OPINL - Office Properties Income Trust And Diversified Healthcare Trust Merger: A Bondholder's View

2023-04-21 00:35:29 ET

Summary

- Last week, Office Properties Income Trust and Diversified Healthcare Trust announced an all-stock merger.

- As an Office Properties Income Trust bondholder, I wanted to see what the merged companies looked like on paper.

- Free cash flow and liquidity remain concerns for the combined company.

Last week, Diversified Healthcare Trust ( DHC ) and Office Properties Income Trust ( OPI ) announced an all stock merger . I'm familiar with both companies since I have held Office Properties bonds and advised investors to avoid Diversified Healthcare Trust debt . Since I held Office Properties' debt, I decided to analyze what the combined companies would look like to see if my investment was safe.

In terms of profit and loss, Diversified Healthcare's revenue and expenses will make up 70% and 76% of the combined company, respectively. Office Properties' $111 million in operating income is going to be combined with Diversified Healthcare's $93 million operating loss to create a company that has a 1% operating margin. The profitability (or lack thereof) is not nearly enough to cover the $313 million in interest expenses.

TIKR data uploaded into spreadsheet

On the balance sheet side, Diversified Healthcare Trust brings 60% of the total assets and 56% of the liabilities into the combined company. What's interesting for Office Properties stakeholders is that the combined company will have a lower leverage ratio than Office Properties standalone entity. This is because Diversified Healthcare's leverage ratio is close to 1.2 to 1 while Office Properties is nearly 2 to 1. The combined entity will have a book value of over $4 billion and have a leverage ratio of approximately 1.5 to 1.

TIKR data uploaded into spreadsheet

For bondholders, the cash flow statement is essential to understanding whether a company's debt is a good investment or not. The cash flow statement highlights whether a company can generate enough cash from day-to-day operations to support capital expenditures and ensure that it won't need to acquire additional debt to do so. Ideally, free cash flow (cash flow from operations minus capital expenditures) is strong enough to pay off some debt.

In this case, Diversified Healthcare Trust is currently burning cash on a day-to-day basis and, after capital expenditures, has a free cash flow burn of approximately $400 million over the last twelve months. The combined company sold $843 million in assets, but it cannot sell assets in perpetuity to cover free cash flow deficits. Additionally, there are $116 million in dividend obligations, mostly from Office Properties Trust high yielding dividend, but Office Properties is poised to address some of this.

TIKR data uploaded into spreadsheet

Shortly after the proposed merger, Office Properties Trust announced a 55% decrease in its dividend from 55 to 25 cents per share . However, the reduction is not linear because new shares are being issued to account for the Diversified Healthcare shareholders. Diversified Healthcare has 240 million shares, equating to 35.28 million new shares of Office Properties Income Trust. Combined with the existing 48.5 million shares, investors can expect approximately 73.78 million outstanding shares after the merger. This would reduce the dividend obligation from $116 to $74 million annually.

Approximate cash flow statement after dividend cut (TIKR data uploaded into spreadsheet)

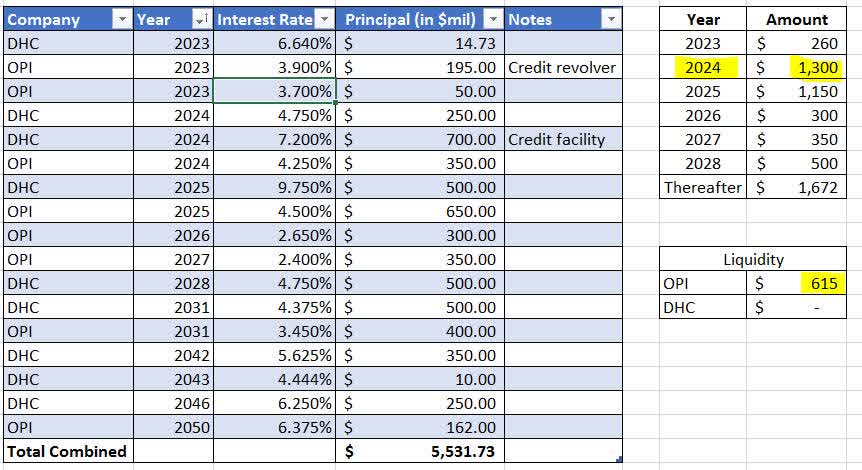

Despite the dividend improvement, the combined company is on track to burn nearly $500 million in negative free cash flow during its first twelve months. Even more troubling is that Diversified Healthcare is entering into this merger with no borrowing capacity. Office Properties' $615 million in liquidity is hardly enough to cover the $1.3 billion in debt coming due next year for the combined company.

{kind=link}

Due to these circumstances, I see a credit downgrade as not only likely, but possibly into the CCC rated arena as Diversified Healthcare currently holds that rating and credit rating agencies are getting uncomfortable around office REITs. This turns my holding of Office Properties bonds from being undervalued to fair valued with future downside more likely. As a result, I have sold my Office Properties Trust debt and am advising investors to avoid both the company's stocks and debt.

For further details see:

Office Properties Income Trust And Diversified Healthcare Trust Merger: A Bondholder's View