VRE - Office REITs: Pain Is Priced In

Summary

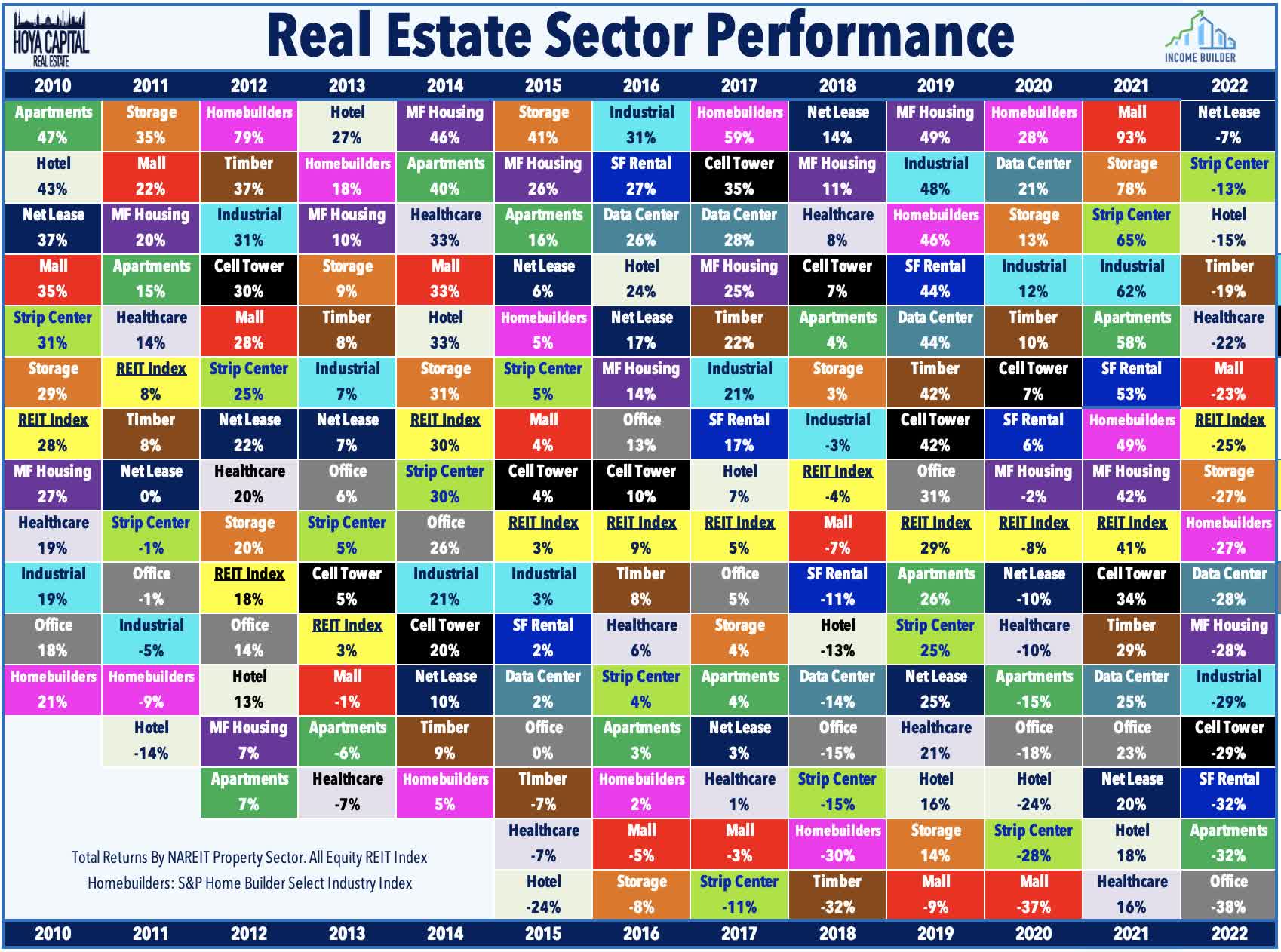

- Office REITs have been far-and-away the worst-performing property sector since the start of the pandemic, as depressed utilization rates and recession concerns have curbed office space demand.

- Work-From-Home-Forever? Occupiers due for renewal have been somewhat-reluctant to cut office space, with leasing volumes still at 75% of pre-pandemic levels, but fundamentals softened more definitively in late 2022.

- Elevated supply growth isn’t helping either, resulting in record-high vacancy rates and giving occupiers ample negotiation power to extract reduced rents and concessions - worse in urban markets with long commutes.

- Workers hate commuting, not the office. As employment markets normalize from historic tightness, utilization rates should recover to around 60% in urban metros and 80% in secondary markets – up 20% from current levels - likely a more optimistic view than market consensus.

- How much is priced-in? With Office REITs trading at historically deep discounts to peers in public and private markets – and average dividend yields near 6% - there appear to be some emerging pockets of value in REITs focused on secondary and tertiary markets.

REIT Rankings: Office

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on February 3rd.

{kind=link}

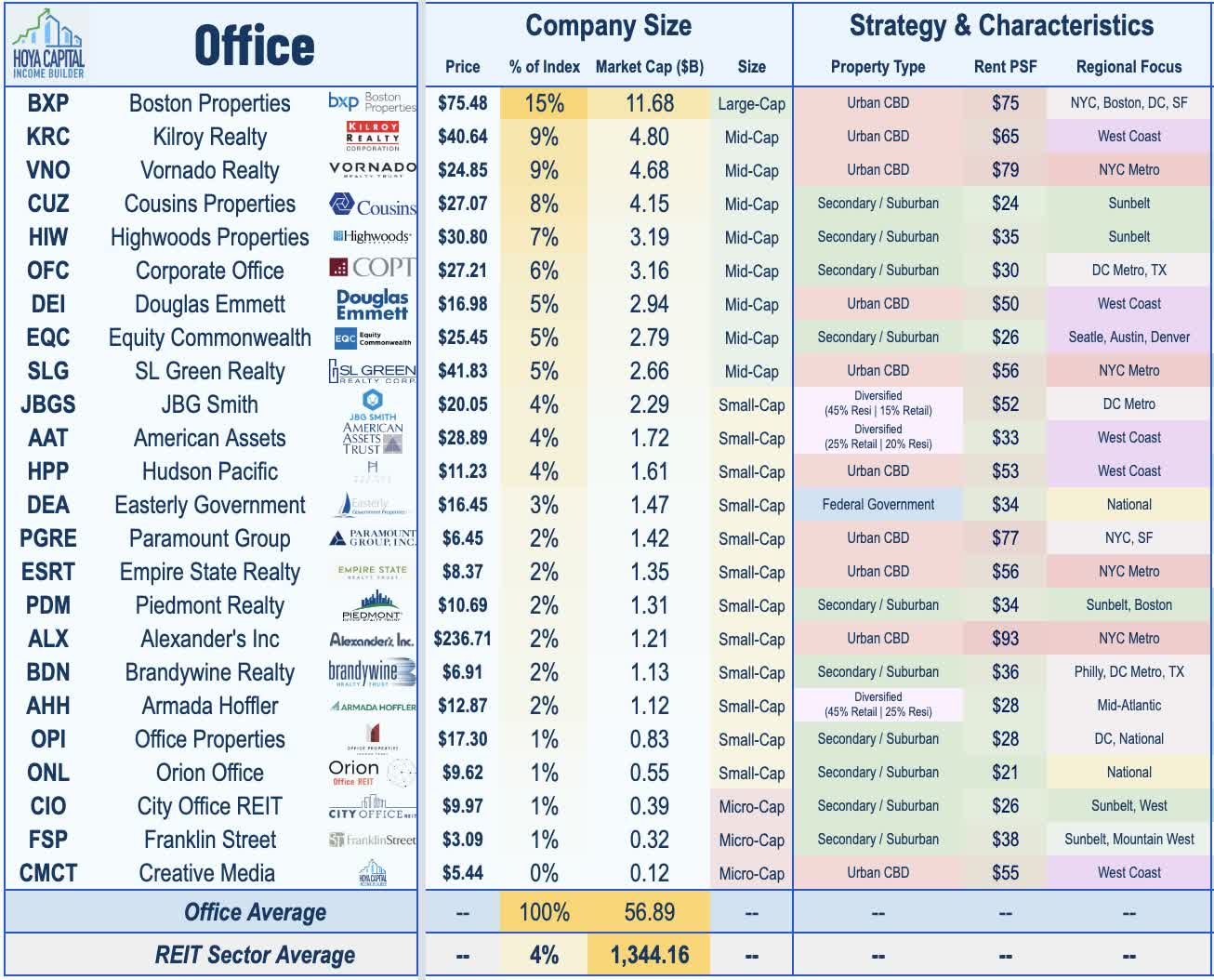

Within the Hoya Capital Office REIT Index , we track the 23 office REITs, which account for roughly $55 billion in market value and comprise 6-7% of the market-cap-weighted REIT Indexes. Office REITs have been far-and-away the worst-performing property sector since the start of the pandemic as depressed utilization rates and recession concerns have curbed office space demand. Office leasing activity and REIT earnings results through the pandemic haven't been as weak as many feared, but corporations won't pay for half-empty space indefinitely and we started to see more definitive signs of softening in late 2022. With Office REITs trading at historically deep discounts to peers in the public and private markets - how much pain is already priced in?

{kind=link}

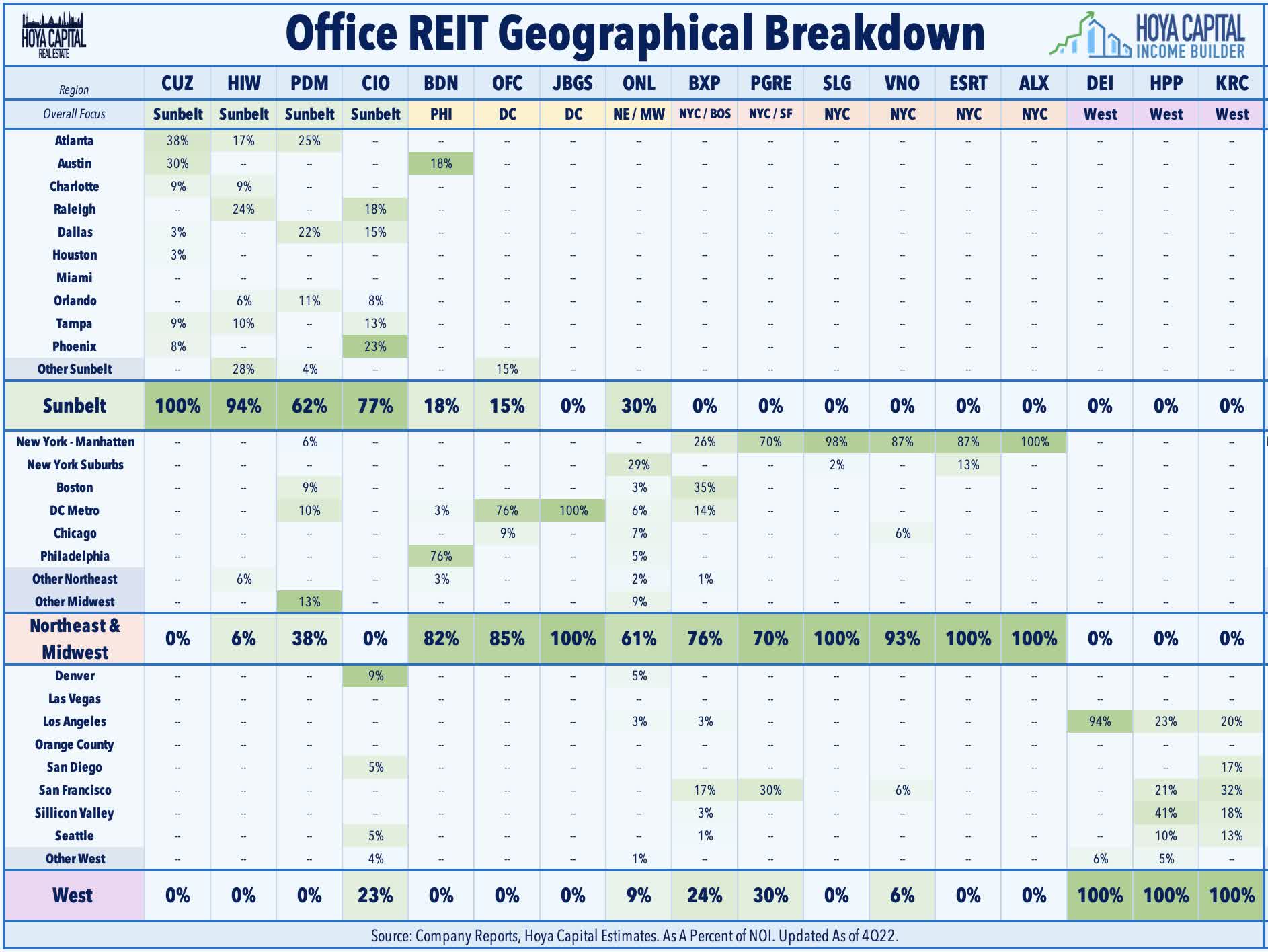

The office sector is typically segmented into two categories. Urban CBD ("Central Business District") or ' Gateway' REITs hold portfolios that are concentrated in the six largest U.S. cities: New York City, Chicago, Boston, Los Angeles, San Francisco, and Washington, D.C., a segment that has been hit especially hard by the pandemic. Secondary/ Suburban REITs , which have generally outperformed throughout the pandemic, hold portfolios concentrated in the Sunbelt regions and/or in secondary markets. As we'll discuss throughout this report, we believe that the longer-term outlook remains far "sunnier" in the Sunbelt and in secondary markets with net population growth, shorter commute times, and a more favorable industry mix, but we're also beginning to see compelling value in some Coastal-focused REITs where the consensus appears to have swung too far in the negative direction.

{kind=link}

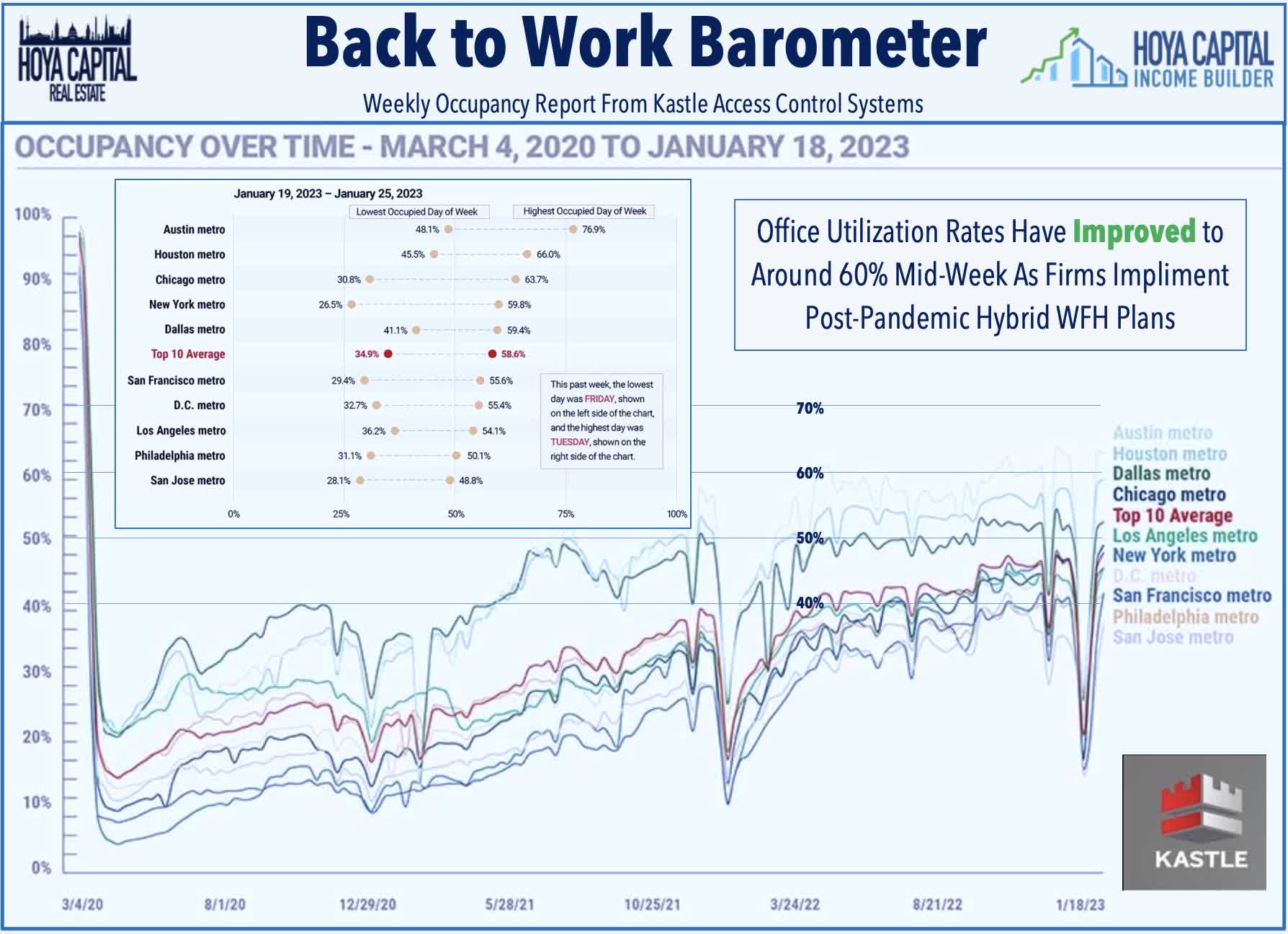

Since early in the pandemic, we've held the view that the Work-From-Home era is truly a "new normal" - a catalyst that accelerated a pre-destined trend of lower office utilization rates - and that the return to the office would be particularly slow in cities with longer average commute times and heavier reliance on public transit. Consistent with that expectation, utilization rates have recovered only a fraction of pre-COVID levels, particularly in dense coastal markets with longer and more transit-heavy commutes. According to recent data from Kastle Systems, office utilization finally eclipsed 50% for the first time since the start of the pandemic in late January. While utilization rates remained at 50% or below in all of the major coastal urban markets, Sunbelt and secondary markets have seen materially higher utilization rates throughout the pandemic. Austin, for instance, is now seeing mid-week utilization rates of over 75%.

{kind=link}

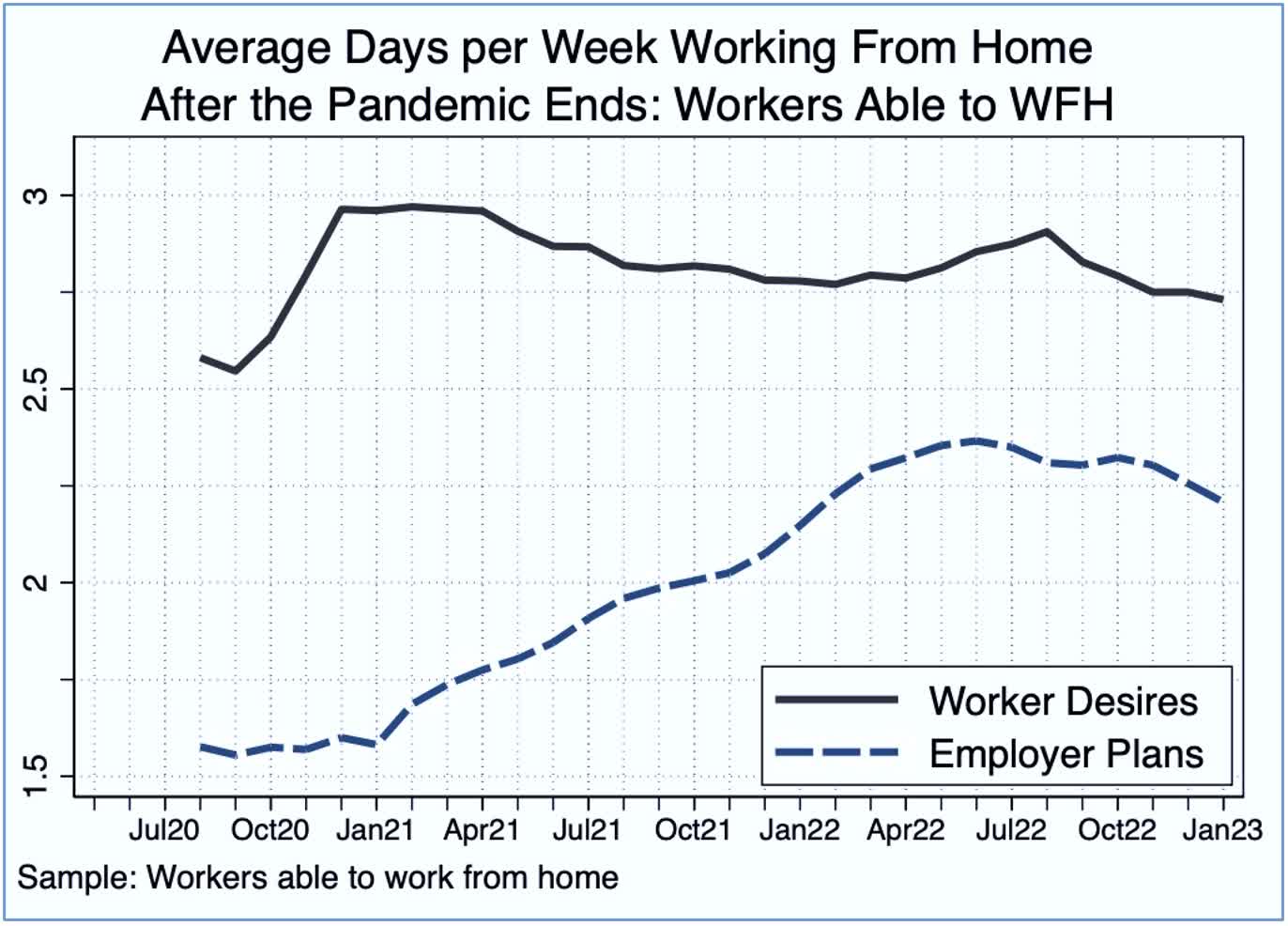

Based on recent survey data discussed in more detail below, we believe the ultimate post-pandemic "trend level" of utilization rates is around 60% of pre-pandemic levels in primary urban metros - up from roughly 45% today, implying a 3-day/week average in-person attendance. In secondary markets where the economic benefits of in-office attendance are more likely to outweigh the costs, utilization rates will be closer to 80% - up from roughly 60% today, implying a 4-day average workweek. We believe that this final 20% of upside utilization will be unlocked as labor markets finally begin to materially loosen, and we have indeed seen more companies use office "mandates" as part of their workforce reduction strategies including recent examples from Disney ( DIS ), Starbucks ( SBUX ), Google ( GOOG ) (GOOGL).

{kind=link}

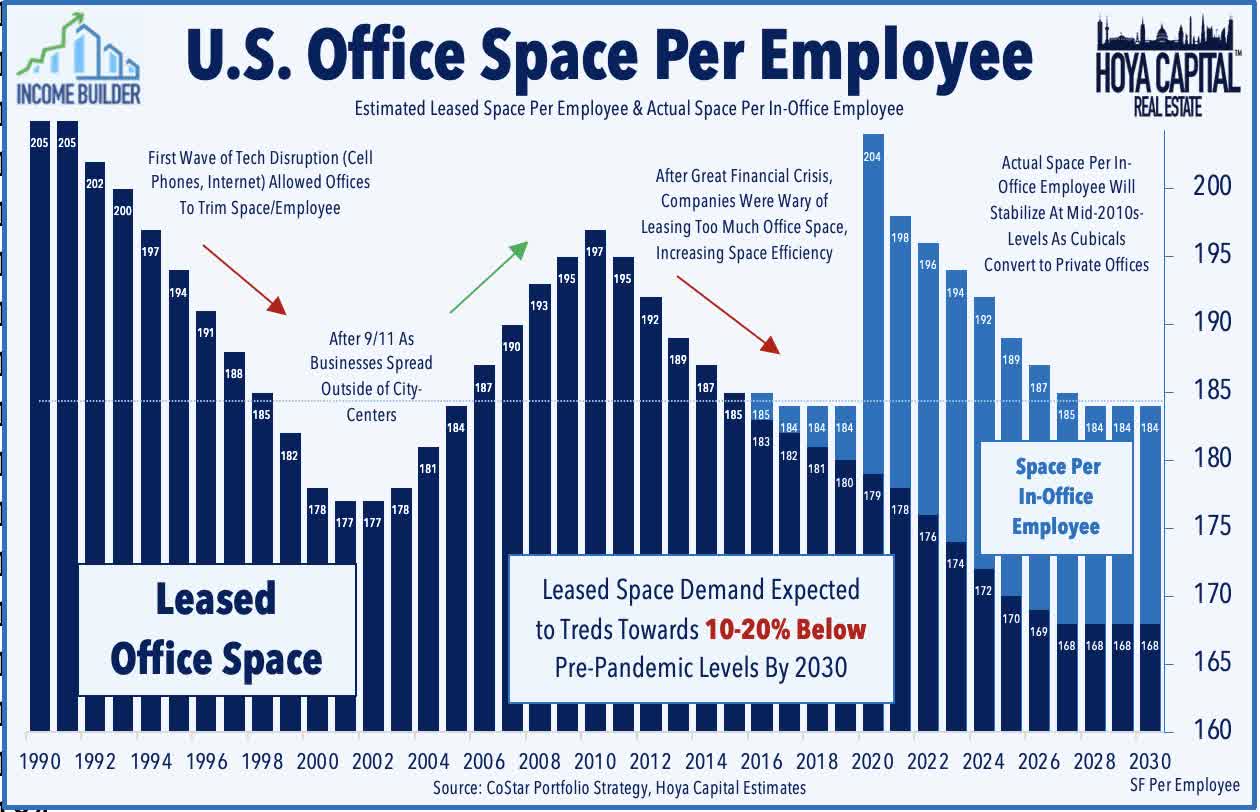

We believe that employers will seek to trim only about half of this incremental "unused" space in their next renewals, implying about a 15-25% reduction in "same company" demand in primary urban metros and 5-10% in secondary markets - which is likely quite a bit more optimistic for office demand than implied by office REIT valuations, which appear to imply cuts that match the lower utilization rates on a 1-for-1 basis. What's overlooked is that we're not too far removed from the GFC period which saw substantial cuts in excess office square footage from 2008-2011 and a decade-long trend towards a higher office "utilization factor"- in other words, jamming more employees into the same square footage with the often-loathed open floor plans. There simply wasn't a huge glut of under-utilized office space before the pandemic, and we believe that employers will be content with some modest space reductions while offering more space per in-office employee through build-outs that include more private office space and fewer open floors and cubicles.

{kind=link}

Where Will Utilization Rates Stabilize?

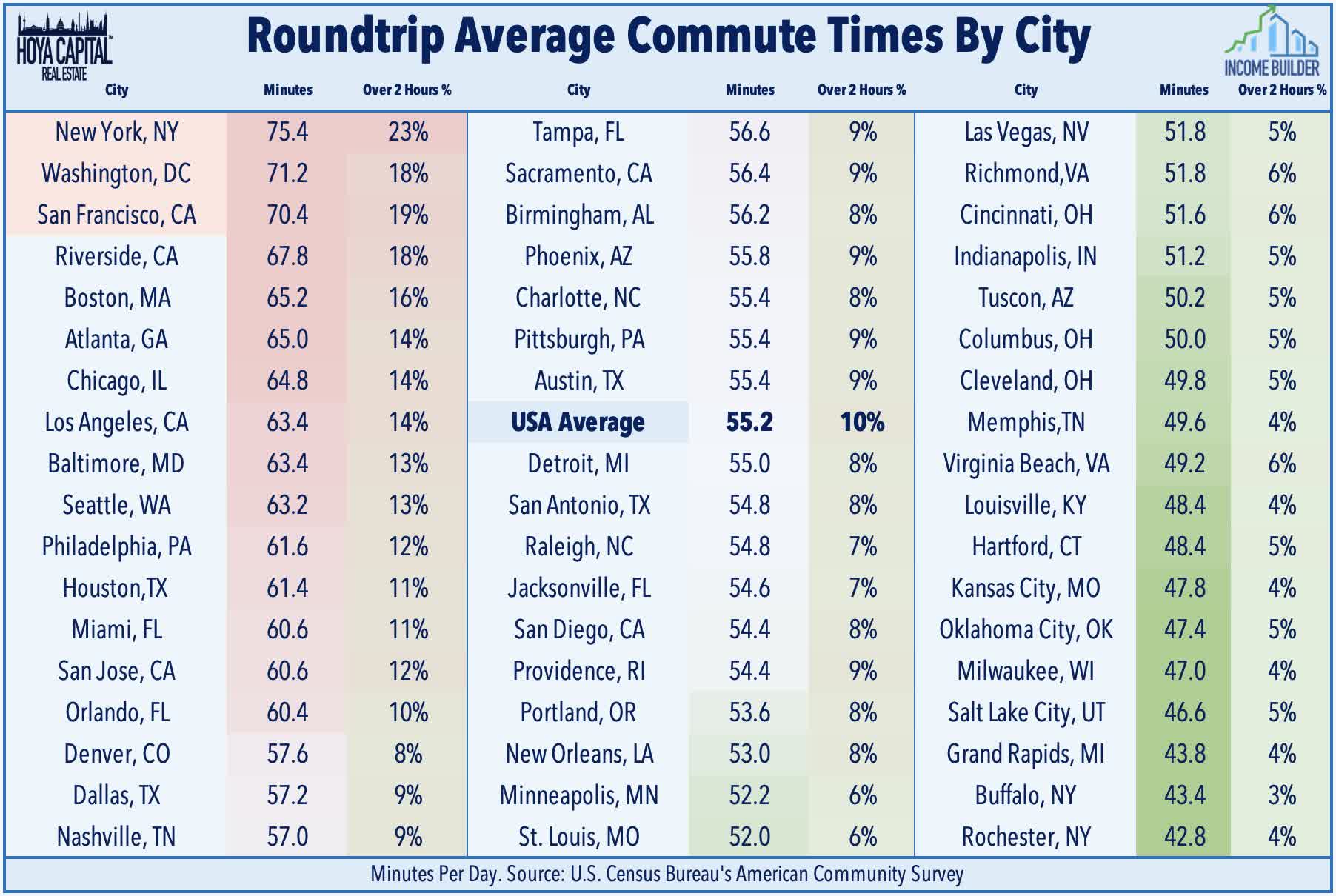

Recently-updated data from the American Community Survey show that over the course of a 5-day work week, remote work employees in cities with particularly brutal commutes "save" an average of 6.5 hours per week and a hundred dollars in transportation costs. Recent surveys from WFH Research confirmed that the lack of a commute is far and away the top benefit of working from home. The survey found that WFH saved office workers an average of 70 minutes per day, of which 40% was reallocated toward work. That "bonus" time allocated towards work seems to explain all of the reported productivity gains of WFH found across most surveys - offsetting the drag from a generally less productive home environment compared to the office.

{kind=link}

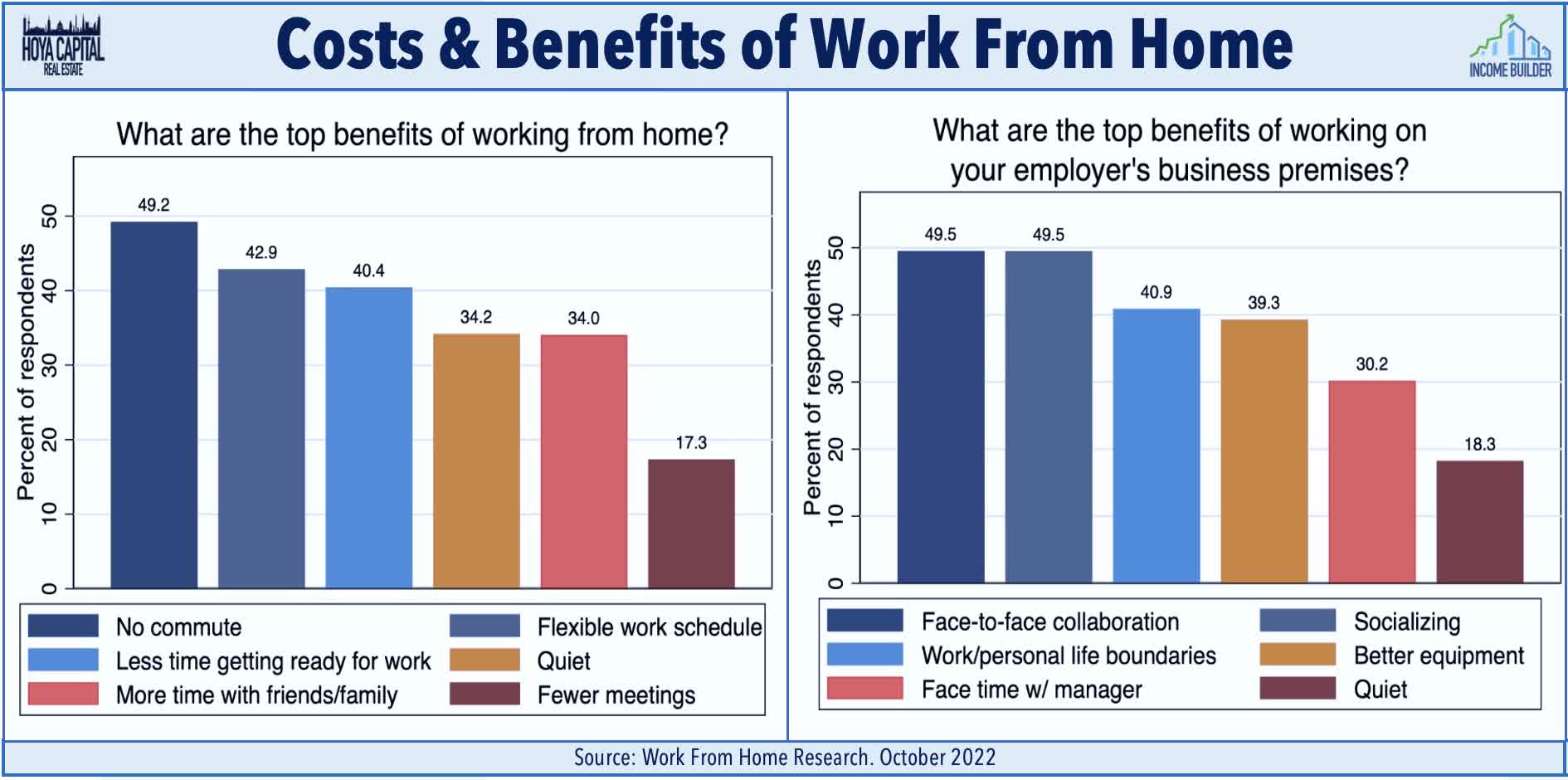

Importantly, survey data continues to show that the office isn't necessarily the problem - it's the commute - and there's a growing consensus that there are quantifiable "costs" of remote work which can accumulate over time if not at least augmented by some non-virtual between employees and clients. A recent Hogan survey noted that employees cited challenges with collaboration (36%), distractions at home (25%), and difficulty with motivation (16%) as the top challenges of the fully-remote environment and a consistently small share of employees want to do away with the office entirely - averaging 10-20% across most surveys - with younger people itching to get back to the office at rates nearly twice that of older cohorts. A recent survey from KPMG found that less than one in five workers would prefer to be fully remote.

{kind=link}

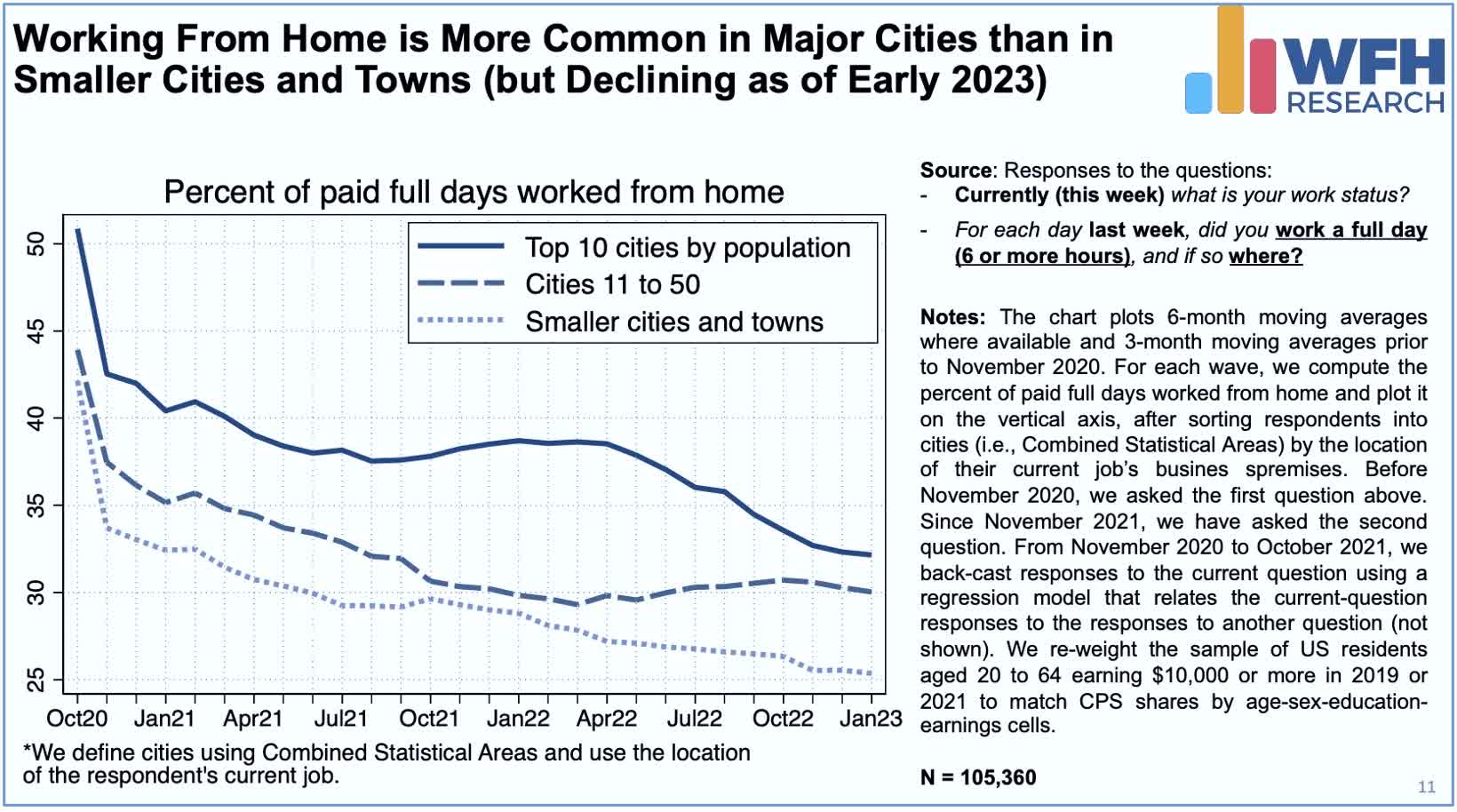

Consistent with this framework, in markets with shorter average commutes, the productivity and social benefit of the office environment are "worth" the commute time. In fact, Work From Home adoption remains primarily a 'Big City' trend with a near-linear correlation between the size of the market and the WFH rates. Industry and tenant mix has also become an increasingly important factor that explains the variance in office utilization rates and also captures some of the effects of commute times. Certain industries are far more WFH-friendly than others, particularly the technology and financial services industries, where WFH Research finds that employers expect just 2.2 to 2.5 office days per employee per week under their post-COVID plans. These office utilization rates are roughly half that of other office-using industries that expect their employees to report to the office 3-4 times per week.

{kind=link}

Office Sector Fundamentals & REIT Earnings

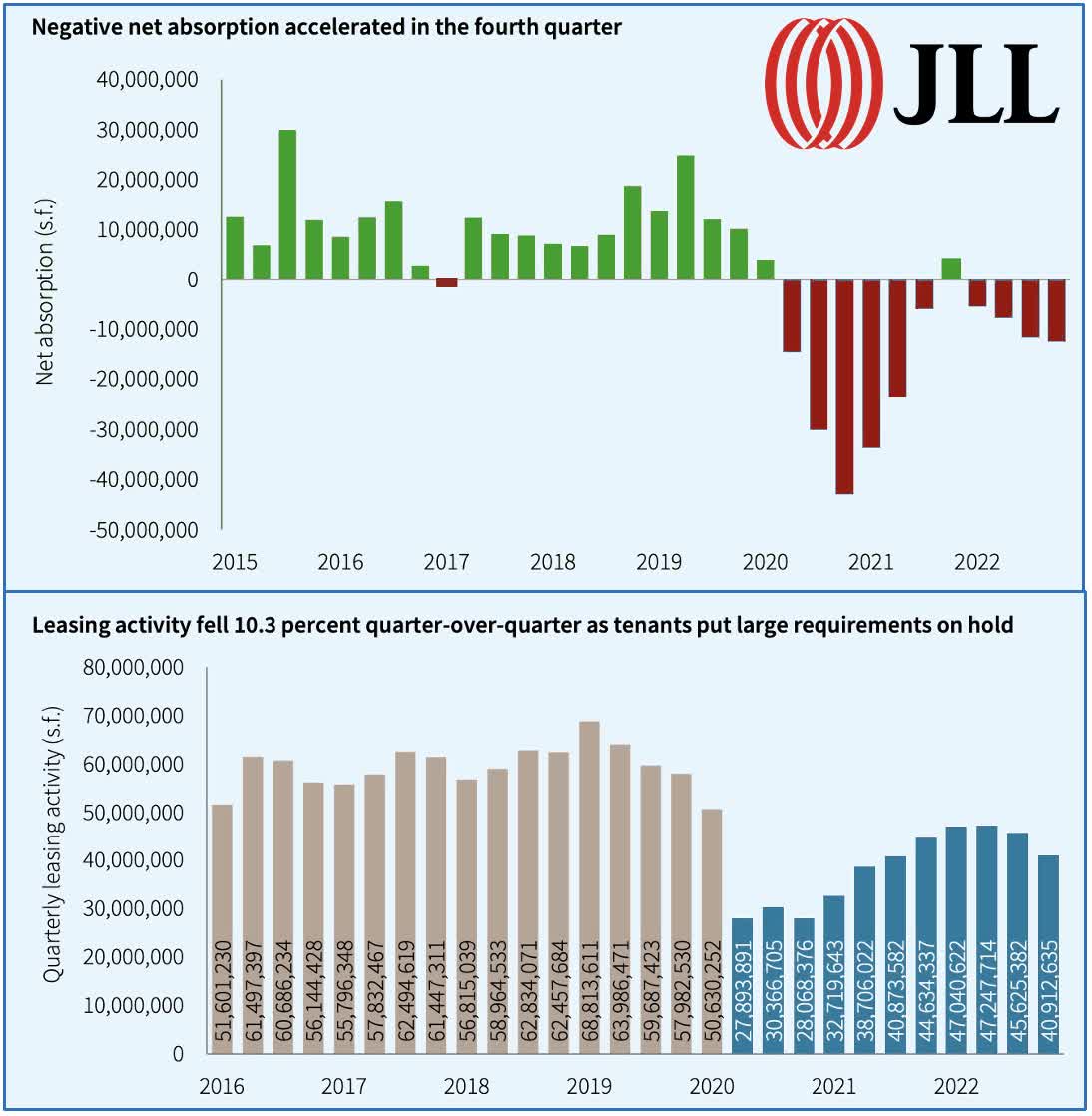

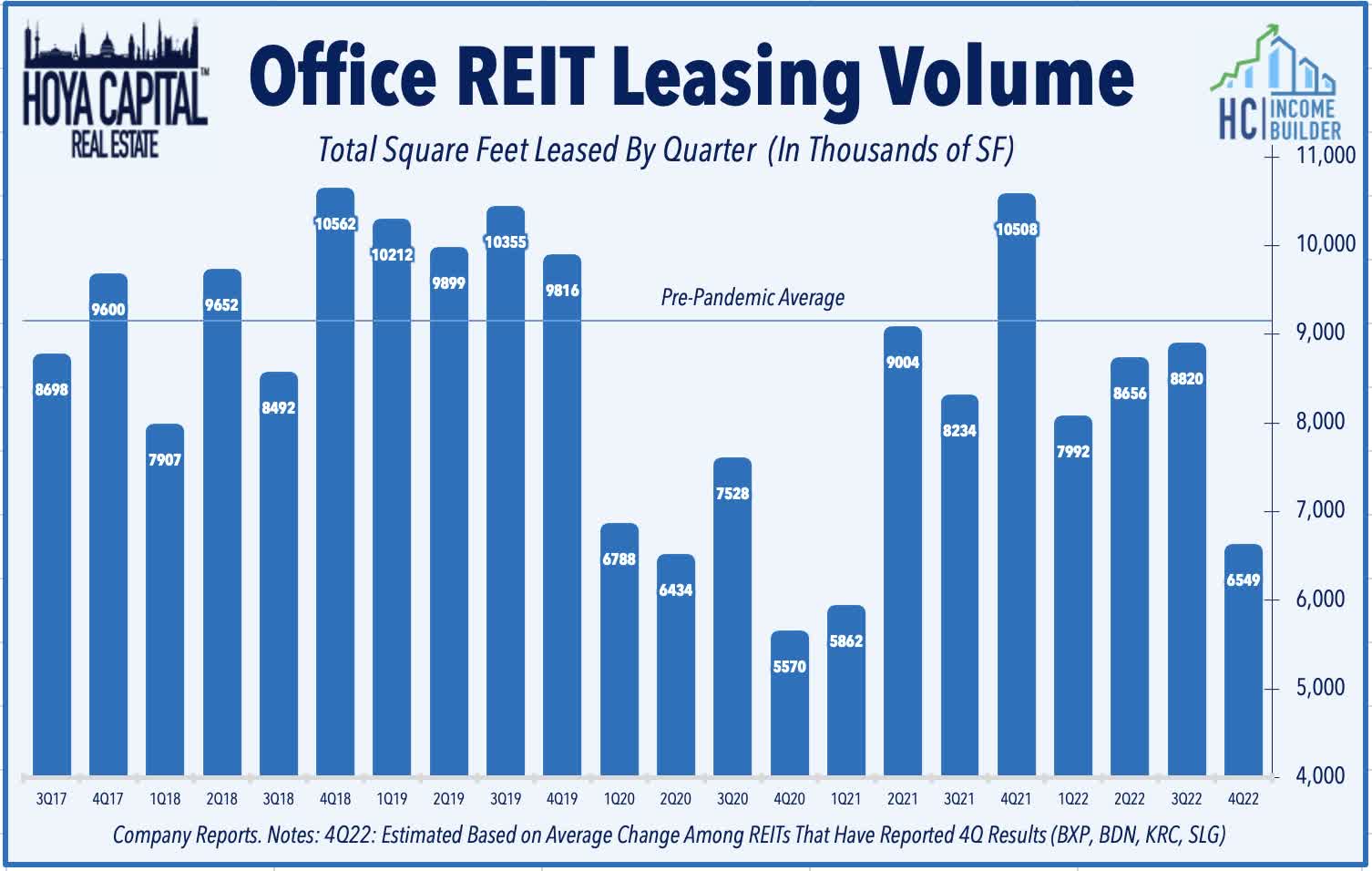

Corporate decision-makers have, so far, been hesitant to make major strategic decisions to dramatically reduce their office footprints, but have been leveraging softening market conditions to extract generous concessions. JLL Research noted in their recent Office Report that leasing activity was relatively strong in 2022 with volumes that were 15.1% higher than in 2021 - which was roughly 25% below pre-pandemic levels. The fourth quarter saw a "notable slowdown" in activity, however, especially among large-cap leases with Q4 recording the lowest quantity of lease transactions over 100k SF since Q1 2021 while total leasing activity fell 10.8% in the fourth quarter 40.7 million SF. The recently quarterly US Office Marketbeat noted several bright spots, seeing strong demand in life sciences markets, in large Sunbelt markets with strong job growth and appeal for growing tech firms, and in recovering secondary markets in the Northeast - notably Fairfield County.

{kind=link}

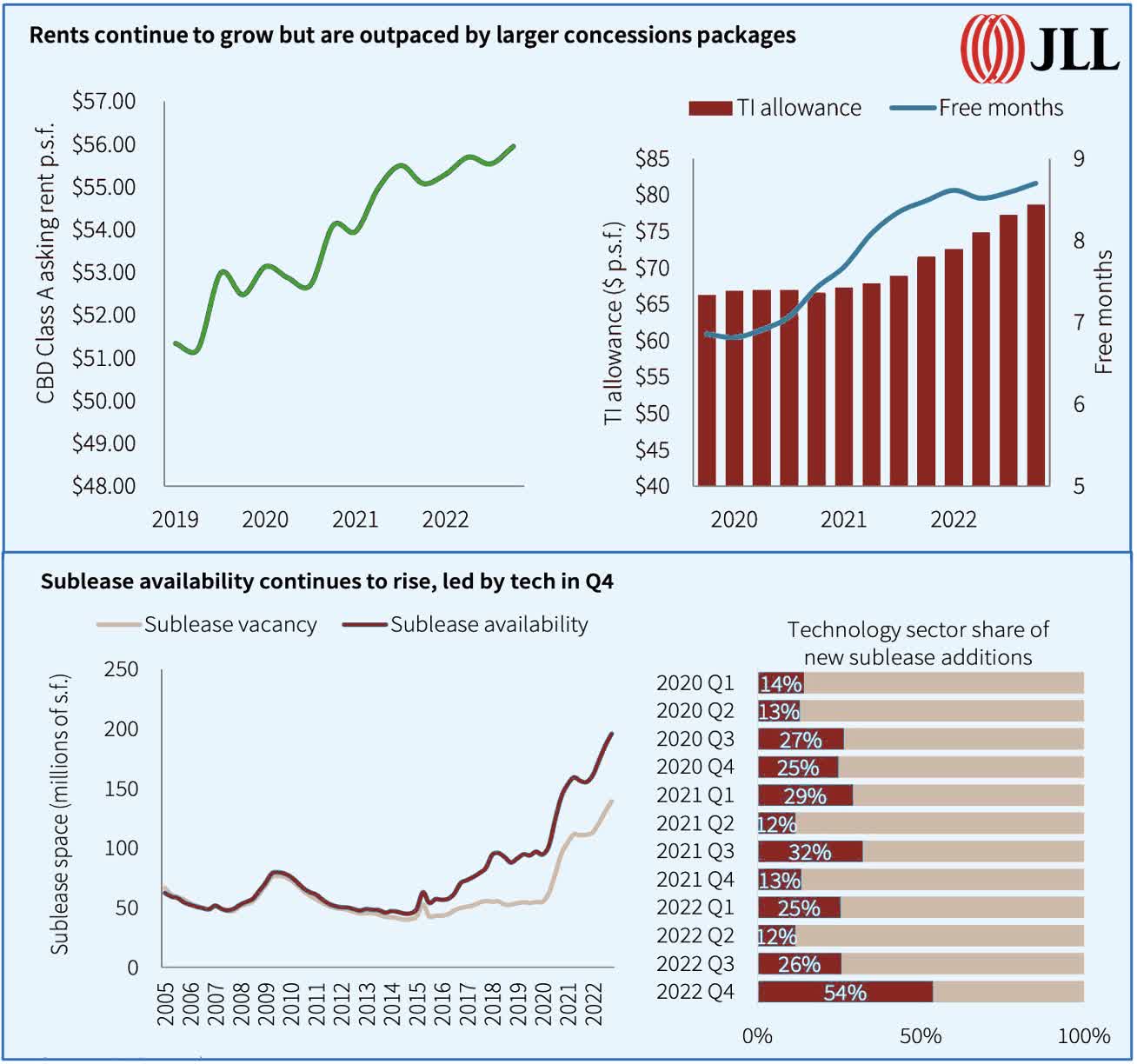

There were also mixed signs on the pricing front with JLL noting that "the relative scarcity of high-quality space enabled landlords to preserve face rental rates" with asking rents rising 0.3% to $38.86/sf, but the increase was "offset by concession packages that eclipsed all-time highs." At the national level, JLL reports that while asking rents are roughly flat since the start of the pandemic, effective market rents have declined by 6.2% as concessions continue to be on the rise. Term-adjusted rent abatement periods have grown 2.5% since the end of 2021 and 26.8 percent since the outset of the pandemic, while tenant improvement allowances have grown by 10% in the last year and 18.8% over the past three years. Space availability in sublet markets also continued to swell - rising to a record 136.6M SF at the end of 2022 - but the pace of sublet additional slowed in late 2022, which JLL believes "indicates that the recent wave of sublease should begin to stabilize in coming quarters."

{kind=link}

These trends have been consistent with office REIT earnings results over the past several quarters which have been defined by

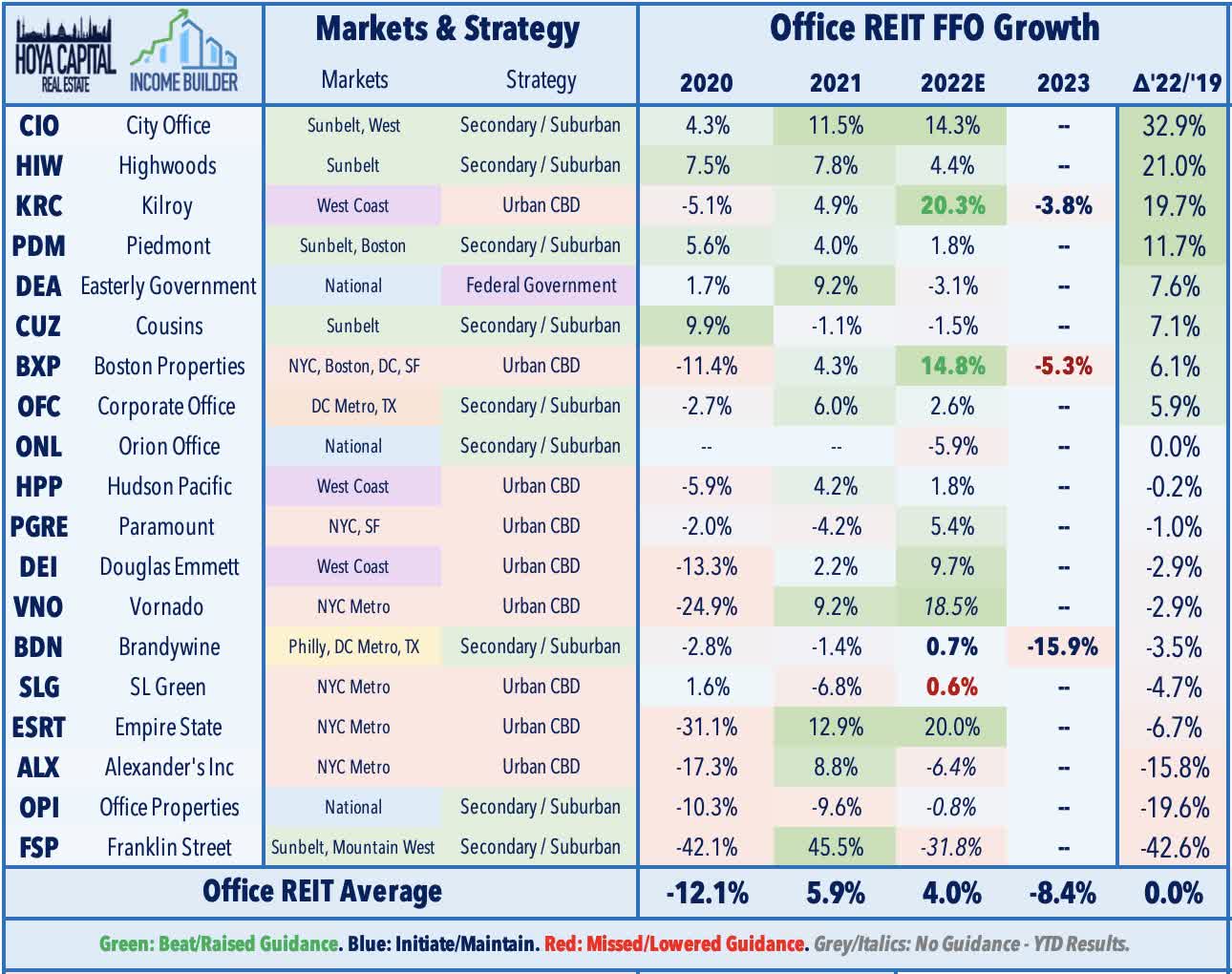

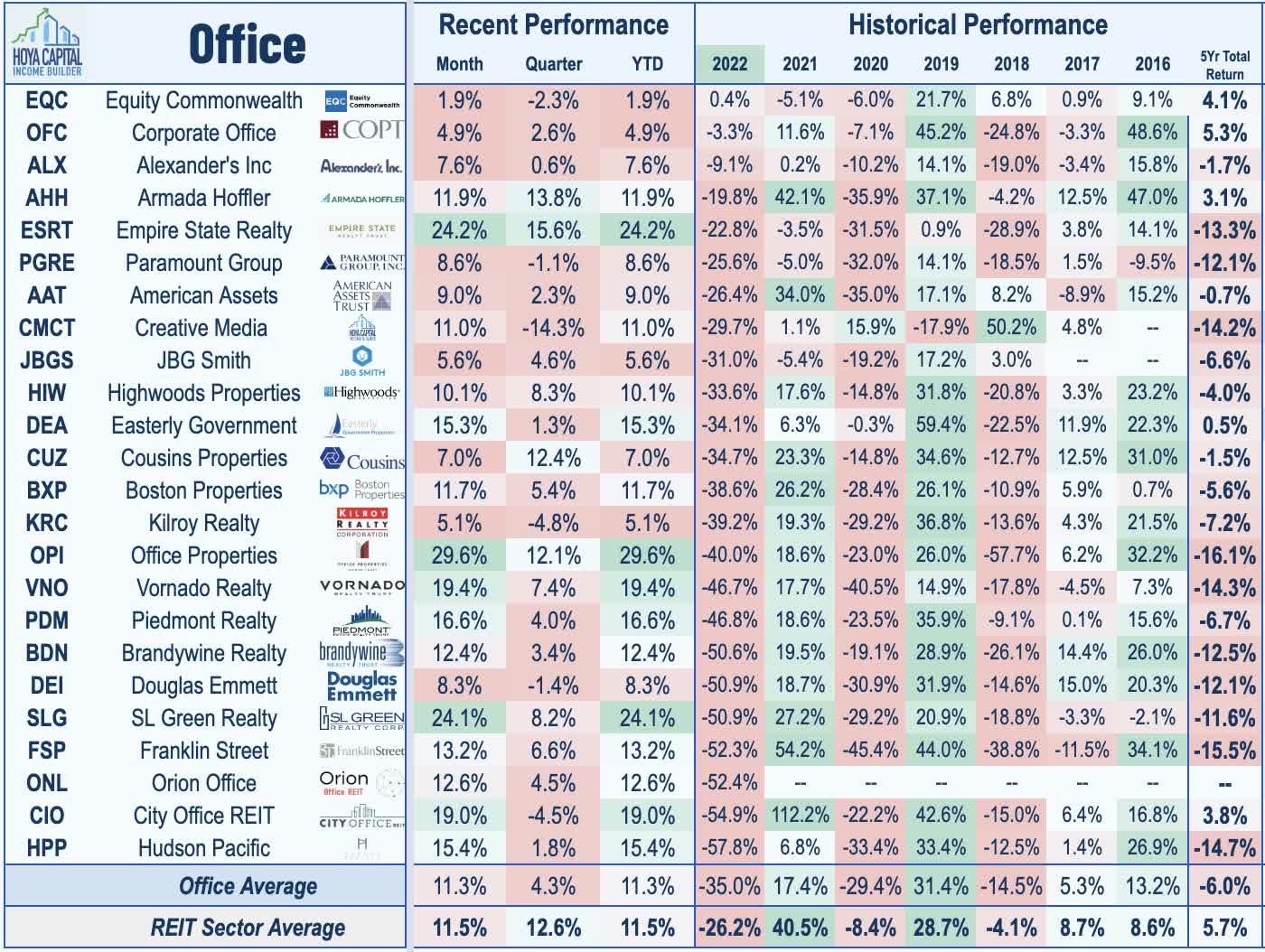

significant outperformance from Sunbelt and secondary-market-focused REITs and coastal REITs with significant specialty lab space assets. Sunbelt-focused Highwoods ( HIW ) has been an upside standout in recent quarters and expects to report full-year FFO growth in 2022 that is 21% above its pre-pandemic level from 2019 - an increase eclipsed only by small-cap City Office ( CIO ). Other notable outperformers through the pandemic include Kilroy ( KRC ) - which confirmed last week that its FFO rose just shy of 20% from 2019-2022 - along with Sunbelt-focused Piedmont ( PDM ) and Cousins ( CUZ ) which are expected to report 2022 FFO that is 12% and 7% above 2019-levels, respectively.

{kind=link}

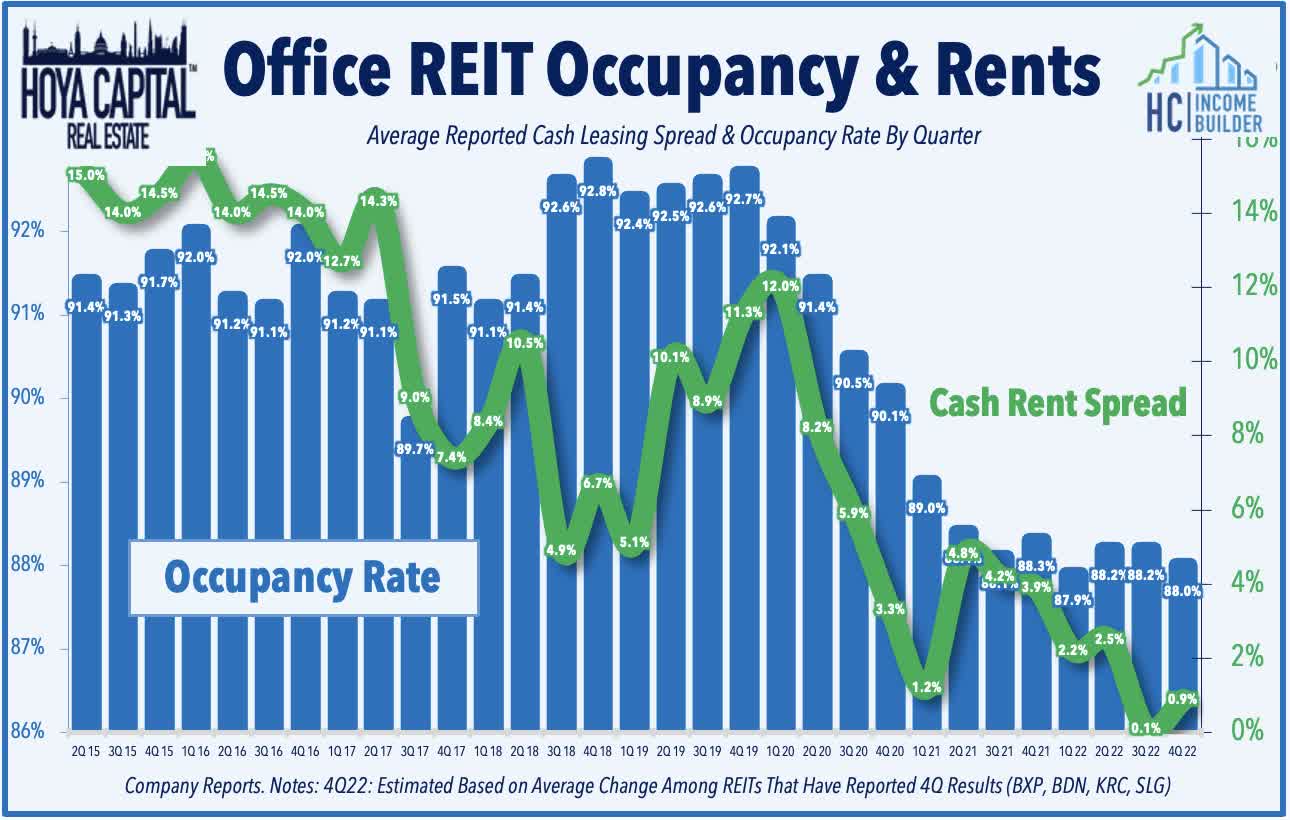

For REITs, the average occupancy rate has trended down only slightly to around 88% in late 2022 while asking rent spreads have managed to remain slightly positive, on average, with Sunbelt strength offsetting Coastal weakness. While still early in fourth-quarter earnings season, results from office REITs haven't been as soft as feared. Boston Properties ( BXP ) recorded FFO growth of 14.8% in 2022 and expects its FFO to decline 5.3% in 2023 at the midpoint of its guidance. Leasing volumes were soft in Q4 - the second slowest quarter in the past decade - but occupancy rates held relatively firm and rental rate spreads actually accelerated slightly to 4.3%. Similar trends were reported by Kilroy, which achieved spreads of 12.3% in Q4 - up from 7.5% in the prior quarter and recorded an 80 basis point sequential increase in occupancy rates.

{kind=link}

Results from Brandywine ( BDN ) - one of the hardest-hit REITs in 2022 - were also better than feared, with BDN reporting that its full-year 2022 FFO rose 0.7% but forecast a 15.9% decline in FFO in 2023. Encouragingly, BDN was able to complete $705M in asset sales in Q4 and used the proceeds to refinance its looming $350M debt maturity and pay down its $600M line of credit, pushing out the majority of its maturities beyond 2026. While leasing volumes improved to about 10% of pre-pandemic averages in Q3, results thus far have been softer with total volumes running at around 33% below comparable pre-pandemic levels across the four REITs that have reported.

{kind=link}

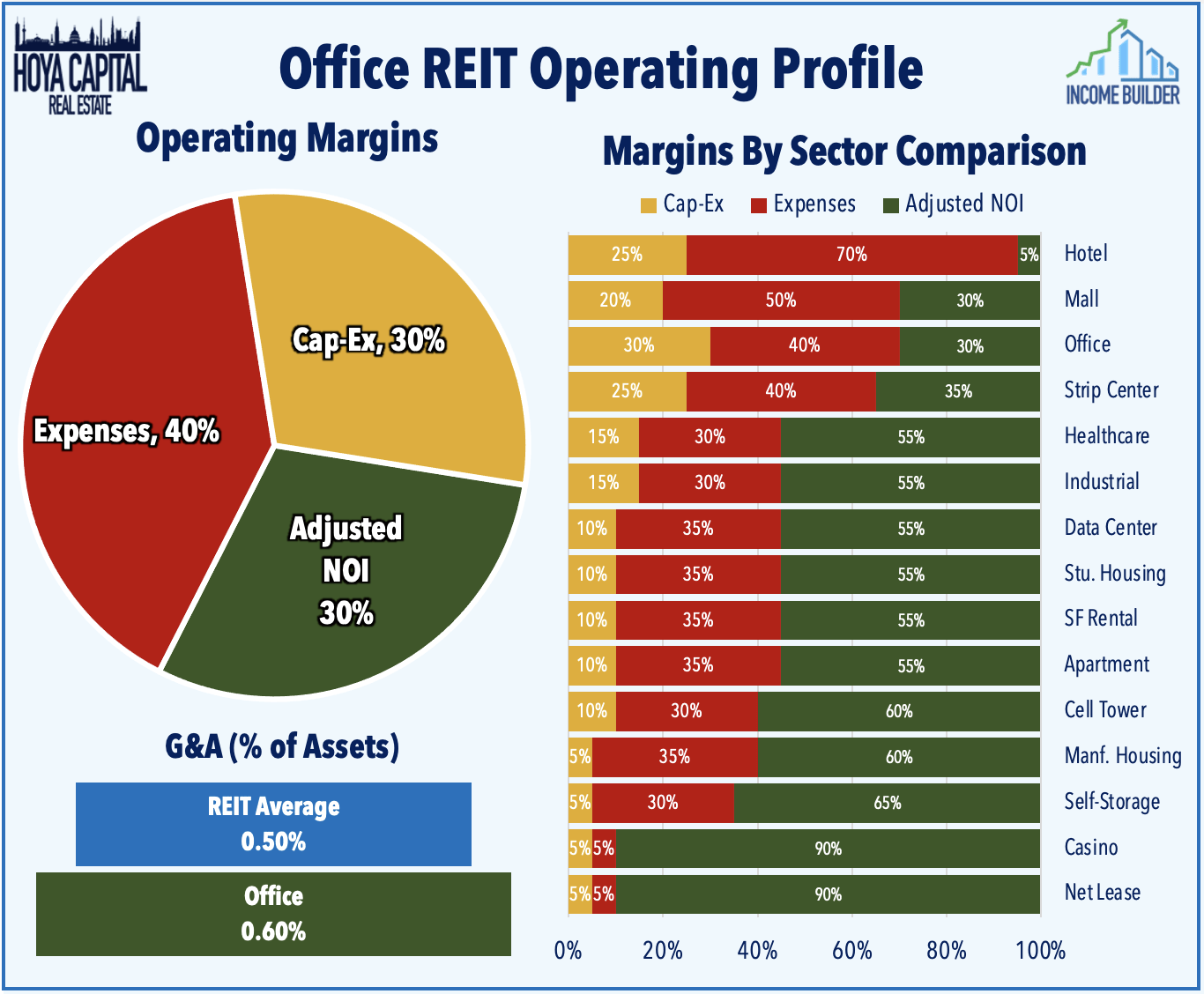

Even in the best of times, office ownership is a tough, capital-intensive business with relatively low operating margins and high capital expenditure needs, as tenants tend to have quite a bit of negotiating power relative to landlords. This is particularly true given the ample available supply - a supply overhang that will linger for much of the next decade. Given the high degree of fixed costs incurred in managing an office property - whether fully occupied or mostly vacant - operating leverage is quite high. Thus, small changes in occupancy and market fundamentals can have significant negative impacts.

{kind=link}

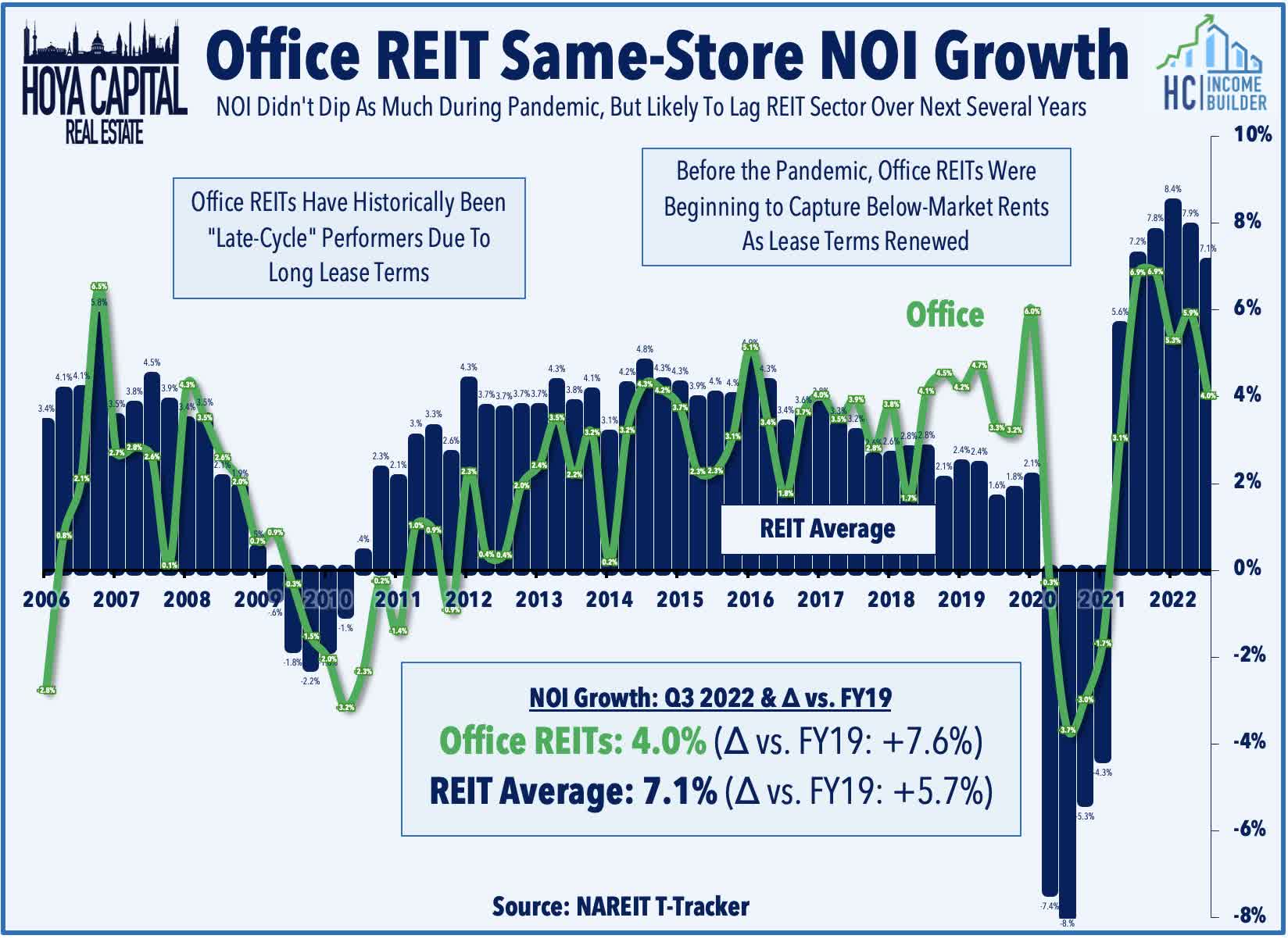

Office REITs were finally hitting their stride right before the pandemic, powered by a seemingly unstoppable streak of job growth that reached over 115 consecutive months. The office REIT sector tends to outperform later in the economic cycle and respond more slowly to economic inflection points given the typically long-term lease structure inherent in office leases, which average 5-10 years for suburban assets and 10-20 years for CBD assets. Same-store NOI growth for office REITs averaged -0.2% in 2020 but bounced back into positive territory in 2021 with 3.9% growth and through the end of Q3, stood 7.6% above pre-pandemic levels despite the broader industry pressure.

{kind=link}

On that note, the broader supply dynamic has been a persistent headwind in many major markets as construction spending on office development ramped up after the 2016 elections, spurred by the passage of corporate tax reform and strong job growth of key office-using sectors. The office pipeline increased to a new cycle-high in late 2019 right before the start of the pandemic, and after a slight pullback during the pandemic, office REITs were again some of the more active developers across the REIT space. According to NAREIT T-Tracker data, the office development pipeline stands at $15.1 billion, up sharply from the 2012 level of $2 billion, representing 26% of office REIT market value which is by far the highest relative pipeline in the REIT sector.

{kind=link}

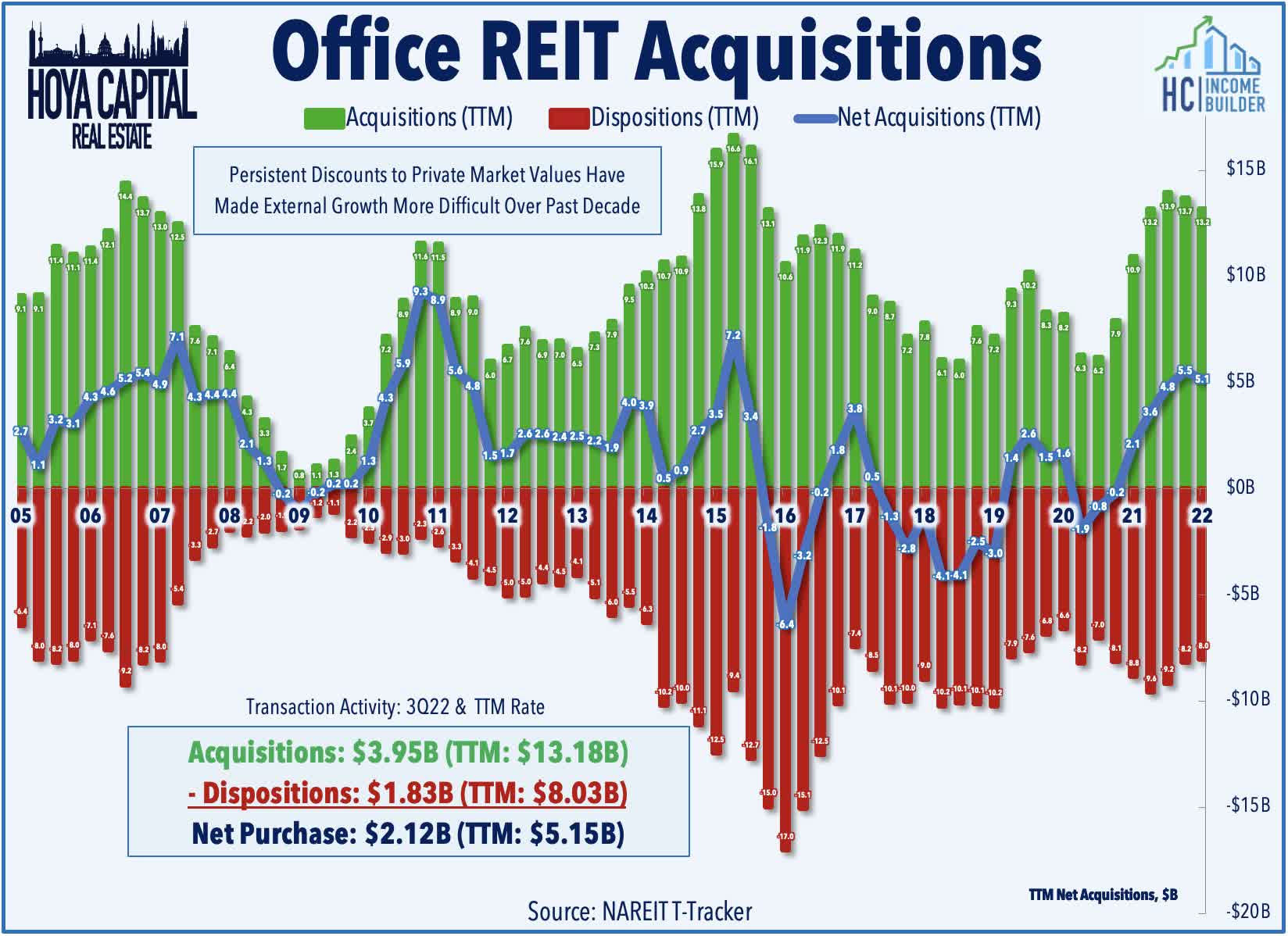

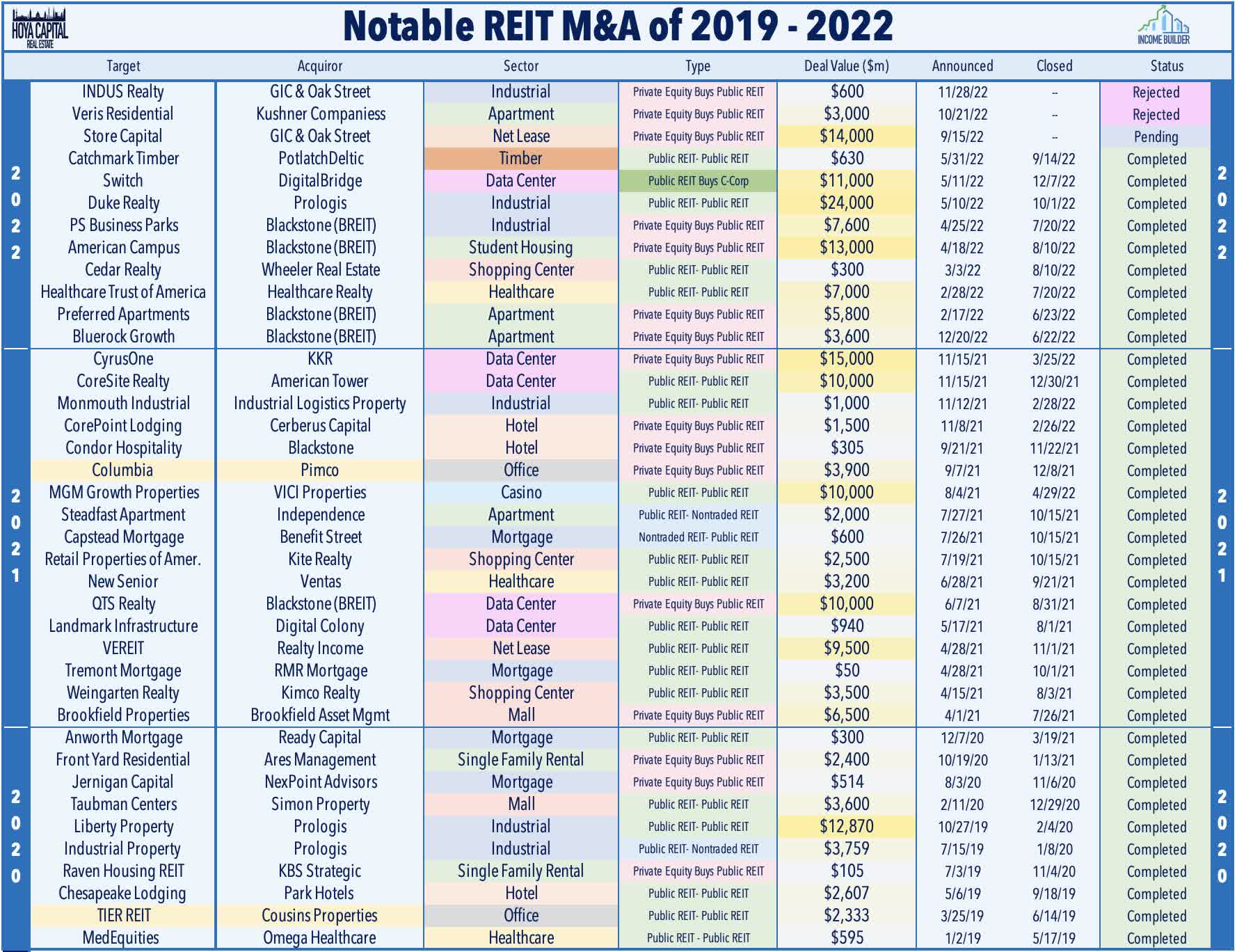

Ground-up development has been the lone source of external growth for office REITs over the past half-decade as accretive acquisitions have been made quite difficult by the persistent valuation discounts relative to private market valuations. As noted above, private market pricing has remained notably firm in recent quarters despite the rise in interest rates, underscored by several major transactions including Google's $2.1 billion deal to buy a Manhattan office building. Office REITs had been showing signs of life on the acquisition front in recent quarters, particularly the Sunbelt-focused REITs with a more attractive cost of capital, recording $13.3 in acquisitions in 2021, the highest since 2017 but most REITs have pulled back amid the latest surge in rates.

{kind=link}

Several office REITs have taken advantage of the steep NAV discounts to create significant shareholder value. Last year, Columbia Property Trust was acquired by PIMCO at a healthy premium, underscoring our belief that the sector is long overdue for a wave of consolidation and asset sales. Elsewhere, Mack-Cali Realty rebranded itself as Veris Residential ( VRE ), reflecting the company's exit from the office sector through a series of asset sales as it transitions into a pure-play multifamily REIT. This move follows a similar strategic shift from Washington REIT , which sold its office portfolio to Brookfield ( BAM ) for $766M as WRE shifts its focus to multifamily and rebranded as Elme Communities ( ELME ).

{kind=link}

Office REITs Stock Price Performance

After riding the 'reopening rotation' and inflation trade to strong gains in early 2022, higher interest rates, recession concerns, and the sluggish "return to the office" have weighed heavily on the office REIT sector in recent months. After leading the gains in the REIT sector early in 2022, office REITs ultimately ended the year as the worst-performing property sector and extended their underperformance to a third-straight year. The Hoya Capital Office REIT Index - a cap-weighted index of the sector - posted declines of nearly 40% compared to the -25% decline from the Vanguard Real Estate ETF ( VNQ ) and also lagging the -18% decline from the S&P 500 ETF ( SPY ).

{kind=link}

The underperformance last year comes after an equally disappointing 2021 in which office REITs gained 23.3% for the year, significantly lagging the 41.3% total returns from the All Equity REIT Index. Diving deeper into the performance of these individual REITs, every office REIT was lower for the year while seven REITs declined by 50% or more including Hudson Pacific ( HPP ), City Office ( CIO ), Orion Office ( ONL ), Franklin Street ( FSP ), and SL Green ( SLG ). Office REITs have rebounded in 2023 alongside the broader rally across the real estate sector, gaining 11.3% through the first five weeks of 2023, roughly matching the 11.5% gains on the broader REIT index.

{kind=link}

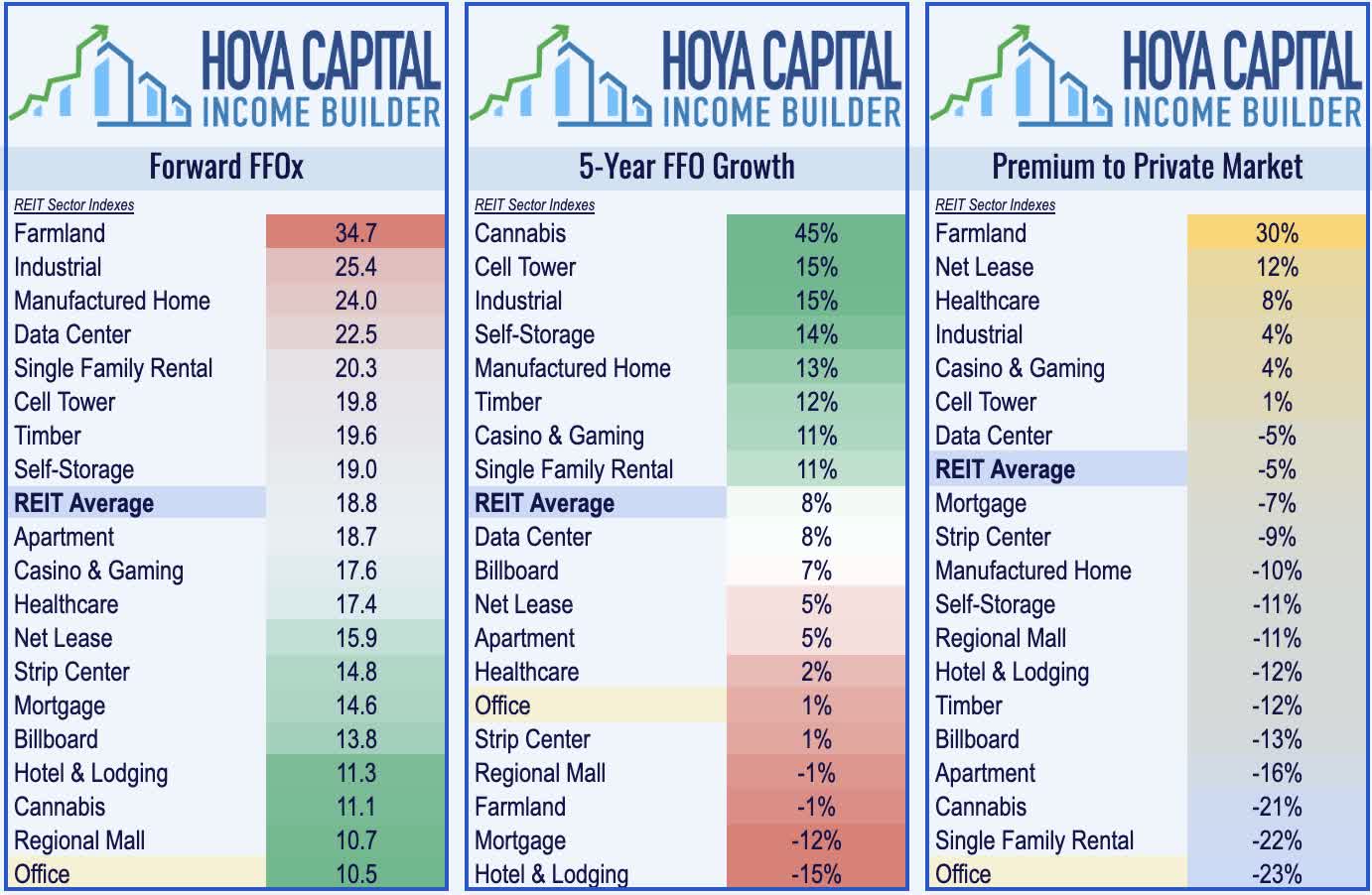

Property-level fundamentals have clearly softened, but the outlook is not as dire as office REIT market valuations imply. Even using the most bearish cap rate estimates, the NAV discount for office REITs is very real and meaningful in the ballpark of 20-25% - the steepest discount in the public REIT sector - and Office REITs now trade at P/FFO multiples below that of Mall REITs. With Office REITs trading at historically deep discounts to peers in public and private markets - and average dividend yields near 6% - there appear to be some emerging pockets of value - notably in REITs focused on secondary and tertiary markets with net population growth, shorter commute times, and a more favorable industry mix.

{kind=link}

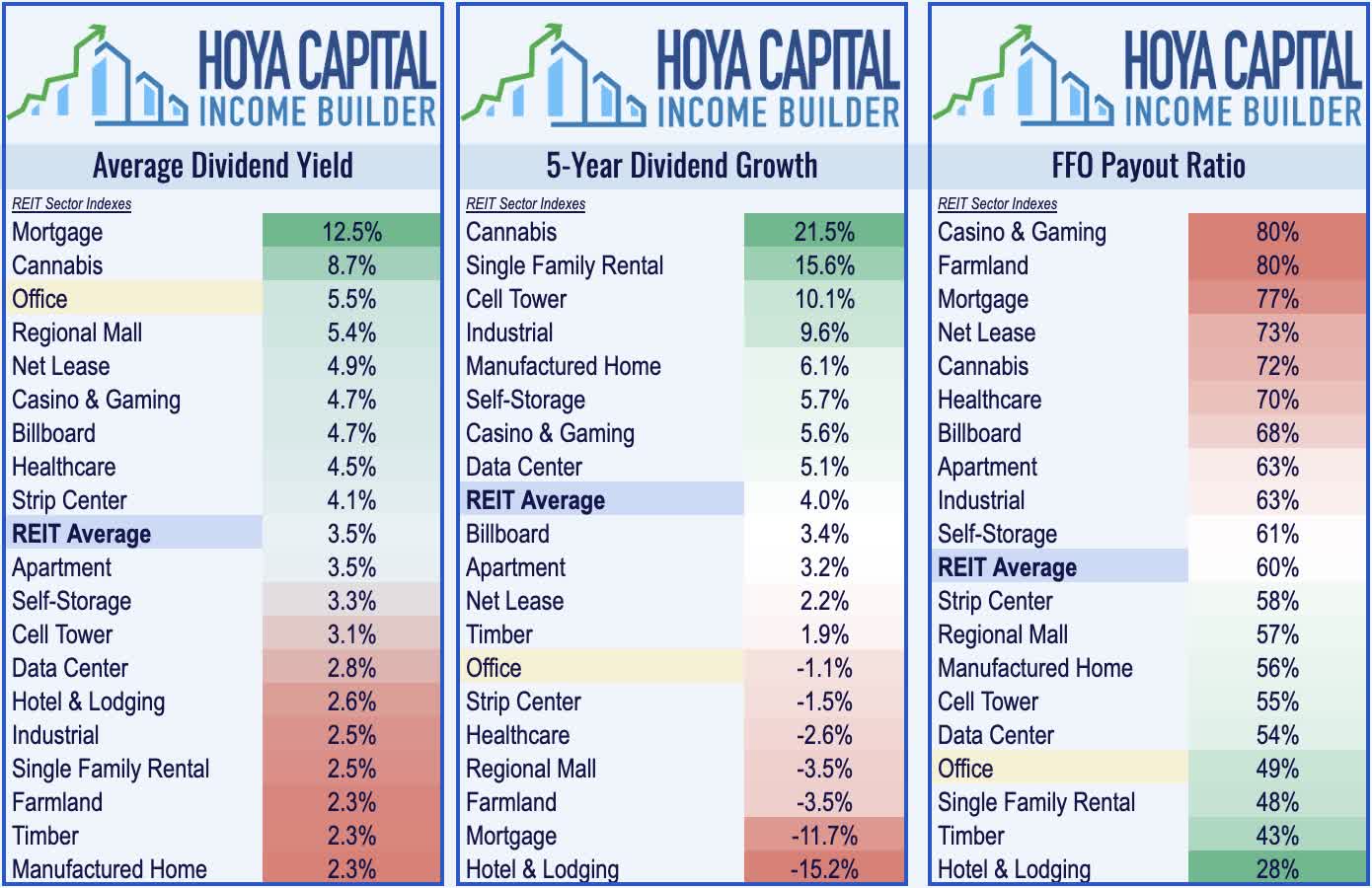

Office REITs Dividend Yields

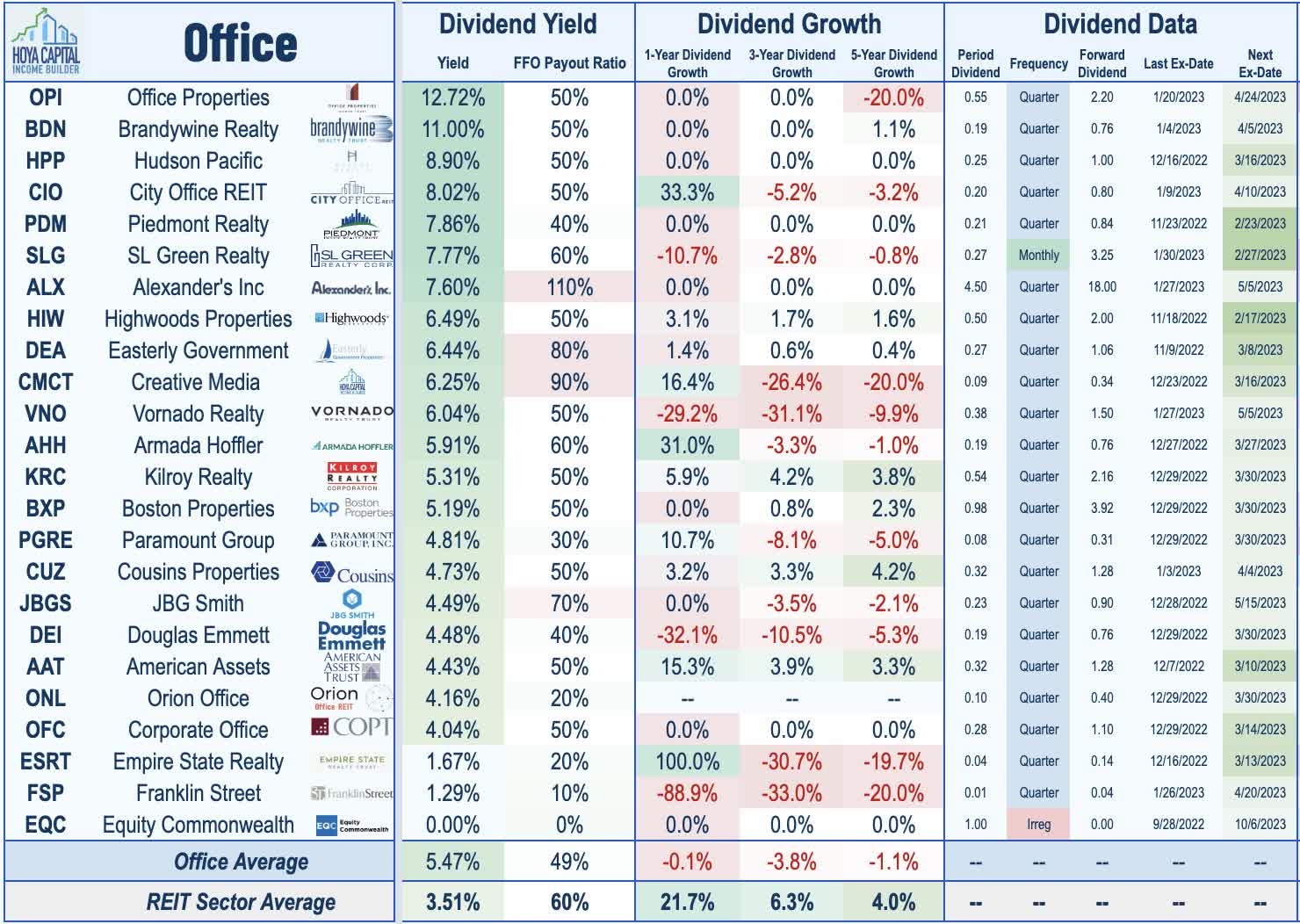

While the growth outlook remains muted, office REIT dividend yields have swelled over the past year amid this post-pandemic pullback. Office REITs now rank toward the top of the REIT sector, paying an average yield of 5.5% compared to the market-cap-weighted REIT sector average of 3.5%, while paying out just 50% of their available Funds from Operations. Seven office REITs boosted their payouts in 2022 - part of a historic wave of more than 120 dividend hikes across the REIT sector in 2022 - while three office REITs (all coastal-focused REITs) reduced their dividends last year: SL Green ( SLG ), Douglas Emmett ( DEI ), and Franklin Street ( FSP ).

{kind=link}

Current payout ratios suggest that these distribution levels should be sustainable, as a whole, but several REITs with weaker balance sheets remain at higher risk for a potential dividend cut if fundamentals weaken further. There is a wide range of dividend distribution strategies employed by the 23 REITs within the sector, with yields ranging from 12.7% from Office Properties ( OPI ) to a low of 0% from Equity Commonwealth ( EQC ). As noted, seven office REITs have hiked their dividends over the past year including Kilroy ( KRC ), Cousins ( CUZ ), Paramount ( PGRE ), and City Office ( CIO ) along with diversified REITs Armada Hoffler ( AHH ) and American Assets ( AAT ).

{kind=link}

Takeaways: Plenty Of Pain Already Priced-In

Pressured by the painfully slow "return to the office" with daily utilization rates still hovering 50% below pre-pandemic norms three years after the pandemic began, Office REITs have been the weakest-performing property sector since the start of the pandemic and dipped another 40% in 2022. We were bearish on the sector for much of the decade prior to the pandemic given their premium valuation, low dividend yields, and underappreciated cap-ex burden, but we now see the consensus swinging too far in the negative direction with office REIT valuations below that of even more structurally-troubled property sectors including Class B and C malls. We've brought our exposure up to more-or-less "sector neutral" across the balance of our portfolios, skewing this exposure towards Sunbelt and secondary markets with net population growth, shorter commute times, and a more favorable industry mix.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Office REITs: Pain Is Priced In