PDM - Office REITs Look Cheap But There Could Be More Pain Ahead

Summary

- Office REITs were battered by the pandemic, and some are offering attractive yields.

- 2022 was supposed to be a year of recovery for office REITs but that hasn't materialized.

- America now has a glut of office space driven by hybrid working strategies and growing layoffs. There is likely to be more pain ahead.

- Although new office construction has slowed, it would take time for the market to rebalance.

- More medium term pain could impact earnings and underlying property values, ultimately affecting stock prices.

Beaten-down office REITs are getting investor attention with enticing yields and low stock prices. But more pain ahead means further capital losses cannot be ruled out.

America has a glut of office space and a rebalance could be years away

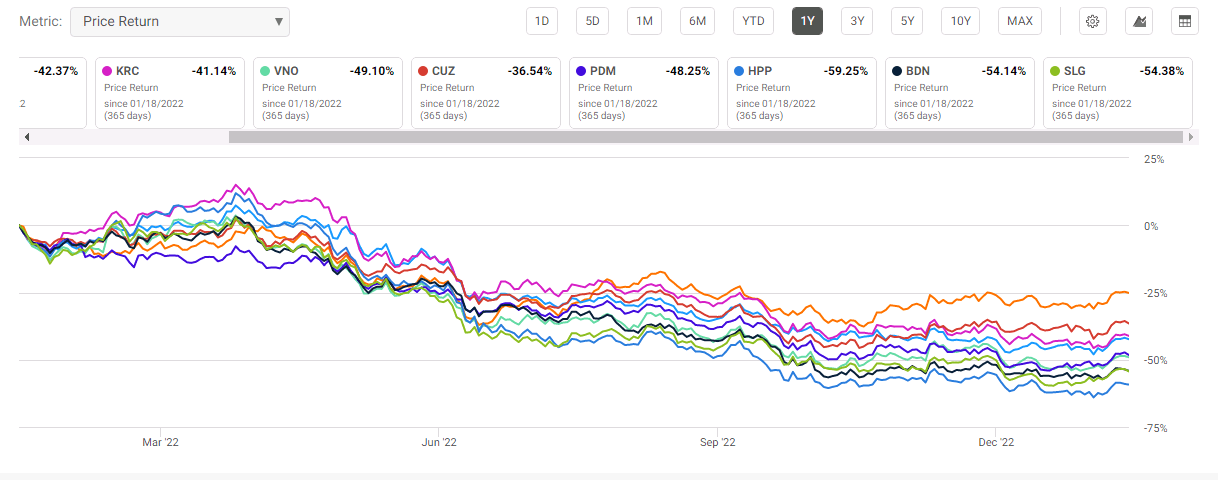

2022 was expected to be the year employees return to work and office demand normalizes, but instead, rising interest rates and an anticipated recession along with hybrid working becoming the norm have kept America's office vacancy rates at record highs , crimping investor demand for office REITs amid concerns over the near term and long term demand for office real estate in the U.S. Office REITs have been particularly hard hit relative to other real estate categories.

S&P Global

After significant stock declines over the past year, office REITs are trading at attractive yields, attracting investor attention in the process.

{kind=link}

{kind=link}

Office REITs' dismal performance is not surprising considering America now has a glut of office space with vacancy rates running at around 19% nationwide, a record high, and office occupancy is only about half of pre-pandemic levels.

Looking ahead, America's office sector is likely to see continued weakness; the country's blossoming tech industry, at one time a major source of demand for office space, is now scrambling to cut costs through employee layoffs and streamlining office footprints as investors, increasingly conservative due to rising interest rates, turn away from unprofitable, risky tech investments. Office vacancy rates are particularly high in America's tech hubs such as California, which has an office vacancy rate of 26% , a 30-year-high.

Yet with inflation at 6.5% (which although considerably improved from a few months ago, remains far away from the Fed's 2% target), further interest rate hikes are expected in 2023 which could lead to millions more layoffs, not just in the relatively more vulnerable tech sector but in other industries as well including fashion , finance , and food service. Goldman Sachs ( GS ) is laying off 3,000 workers (the largest since the 2008 financial crisis), Coinbase ( COIN ) laid off another 20% of employees this year, McDonald's ( MCD ) CEO says layoffs are coming, Bed Bath & Beyond ( BBBY ) is planning more layoffs. Layoffs are likely to drive further office downsizing as well, significantly impacting demand.

While it could be hoped that a looming recession could swing the Fed towards an accommodative monetary policy, which could potentially reinvigorate workforce expansion and therefore office demand, hybrid working appears to be here to stay, a significant structural change that is likely to delay any rebalancing in America's office supply and demand.

About 25% of American employees are working remotely, compared with around 6% pre-pandemic. That would suggest around 1 billion sq ft of the total 4 billion sq ft of total office space being redundant in the U.S., a significant figure. For perspective, the country added around 682 million sq ft of office space over the ten years until pre-pandemic year 2019 according to some estimates.

Commercial Cafe

On the supply side, new office construction has already been slowing and with interest rates expected to remain elevated for 2023, construction activity could continue to drop.

Statista

But this alone is unlikely to be sufficient to address the glut. Older, low-grade buildings which tend to have higher vacancy rates could be converted into other developments thereby reducing office supply, but this too is proceeding at a snail's pace with high interest rates and high construction costs delaying conversion projects; just 2% of America's offices are scheduled for conversion, far lower than the country's current office vacancy rate of 19%, and far short of the current occupancy rate of around 50%. Absorbing America's excess office space is thus likely to take years, barring any unforeseen events that would bring employees back to office. Even if they do, this is likely to take time, as with inflation running high and interest rates marching upwards, employers may actually encourage remote working arrangements to cut costs, particularly in states with the highest office rents nationally such as New York and California. A survey by EY revealed that 90% of tech business leaders say that remote work can help them save money, and 70% of them are doubling down on investing in remote work.

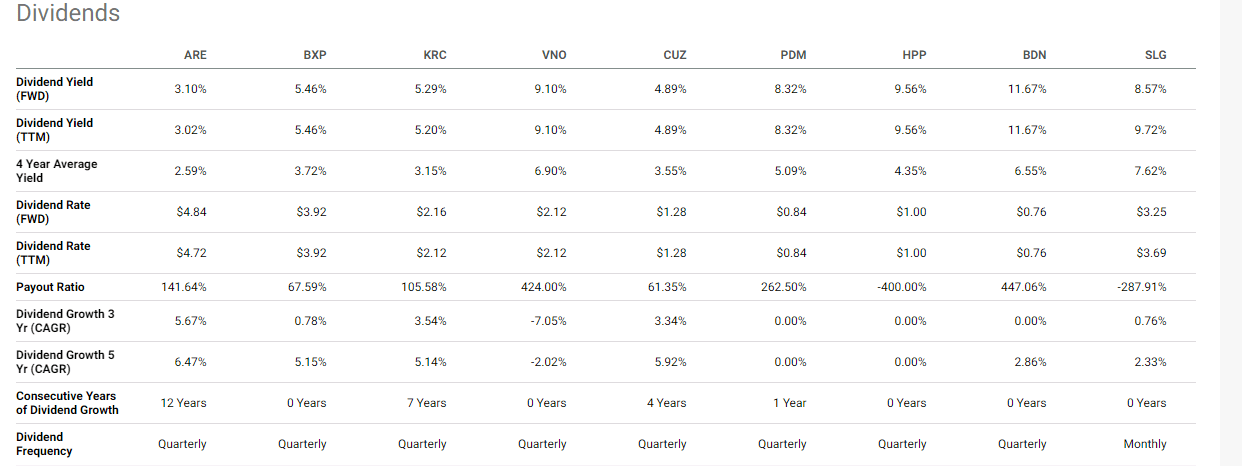

Leased rates are currently quite strong for office REITs but they have been declining. Piedmont Office's ( PDM ) leased rate of 86% in 2021 is down from 91.2% in 2019. Boston Properties' ( BXP ) leased rate of 88.8% in 2021 is down from 93% in 2019. Brandywine's ( BDN ) leased rate of 92.7% in 2021, is down from 95.5% in 2019. Kilroy Realty's ( KRC ) leased rate of lease rate of 93.9% in 2021 is down from 97% in 2019. SL Green's ( SLG ) leased rate of 91.6% in 2021 is down from 94.3% in 2019 . Hudson Pacific Properties' ( HPP ) 92.8% leased rate in 2021 is down from 95.1% in 2019 . Cousins Properties' ( CUZ ) 91.6% leased rate in 2021 is down from 93.6% in 2019.

Looking ahead, as tenants downsize, leases coming up for renewal this year and thereafter may not be renewed or tenants may opt for smaller office sizes, impacting leased rates. The market's shift to favoring tenants could also impact landlord negotiating power and pressurize rents in the process, and therefore affect earnings and potentially dividends as well. Meanwhile, falling yields could impact office real estate valuations. A study by business professors from Columbia and New York University projects the value of U.S. office buildings could plunge 39% in the coming years. A drop of this magnitude could be detrimental to balance sheets and could be disastrous for players with weaker balance sheets.

Overall, office REITs have already been battered but with trends pointing to further pain ahead, further declines to stock prices cannot be ruled out.

Longer term, the market should rebalance, but this is likely some time away

Longer term, high construction costs and difficulty securing loans could keep new office supply low. Meanwhile, the market is likely to consolidate through asset sales and exits, and this process could accelerate if office property values drop.

On the demand side, remote working meanwhile may actually moderate as disadvantages including running costs and overlooked promotion opportunities, alongside a weakening labor market driven by a slowing economy, could jolt some workers to return back to office.

It remains to be seen when the market will rebalance, and it is impossible to precisely time when this would materialize. But at the moment, there are few indications, if any, that a state of stability will be reached anytime soon.

Conclusion

Real estate is entering a downcycle and office REITs which have seen significant drops in share prices now look cheap with 5%-10% yields. But with America's office real estate market seeing fundamental alterations in market demand there is likely further medium-term pain ahead with downward pressure on rents, lease rates, and therefore asset values likely to impact earnings and stock prices medium term.

For further details see:

Office REITs Look Cheap But There Could Be More Pain Ahead