ARE - Office REITs For 2024 - The Upside After The Fact

2024-01-07 22:51:35 ET

Summary

- I have been investing in Office REITs and have seen positive returns on their picks.

- The recent surge in rate-related and macro-related factors has changed the upside potential for these REITs.

- While there is still appeal in investing in Office REITs, the best upside has passed, and valuations have become less attractive.

Dear subscribers,

I've been fairly clear in the last few months about the fact that I'm going into Office REITs, and my three picks of Highwoods ( HIW ), Kilroy ( KRC ), and Boston Properties (BXP).

My shares were bought at a mix of valuations, but one thing they all have in common after the last few days is that they're all firmly in the green. Also, the fact that none of the companies mentioned are any longer at what I would consider their "bottom".

The latest few days of rate-related and macro-related surges have resulted in a very much changed upside for many of these REITs.

Of course, at the same time, I've seen over the past few days, in comments and in suggestions, that now might be the time to invest in these office REITs.

What?

This article seeks to offer suggestions and some guidance, for investors who are looking to learn something about valuation and strategies that can be applied to most investors looking to beat the market using fundamental strategies.

Office REITs - why I've outperformed, and why I'm not selling (yet)

I have written no less than ten articles on the aforementioned companies during 2023 in a mix of singular and multi-company articles where I have, time and time again, called these companies to be worth buying. While it's true that I've always been clear about the risks and will continue to be this here - remember, we're talking about office space , the false equivalency that many investors have fallen to here is that because offices are seeing a downturn, all office property companies should be avoided.

I am hoping that the past few days have shown you, if you've avoided these investments like many seem to have done, that this is not the case and how much of the undervaluation was perceived rate risk to the companies in question.

Is the risk over?

No, I would argue that the fundamental risk to these companies is virtually unchanged since my last set of articles for them. The market may believe itself to have better visibility for 2024, but:

- These company fundamentals have not changed.

- Their credit rating has not changed.

- Their dividends have not changed

- Their management has not changed.

What has changed is market perception. And as you've seen over the past few days, if you miss out on these few up-days, then you miss out on a whole lot of growth. Many of the office companies in question, where I have secured yields of over 7.5% on cost , are now yielding less than 5.5-6%.

Not only is this materially deteriorated from their previous, appealing valuations during troughs, but it's at a level where I would argue that there are companies with better upside here.

Let me name a quick example.

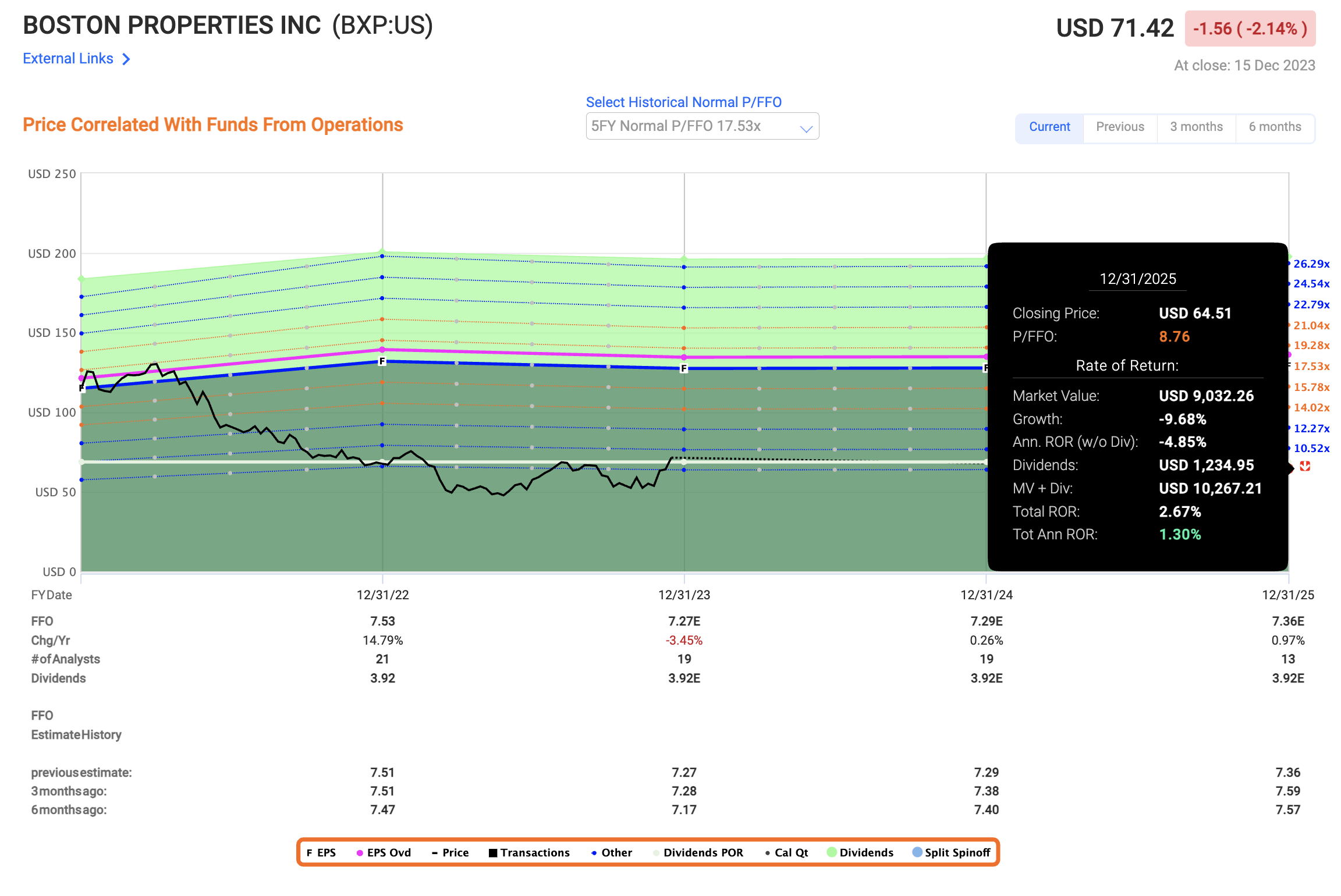

On the one hand, I have Boston Properties - a great, BBB+ rated office rate. At the trough, it yielded over 7% and I could see a conservative upside of 25% annually, by which I mean an upside to less than 8.7x P/FFO even with a growth of nearly 0% until 2025E. At a 25% upside, this was a great potential - but now the potential to that 8.7x is like this.

F.A.S.T Graphs BXP Upside (F.A.S.T Graphs)

{kind=link}

While the company could go higher, we also need to estimate where this company could go, and how high it could go given the growth rate the company is forecasted.

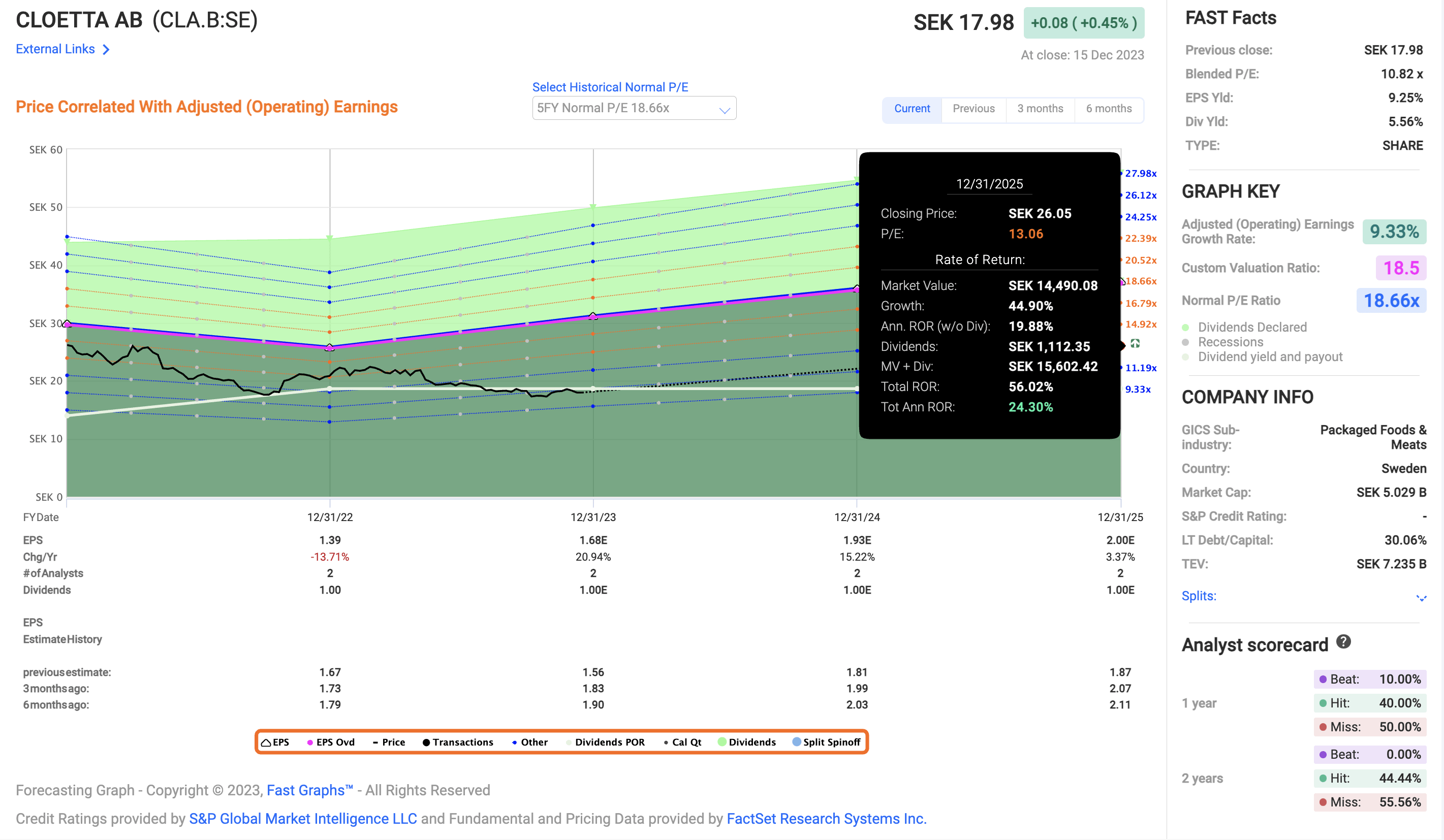

And then compare it to something like Cloetta ( OTCPK:CLOEF ). This is a Swedish candy and food company yielding more at 5.56%, with an upside to a conservative 13x P/E that looks like this.

F.A.S.T Graphs cloetta upside (F.A.S.T graphs)

{kind=link}

So you can see how a company's appeal on the broader market is dependent on a multitude of factors, but all things being equal, valuation is the key deciding factor. So if choosing between these two companies today, and if I didn't have full exposure to Cloetta AB, that's what I would add to my portfolio.

The latest few days have really pushed all of these REITs, especially those that have been significantly undervalued, to levels where they might no longer be that appealing if we assume that a zero-growth estimate results in pressured multiples for the next few years.

As I've been saying in my past articles, these office REITs have been undervalued for a very long time, and despite pressured growth rates and refinancing risks, all of them have also shown continued strong demand for their properties - and we're not even talking about Alexandria ( ARE ) here, the REIT that has been done best by far, with RoR of over 30% since my investment.

In this article, I want to clarify where I see the appeal for Office REITs like BXP, HIW, and KRC after this recent surge.

I want to clearly state that there is continued appeal in investing here , but want to make it equally clear that the best upside has now passed.

I'm talking about the upside to a 7-9x P/FFO for these REITs of over 20%. In order to get those rates of return now, you need to actually estimate these REITs trading at double-digit multiples, in the case of KRC, almost above 11x to get a 15% annualized RoR here. (Source: F.A.S.T graphs)

These are not outlandish demands or projections - not when you consider that KRC for instance, manages a historical premium of almost 18x P/FFO.

But is that premium likely in a world of a 4-5% risk-free rate when the company is forecasted, with 100% accuracy, to grow earnings at negative amounts for the next few years?

While all of the office REITs have seen a resurgence, and all of their quarterly reports and releases show operational stability that would deny any sort of fundamental decline firmly, all of the forecasts are very clear in one matter.

Any sort of FFO/AFFO growth in the next few years will be small, if not slightly negative. And while you may generate double-digit returns, those returns become less and less appealing the higher these stocks go.

That's why I keep a very close eye on quality stocks - like these office REITs - and once they actually go lower, I buy more.

When Alexandria hit double digits, that's when I really dialled up my buying. Alexandria represents the single largest office REIT in my portfolio and over 1% of my current total, both privately and commercially for a very specific set of reasons.

Take my criteria as an example.

- Alexandria is BBB+ rated.

- Alexandria's dividend is extremely well-covered.

- Alexandria, unlike these other REITs, is estimated to grow at 4-5% FFO annually.

- Alexandria has a historical 10-year 100% forecast accuracy (Source: FactSet)

- Alexandria is a bit more specialized in terms of the office sub-sectors and is unlikely to see a significant decline even in a hard market environment.

All of the other office REITs have appeal as well - and are cheaper - but none are as qualitative, and I first and foremost focus on quality.

Let's look at what sort of buying appeals these REITs still have today.

Valuation for KRC, HIW, BXP (And ARE).

We now enter what I view as a period to be more careful. I view valuations for many companies at their peak, or at record levels. I maintain a large list of companies that I cover together with price targets, and I have rarely seen so few worth buying as I am seeing today. The potential for companies to "drop" back down seems higher at this time.

That being said, if you want to invest in Office REITs now, it's not "too late", provided you moderate your growth assumptions.

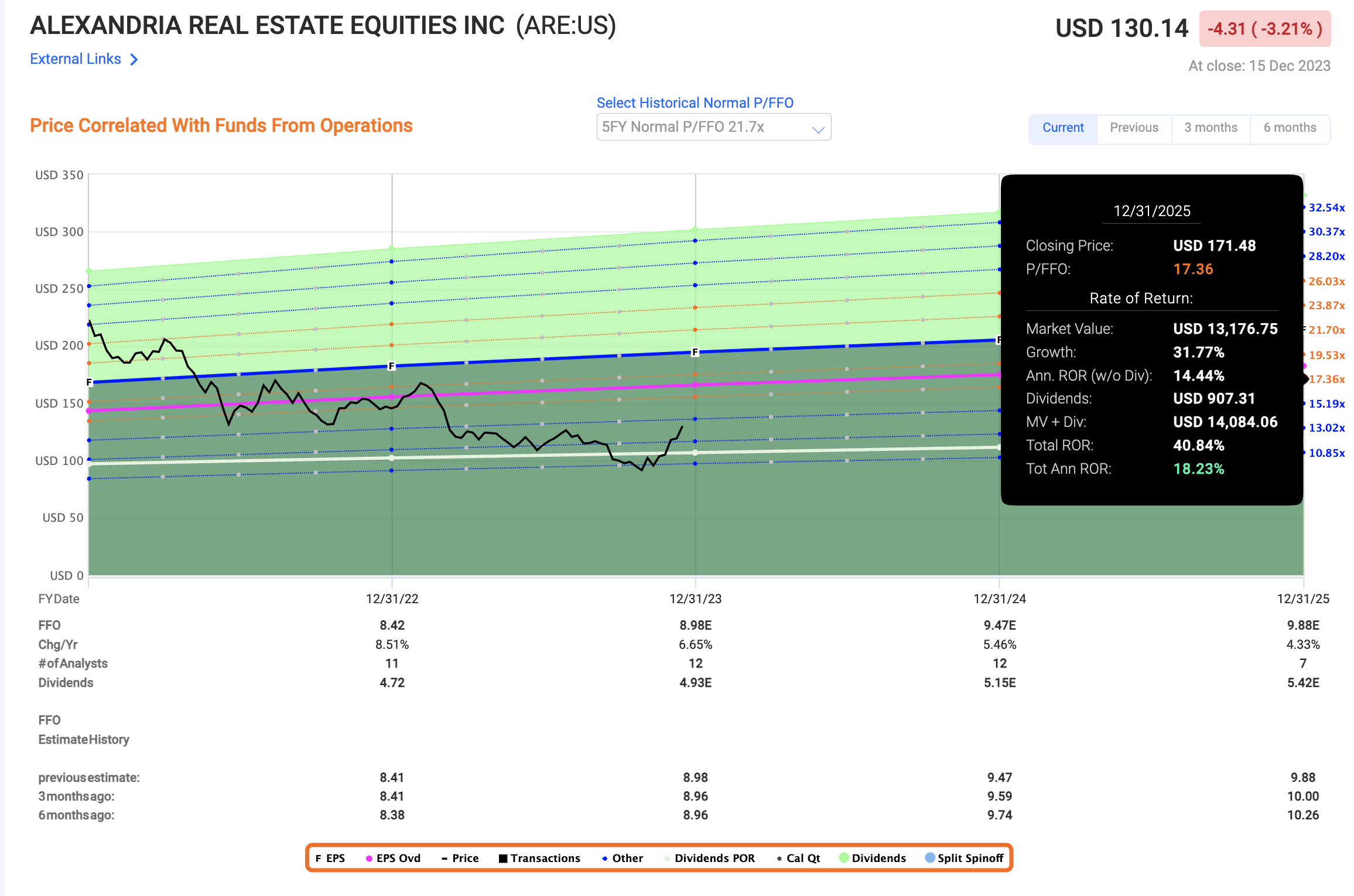

Less than 2 weeks ago, you could get 20%+ annualized RoR if forecasting ARE below 15x P/FFO. Today you need to forecast it at 16-17x P/FFO to get above 15% per year and only a yield of 3.9% instead of almost 4.5%. The current share price isn't unattractive, and I still consider ARE to be a "BUY", with the following realistic upside.

{kind=link}

This is the highest-quality office REIT upside, and I refer you to my other articles to understand why this isn't your typical office REIT.

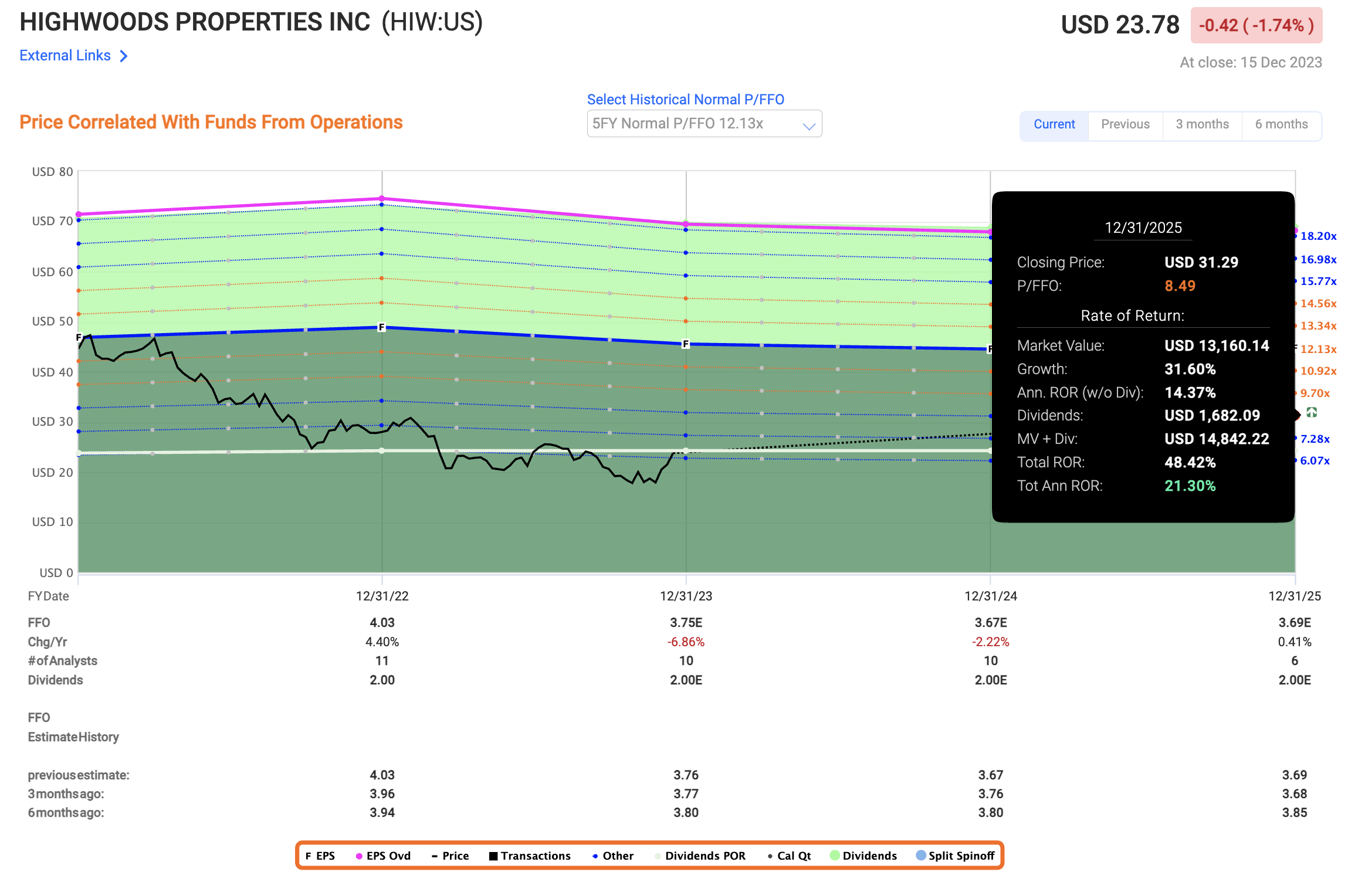

Out of the other REITs here, they now trade at a mix of valuation multiples - usually related to fundamentals and growth prospects. Highwood is by far the cheapest of the bunch, currently still at an 8.4%+ yield, but the REIT is also the one that's expected to decline over 1% per year, making an upside to any significantly "high" multiple less likely than the others.

I still consider Highwood a "BUY" here, but only to a 7-8x P/FFO, at most 8.5x. And to an 8.5x, this company still manages around 21% annually - though again, we're talking about investing in a company that seems likely to decline, which puts a question mark on any upward trajectory it might have.

{kind=link}

A similar case is true for Boston properties - though this is the one office REIT I cover here, except Alexandria, that's expected to grow FFO. Even if that growth is only 0.5% per year. However, as a result, the company is close to 10x P/FFO here compared to HIW, and you need to estimate it at 12.5x to get even 17% per year.

My point here is that these rates of return are quite good, but nowhere near as good as they once were only 2-3 weeks back, or months back.

My point is that entire sectors or subsectors sometimes, irrationally, trade down for extended periods, and this is the time to invest in them - not when they've already recovered over 10-18%, which is what has happened only in the past 1-2 weeks.

It requires identifying what I consider to be fundamentally sound businesses. You may see that I've not covered businesses I consider riskier all that much, but instead focus on the BBB-rated or above companies, where any fundamental decline over the long term seems quite far off. While I do own a stake in Medical Properties Trust ( MPW ), for instance, that stake is extremely small - and while I do view it as a "spec" buy, this is a business that while yielding 11%, is also estimated at growing FFO negative 6% or less yearly in the next few years. Couple this with some management issues, and I'm clear why I am not going as deep as in the companies that I have mentioned here.

My point here is, be aware of valuation

My point is that I am constantly looking out for the best valuation and fundamental-related upsides, and while Office REITs are still good picks here, their risk profile has not, at least to my mind, materially improved or declined. The market's view on them has. However, this recent surge has made other options far more interesting - as I showed you with my example for Cloetta. There are perhaps 15-20 undervalued companies that I would say have less of a negative interest rate risk than these REITs do, and these have all become much more interesting to me after the past few weeks.

As we're moving toward the end of 2023, I think it's important to be realistic about what 2024 could bring. While we might see a continuation of the positive development we've seen so far, I prefer to err on the side of caution here and expect a far more sobering experience for the coming investment year.

That's why my battle cry for 2024 will be centered around picking only the most qualitative but undervalued equities to invest in - companies with high outperformance potential even in the case of sub-par development.

If you missed out on investing in these 4 companies at trough valuations, then I am hoping that my articles for the remainder of 2023 and going into 2024 can provide you with qualitative ideas for where one could put one's money for the short, medium or longer-term.

I'll continue to provide conviction here, in the sense that I very, very rarely write about companies I have no "skin in the game in", and make it very clear where I see the risk-reward ratio.

For now, this is what I see for the Office REITs that I cover here. I consider them "BUY" still, but their appeal has materially changed from only a few weeks back.

For further details see:

Office REITs For 2024 - The Upside After The Fact