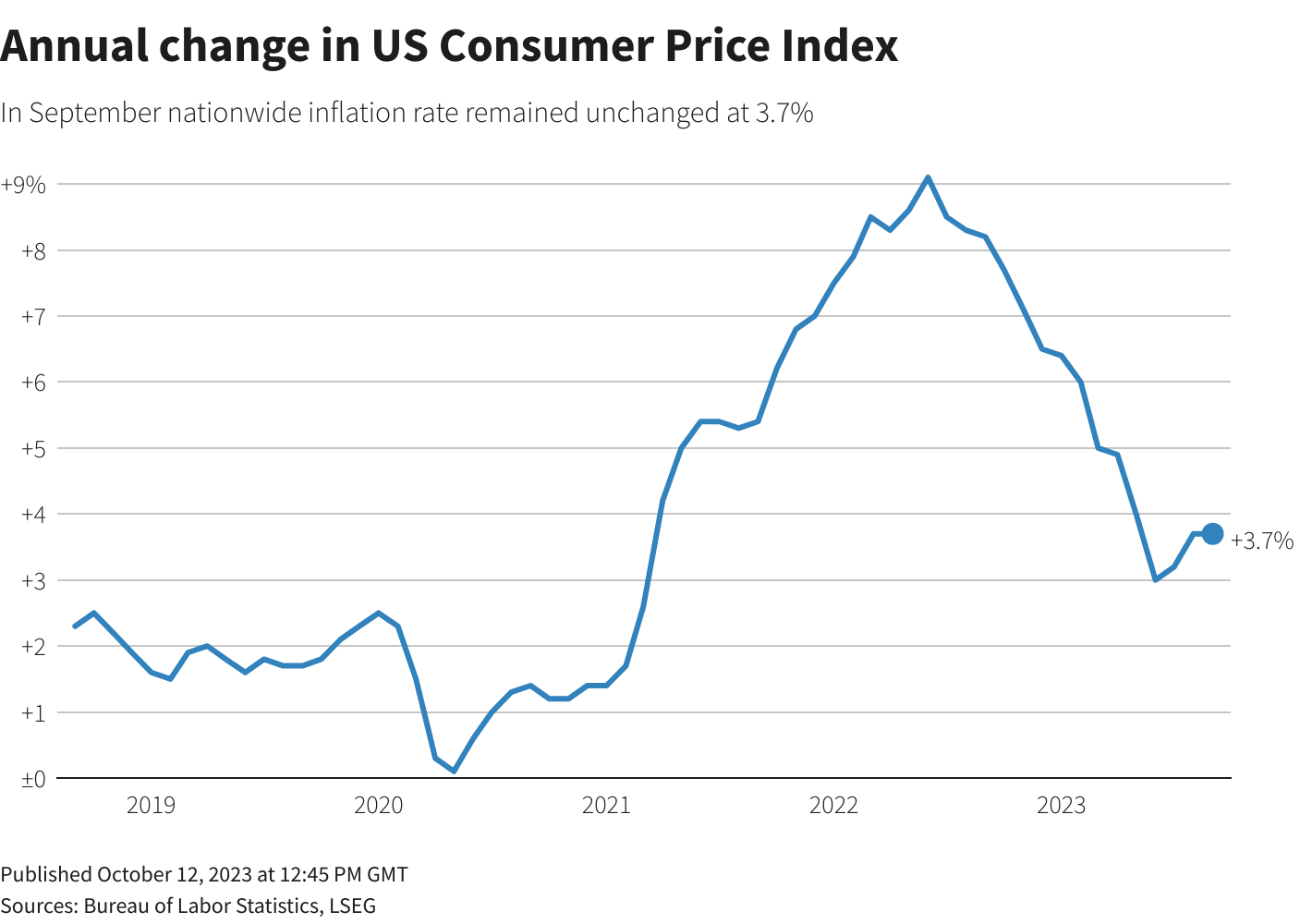

- Consensus expectations are for the 3.7% annual CPI to drop to 3.4%

- Consensus expectations are for a monthly increase of 0.2%, or half of last month's increase.

{kind=link}

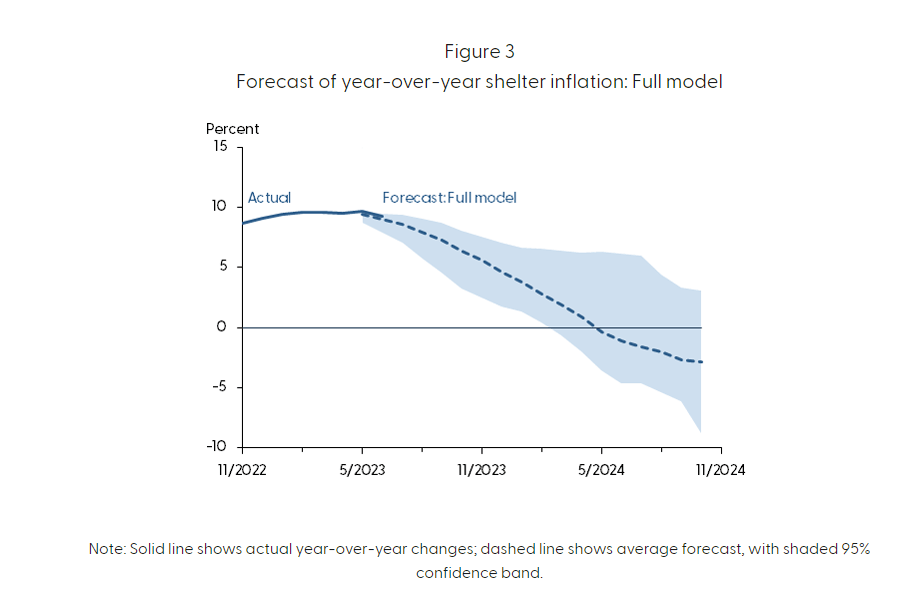

I suspect that something different may occur. We may see some real weakness as some supply-side drivers continue the normalization process, and a steep monthly drop in energy prices should be prominent in the report. And despite the strength in rents that helped the report exceed expectations last month, independent measures continue to suggest some alleviation or price pressure is forthcoming. Furthermore, some compelling research from the San Francisco Fed suggests that shelter inflation will be coming down convincingly in 2024.

{kind=link}

Shelter is the whole game regarding the future of Fed decision-making, and I think there's firm evidence that it will come down convincingly. It notoriously lags. However, if you remove shelter from the core CPI, it drops to well below 2% and brings broader CPI to 2%. So it really is the whole ball game. In previous work , I've explained why some asymmetric per capita consumption of the rich is helping to drive the stickiness here.

But convincing evidence from all sorts of leading and concurrent data sources suggests the shelter is so plaguing the Fed right now that it will be a welcome guest in the future. If this report shows the first cracks in a shelter at a time when Energy has dropped so quickly, a significant downside miss is possible. Goldman Sachs recently did an excellent report illustrating why the last chapter of inflation could be easier than consensus expects, and I wholeheartedly agree with their conclusion.

Goldman Sachs Global Investment Research

The following CPI report is coming out on Tuesday, November 14th. Wall Street highly anticipates this report because one of the key things market observers are looking for is evidence that the Fed has vanquished inflation. I believe this report will be a downside miss. One of my favorite market commentators, Seth Golden (@SethCL), has pointed out that in months when gasoline has been down a similar amount to what it's been down in October, the CPI report tends to come to light. As Mr. Golden pointed out:

In the 14 other months since 2005 that saw gas prices decline -9%+, headline #CPI during the comparable month declined an average of -0.4% with negative readings 12 times.

So, I think this factor suggests CPI forecasts are too high. And I mentioned that seasonality for gasoline would likely be a positive factor in the last two months of the year. That dynamic appears to be playing out nicely so far, which is particularly impressive given the white-hot tensions in the Middle East. However, I have been confident since the October 7th attacks that despite the shocking nature of this chapter of the Arab-Israeli conflict, the effects on markets and volatility would be much more subdued than consensus expected.

{kind=link}

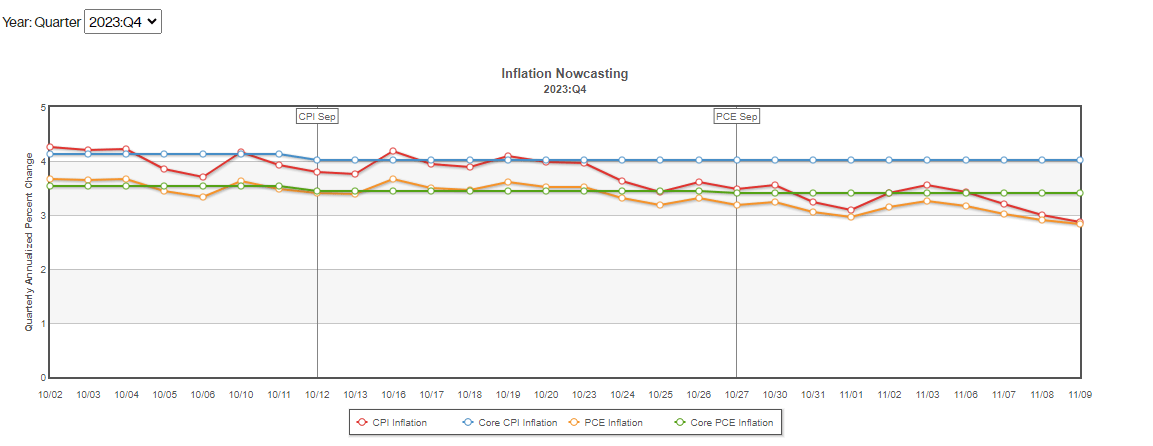

The last CPI report was mostly in line but slightly hot, caused by elevated rental costs. Still, the report showed the broad trend of downward inflation remained intact. But let's also remember a crucial factor: it showed the core accelerating at the slowest pace in two years. I don't think anything is suggesting that this will be reversed. I also think the strength in rents was likely seasonal and should be subdued in this report compared to the last report. I do not think that the hot rents last month were the beginning of a trend. The Cleveland Fed's Inflation prediction tool also suggests a lower level.

{kind=link}

Furthermore, an underappreciated factor that should be showing up in the inflation numbers is that the world's second-largest economy has been experiencing severe weakness. China is experiencing outright deflation right now, and that weakness will certainly mean lower prices for many U.S. consumers. The Fed has surely noticed such a significant development.

Bloomberg

When Xi Jinping comes to visit next week and everyone starts talking about how bullish Re-globalization is for stocks and how it will also alleviate inflationary pressure, remember that your pal Chris was writing about it months ago . In all seriousness, though, much is working positively for the Fed on inflation.

Risks and Where I Could Be Wrong

There is a lot of reason to suspect that inflation might be tricker to vanquish than the Fed would hope. Indeed, the institution lost some recent credibility, calling for inflation that would be "transitory" and far less impactful than it ended up. But one of the positives on inflation now is that the bears can't have it both ways.

If the economy is slowing, it will be tough for inflation to catch up. However, there could be the dreaded outcome of "stagflation." As remote a risk as this is, it is certainly not remote enough not to warrant mention. Unfortunately, if a dramatic escalation in the Middle East or elsewhere led to wider conflagrations than currently exist, that outcome would become much likelier.

{kind=link}

And the Fed's inflation dashboard is still flashing all red, no matter what the rest of the data says. And that is important. The recent GDP report came in very hot, and there are other indicators that the US consumer is only just starting to tap credit sources. So, inflationary pressure looks mainly in hand, but there is always a genuine chance it could reignite. Furthermore, any of the following risks could become so acute that they cause the market to shift focus and fall even if inflation is vanquished rapidly.

- Escalation of geopolitical risks in China, Ukraine, or the Middle East.

- Fed policy error.

- The banking crisis worsens.

- Return of inflation.

- CRE meltdown.

- Write-downs of private assets.

Furthermore, US borrowing costs are soaring, and U.S. treasury demand insurance is up. There has been a lot of upward pressure on rates, mainly from an expanding term premium. There is no shortage of risks, but I think we will climb the wall of worry into year-end, and I think this inflation report will show some "shock and awe" progress that has been lacking for a few months.

Conclusion: Powell's Playing Bughouse, Pundits Playing Chess

Many may read this and ask themselves: is this guy crazy? Did he hear how hawkish Powell was? One of the silly things I see repeatedly is when the media expresses surprise that Powell has again said that he may use the Federal Funds rate to contain inflation if required. This seems as obvious a decision as taking your guns to Dodge City, and I'll explain why.

Chess is a complicated game. It is a much more highly valued skill in some cultures than our own. Some train children from a very young age to be chess masters, and one of the ways they do it is with the game of Bughouse .

Now, for our purposes, I certainly don't have time to explain the chess game. However, I will briefly explain the Bughouse for those who do understand chess. Bughouse is a four-player variant of chess. Instead of just two players, each player has a partner who is playing the opposite of the color that they are. When your partner takes his direct opponent's piece, he gives it to you, and you can place it anywhere on the board. This changes the strategy entirely, as any open square is now vulnerable.

The difference between chess and Bughouse is similar to that between the Fed in Volcker's era and the modern-day Fed of Powell. In Volcker's day, the market responded to Fed open market operations; it didn't anticipate them far in advance. Powell's playing Bughouse. And in a world where the market can anticipate things several moves ahead in some cases, it's never wise to leave an open square. And that's why you can count on Powell talking tough on inflation until things are in hand, even though he and many on the committee likely focus on much of the same data (and so much more) introduced in this article.

For further details see:

October CPI Preview: Downside Miss Likely