OEF - OEF: Beware The Optimism Priced Into The S&P 100 Uber Caps

2023-07-14 13:42:04 ET

Summary

- The S&P 100, as reflected in the iShares S&P 100 ETF, has extended its outperformance vs. other developed market ETFs following a better-than-expected CPI report.

- But a closer examination of core inflation drivers and market pricing suggests caution may be warranted.

- With a select group of the S&P 100 Uber caps also at record valuation multiples on generative AI hopes, technical rebalancing-driven headwinds may be on the horizon as well.

The latest inflation print out of the U.S. was exceedingly bullish, decelerating to 3.0% in June (down from 4.0% in May and 4.9% in April) and sending stocks rallying higher on the news. But a look beneath the hood suggests some caution is warranted – yes, headline CPI is trending closer to the Fed's 2% target, but at 4.8%, core CPI (i.e., inflation excluding food and energy) remains rather sticky. And perhaps even more importantly, the key driver of the core, wage pressures, are still elevated. So, in contrast with the market pricing in a more optimistic outcome post-July hike, I suspect a pivot from recent Fed hawkishness may not yet be on the horizon.

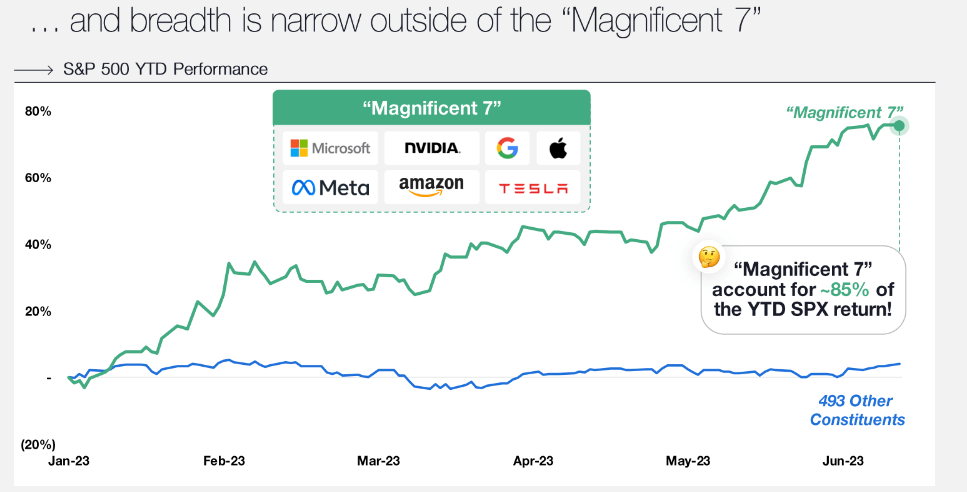

In the meantime, the high concentration of U.S. equity returns is a pressing issue – minus the " magnificent seven " stocks (a term coined by Coatue for the group comprising Microsoft (MSFT), Nvidia (NVDA), Tesla (TSLA), Google (GOOGL), Amazon (AMZN), Meta Platforms (META), and Apple (AAPL)), many of which have re-rated on artificial intelligence ("AI") hopes, the S&P Index (SP500) would have underperformed this year.

To be clear, I am not arguing against the potential of generative AI, as it may well drive a meaningful uplift to earnings and the lower cost of capital going forward. But underwriting a positive outcome (e.g., NVDA at >20x fwd revenues), let alone the timing of it seems premature here. Ahead of next week's big Nasdaq rebalance , overbought large-caps, many of which are part of the iShares S&P 100 ETF ( OEF ), could come under pressure; net, I would steer clear pending a better entry point.

Fund Overview - Low-Cost Exposure to an Increasingly Concentrated Blue-Chip Basket

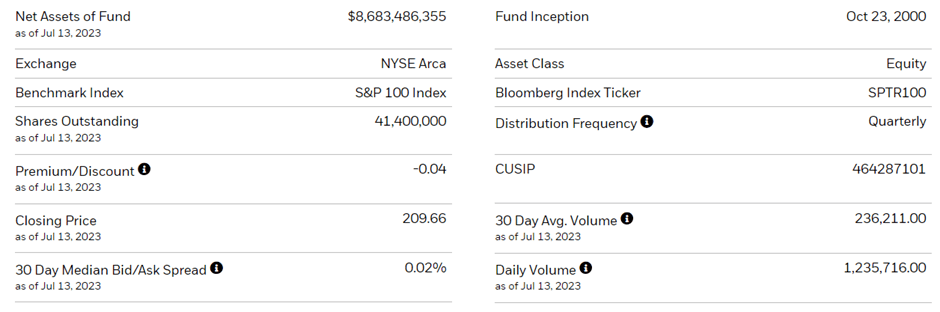

The U.S.-listed iShares S&P 100 ETF ((OEF)) tracks, before fees and expenses, the performance of the S&P 100 Index (SP100), comprising the largest blue-chip companies across multiple industry groups in the S&P 500 index (subject to approval from the S&P Index Committee). The exchange-traded fund ("ETF") held ~$8.7bn of net assets at the time of writing and charged a competitive 0.2% expense ratio. A summary of key facts about the ETF is listed in the graphic below:

{kind=link}

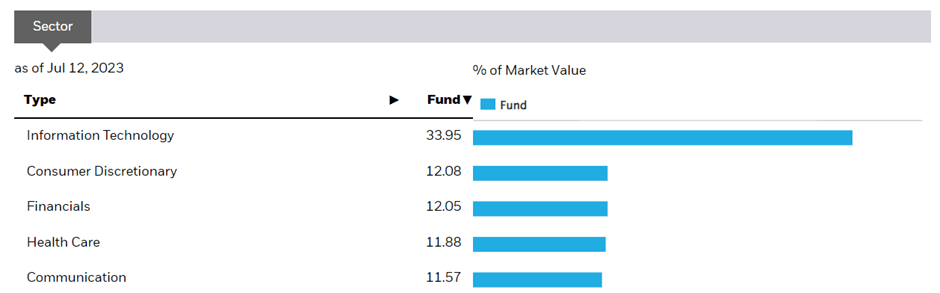

The fund is spread across 101 holdings (including cash), with the largest sector allocation (by far) going to Information Technology at 34.0%, followed by Consumer Discretionary at 12.1% and Financials at 12.1%. Additional sector exposures above the 5% threshold include Health Care (11.9%), Communication (11.6%), and Consumer Staples (7.1%). With the top five sectors accounting for a larger ~82% of the total portfolio, OEF screens as one of the more concentrated developed market ETFs from a sector perspective. In line with the tech-heavy exposure, the fund's equity beta is slightly above the S&P 500 at 1.02, while the standard deviation of its returns stands at 18.7.

{kind=link}

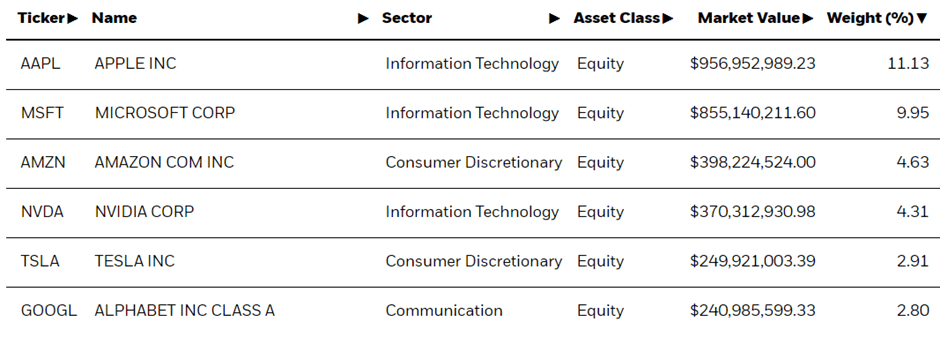

The fund's single-stock allocation reveals a heavier tech sector exposure than the headline sector breakdown suggests, with seven of the top ten holdings either directly or indirectly involved in tech (e.g., tech heavyweights like AMZN and GOOGL are listed under consumer discretionary and communication, respectively). Apple is the largest holding at 11.1%, followed by Microsoft at 10.0% and Amazon at 4.6%. Google is another leading ETF component, with exposure split across the class A and class C shares. Nvidia is the biggest gainer this year at 4.3%, while Tesla is the largest non-tech allocation at 2.9%. Despite OEF's increasing concentration in recent months, the sector balance consideration applied by the S&P 100 index committee generally keeps the ETF exposures in check.

{kind=link}

Fund Performance – Track Record Turbocharged by Last Decade's Outperformance

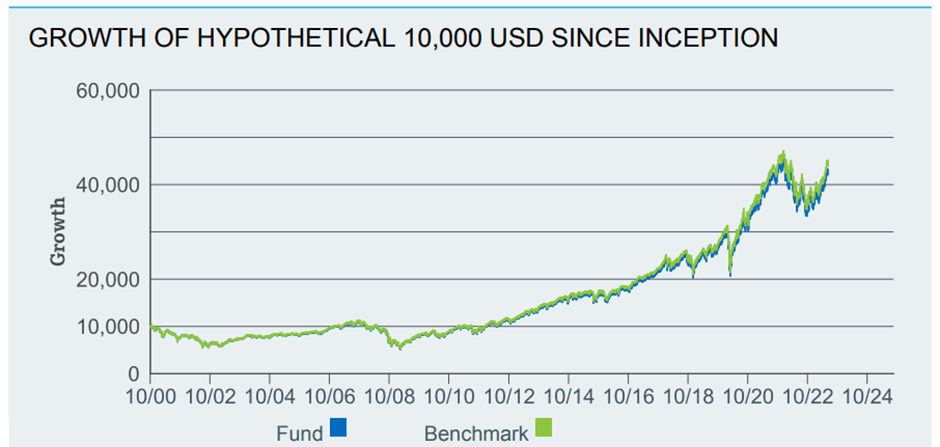

Having outperformed virtually all other developed market blue-chip indices this year at +22.5%, OEF makes a compelling case for owning quality. The strong YTD return has further boosted the fund's capital appreciation track record, which now stands at +6.7% annualized in market price and NAV terms since its inception in 2000. Most of the outperformance has been front-end loaded; outside of last year's -21.0% drawdown, the fund has consistently delivered low-double-digit % returns (+32.0%, +21.2%, and +29.1% in 2019, 2020, and 2021, respectively). In tandem, the fund's annualized five and ten-year returns have outpaced its closest comparable, the iShares Core S&P 500 ETF (IVV), at +13.4% and 13.2%, respectively.

{kind=link}

With the fund largely concentrated around high-growth big tech names, the distribution yield has generally been low (1.3% on a trailing twelve-month basis). Given the fund's holdings in companies with attractive reinvestment runways, however, management can't be faulted for reinvesting the excess cash vs distributing it to shareholders. That said, the OEF portfolio's underlying 23.6x P/E valuation stands out, a result of this year's rally largely coming from re-rated valuations (vs higher earnings). While the fund's blue-chip names could well grow into their valuations over time, there certainly isn't a lot of safety margin here.

{kind=link}

Near-Term Boost From Lower Inflation, But How Sustainable Is The Optimism

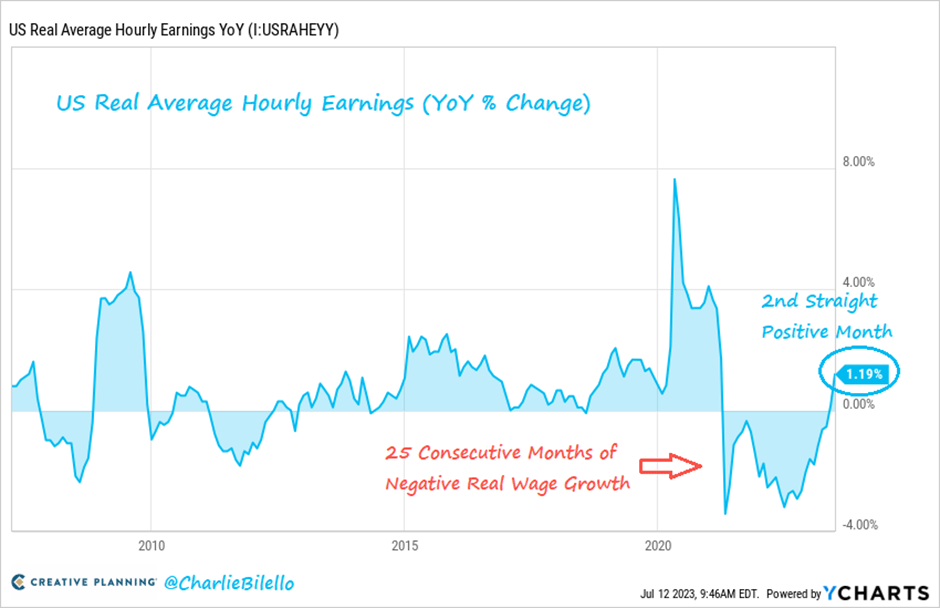

This week's consumer inflation report came in well below expectations, with the headline print moderating to 3.0% - down a full percentage point from last month. While undoubtedly a positive development, a closer look at the underlying drivers indicates outsized contributions from lower airfares due to declining jet fuel prices and a sizeable decline in used car prices, likely a result of higher rates biting into demand. But the key hurdle to a Fed pivot remains the persistent labor market tightness, with average real hourly earnings accelerating to 1.2% on the back of more blowout jobs reports (ADP +497k and the BLS at +209k). Alongside the fading USD strength (more so after the improved consumer inflation numbers), the strong wage growth should keep consumer balance sheets resilient, in turn, feeding into the persistence of core services inflation (at +4.8% vs the +3.0% headline).

{kind=link}

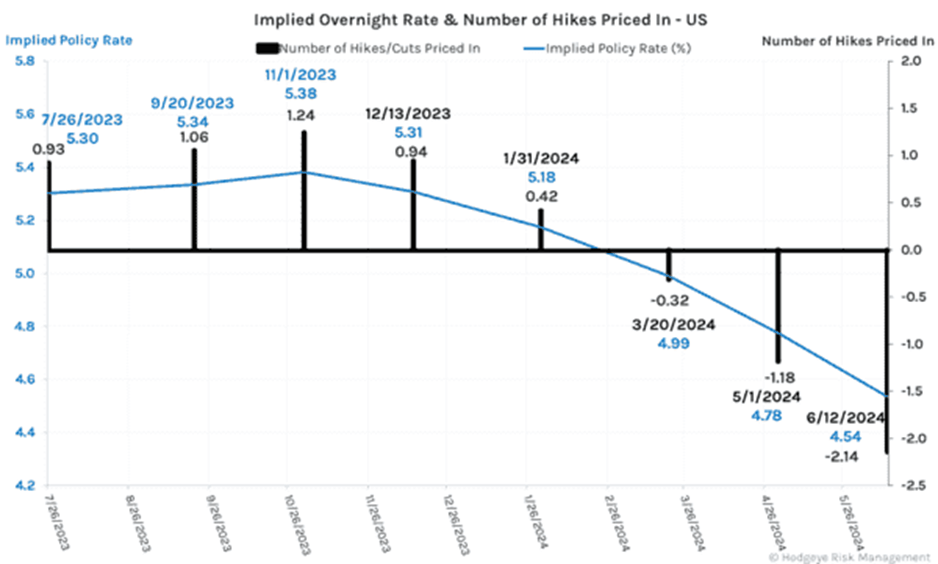

With the combination of labor market resilience, higher wages, and higher consumer spending likely to extend into the coming months, the readthrough for Fed policy isn't all that dovish, in my view. Even if core goods inflation continues to pull down the headline print post-June, ongoing labor market tightness should keep the Fed on track for another 25bp policy rate hike in July - at the very least. The 'liveness' of the September meeting is less clear, as the June CPI and subsequent labor market data may well tilt the scales toward another "skip" to November instead. Either way, with market pricing post-CPI pointing to only one more implied hike this year and three cuts through June 2024 (per overnight indexed swap ((OIS)) data), the risk-reward isn't skewed favorably for OEF bulls.

{kind=link}

Beware The Optimism Priced Into The S&P 100 Uber Caps

Buoyed by a small group of AI-driven stocks, the S&P 100 ETF has re-rated significantly this year in hopes of generative AI unlocking new profit pools for big tech. Further, accelerating the YTD rally was this week's surprisingly benign inflation print, at a +3.0% headline in June (vs. the Fed's 2% target). But with core CPI still running at sub-5%, wages remaining elevated, and the labor market remaining tight despite the accelerated rate hikes, the case for a Fed pivot isn't as airtight as the market seems to think.

Given current market assumptions for Fed dovishness post-July and AI-driven earning uplifts, there isn't much safety margin here; hence, I would remain cautious pending a meaningful valuation reset for the "magnificent seven" (particularly for Nvidia, which trades at >20x fwd revenue). Next week's Nasdaq-100 rebalance, a measure to address the elevated concentration of the tech mega-caps, likely won't be the straw that breaks the camel's back, but should add some downward pressure on OEF regardless.

{kind=link}

For further details see:

OEF: Beware The Optimism Priced Into The S&P 100 Uber Caps