OCCIO - OFS Credit Company: I'm Passing On The 25.6% Yield

2023-05-08 10:54:02 ET

Summary

- OFS Credit is paying out a 25.6% yield to its shareholders from a portfolio of CLOs.

- The closed-end fund has lost more than half of its value since its 2018 IPO.

- Around 41% of its distributions have been driven by return of capital.

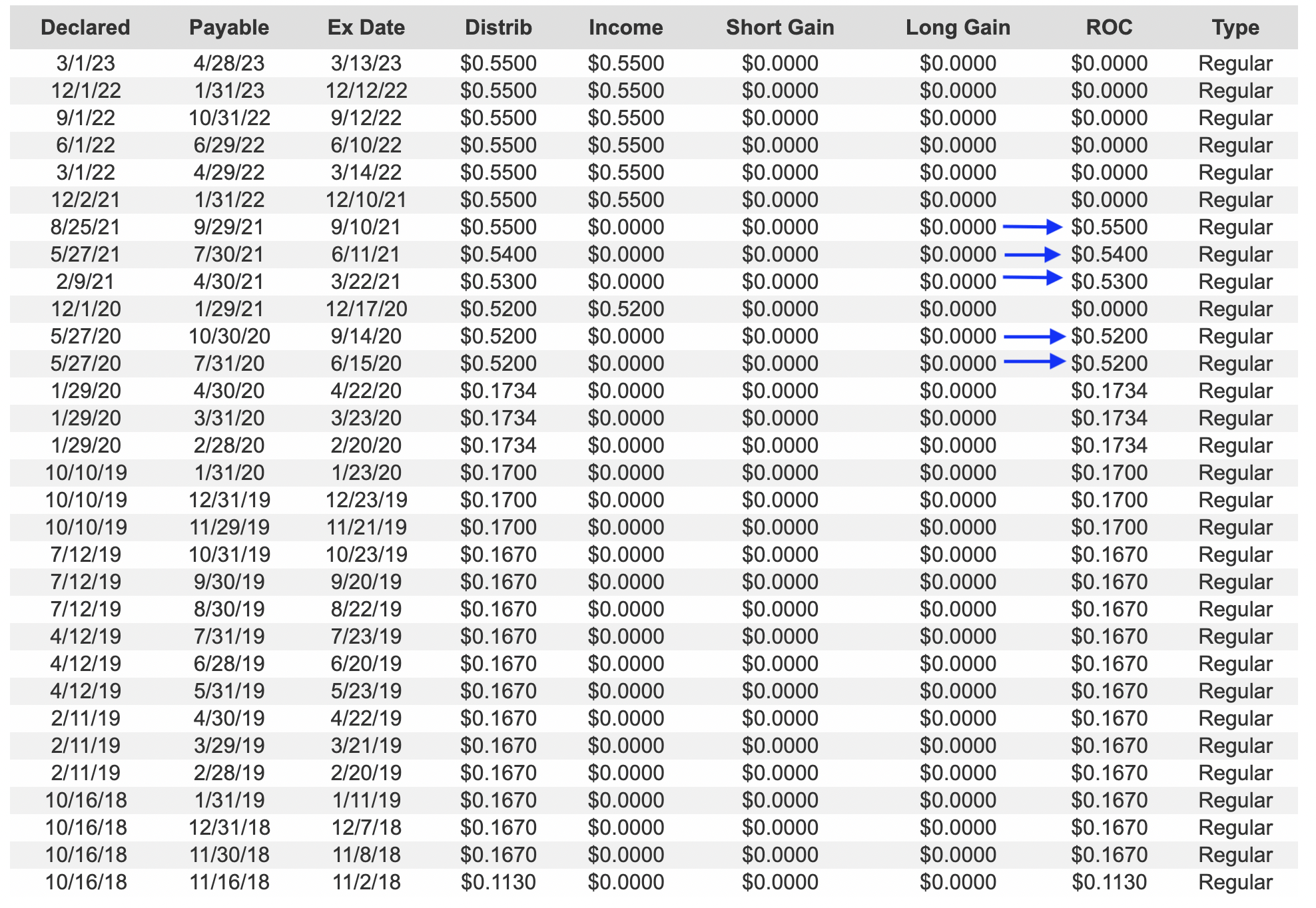

OFS Credit Company ( OCCI ) last declared a quarterly distribution of $0.55 per share , in line with the prior payout, and for a 25.6% forward yield. The Chicago-based closed-end fund invests in collateralized loan obligation ("CLO') debt and equity securities. The target is income, and this has surprisingly remained stable against the broader disruption wrought by the rapid rise in the Fed funds rate on the US capital markets over the last year. CLOs are highly levered products built from different tranches of pooled first lien and senior secured loans.

The yield has been trending up since early 2022 with the CEF down by 21.5% over the last year. Apart from the 2020 jump when OFS switched from monthly to quarterly payouts, the CEF has increased its per share quarterly payouts from $0.52 to $0.55, a 5.8% increase from 2020. As OFS is a CEF and mainly invested in the equity tranche of CLOs, it's been able to meet its distributions from a mix of the interest and principal payments from the underlying loans and from a return of capital. The former better aligns with long-term shareholder value creation against a 14.34% expense ratio. The latter leads to an erosion of principal and diminished downstream income potential.

Return Of Capital And The Illusion Of Stability

The heavy use of ROC has rendered the CEF a significantly less attractive investment. ROC was used judiciously before the switchover to quarterly payouts and continued to be used up until the fourth quarter of 2021. There have been five ROC payments over the last 12 payment periods to place ROC as a percentage of total distributions at 41%.

{kind=link}

Prior to the distribution switchover, the CEF was solely paying out its distributions from ROC. Whilst the CEF looks to have inverted this trend since the first quarter of 2021, there is always the risk that distributions slip back into ROC if there's any disruption to the CLO portfolio. Hence, shareholders hoping that the relatively recent income-based distributions herald the start of a longer-term trend could be left wanting. Critically, ROC is a broadly unreliable income source within the context of net asset value and is an artificial inflation of the CEF's actual yield.

{kind=link}

OFS's total market value currently sits at $95.78 million, with its price per share of $8.60 set against a portfolio with a net asset value per share that sat in between $8.82 and $8.92 as of the end of March. NAV per share has been trending down and stood at $10.13 as of the end of January.

The CEF went public in October 2018 at a $20 offering price and has since shed more than half of its value. A reflection of both ROC and headwinds experienced by CLOs as a result of the marked rise in interest rates. I expect these headwinds to remain through 2023 as interest rates come to a crescendo.

{kind=link}

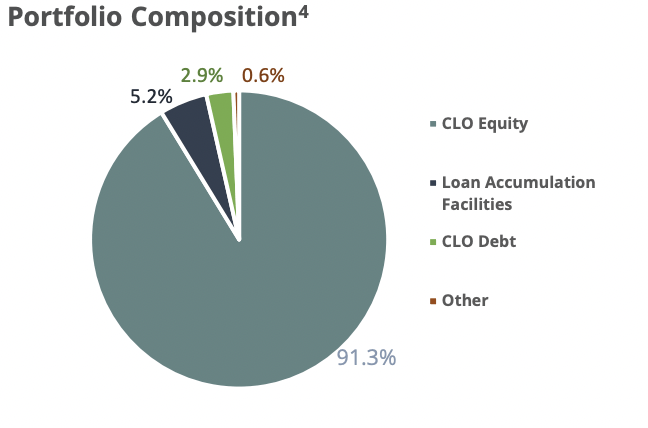

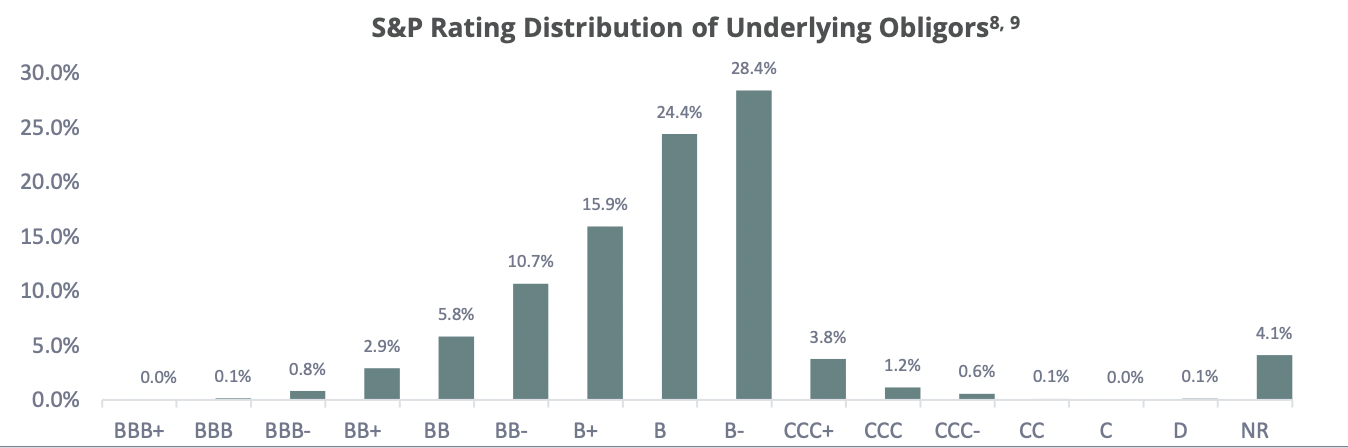

OFS's portfolio is highly concentrated on the riskiest part of CLOs formed from portfolios of low credit-rated with a small allocation to unrated loans. The bulk of its underlying obligors is rated a B-, essentially junk, by the S&P. This should drive greater income but comes with an enhanced scope of default and losses, especially if the US falls into a recession.

{kind=link}

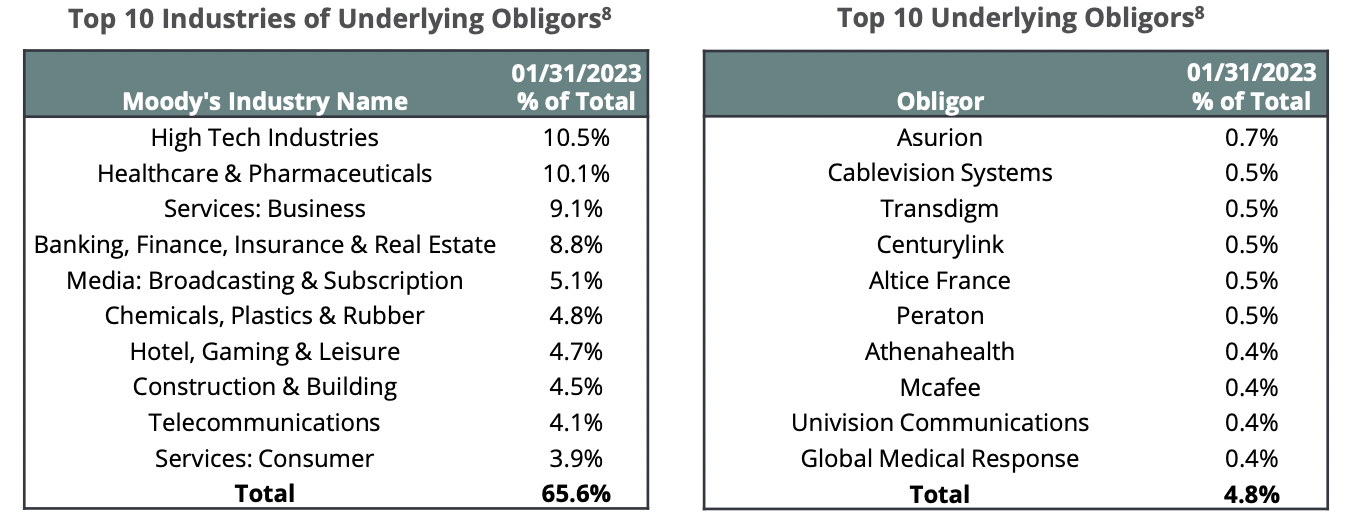

This is mitigated by the broad spread across several industries, with high tech, healthcare and pharmaceuticals, and business services forming the largest three industries from underlying obligors as of the end of January. Further, and due to the nature of CLOs, its top 10 obligors did not constitute more than 4.8% of its portfolio. Hence, the US would likely have to realize a deep recession for these large companies to experience difficulties repaying their loans.

The Series C Term Preferreds

OFS Credit Company Series C Term Preferred Stock ( OCCIO ) offers a distinct way to play the CLO portfolio without direct exposure to the still-declining NAV. There are a few things to note here. Firstly, they're monthly paying, which provides a more frequent stream of income versus the quarterly paying commons. They're also currently trading at a small $1.78 discount to their par value.

{kind=link}

Further, they're term preferreds with their maturity date set for the end of April 2026. Hence, whilst their headline coupon of $1.53125 currently offers a 6.6% yield on cost, they're set to realize materially less volatility over the next few years until maturity. They're trading past their call date which came up at the end of last month, so OFS could redeem them at any time, but this is unlikely ahead of the maturity date. Critically, whilst the yield is materially lower than the common shares, this offers less risk and a price firmly anchored around its $25 par value. The yield on both is incomparable at 25.6% versus 6.6%, so the commons will continue to make the better choice for yield chasers. Overall, I'm neutral on the CEF.

For further details see:

OFS Credit Company: I'm Passing On The 25.6% Yield