CMSD - OGE Energy: A Lot To Like But Too Expensive Today

Summary

- OGE Energy enjoys remarkably stable cash flows, which should appeal to investors in today's economic environment.

- The company's region is growing and OGE should be able to deliver a 9% to 11% total annual return over the next three to four years.

- The company is now a pure-play electric utility, which may endear it to ESG funds that control substantial assets.

- The company has one of the strongest balance sheets in the industry and can easily maintain its dividend.

- The stock looks too expensive today and it may make sense to wait for it to come down before buying in.

OGE Energy Corp. ( OGE ) is a regulated electric utility that operates in Oklahoma and Arkansas. The utility sector has long been a favorite of conservative investors due to the financial stability of most companies in the sector along with their generally high dividend yields. OGE Energy is certainly not an exception to this as the company yields 4.15% at the current price. Admittedly, Oklahoma and Arkansas are not necessarily the area that many people will think of when considering a utility investment, but that certainly does not prevent the company from having a number of attractive characteristics. One of the most important of these is that this company is growing at a fairly rapid pace and should be able to give investors a respectable total return. Unfortunately, the stock is a bit pricey today, which we will discuss over the course of this article. As some readers might recall, I discussed this company back in March and was reasonably impressed with its strong renewable credentials. The overall thesis has not changed but we have had a few quarters pass since that time so it's certainly worth revisiting this company to update our thesis and determine if we need to take any action with respect to our portfolios.

About OGE Energy Corp.

As stated in the introduction, OGE Energy is a regulated electric utility that operates in Oklahoma and Arkansas. This is not a particularly heavily populated area of the country as indicated by the fact that the company only has 887,000 customers in its service territory. This does not stop the company from having many of the characteristics that attract conservative investors to the utility sector. One of the most important of these is that the company has remarkably stable cash flows over time. We can see this quite clearly by looking at the company’s operating cash flow. This chart shows these figures over the past eleven quarters:

{kind=link}

As we can see, with the notable exception of a few quarters, the company’s operating cash flows are generally pretty similar over time. This is due to the fact that the company provides a service that's typically considered to be a necessity. After all, how many of us do not have electricity in our homes? The fact that we have such a service has become a staple of our modern way of life. As such, most people will prioritize paying their electric bills ahead of making discretionary expenses during times when money gets tight. This is something that's very important today as inflation has been devastating the budgets of many households. As I have mentioned in numerous recent articles, there are many people that are now working second jobs or performing other tasks outside of their primary work in order to obtain the extra money that they need to pay their bills and eat. In such a situation, it can be a good idea to be invested in a company whose cash flows will not really be affected by a decline in discretionary spending like a utility. As we can see above, OGE Energy certainly qualifies here.

Naturally, as investors, we like to see more than simple stability. We like to see a company that we are invested in grow and prosper. OGE Energy is well positioned to do this in two ways. The first way is by taking advantage of the demographics of its service area. The populations of both Oklahoma and Arkansas are growing at a fairly quick pace right now, which has allowed the company to grow its customer base. Over the past year, OGE Energy has increased its number of paying customers by 1.2%:

OGE Investor Presentation

Admittedly, a 1.2% customer growth rate may not seem like much but it's more than many other electric utilities have managed to deliver over the same period. This is nice because increasing its customer base is one of the only ways that a regulated utility can grow. It should be pretty obvious how this would be the case. After all, the more customers that the company has, the more people it has paying their monthly bills. All else being equal, this should result in more revenue and more money making its way down to the company’s bottom line.

There's another way that OGE Energy is likely to produce growth, which is quite nice because it's unlikely that anyone would be very happy with a mere 1.2% growth rate. This is by expanding its rate base. The rate base is the value of the company’s assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the amount that it charges its customers in order to achieve that rate of return. The usual way that a company increases its rate base is by investing money into modernizing, upgrading, and expanding its utility infrastructure. OGE Energy is currently planning to spend $4.75 billion on this over the 2022 to 2026 period:

OGE Investor Presentation

This should allow the company to grow its earnings per share at a 5% to 7% compound annual growth rate over the period. When we combine this with the 4.15% current yield, investors should be looking at a 9% to 11% total average annual return, which is certainly reasonable for a utility company.

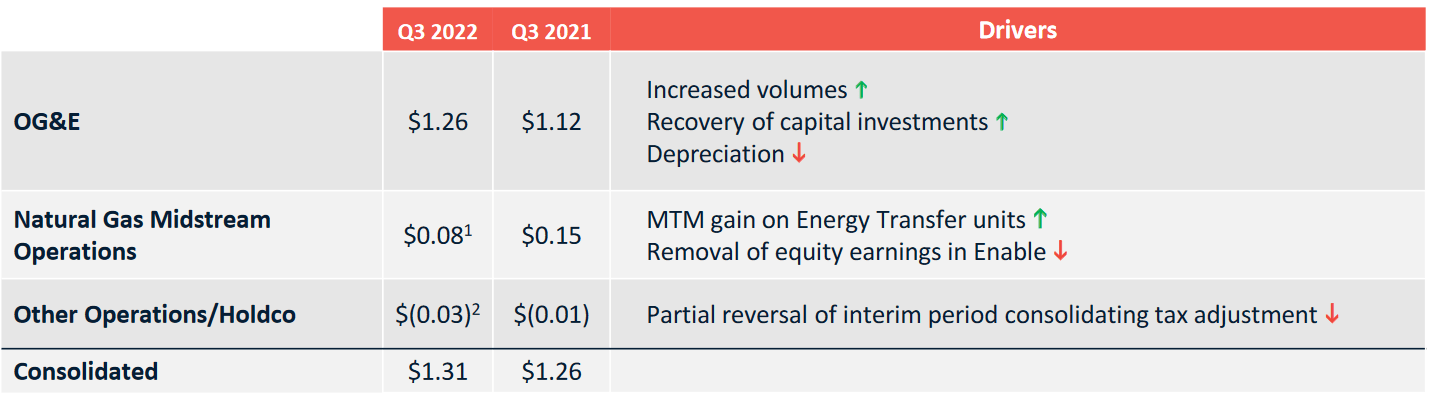

This would be a continuation of the company’s historic earnings per share growth. Over the 2015 to 2021 period, OGE Energy’s electric utility business grew its earnings per share by 33%. In the third quarter of 2022, the company’s electric utility reported earnings per share of $1.26, which represents a 12.5% increase over the $1.12 that it reported in the prior-year quarter. That's well above the company’s projected growth rate based on its customer base growth and rate base growth over the next four years, so unfortunately, it does appear that we should expect to see the company’s growth slow down. With that said though, it should still be able to produce sufficient growth to satisfy its investors.

As some eagle-eyed readers may have noticed, I referred specifically to the electric utility’s earnings per share in the previous paragraphs. This is important because OGE Energy previously owned partnership units of Energy Transfer ( ET ), which is a midstream oil and gas company. The company acquired these units back in December 2021 when it sold Enable Midstream to Energy Transfer. The company sold off all of its Energy Transfer units during the third quarter of 2022 so it's now a pure-play electric utility. This could have a slight negative impact on the company’s earnings over the next few quarters as the company derived $0.08 per share from this unit during the third quarter:

{kind=link}

Over the long term though, the company only being a pure-play electric utility may not be a bad thing. First of all, we have been hearing a lot about the electrification of the economy. This refers to the conversion of things that are traditionally powered by fossil fuels to the use of electricity instead. The most common areas that are being targeted for conversion are transportation (electric cars) and space heating. There are some activists that picture a world in which everything is powered by renewable-produced electricity and no fossil fuels are consumed. While that world is a long way off, the fact that OGE Energy is now a pure-play electric utility may increase the appeal of the company in the eyes of those activist investors. This could be particularly important for attracting the attention of the various environmental, social, and governance funds that have gained a substantial amount of money over the past few years. As I pointed out in a recent article , these funds had a total of $357 billion in assets under management as of December 2021, which is a number that continues to increase. Indeed, State Street states that it has $516 billion in its environmental, social, and governance funds today. As these funds are generally unlikely to invest in a company with fossil fuel exposure, the fact that OGE is now a pure-play electric company may begin receiving investments from these funds. When we consider the size of these funds, we can see that they could drive up the stock or at the very least put a floor under it to prevent it from falling too far in the event of a downturn. This is something that we should be able to appreciate somewhat, particularly from the perspective of risk aversion.

Financial Considerations

It's important that we look at the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. As this is usually accomplished by issuing new debt and using the proceeds to repay the maturing debt, this can cause a company’s interest expenses to increase following the rollover depending on the conditions in the market. In addition, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a firm’s cash flows to decline could push it into financial distress if it has too much debt. Although electric utilities like OGE Energy tend to have remarkably stable cash flows, this is still a risk that we should not ignore.

One metric that we can use to evaluate a company’s financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. The ratio also tells us how well a company’s equity can cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of Sept. 30, 2022, OGE Energy had a net debt of $4.0919 billion compared to a total shareholders’ equity of $4.4407 billion. This gives the company a net debt-to-equity ratio of 0.92. This is quite low for an electric utility as we can clearly see by comparing OGE Energy to some of its peers:

| Company |

| Net Debt-to-Equity Ratio |

| OGE Energy Corp. |

| 0.92 |

| DTE Energy ( DTE ) |

| 2.22 |

| Eversource Energy ( ES ) |

| 1.41 |

| Entergy Corporation ( ETR ) |

| 2.14 |

| CMS Energy ( CMS ) |

| 1.81 |

As we can clearly see, OGE Energy has a considerably lower ratio than its peers. It is, in fact, one of the few electric utilities nationwide that has a net debt-to-equity ratio of less than 1.0. It also represents a substantial improvement over the 1.24 ratio that the company had the last time that we looked at it. This is a good sign from a risk management perspective as it clearly tells us that the company is not employing too much leverage in its financial structure. As such, the risk that is presented by its debt is unlikely to be something that we really need to worry about.

Dividend Analysis

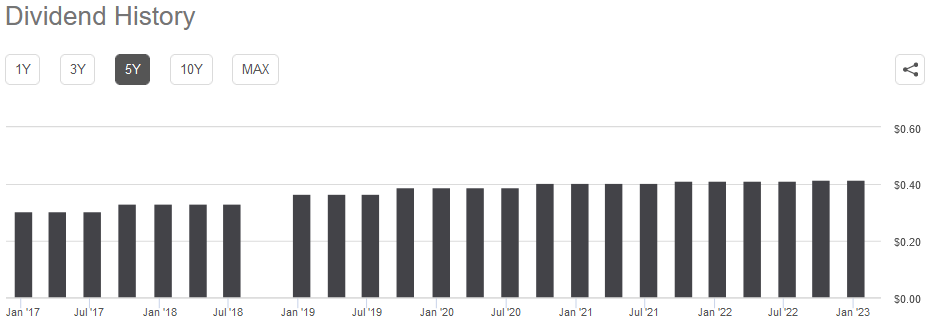

As mentioned in the introduction, one of the reasons why investors purchase shares in utilities is because of the high dividend yields that they tend to possess. OGE Energy is no exception to this as the company boasts a 4.15% dividend yield at the current share price. OGE Energy also has a history of increasing its dividend annually:

{kind=link}

This long history of dividend growth is something that's quite nice to see during inflationary times like the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it feel as if an investor is getting poorer and poorer with the passage of time. The fact that the company increases its dividend with time because the higher amount of money that we receive from the company each year helps to maintain the purchasing power of the dividend. As is always the case though, it's critical that we ensure that the company can actually afford the dividend that it pays out. After all, we do not want to find ourselves the victims of a dividend cut that both reduces our incomes and almost certainly causes the company’s stock price to decline.

The usual way that we evaluate a company’s ability to pay its dividend is by looking at its free cash flow. The free cash flow is the amount of money that was generated by a company’s ordinary operations and is left over after it pays all of its bills and makes all necessary capital expenditures. This is therefore the amount that the company has available to do things like buying back stock, reducing its debt, or paying a dividend. During the third quarter of 2022, OGE Energy reported a levered free cash flow of $674.9 million but only paid out $82.0 million in dividends. Clearly, the company easily covered its dividend during the latest quarter.

However, the third quarter was somewhat unusual due to the substantial amount of money that the company received from the sale of its Energy Transfer common units. We should therefore look at the company’s trailing twelve-month numbers to try and balance out the impact of this. During the twelve-month period that ended Sept. 30, 2022, OGE Energy had a negative levered free cash flow of $551.7 million, which is clearly not enough to pay any dividend.

However, it's common for utilities to finance their capital expenditures through the issuance of debt and equity. This is due to the enormous costs involved in constructing and maintaining utility-grade infrastructure. The company will then pay its dividends out of operating cash flow. During the twelve-month period that ended Sept. 30, 2022, OGE Energy had an operating cash flow of $948.6 million but only paid out $328.5 million in dividends. Thus, it completely covered its dividend with quite a lot of money left over. Overall, the company’s dividend appears to be reasonably sustainable.

Valuation

It' s always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a sure-fire way to generate a suboptimal return on that asset. In the case of a utility like OGE Energy, one ratio that we can use to value it is the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company’s forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 could be a sign that the stock is undervalued relative to the company’s forward earnings growth and vice versa. However, there are very few stocks with such a low ratio in today’s still-hot market. Thus, the best way to use the ratio is to compare OGE Energy with its peers in order to determine which stock currently offers the best relative valuation.

According to Zacks Investment Research , OGE Energy will grow its earnings per share at a 5.00% rate over the next three to five years. This seems a bit low considering the population growth in the region and the company’s rate base growth over the period but it is still the very low end of the projections that we used earlier. At this earnings per share growth rate, OGE Energy has a price-to-earnings growth ratio of 3.71 at the current stock price. Here is how that compares to the company’s peer group:

| Company |

| PEG Ratio |

| OGE Energy |

| 3.71 |

| DTE Energy |

| 3.25 |

| Eversource Energy |

| 3.15 |

| Entergy Corporation |

| 2.64 |

| CMS Energy |

| 2.65 |

As we can pretty easily see, OGE Energy appears to be quite richly valued at the current price. However, it does have a considerably more attractive valuation than what we saw the last time that we looked at the company. This could be due to the company attracting money from environmental, social, and governance investors and funds but the actual cause hardly matters. It still looks like it may be best for the price to become more attractive before buying into the company.

Conclusion

In conclusion, OGE Energy does have a few things to like. In particular, the company’s location gives it a customer growth rate that exceeds many other utilities. This combined with its rate base growth and high yield gives the company quite an attractive potential total return. Unfortunately, the current stock price appears to be a bit high. This company is certainly worth watching to see if a reasonable price presents itself though as it does have a lot to offer to any portfolio but it may not be the best purchase today.

For further details see:

OGE Energy: A Lot To Like But Too Expensive Today