OPAD - Offerpad Solutions: 5 Headwinds That May Be Too Strong To Overcome

2023-10-04 10:26:26 ET

Summary

- Offerpad Solutions went public in September 2021 with high expectations, but its value has since plummeted to 10% of its IPO valuation.

- The company operates as an "iBuyer," offering to buy homes directly from homeowners, but the real estate market is not conducive to instant transactions.

- Offerpad's market share in the iBuyer space is about 20%, but its gross margin and profitability are low, raising concerns about its future.

The adage "right place at the right time" applies many times to the stock market in general and to specific companies and their stocks to a greater extent. In hindsight, 2021 was the best time for Offerpad Solutions Inc. ( OPAD ) to have IPO'd as the market in general was running high, and the housing market was ablaze. I remember a few houses in my neighborhood, a nice suburb close to one of the hottest metros in the US but by no means a super-hot market, selling many houses way above the list price.

So, it is not surprising that Offerpad created a lot of excitement when it went public in September 2021, valued at $2.70 billion. So high were the expectations that the CEO called the entire US real estate market as his company's Total Addressable Market ((TAM)) at $1.9 trillion. I mean, what was to not like?

- Favorable stock-market conditions: Check

- Favorable sector/industry conditions: Check

- Favorable trend (with everything going online during COVID recovery): Check

Fast-forward almost exactly two years, the company is worth about 10% of its IPO valuation at $265 million. What went so wrong? Could things prove? Let's find out, but before that, a quick introduction to the company.

What Does Offerpad Offer?

Offerpad Solutions Inc. is an "iBuyer" company, which means they offer to buy homes directly from homeowners to make the process painless for the home sellers. But pain is a zero-sum game in the business world. Someone's gain is someone else's pain. Unfortunately, here, it appears like the company and its investors are the ones in pain.

The process is described below on the company's website: Tell them about your home, expect an offer within 24 hours, accept the cash offer with no requirements for showing or choose to list with them.

Offerpad Process (offerpad.com)

{kind=link}

The Most Non-i Sector

When I initially heard about "iBuyer", I thought "here comes one more company, almost 25 years late, using "i" for internet to convey they are digital". And it made sense, too, meaning the iBuyers operated without most of the overheads of a traditional real estate firm. But it turned out to be "i" for instant, and that fits the bill perfectly as well. Hear me out.

Whether it is "instant" or "internet", Real Estate happens to be one of the most unfit sectors for both words. Real Estate transactions are meant to take time. Not because that is how "they" wanted it to be, but homeownership is easily one of the largest financial obligations for most families. Let me rephrase that. It is the largest source of wealth according to the National Association of Realtors. Besides, there are plenty of nuances associated with buying a property, including but not limited to scrutinizing the location and the inspection report. From the seller's perspective too, there are checks and balances in place, including not hurrying into an offer and selecting the right buyer who will not spring last-minute surprises. These things are not supposed to be instant or purely over the internet.

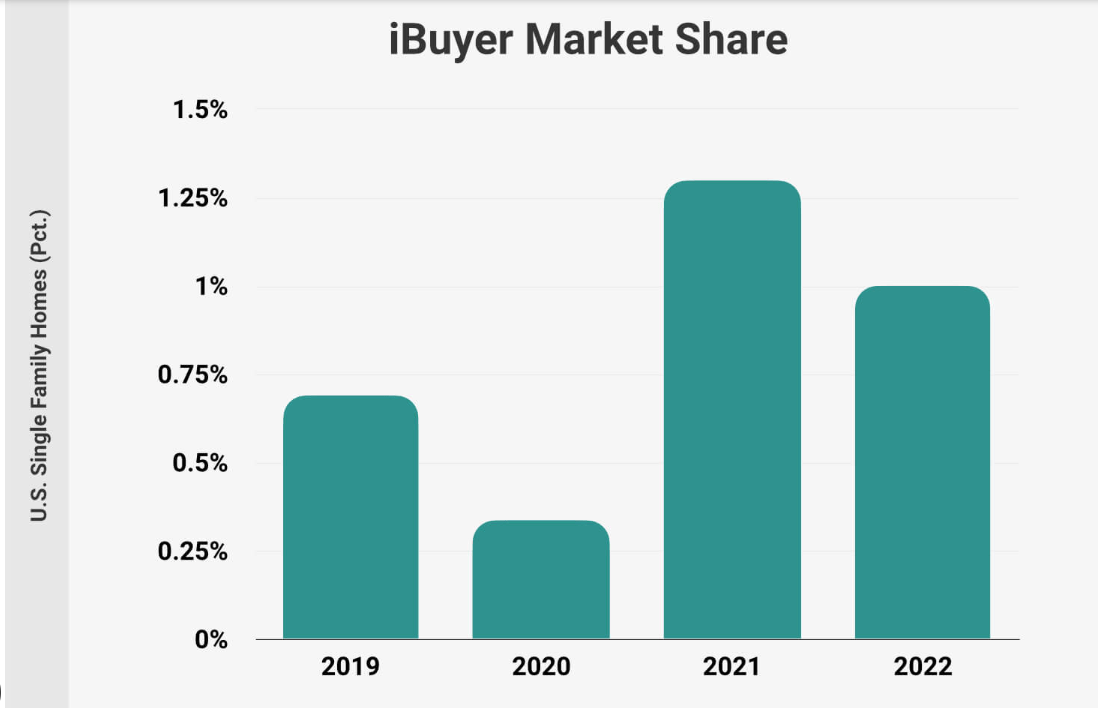

But what about the $1.9 trillion TAM that the CEO talked about when the company went public? Well, looking at the real estate market's TAM in case of Offerpad is like saying that starting a new car company is promising because it has access to a $1.53 trillion market. But let's just play along and plug some numbers. iBuyers have a total of about 1% market share (based on the number of transactions) of the US housing market. Extrapolating that to market value based on the $1.9 trillion housing market, we arrive at $19 billion as the current market share for iBuyers in total. That may sound impressive on the surface, but let's keep digging in.

iBuyer's Overall Share (rubyhome.com)

{kind=link}

20% of 1% Is Not Much At Even 10% Gross Margin

Like we played along in the section above about the company's TAM, let's play along with the numbers below, giving the company the benefit of the doubt.

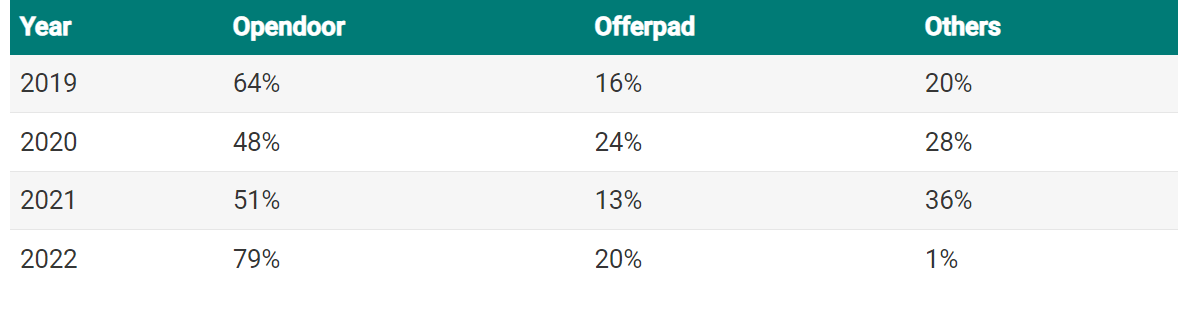

Offerpad has about 20% market share in terms of transactions in the iBuyer space, second only to (but by a wide margin) Opendoor Technologies Inc. ( OPEN ). 20% of the $19 billion iBuyer market share is about $3.80 billion and Offerpad reported $4 billion in annual revenue in 2022. So, close enough in the larger scheme of things that the number of houses sold (as a percentage) roughly translates into the revenue made (as a percentage). $4 billion in revenue in the first full year as a public company is not as bad as you think. Could the company be undervalued at 0.065 times 2022's revenue? Perhaps, but let's keep going.

iBuyer Marketshare (rubyhome.com)

{kind=link}

In its best-ever quarter as a public company, Offerpad reported a 9.80% gross margin, and it should be noted that this was the company's first report as a public company. Using 2022's full year revenue of $4 billion and the highest ever margin as a public company at 9.80%, we arrive at a gross annual profit of $392 million if everything aligns, from the macro conditions to sector conditions to the company's general operations. That means, under the best of situations and assumptions, the company is now trading at .67 times sales. Still, not too bad.

But now it is time to turn our focus to the current reality and what the future may look like. Getting back to gross margin, I love the picture below from Robinhood.com that reminds us to be careful about gross margin. It does not include operating costs, interest payments, and tax payments. Including each one of those items ignored by the gross margin, Offerpad made 5 cents per share in 2021 and lost 61 cents per share in 2022. Refer page 5 here . That gives the stock a multiple of 165 based on 2021's profit, and now things are starting to look bad. But hold on, it gets worse.

Gross vs Net (learn.Robinhood.com)

Macro Conditions Couldn't Be Worse

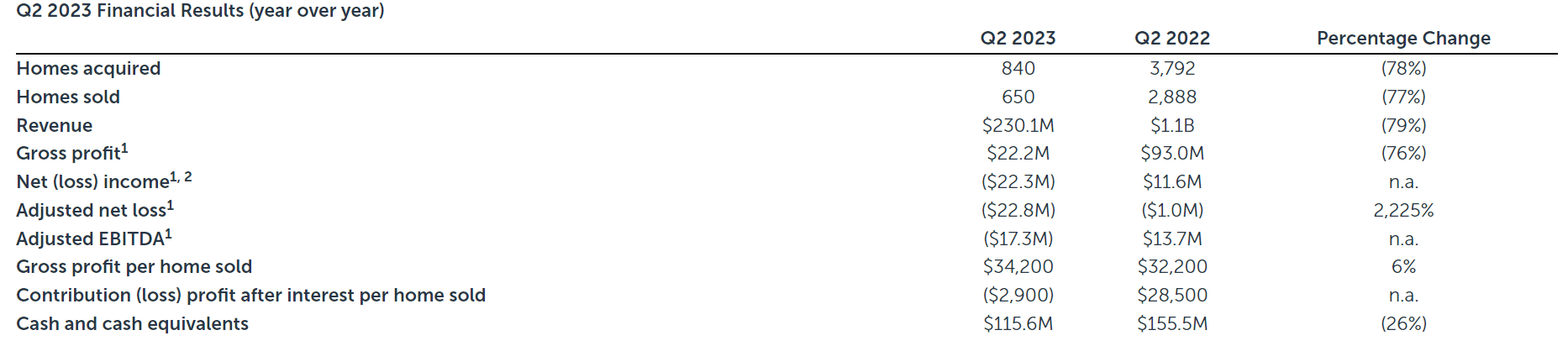

When Offerpad went public, the market was in a hurry. Home sellers were in a hurry, likely because they knew the craziness wouldn't last. The home buyers were in a hurry because every other buyer was in a hurry. This now appears like a thing of the past as inventory has been building up steadily and this shows in Offerpad's 2023 numbers with the company reporting at 78% YoY decline in homes acquired. While the company focused on its gross profit going up 205% QoQ in its recent Q2 results , things looked dreadful on a YoY basis overall, which is a better longer-term trend indicator.

OPAD Q2 2023 (investor.offerpad.com)

{kind=link}

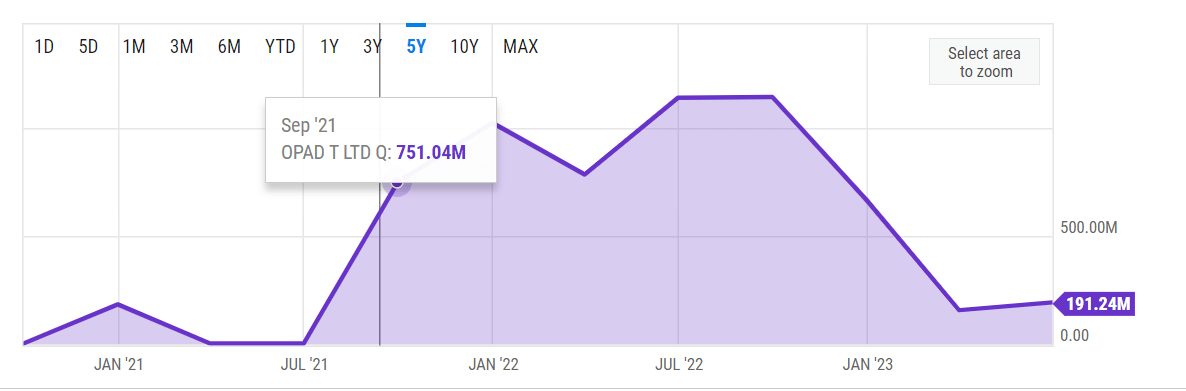

The Dreaded D-Word

Offerpad, like many of the small-caps I've analyzed over the past few months, is burdened by a (relatively) huge debt load. The company's current long-term debt of $191.24 million is 72% of the company's market cap. This has resulted in the company paying $40.3 million and $46 million in interest expenses in the last two quarters. While the company has about $115 million in cash and short-term equivalents, we must keep the company's business model in mind, cash offers to sellers within 24 hours.

{kind=link}

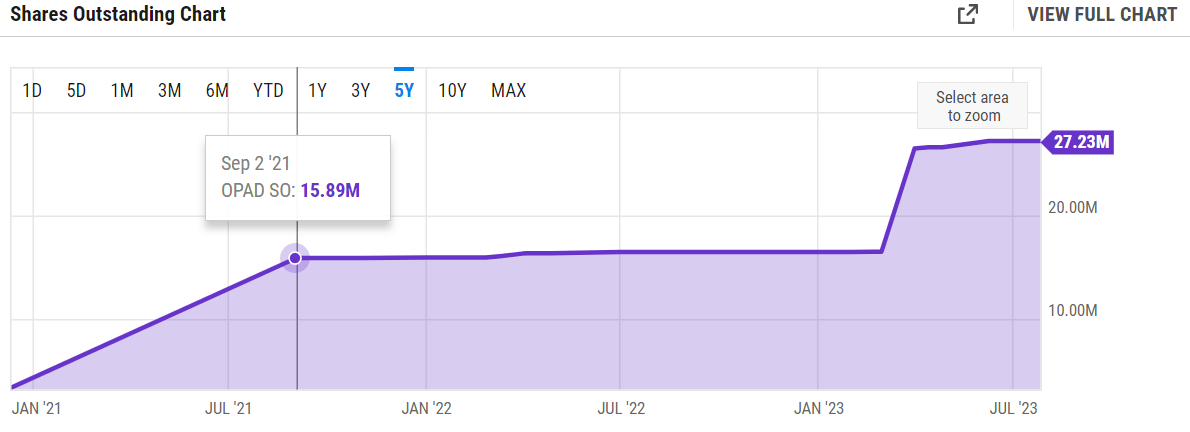

The Dreaded D-Word, Again

When you don't bring in enough money through your business operations, you have only two choices: take on debt or sell more shares to raise money. Offerpad has done both as the company's total shares outstanding have gone up by more than 70% since its IPO. Please note that the chart below takes into account the 1:15 reverse split executed by Offerpad in June of this year.

If the business does not recover quickly, with the cost of borrowing so high, I expect more dilution to come into the picture.

{kind=link}

Conclusion

Each one of the headwinds identified above is strong enough to derail any company. For example, some companies diluted their way to irrelevance while some are drowning in their own debt . Similarly, market conditions, including macro, competition, and being in the wrong space are challenging enough on their own. When you consider that Offerpad Solutions is facing all 5 of these headwinds at the same time, I find it prudent to ask if the company will even survive for long given the expectations around rates. There is a reason more established players exited the iBuyer space in 2021 at the market's peak. Hence, I rate the stock a sell.

For further details see:

Offerpad Solutions: 5 Headwinds That May Be Too Strong To Overcome