PDM - Office Isn't Dead Especially Those Soaking Up The Sunbelt

2023-03-30 07:00:00 ET

Summary

- In the business world, there were calls for “the death of malls,” the death of fitness centers, the death of movie theaters… and the death of offices, too.

- Don’t get me wrong: I’m very well aware that the office debate still rages.

- Yet many of those same big companies have rethought their 2020 thinking, telling employees today that they’re “coming back to the office.” Or else.

We all know the story of 2020.

The year began with so much promise in so many places. Individuals and corporations alike were touting a time of “perfect vision,” which might have been the biggest joke ever played out on the world. Very few people, if anyone at all, saw the global pandemic with its shutdowns coming.

Yet, just like that, before the first quarter could close, we were all shut up in our homes, going back and forth between watching online calculations of infection rates pile up and trying to distract ourselves by binge-watching Netflix and Hulu.

It wasn’t a pretty time, with loved ones lost, income sources ruined, businesses shuttered, and fears running rampant of what more could still happen.

In the business world, there were calls for “the death of malls,” the death of fitness centers, the death of movie theaters… and the death of offices, too. Life was online for good, expert after expert said. And, admittedly, I didn’t think fitness centers and theaters were going to make it, either.

But they did to varying degrees. Apparently, society hasn’t progressed enough to be content with a Wall-E- like world. That 2008 Disney and Pixar production showed a future where nobody did anything for themselves. Life was handed to them electronically to the point where they didn’t even stand, carried around on motorized floating carts wherever they wished to go.

Humanity had turned into amorphous blobs from lack of even the most basic exercise.

That could still happen, but like I said above, we’re not there yet. Despite how the ultimate fate of movie theaters remains questionable, gym use is back big-time, many of the malls that survived are doing just fine (or better) today, and traffic jams are most definitely a thing again as people once again go back to the office.

Whether they like it or not.

The Debate Around Office Survival Goes On

Don’t get me wrong: I’m very well aware that the office debate still rages. It seems like every other week, we hear of some employee expression against the non-changing times. The claims are common, passionate, and often grounded in firm logic.

The let-me-work-from-home crowd says they’re more productive outside of the office due to:

- Lack of cooler talk

- Lack of commuting

- Lack of time spent getting food from restaurants (the kitchen fridge is right there, after all).

That’s not to say they don’t have self-focused reasons to stay home, of course. Lack of cooler talk can be a major bonus when you don’t like your colleagues. The money not spent on gas driving to and from work can go a long way toward paying the grocery bill. And let’s face it… working in your PJs can be a dream come true when you’re just not feeling like making the aesthetic effort.

But perhaps their biggest reason for wanting to work from home is that they’re used to it.

Nobody asked them to be locked in their homes for months or more on end. That was forced on them, along with the notion that “the new normal” was there to stay.

Consider the CNN headline , “The Office, as You Know It, Is Dead” from August 25, 2020. It began like this:

“Bustling skyscrapers and office parks packed with workers could be a relic of the pre-pandemic world.

“The health crisis has forced millions of Americans to abandon their offices in favor of working from home, for better or worse. Now there are signs this may not be a short-term phenomenon, but more of a permanent shift in favor of remote work even after a Covid-19 vaccine is in place.

“More than two-thirds (68%) of large company CEOs plan to downside their office space, according to a survey released Tuesday by KPMG.”

Moreover, the pandemic was “proving employees don’t need to work in cubicles to be successful.” So why bother with the high costs of renting?

Read a bit further down and you’ll see an opinion from KPMG CEO Paul Knopp, who told CNN Business that, “This is a longer-term trend. It’s here to stay.”

Yet many of those same big companies have rethought their 2020 thinking, telling employees today that they’re “coming back to the office.” Or else.

… But Should It?

Again, in those employees’ defense, the “death of the office” talk didn’t stop after 2020. The debate was still raging in February 2021, when Forbes published , “The Office Is Dead. Long Live the Office!”

While it supported the continuing existence of said concept, it was through a hybrid model. Most news outlets were arguing for that reality at the time, yet so many people were still working remotely, with no office time spent whatsoever.

Nor did that change intensely enough to stop Globalization Partners from running a blog titled “Is the Office Dead? The Great Debate Between Remote and In-Office Work" on August 25, 2022. And even this year, on March 3, CNBC published , “Full-Time Office Work Is ‘Dead’: 3 Labor Experts Weigh in on the Future of Remote Work.”

It included the following “Key Points”:

- “Remote work ballooned during the Covid pandemic as a public health measure.”

- “The share of full-time remote work seems poised to flatline at a level five times that of 2019.”

- “Workers and companies have reaped benefits, especially in so-called ‘hybrid’ arrangements.”

I write this to reassure you that I completely understand if you think the office is dead, too: that, as an investor, you’d be crazy to consider putting your money into a company built around renting out office space.

Based on the information we’ve all been bombarded with these past three years, you might reasonably think you’d make lackluster returns, at best. But in the case of real estate investment trusts, that doesn’t have to be the case.

I’ve compiled a list below of office real estate investment trusts, or REITs, that I see good – even great! – things for going ahead, with those focused on the Sunbelt looking particularly good.

These states and the cities within them tend to be more traditional, at least when it comes to how they work. That’s why there’s a lot to be said in favor for the landlords that operate there.

Over the River and Through the “Woods” to an Office REIT We Go

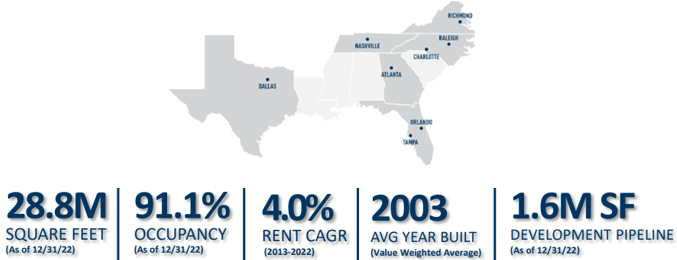

Highwoods Properties, Inc. ( HIW ) specializes in office properties primarily located in Atlanta, Georgia; Charlotte and Raleigh, North Carolina; Dallas, Texas; Nashville, Tennessee; Orlando and Tampa, Florida; and Richmond, Virginia. The REIT clearly has a heavy presence in the Sunbelt region, which should serve it well due to the ongoing trend of migration to the southern regions of the country.

{kind=link}

HIW has 28.8 million square feet of real estate with a 91.1% occupancy rate… a rent compound annual growth rate ((CAGR)) of 4%... and, as of December 31, 2022, $1.6 million in its development pipeline.

New leasing volume did decline significantly in 2020, but it’s since increased over the last two years. Plus, HIW has shown strength in its new leasing volume, with new leases in 2022 exceeding the 2019 levels… by over 19%! Additionally, new leasing volume exceeded 2013’s and 2014-2021.

HIW Investor Presentation

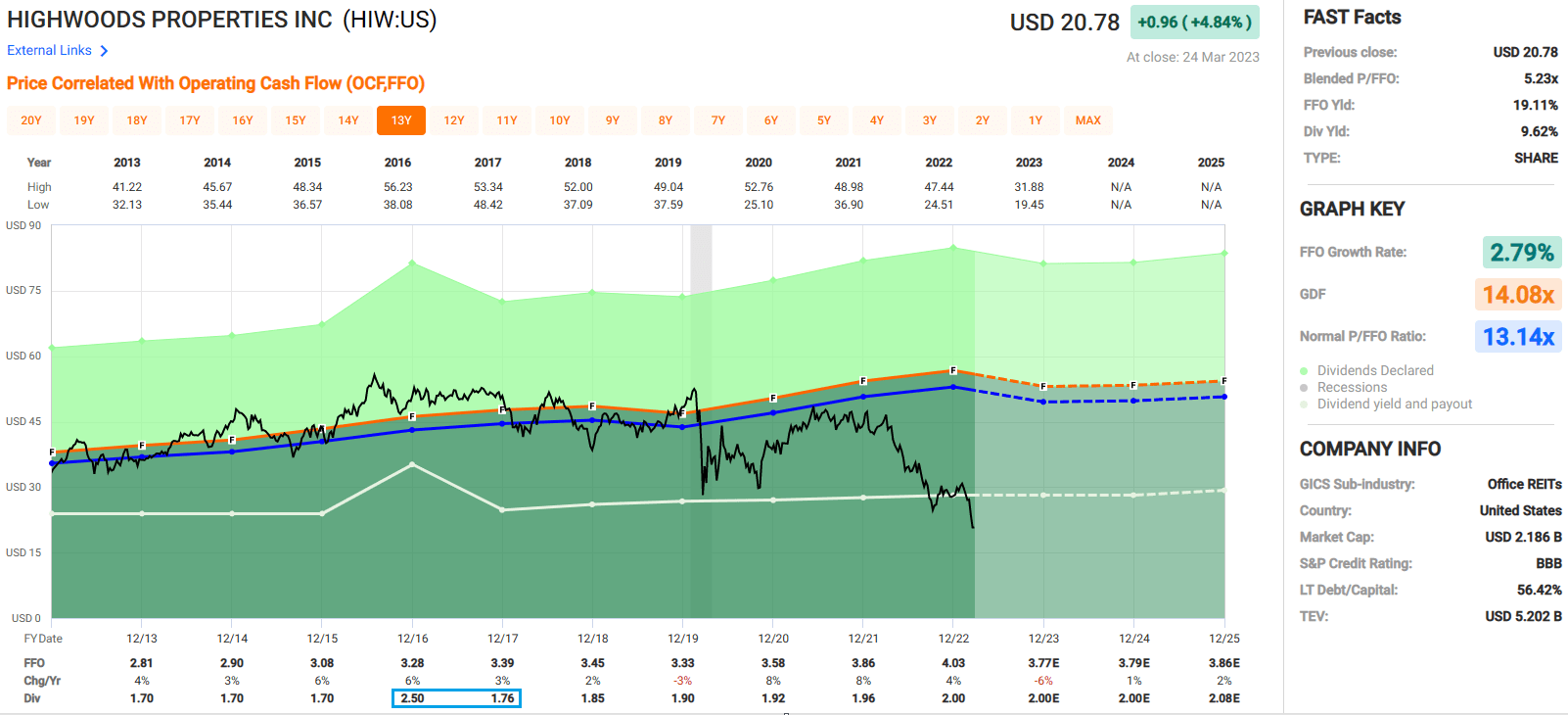

It’s also averaged dividend growth rate of 3.05% over the last 10 years. For the record, what looks like a dividend cut in 2017 was not. HIW paid a special dividend of $0.80 in 2016 but resumed its normal quarterly payouts after that. The quarterly rate in 2016 was $0.425, which was increased in 2017 to $0.44.

The REIT has averaged a funds from operations ((FFO)) growth rate of 2.79% since 2013. Analysts expect FFO to fall by 6% in 2023, but then increase by 1% in 2024 and 2% in 2025.

{kind=link}

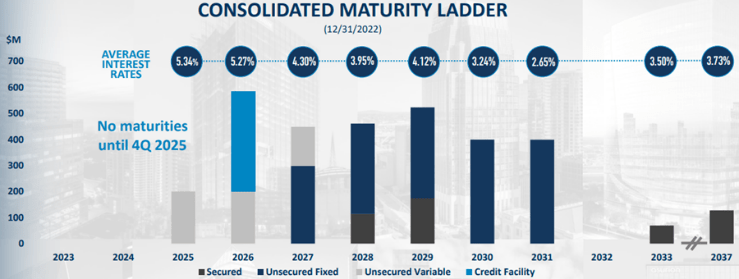

Its balance sheet is BBB rated, and the REIT boasts solid credit metrics:

- 5.9x net debt to earnings before interest, taxes, depreciation, and amortization for real estate (EBITDAre)

- 41.6% debt + preferreds as a percentage of gross assets

- 4.1% weighted average interest rate

- No consolidated debt maturities until the fourth quarter of 2025.

{kind=link}

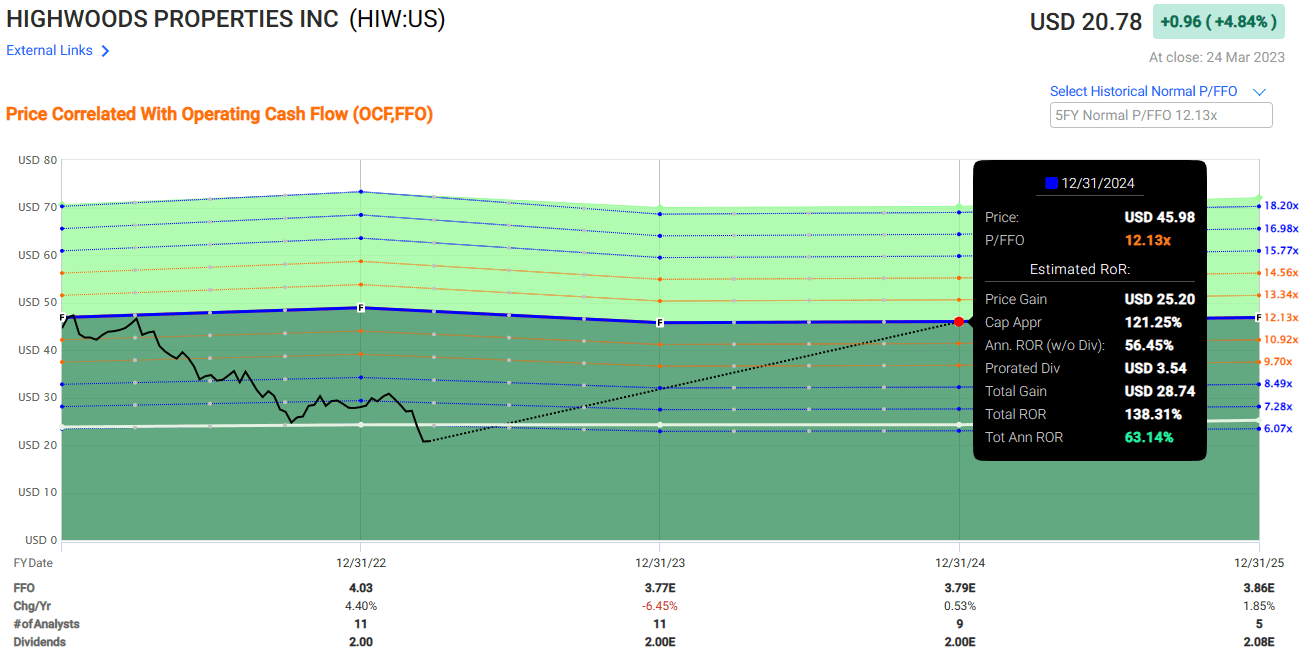

Highwoods is trading at a significant discount, with a current p/FFO of 5.23x vs. its normal 13.14x. And it currently pays a 9.62% dividend yield that’s well covered with an AFFO payout ratio of 76.74%.

iREIT maintains a Strong Buy here, with a total return estimate of 63.14% annually by 2024, assuming that HIW’s p/FFO reverts to its five-year average.

{kind=link}

Trust This Office REIT to Get the Job Done

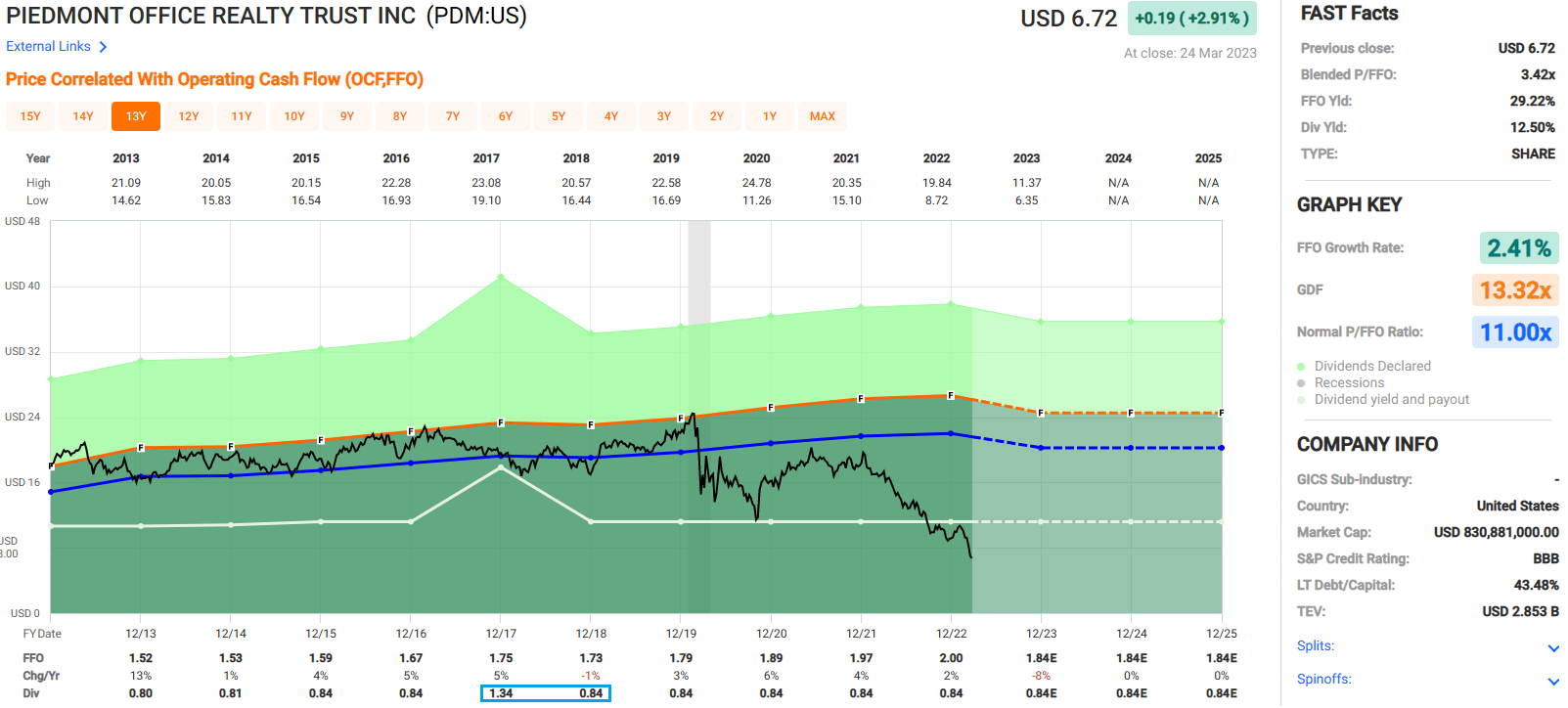

Piedmont Office Realty Trust, Inc. ( PDM ) owns, manages, and develops Class A office properties in Atlanta; Boston, Massachusetts; Dallas; Minneapolis, Minnesota; New York, New York; Orlando; and Washington D.C.

There are obvious cities in that list that aren’t in the Sunbelt region. But two-thirds of its annualized lease revenue ((ALR)) comes from such states.

Piedmont owns 51 office properties that cover 16.7 million square feet that were 86.7% leased with a remaining lease term of approximately six years.

Additionally, no tenant accounts for more than 5% of PDM’s ALR.

PDM Form 10-K

Piedmont’s leasing transactions during 2022 included the largest amount of annual new tenant leasing since 2018. For the full year, the company had 203 leasing transactions, with new tenant leasing at 763,000 square feet and total leasing at 2,153,000.

PDM Presentation

Piedmont has a compound dividend growth rate of 0.49% over the last 10 years. What looks like a dividend cut in 2017 was not. PDM paid a special dividend of $0.50 in 2017 but resumed its normal quarterly payouts in 2018.

Then again, while PDM hasn’t cut its dividend since 2013, it hasn’t raised it much either. In 2014, it bumped it up a penny to $0.81… to $0.84 in 2015… and not a cent since.

Analysts expect it to remain at $0.84 on an annual basis until 2025.

PDM has averaged an FFO growth rate of 2.41% since 2013, though analysts expect it to fall by -8% in 2023 and remain flat in both 2024 and 2025.

{kind=link}

So why am I recommending it?

This office REIT has a strong balance sheet with a BBB rating and solid credit metrics:

- 6x net debt to core EBITDA

- 37.2% net debt to gross assets

- 90% of its debt is unsecured

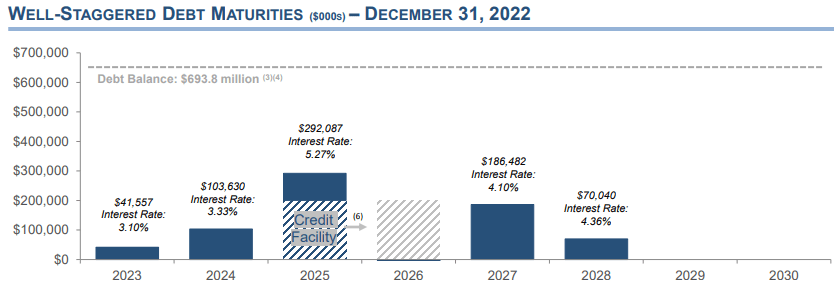

- $17 million in cash on hand with $600 million available on its unsecured credit line.

PDM does have some sizable maturities that come due over the next three years. But it has the liquidity to service its debt obligations in the near term.

PDM Presentation

And here’s the really interesting aspect I want to highlight…

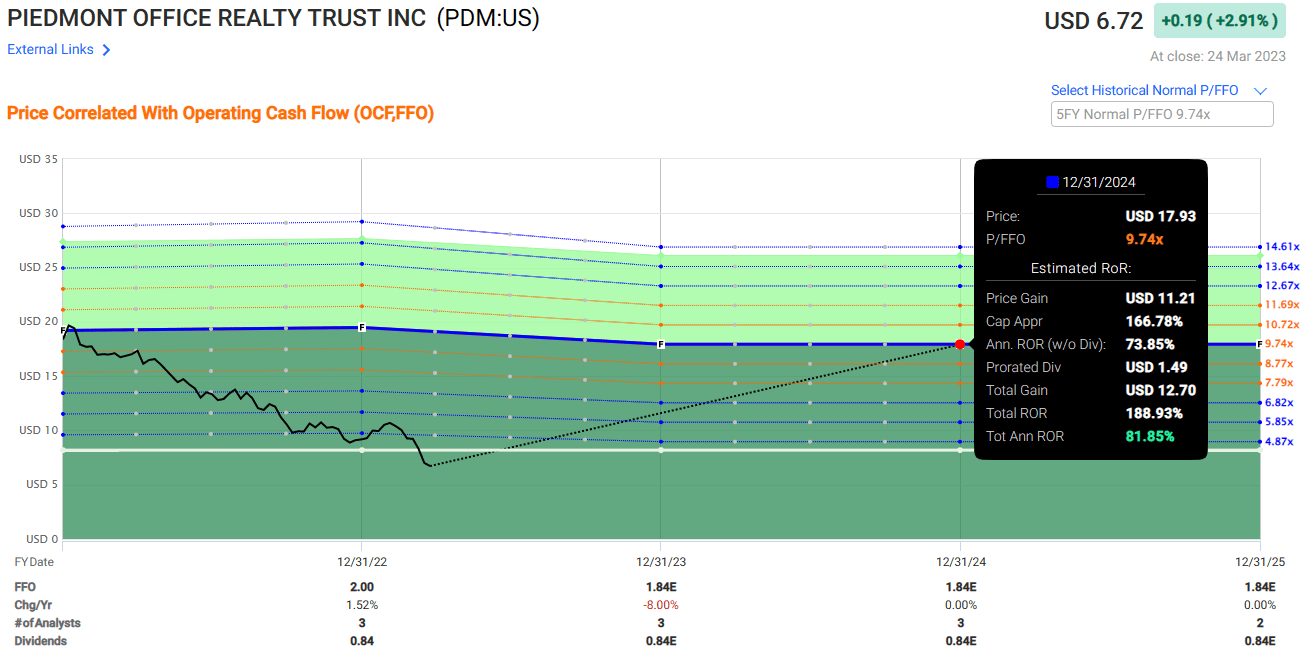

PDM is trading at a significant discount with a current p/FFO of 3.42x versus its normal 11x. It currently pays a dividend yield of 12.5% that still manages to be well-covered with an AFFO payout ratio of 60.22%.

- iREIT maintains a Spec Buy with a total return estimate of 81.85% annually by 2024, assuming its p/FFO multiple reverts to its five-year average.

{kind=link}

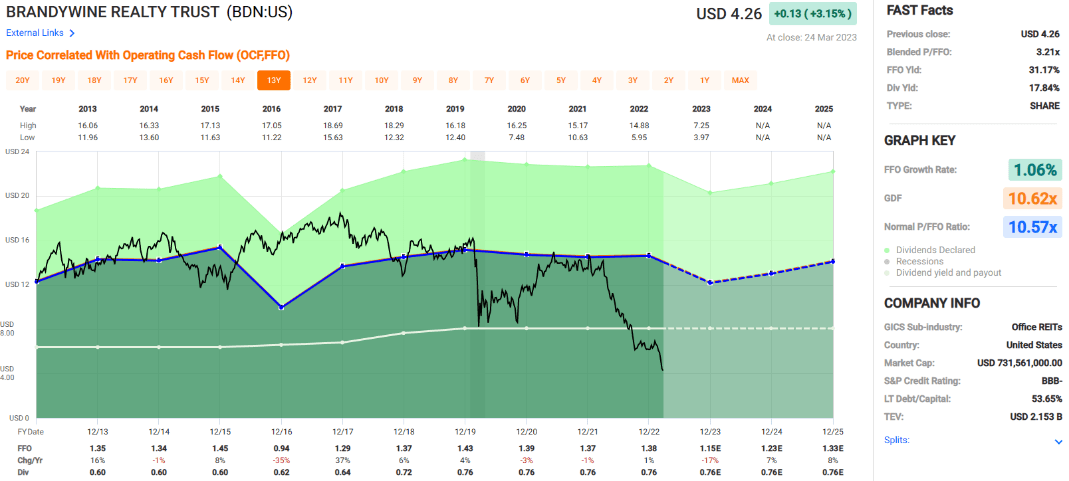

Take a Sip or Two of This Office REIT

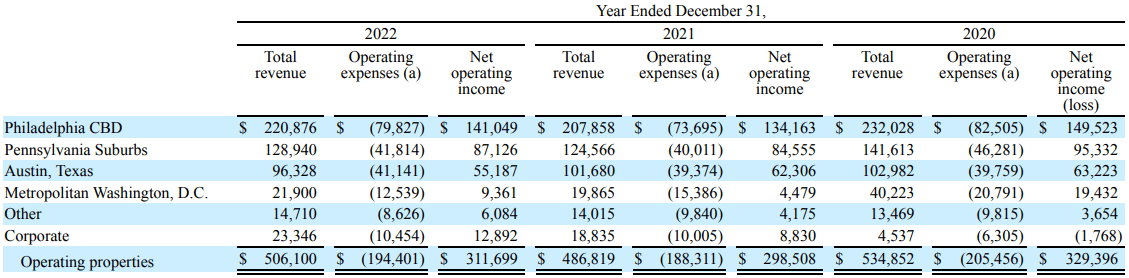

Brandywine Realty Trust ( BDN ) boasts a portfolio of mostly office properties but also some life-science, residential, and mixed-use assets as well. At year-end 2022, it owned 12.8 million net rentable square feet with an average occupancy rate of 89.8%.

BDN operates in five primary markets: the Philadelphia Central Business District ((CBD)) of Pennsylvania; Pennsylvania suburbs; Austin suburbs; Metropolitan Washington, D.C.; and elsewhere. As shown below, the majority of its revenue and net operating income ((NOI)) comes from Philly’s CBD, followed by the Pennsylvania suburbs and Austin. So perhaps this one is stretching it a little thin on the Sunbelt theme, but it does still have a presence there.

{kind=link}

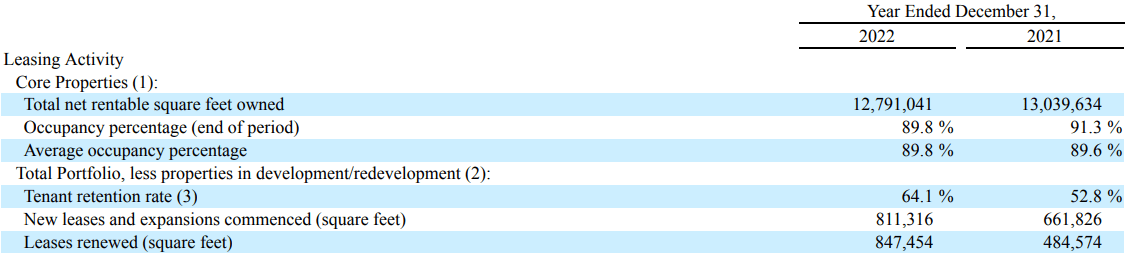

BDN’s leasing activity improved significantly year-over-year with a 64.1% 2022 total retention rate compared to 52.8% in 2021. New leases in 2022 totaled 811,316 square feet versus 661,826 in 2021. And leases renewed in 2022 came in at 847,454 square feet compared to 484,574.

{kind=link}

Brandywine has a compound dividend growth rate of 2.39% over the last 10 years, with no dividend cuts since 2013. Increases to that payout have been less impressive, admittedly.

It moved the dividend from $0.72 per share to $0.76 in 2019 but hasn’t raised it since. And analysts expect the dividend to remain at $0.76 on an annual basis until 2025.

BDN has averaged an FFO growth rate of 1.06% since 2013. That calculation is supposed to fall 17% in 2023 but then increase by 7% and 8% in 2024 and 2025, respectively.

{kind=link}

This office REIT has a reasonable balance sheet , rated BBB-, with a net debt to EBITDA of 7.2x and a fixed-charge coverage of 2.3x as of Q3-22. Its weighted average interest rate is 5% and a weighted average maturity of 4.8 years.

$54.3 million of principle matures in 2023, and the company has $17.6 million in cash and cash equivalents, with $505.2 million available to them under their unsecured credit facility.

{kind=link}

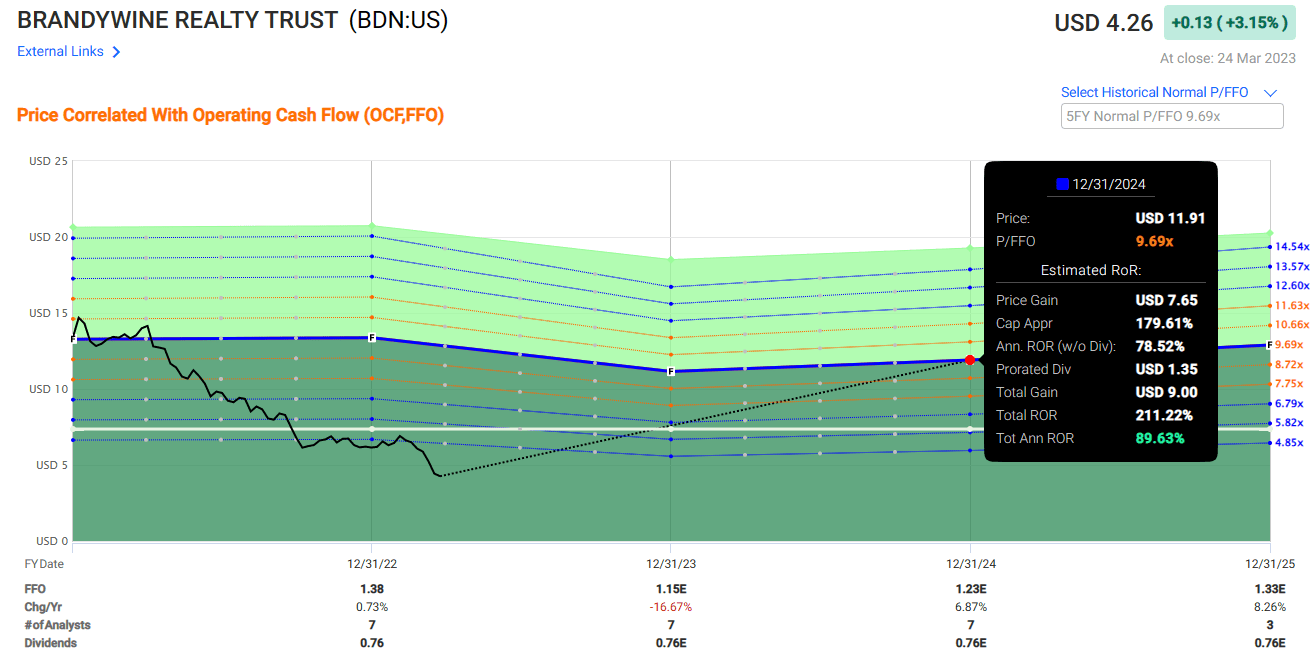

BDN is trading at a significant discount, with a current p/FFO of 3.21x versus its normal 10.57x. It currently pays a dividend yield of 17.84%, which is covered with an AFFO payout ratio of 84.44%.

iREIT maintains a Spec Buy , with a total return estimate of 89.63% annually by 2024 assuming that BDN’s p/FFO multiple reverts to its five-year average.

{kind=link}

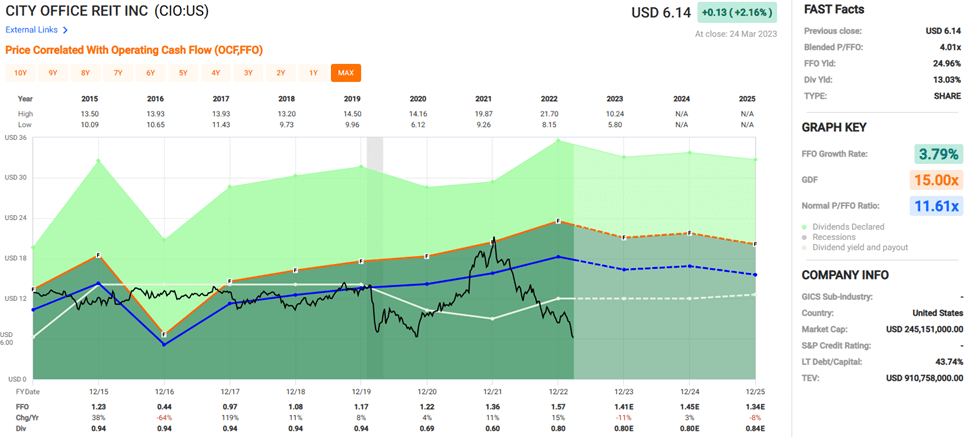

The City Isn’t Dead Yet Either

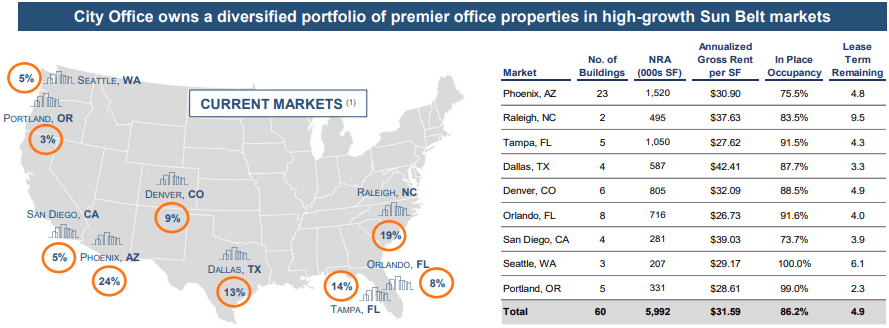

City Office REIT, Inc. ( CIO ) is an internally managed office REIT with properties predominately in the Sunbelt region. It owns 60 office buildings covering approximately 6 million square feet in Dallas; Denver; Orlando and Tampa; Phoenix, Arizona; Portland, Oregon; Raleigh; San Diego, California; and Seattle, Washington.

CIO has an 86.2% occupancy rate and a weighted average lease term of 4.9 years as of December 31, 2022.

{kind=link}

In 2022, it completed approximately 777,000 square feet of new and renewal leasing. This number is down from its new and renewal leasing of 1 million square feet in both 2021 and 2020. However, the 2022 numbers are up from its pre-Covid, 2019 levels of 692,000 square feet.

CIO Form 10-K (compiled by iREIT)

City Office REIT has a compound dividend growth rate of -2.28% since 2016. Its payout remained flat at $0.94 per share from 2015 to 2019 before being cut to $0.69 in 2020 and then cut again to $0.60 in 2021.

In 2022, CIO did increase that incentive by 33.33% to $0.80 per share, which is encouraging. Then again, it’s still not the $0.94 it used to be at. Analysts expect the dividend to remain flat both this year and next and then increase to $0.84 in 2025.

CIO has averaged an FFO growth rate of 3.79% since 2015. Analysts expect FFO to fall 11% in 2023, increase 3% in 2024, and then fall 8% in 2025.

{kind=link}

However, the company has a decent balance sheet with a net debt to annualized adjusted EBITDA of 6.4x and a long-term debt to capital of 43.74%. Its weighted average interest rate is 4.4%, and 90% of its debt is fixed rate. Most of the debt is secured, which Dane Bowler pointed out in a recent article .

Additionally, it has a weighted average maturity of 3.2 years, with minimal debt maturities in 2023. CIO has $28 million of cash and cash equivalents, and over $100 million available under its revolving line of credit.

{kind=link}

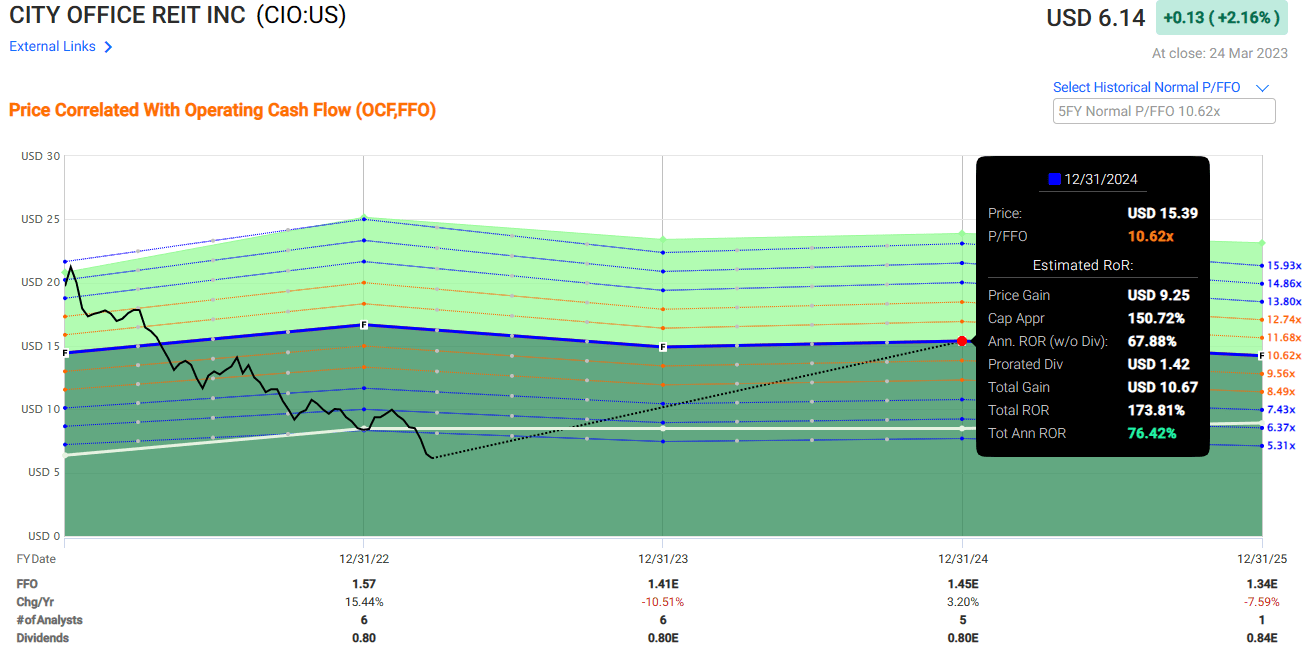

The REIT is trading at a significant discount, with a current p/FFO of 4.01x versus its normal p/FFO of 11.61x. It currently pays a dividend yield of 13.03%.

Somewhat concerning – and therefore something to keep an eye on – is its payout ratio. CIO has consistently paid more in dividends than its earnings ((AFFO)). It’s been over 100% each year since 2016, with the exception of 2021 when it came in at 71.43%. In 2022, CIO’s AFFO payout ratio was 119.40%.

iREIT maintains a Spec Buy with a total return estimate of 76.42% annually by 2024, assuming that its p/FFO multiple reverts to its five-year average. That’s a very generous and optimistic assumption and we’re taking a more conservative approach – adding CIO to our dividend cut watch list .

{kind=link}

An Office REIT That Could Treat You Like Family

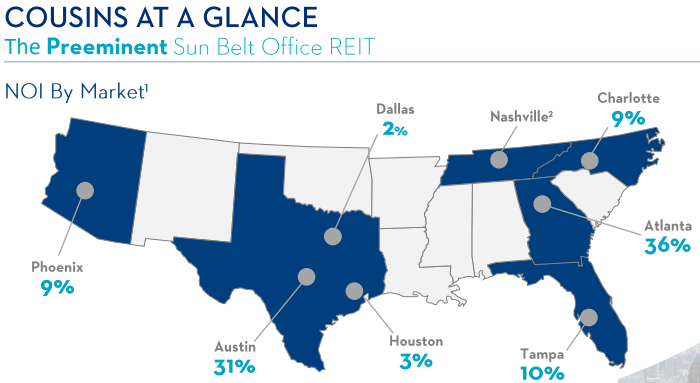

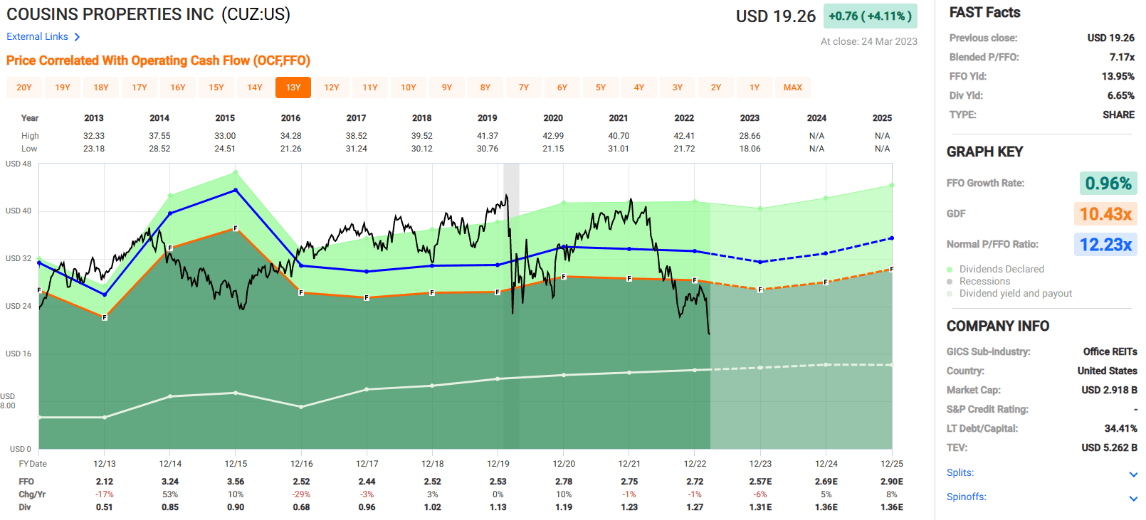

Cousins Properties Incorporated ( CUZ ) is a Sunbelt focused office REIT with properties in Austin and Dallas, Tampa, Phoenix, Charlotte, and Nashville. But its largest market is in Atlanta, which accounts for 36% of net operating income ((NOI)).

Austin is its second-largest at 31%, followed by Tampa at 10%.

{kind=link}

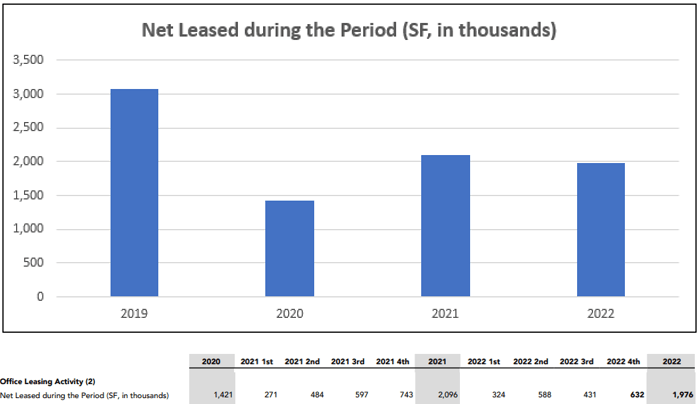

As of the fourth quarter of 2022, CUZ had 36 total operating properties covering 19.1 million rentable square feet with a weighted average occupancy rate of 86.6%. And in 2022 alone, it executed 1.9 million square feet of office leases.

CUZ’s leasing activity did drop significantly from 2019 to 2020. Net leased volume (measured by square feet) increased in 2021 and then slightly decreased in 2022. In all, while it’s improved from its 2020 low of 1.4 million square feet, it’s still well under its 2019 levels of 3 million.

CUZ Investor Presentation (compiled by iREIT)

{kind=link}

With that said, Cousins Properties has had a compound dividend growth rate of 9.59% since 2013. The dividend was cut in 2016 from $0.90 to $0.68, but it’s increased each year since to $1.27 per share as of last year.

Analysts expect the dividend to increase to $1.31 in 2023 and to $1.36 in both 2024 and 2025.

CUZ has averaged an FFO growth rate of 2.78% since 2013. And while FFO will likely fall 11% this year, it’s expected to increase by 10% and 6% in 2024 and 2025, respectively.

{kind=link}

There’s some iffy information for this REIT, I recognize. But its balance sheet is strong with a net debt to annualized adjusted EBITDAre of 4.93x and a fixed-charge coverage ratio of 5.21x. It has a weighted average interest rate of 4.48% with a weighted average maturity of 3.9 years, while 79% of its debt is fixed rate.

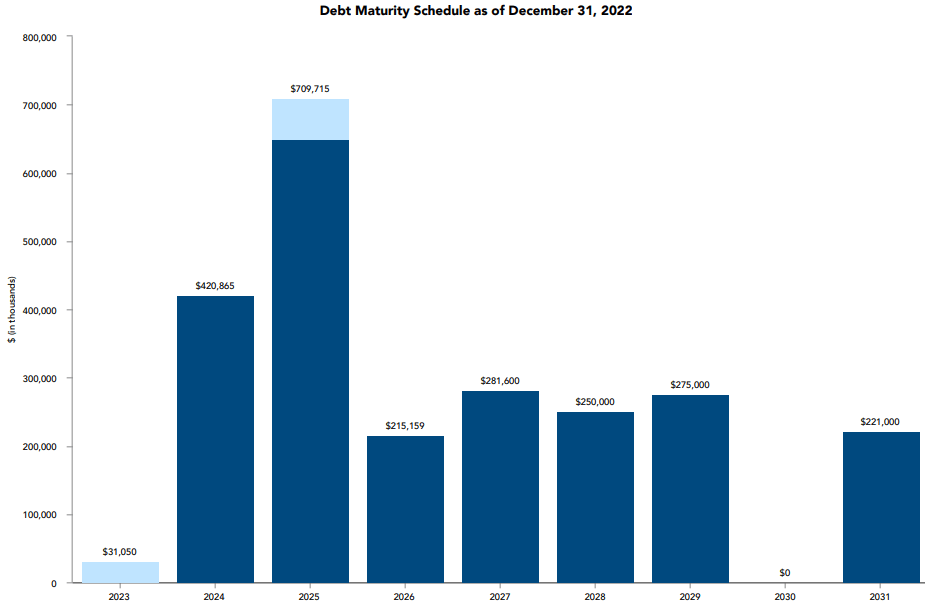

Additionally, CUZ has $949 million in liquidity with no major maturities until 2024.

{kind=link}

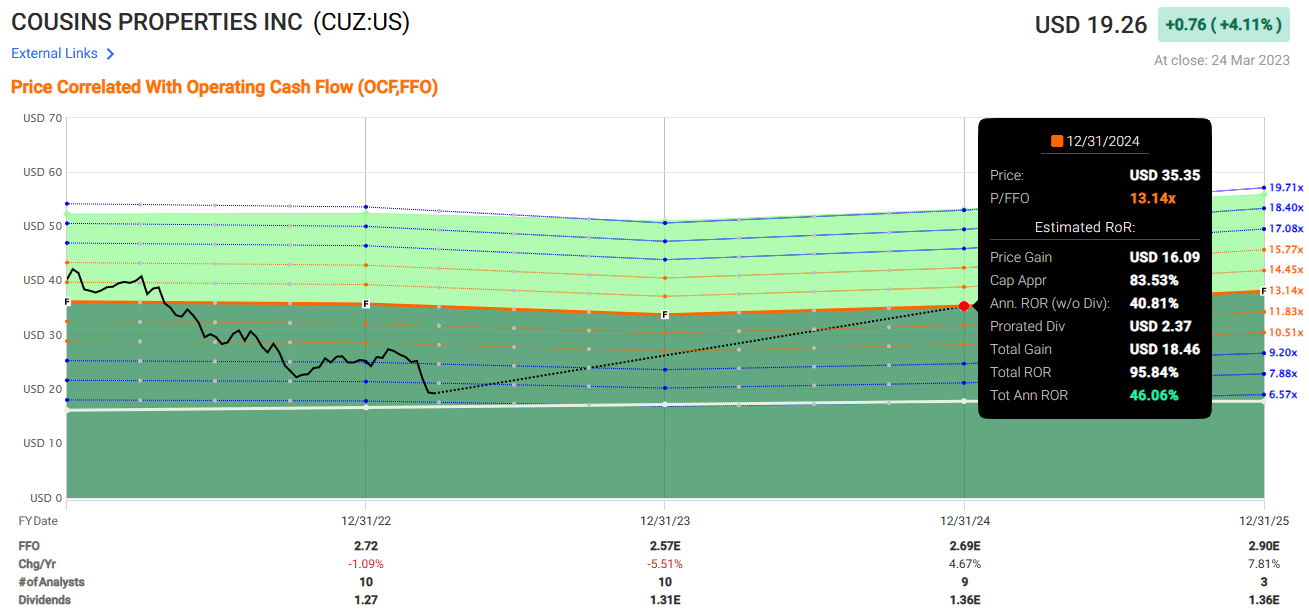

Cousins Properties is trading at a significant discount, with a current p/FFO of 7.17x vs its normal 12.23x. It currently pays a dividend yield of 6.65% that’s well covered with an AFFO payout ratio of 69.40%. iREIT maintains a Spec BUY with a total return estimate of 46.06% annually by 2024 – assuming its p/FFO multiple reverts to its five-year average.

{kind=link}

In Closing…

A few days ago I covered NYC office REITs , and in this article I highlighted five sunbelt plays.

Next I’ll be working on a few more specialized office REITs including Boston Properties ( BXP ), Alexandria Real Estate ( ARE ), Kilroy Realty ( KRC ), Orion Office ( ONL ), and Easterly ( DEA ).

As always, thank you for reading and I look forward to your comments below.

Happy SWAN Investing!

For further details see:

Office Isn't Dead, Especially Those Soaking Up The Sunbelt