OGE - OGE Energy: Positive Demographics And Growth Potential Questionable Valuation

2023-08-16 10:07:19 ET

Summary

- OGE Energy Corp. reported disappointing Q2 2023 earnings results, missing analyst expectations for revenues and earnings.

- Revenues were down year-over-year, but earnings and operating cash flow were up, showcasing stability in challenging market conditions.

- The company's growth opportunities lie in its expanding customer base and plans to invest in infrastructure to grow its rate base.

- The company is positioned to deliver a 10% to 12% total annual return on average over the next five years.

- OGE Energy Corp. is arguably overpriced relative to its peers, which is perhaps the only real problem with it.

On Wednesday, August 9, 2023, Oklahoma-based regulated electric utility OGE Energy Corp. (OGE) announced its second quarter 2023 earnings results. At first glance, these results were quite disappointing, as the company failed to meet the expectations of its analysts both in terms of top line revenues and bottom line earnings. For its part, the market appeared to be indifferent to the company's performance, as the share price remained reasonably stable until it got caught up in the market selloff that began on Friday, August 11:

{kind=link}

However, a closer look at these results may bring a bit of sobriety to the market's reaction. One of the things that investors typically appreciate with utility stocks is their overall stability through any market conditions. OGE Energy's earnings reports actually showcased this, as its revenues were down year-over-year, but earnings and operating cash flow were actually up. The fact that revenues were down is somewhat disappointing, but both of the other metrics are far more important. Indeed, the fact that both of these bottom-line figures were up year-over-year is something that is very nice to see right now considering that the leading economic indicators are projecting that the United States will enter a recession in the very near future, if it is not already in one. The fact that OGE Energy is well positioned to continue to deliver this growth going forward regardless of economic conditions further adds to the appeal. Unfortunately, the company appears to be somewhat expensive relative to its peers today so it may be smart to be cautious before making an investment in it.

Earnings Results Analysis

As regular readers are no doubt well aware, it is my usual practice to share the highlights from a company's earnings report before delving into an analysis of its results. This is because these highlights provide a background for the remainder of the article as well as serve as a framework for the resultant analysis. Therefore, here are the highlights from OGE Energy's second quarter earnings report :

- OGE Energy reported total revenue of $605.0 million in the second quarter of 2023. This represents a 24.72% increase over the $803.7 million that the company reported in the prior-year quarter.

- The company reported an operating income of $147.5 million during the reporting period. This represents a 4.16% decline from the $153.9 million that the company reported in the year-ago quarter.

- OGE Energy reported that its load (electric consumption) increased by 3.5% year-over-year during the most recent quarter. This is a continuation of the load growth trend that the company has been experiencing over the past few years.

- The company reported an operating cash flow of $309.1 million in the current quarter. That compares very favorably to the negative $50.8 million that the company had in the corresponding quarter of last year.

- OGE Energy reported a net income of $88.4 million in the second quarter of 2023. That represents a 20.93% increase over the $73.1 million that the company reported in the second quarter of 2022.

It seems essentially certain that the first thing that anyone reviewing these highlights will notice is that OGE Energy's revenues declined year-over-year. Indeed, I specifically pointed this out in the introduction to this article. The company did not provide a specific reason for this in its earnings report, but revenues reported by Oklahoma Gas & Electric, which is the regulated electric utility that accounts for the majority of the company's business, reported that its operating revenue was down across the board:

| Q2 2023 |

| Q2 2022 |

| Residential |

| $223.1 |

| $294.6 |

| Commercial |

| $161.0 |

| $197.7 |

| Industrial |

| $53.1 |

| $82.5 |

| Oilfield |

| $47.2 |

| $79.5 |

| Public Authorities and Street Light |

| $54.0 |

| $72.6 |

| System Sales Revenue |

| $538.4 |

| $726.9 |

| Integrated Market |

| $18.8 |

| $43.0 |

(all figures in millions of U.S. dollars.)

The company did see its sales of electricity decline in a few of these areas. For example, residential electric consumption went down year-over-year, but commercial consumption of electricity went up by the same amount. This could be a sign that people spent less time at home and began to spend more time at work, which is consistent with what we have seen in some other areas of the country as fear of the coronavirus has abated and people continue to return to their normal lives.

Another factor here that could have affected the company's revenue is that Oklahoma Gas & Electric utilizes some natural gas plants to generate electricity. Natural gas prices were substantially higher in the second quarter of 2022 than they were in the second quarter of 2023. The company itself points this out as its weighted average natural gas fuel cost was $2.619 per kilowatt-hour in the reporting period compared to $7.613 per kilowatt-hour a year ago. The company can pass these costs through to its customers via "fuel adjustment clauses," which could have resulted in the company's revenues being much higher last year simply due to these costs. The fact that its operating income did not vary nearly as much as its revenue year-over-year supports this theory.

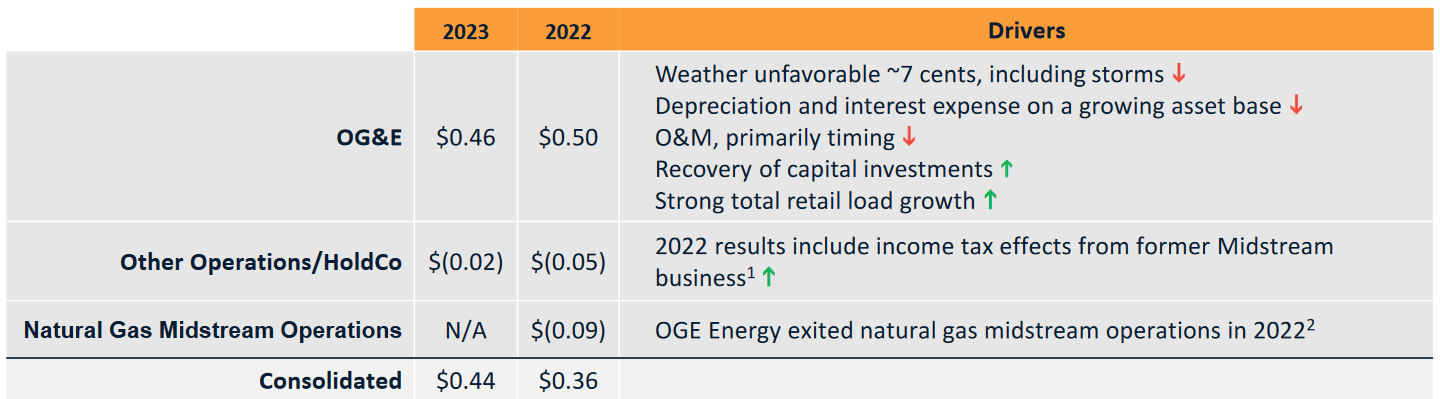

Another thing to consider when comparing the company's performance to the prior-year quarter is that OGE Energy exited the natural gas midstream business last year. The company points this out in its earnings press release:

"Earnings for the second quarter of 2022 included a loss of $0.09 per share per diluted share from natural gas midstream operations, which OGE Energy fully exited in 2022 through the sale of all Energy Transfer (ET) units. Beginning in 2023, OGE Energy no longer has a Natural Gas Midstream Operations reporting segment."

This appears to have had a bigger impact on its income than on its revenue. The total top-line revenues that the company reported during the second quarter of this year and the second quarter of last year match what it says the electric utility business alone brought in. As stated in the quote above, though, the company's Natural Gas Midstream Operations business actually dragged down its net income a year ago. When we adjust for this, the electric utility business actually did worse year-over-year:

{kind=link}

This is quite clearly visible here. The company's reported earnings per share were $0.44 in the second quarter of 2023 compared to $0.36 per share a year ago. However, the electric business alone actually saw its earnings per share decline by $0.04 year-over-year. In fact, were it not for that $0.09 per share loss from the divested midstream business, OGE Energy would have reported earnings per share of $0.45 in the prior-year quarter. Thus, the company did worse in the most recent quarter on an apples-to-apples basis. This is not something that we like to see.

Fortunately, it did not appear that things are really that bad here. The biggest negative drag on its earnings in the most recent quarter was the weather, which actually makes sense. There were quite a few damaging thunderstorms and tornadoes during the second quarter. For example, an outbreak of severe thunderstorms left hundreds of thousands of people across Oklahoma without power in early June. In April, an outbreak of tornadoes across the Great Plains resulted in at least eight tornadoes leaving a path of destruction across parts of Oklahoma. The company estimates that the lost revenue from the power outages and the costs of repairing its infrastructure following this storm reduced its earnings per share by $0.07 compared to the same period in 2022. If it was not for this $0.07 per share impact, the electric company and OGE Energy overall would have posted much stronger results than a year ago. This could also be a contributor to the lower revenues that the company experienced and which we discussed earlier. Unfortunately, there is not much that we can do about the weather, and this is just a risk that accompanies investing in an electric company serving the Great Plains.

Growth Opportunities

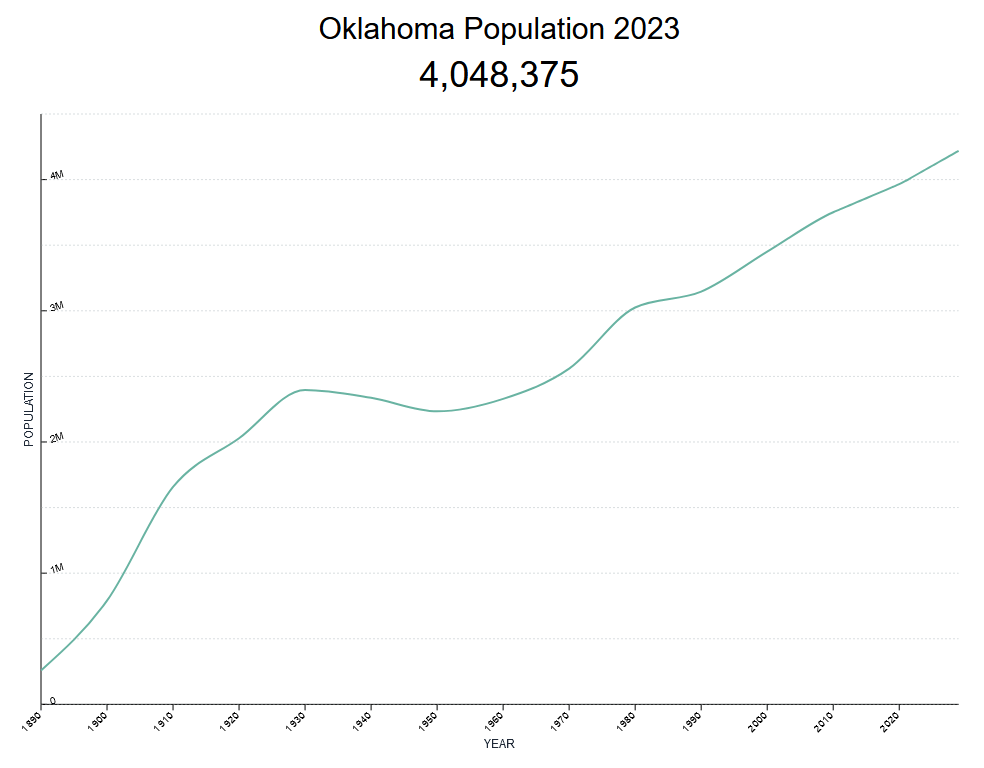

One story that we do not hear very much about in the mainstream media has been that people have been leaving some of the high-cost-of-living states on the West Coast and Northeast to the Heartland and Deep South. Oklahoma has been a beneficiary of this trend. As we can see here, Oklahoma's population has been growing its population at a 0.71% annual rate, which is expected to continue until at least 2029:

{kind=link}

This has benefited OGE Energy. The company reports that its customer base has been growing by around 1.0% annually since 2020:

OGE Energy

At the end of the second quarter of 2023, the company's customer count stood at 891,755, which represents a 0.83% increase over the 884,397 that it had at the end of the year-ago quarter. This is roughly in line with the state's population growth rate. Overall, this is something that is very nice to see because growing its customer base is one of the only two ways that a utility company can generate revenue and earnings growth. After all, the more customers that the company has paying their monthly bills, the more total money it will have coming in the door all else being equal. This means that it has more money available to cover its fixed expenses and make its way down to cash flow and profits. Unfortunately, utility companies are typically monopolies that are confined to a limited geographic area so their ability to grow by adding customers is largely out of their control. The fact that OGE Energy's service territory is seeing population growth is thus a good thing for the company's forward growth prospects and it is certainly something that we should appreciate as investors.

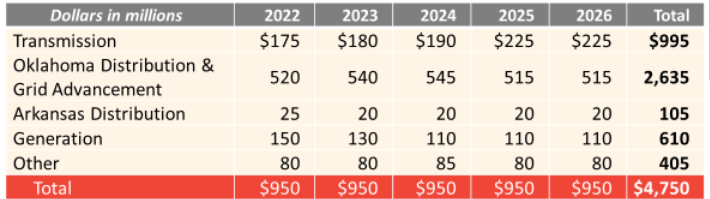

Naturally, though, we are unlikely to be satisfied with a mere 1% annual growth. After all, nearly all companies aim to deliver significantly better than that. Fortunately, OGE Energy does have another method through which it can grow its earnings, and this one is actually within the company's control. The company is primarily aiming to grow its earnings per share by increasing the size of its rate base. The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this allowed rate of return is a percentage, any increase to the rate base allows the company to increase the price that it charges its customers in order to earn that allowed rate of return. The usual way through which a company grows its rate base is by investing money into upgrading, modernizing, and potentially even expanding its utility-grade infrastructure. OGE Energy is planning to do exactly this. The company has unveiled a five-year $4.75 billion capital investment plan intended to improve its infrastructure and grow its rate base:

{kind=link}

This plan should be sufficient to allow the company to grow its earnings per share at a 5% to 7% compound annual growth rate over the 2022 to 2026 period. When we combine this with the company's current 4.88% dividend yield, investors should be looking at a 10% to 12% total annual return on average. That is certainly impressive for a conservative electric utility, as it is actually better than most other electric utilities that I have discussed recently are expected to deliver.

Financial Considerations

It is always important to look at the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is usually accomplished by issuing new debt and using the proceeds to repay the maturing debt. This can cause a company's interest expenses to increase following the rollover in certain market conditions. This could be an especially big concern today because right now the target federal funds rate is at the highest level that has been seen since 2001, although the effective federal funds rate is only at 2007 levels. As such, it is a pretty safe bet that any debt rollover today will result in a company's interest expenses going up. OGE Energy even mentioned in its earnings conference call that rising interest rates are having a negative impact on its financial performance.

In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company's cash flows to decline could push it into financial distress. While electric utilities like OGE Energy usually have remarkably stable cash flows, there have been bankruptcies in the sector before so this is certainly not a risk that we should ignore.

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well a company's equity will cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of June 30, 2023, OGE Energy had a net debt of $4.7568 billion compared to shareholders' equity of $4.3791 billion. This gives the company a net debt-to-equity ratio of 1.09 today. This is, unfortunately, not quite as good as the 1.02 ratio that the company had the last time that we discussed it. That is not a very good trend, but this company usually sees its finances improve significantly in the second half of a year so hopefully that will help it reverse this trend. Here is how the company compares to its peers:

| Company |

| Net Debt-to-Equity Ratio |

| OGE Energy |

| 1.09 |

| DTE Energy ( DTE ) |

| 1.89 |

| Eversource Energy ( ES ) |

| 1.58 |

| Entergy Corporation ( ETR ) |

| 1.92 |

| CMS Energy ( CMS ) |

| 1.91 |

Despite the fact that OGE Energy's net debt-to-equity ratio got worse over the past two quarters, it is still nowhere near as reliant as many of its peers. This is a good sign as it indicates that the company is not overly dependent on debt to finance its operations. We should not have to worry too much about the company's debt load, although we still want to ensure that it does not continue in the wrong direction.

Distribution Analysis

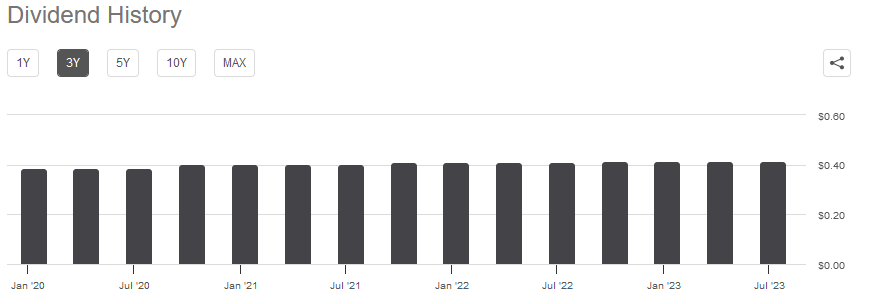

One of the biggest reasons that investors purchase shares of electric utilities like OGE Energy is that they tend to have higher yields than many other things in the market. OGE Energy is certainly not an exception to this, as its 4.88% yield is substantially higher than the 1.46% yield of the S&P 500 Index (SP500). OGE Energy also has a long history of raising its dividend annually, although its past few increases have been very small:

{kind=link}

The fact that the company increases its dividend annually is something that is very nice to see during an inflationary environment, such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it feel as though we are getting poorer and poorer with the passage of time, which is a particularly big problem for anyone that is depending on their portfolio for income. The fact that the company increases the amount that it pays its investors every year helps to offset this effect and ensures that the dividend maintains consistent purchasing power over time. With that said, the company's dividend increases over the past few years have been much less than the current rate of inflation, so it has not been fully successful at mitigating the loss of purchasing power. It is still better than nothing, though.

As is always the case, we want to ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut since that would reduce our incomes and almost certainly cause the fund's share price to decline.

The usual way that we judge a company's ability to sustain its dividend is by looking at its free cash flow. The free cash is the amount of money that was generated by the company's ordinary operations and is left over after the company pays all of its bills and makes all necessary capital expenditures. This is therefore the amount that is available to do things such as reducing debt, buying back stock, or paying a dividend. During the twelve-month period that ended on June 30, 2023, OGE Energy had a levered free cash flow of $349.7 million. This makes this company one of the few utilities to actually achieve a positive free cash flow over that period. The company only paid out $331.4 million in dividends over the twelve-month period, so it did manage to afford the dividends, but the coverage was quite tight. Nevertheless, most utilities have a negative free cash flow, so OGE Energy is still in pretty good shape.

Valuation

It is always critical that we do not overpay for any assets in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility like OGE Energy, we can value it by looking at the price-to-earnings growth ratio. This is a modified version of the familiar price-to-earnings ratio that takes a company's forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. However, there are very few stocks that are undervalued relative to their earnings growth in today's still red-hot market. This is particularly true in the low-growth utility sector. As such, the best way to use this metric today is by comparing OGE Energy's valuation to its peers in order to see which company offers the most attractive relative valuation.

According to Zacks Investment Research , OGE Energy will grow its earnings per share at a 3.65% rate over the next three to five years. This is a bit lower than it should be able to achieve based on its rate base growth, but we will give the benefit of the doubt for now. This earnings per share growth rate gives the company a price-to-earnings growth ratio of 4.62 at the current price. Here is how that compares to the company's peers:

| Company |

| PEG Ratio |

| OGE Energy |

| 4.62 |

| DTE Energy |

| 2.88 |

| Eversource Energy |

| 2.67 |

| Entergy Corporation |

| 2.55 |

| CMS Energy |

| 2.35 |

As we can see here, OGE Energy appears to be incredibly expensive relative to its peers. However, this is assuming that the Zacks earnings per share growth rate is correct. As we discussed earlier in this article, the company should be able to achieve a 5% to 7% compound annual growth rate based on its rate base growth. That brings the company's price-to-earnings growth ratio down to 3.37 on the low end and 2.41 on the high end. Realistically, the company still does not appear especially cheap, but it is not ludicrously overvalued either if its earnings per share growth manages to hit that target range.

Conclusion

In conclusion, OGE Energy Corp.'s second-quarter 2023 results were weaker than we really wanted to see. This was largely due to poor weather conditions during the quarter though, so hopefully it will not be a persistent issue. The company's service area is growing at a fairly rapid pace and it is in the process of taking advantage of that. This should result in fairly respectable total returns for the company's investors going forward. The only issue here is that OGE Energy Corp. stock is arguably overvalued at the current level, but its share price has been declining over the past few days, so maybe a good opportunity to buy in will present itself in the near future.

For further details see:

OGE Energy: Positive Demographics And Growth Potential, Questionable Valuation