REYN - Oil-Dri Corporation Of America: Upside Doesn't Stop Here

2023-05-01 11:40:00 ET

Summary

- Oil-Dri Corporation continues to generate attractive and growing topline and bottom line results.

- This trend doesn't look set to stop soon, and the company has enjoyed favorable market dynamics for years that push profits higher.

- Given how shares are priced, the business does seem to offer a bit of additional upside from here.

I have found that, in life, there are good problems to have and bad problems to have. A bad problem is buying shares of a company only to see that company's share price decline materially. A good problem is to buy shares of a company, to see those shares shoot up, but then to have to worry about when the optimal time to sell is. A good example of the latter situation involves a company called Oil-Dri Corporation of America ( ODC ). This fairly small enterprise, boasting a market capitalization of only $307.5 million, produces and sells sorbent products, including those that are used for agriculture and horticulture, as well as a variant that can be used for cat litter. Frankly, I could spend half this article discussing the specific uses of what it produces. To many, this may not seem like a very exciting place to invest. But the fact of the matter is that management has done incredibly well in growing the company's top and bottom lines in recent quarters. Shares definitely are trading at levels that are closer to fair value than they were previously. But if management can make the second-half of the 2023 fiscal year like the first half has been, I would make the case that some additional upside could exist for those willing to hold on.

Management keeps on delivering

The curse of running a very concentrated portfolio is that, sometimes, you miss out on some really fantastic upside from a company. This is likely a company that you were already bullish on, but you didn't think it was attractive enough to pull the trigger. Such is the case when it comes to Oil-Dri Corporation of America. Back in December of last year, I wrote an article wherein I kept the company rated a 'buy'. Revenue, profits, and cash flows were all growing at a nice clip. But even without that growth, shares of the company looked cheap enough to warrant continued optimism. Since publishing that article , the stock has shot up 26.2% compared to the 5.8% rise seen by the S&P 500. But this was not the only time that I wrote favorably about the enterprise. In August of last year, I initially rated it a 'buy'. The return disparity since then is even more impressive. While the S&P 500 is up only 2.8%, shares of Oil-Dri Corporation of America have seen an upside of 55.2%.

{kind=link}

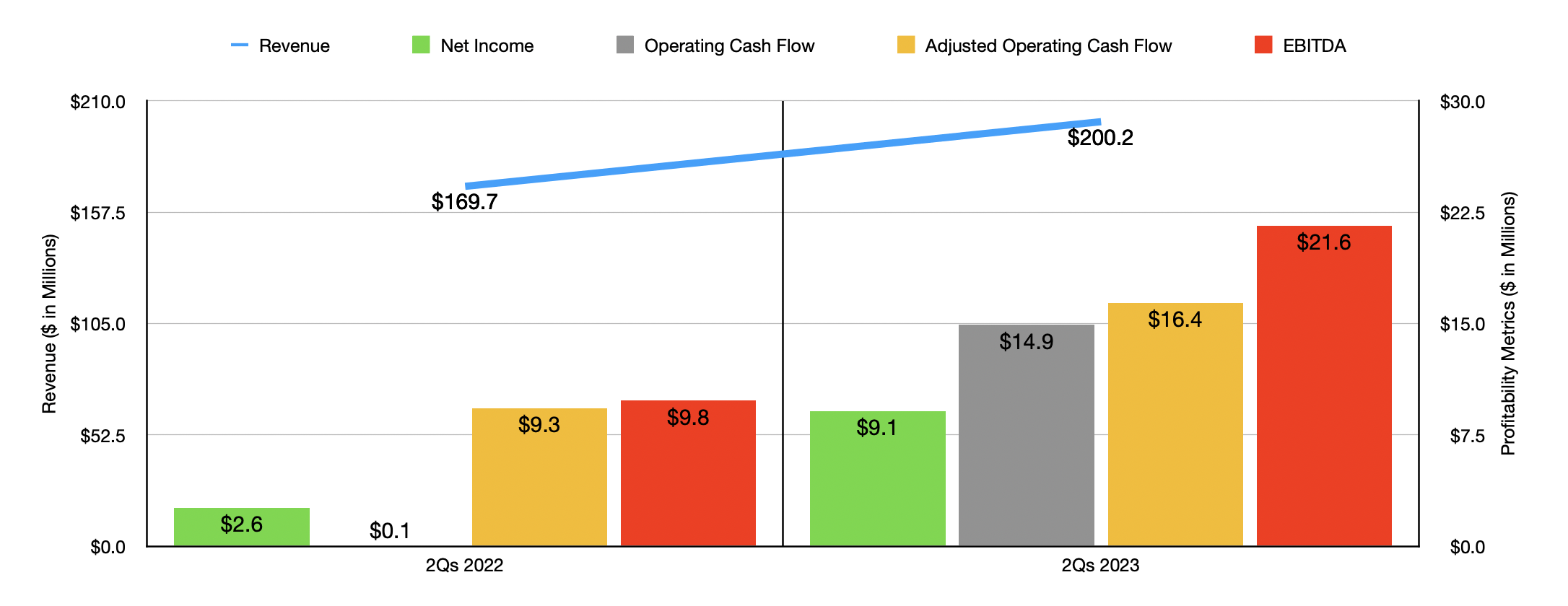

Normally, such a massive upside only comes when a company is being bought out by some other player. But that is not the case here. The fact of the matter is that financial performance has just been that strong. Consider how the company performed during the first half of fiscal year 2023 . Revenue came in at $200.2 million. That's 18% higher than the $169.7 million the business reported one year earlier. Management attributed the sales increase primarily to higher pricing across both of its operating segments. It also helps that demand for its offerings is incredibly high. Management even went so far as to say that they had to take various actions like increasing personnel, expanding production shifts, increasing production equipment, and more, all in order to reduce the backlog. This is absolutely the kind of thing that investors want to see; Strong demand even in the face of higher prices.

When you have a situation like this, you also tend to see drastically higher profitability. Net income, for instance, spiked from $2.6 million in the first half of 2022 to $9.1 million the same time this year. Operating cash flow went from less than $0.1 million to $14.9 million. If we adjust for changes in working capital, we would have seen the number rise from $9.3 million to $16.4 million. Meanwhile, EBITDA more than doubled from $9.8 million to $21.6 million.

{kind=link}

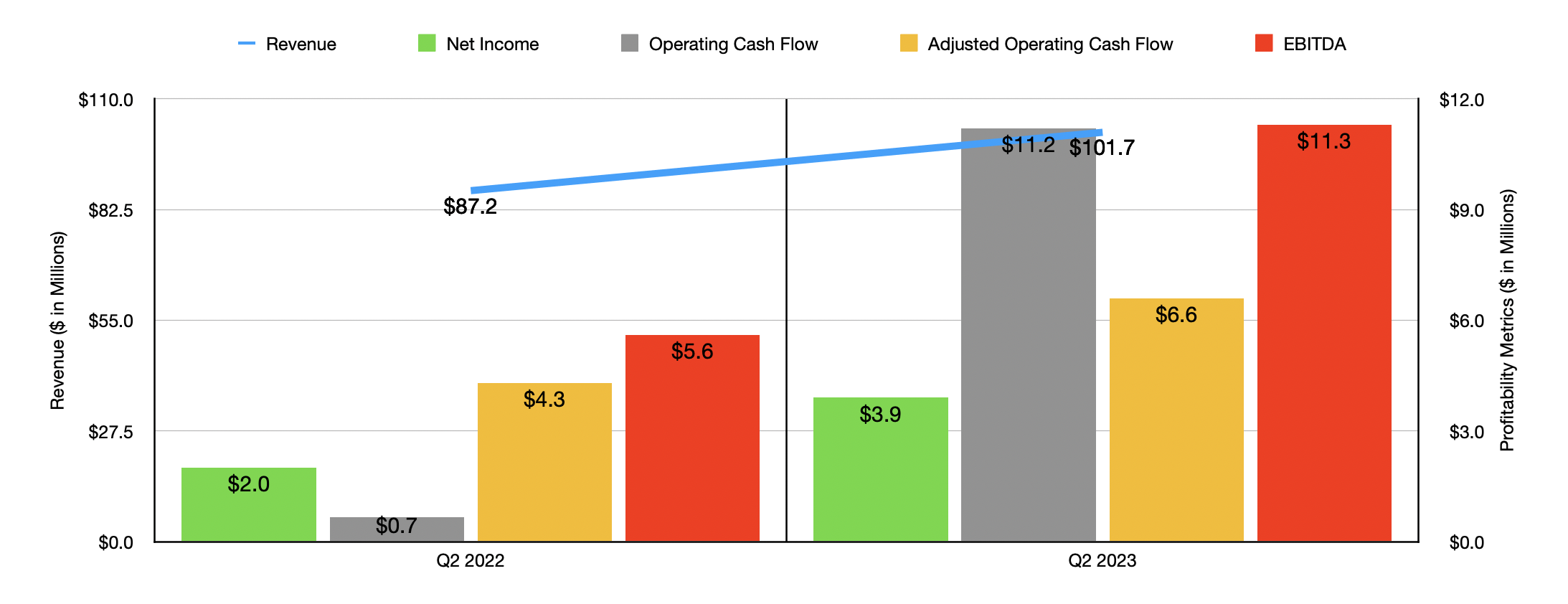

Strong performance for the company has not shown any significant signs of weakening as we move further into the fiscal year. In the second quarter alone, for instance, revenue of $101.7 million was still 16.6% above the $87.2 million reported one year earlier. As you can see in the chart above, profits almost doubled from $2 million to $3.9 million. Operating cash flow, adjusted operating cash flow, and EBITDA are also all up nicely year over year.

{kind=link}

Unfortunately, management has not provided any guidance when it comes to the rest of the year. But if we assume that financial performance in the first half of the year is indicative of where the second-half would be, then we should anticipate net income of around $20 million. This would imply adjusted operating cash flow of $45.1 million and EBITDA totaling $56.2 million. In my opinion, such an assumption would not be unrealistic. After all, one source estimates that the global industrial absorbents market, valued at $3.85 billion in 2022, should climb at a rate of about 4.7% per year until hitting $5.09 billion in 2028. The specialty sorbents market, meanwhile, should climb at a rate of about 8.3% per annum during this time, expanding from $831.5 million in 2021 to $1.46 billion by 2028.

{kind=link}

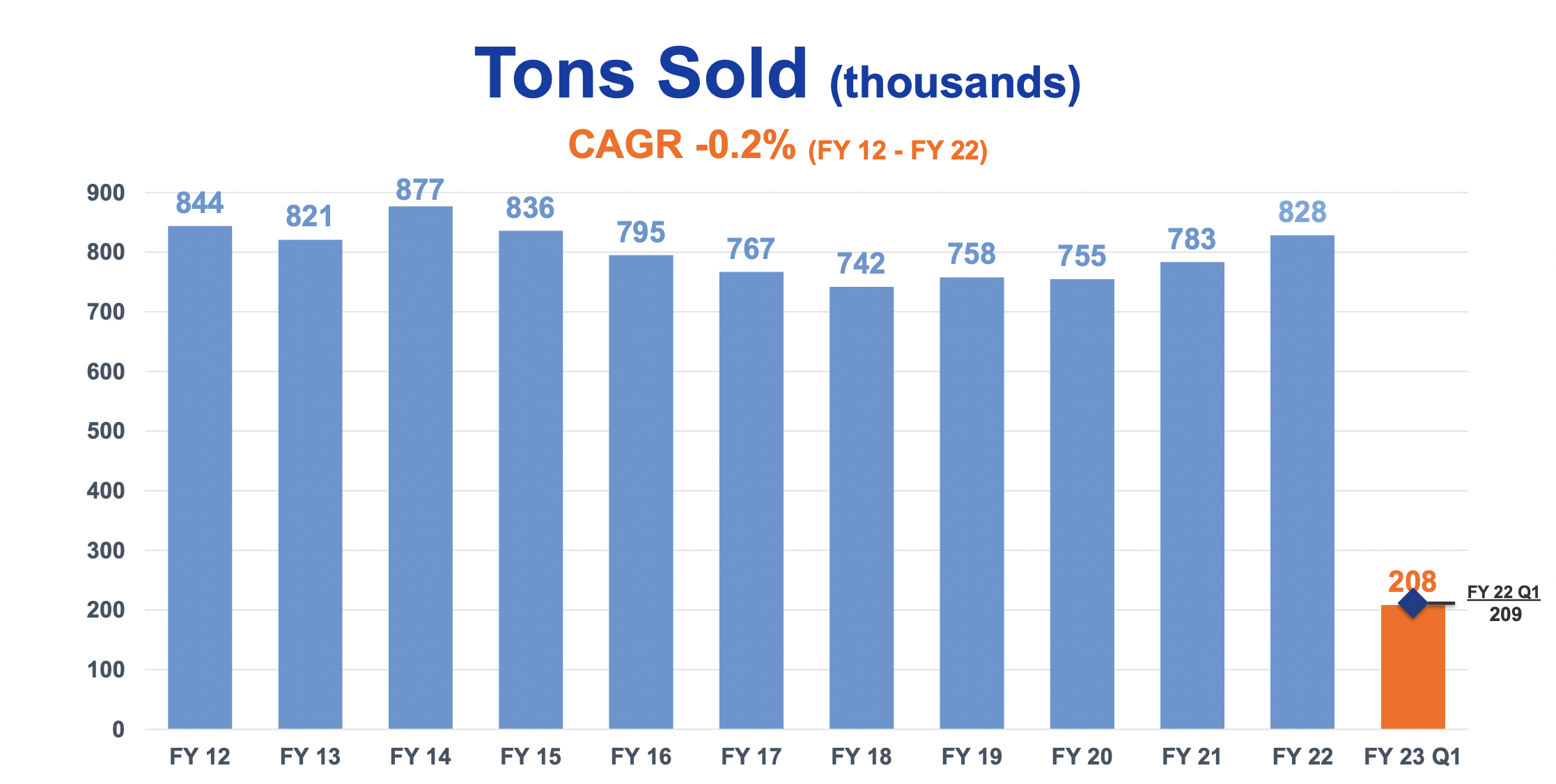

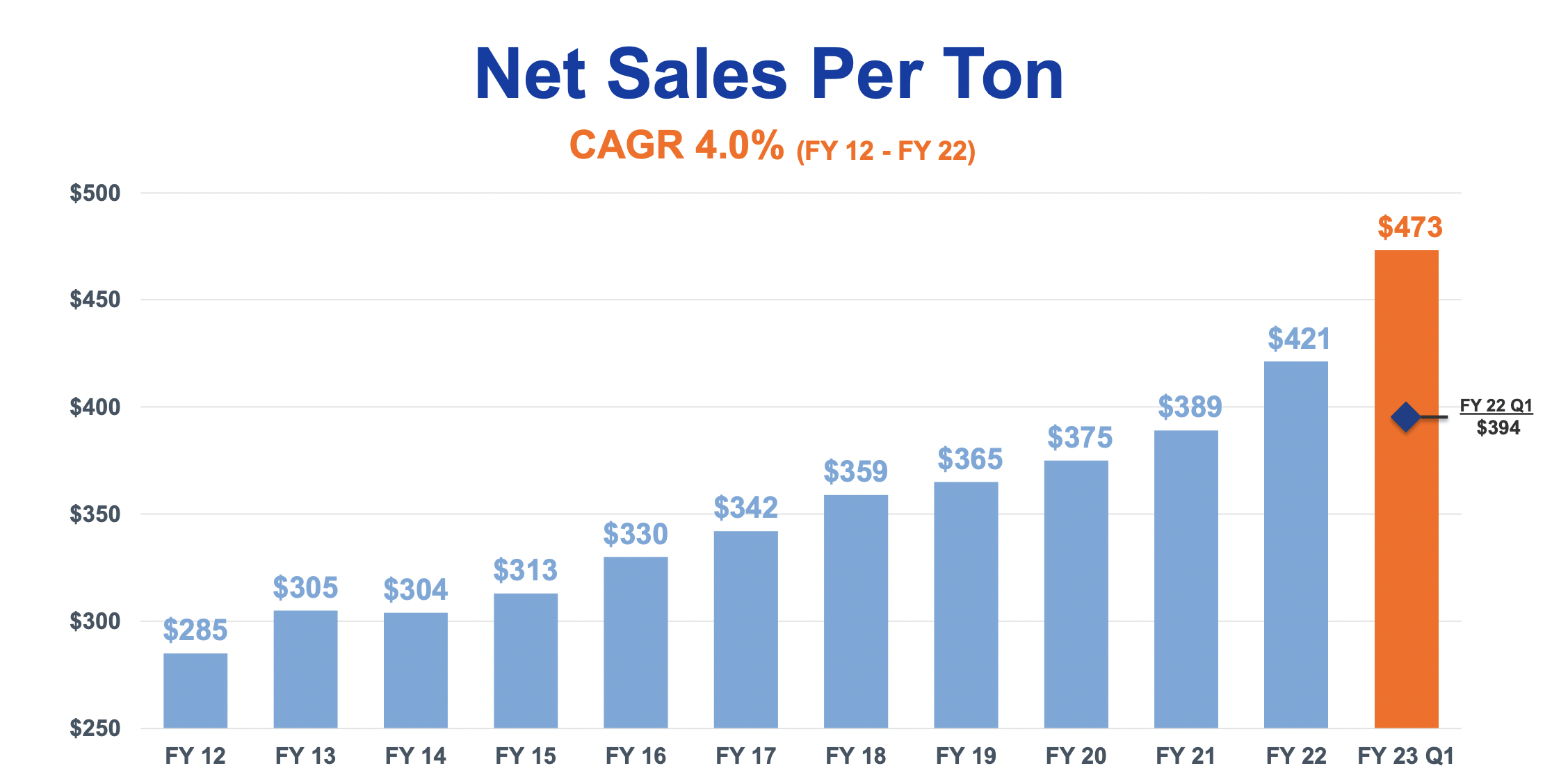

If the past is any indication of the future, then it's likely that higher pricing will play a significant role in any sort of growth that the company experiences. From 2012 through 2022, tons sold by the company actually decreased from 844 thousand to 828 thousand. Though it is true that there has been a general uptrend since bottoming out at 742 thousand tons in 2018. But almost every year during this 10-year window, we saw a rise in revenue per ton. This number shot up from $285 to $421. In the first quarter of 2023, revenue per ton was $473 compared to the $394 reported one year earlier. Management also intends to continue investing in different growth initiatives, such as lightweight cat litter, as well as animal health and agricultural products. Some of this may be organic, but management did say that acquisitions could be on the table.

{kind=link}

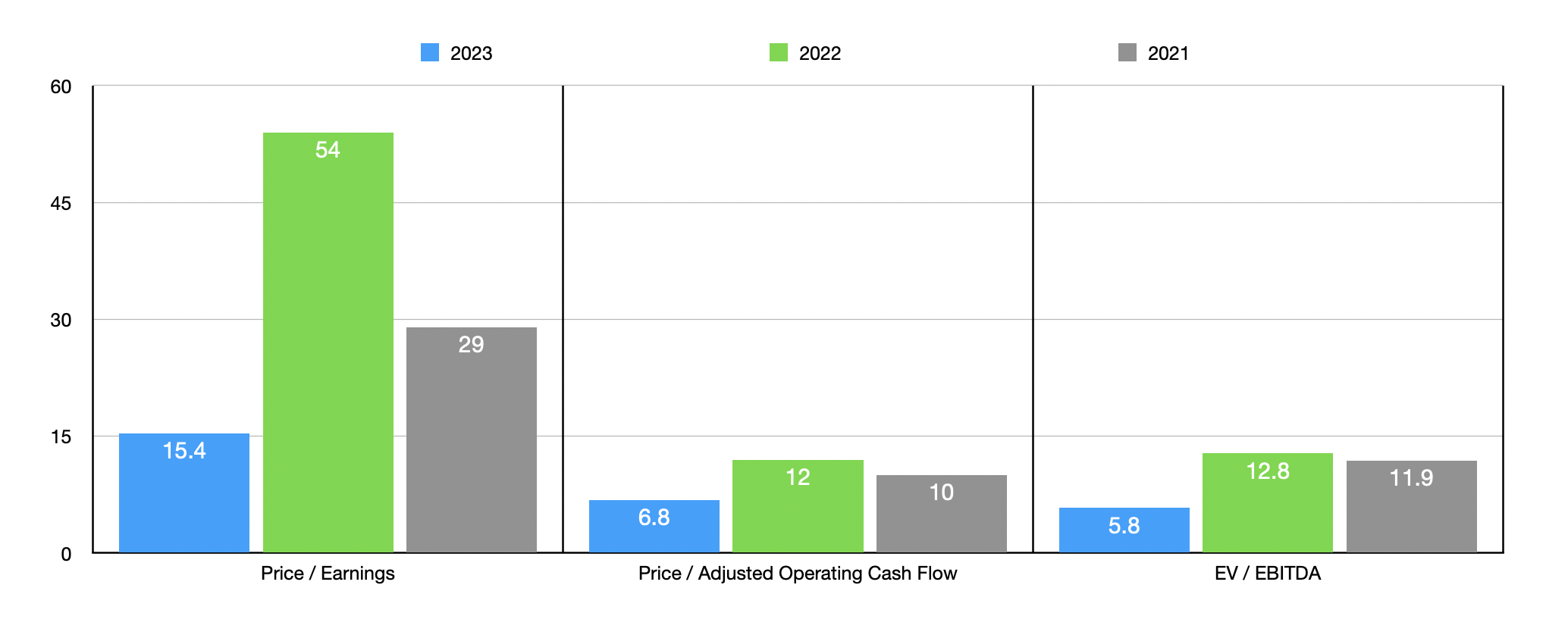

Using the fundamental estimates that I calculated for 2023, as well as the financial results that the company actually generated in 2021 and 2022, I was able to create the chart above. Although shares are not exactly the cheapest on a price to earnings basis, they do look very affordable on a price to operating cash flow basis and on an EV to EBITDA basis. This is particularly true if we assume that financial performance in 2023 turns out as I have estimated. But even if we see results match what they were in 2022, I would say that the company would be no worse than fairly valued. Meanwhile, in the table below, you can see how the company is priced against five similar firms. On a price to earnings basis, two of the five firms were cheaper than our prospect. But when it comes to the price to operating cash flow approach and the EV to EBITDA approach, it ended up being the cheapest of the group.

| Company |

| Price/Earnings |

| Price/Operating Cash Flow |

| EV/EBITDA |

| Oil-Dri Corporation of America |

| 15.4 |

| 6.8 |

| 5.8 |

| Energizer Holdings ( ENR ) |

| 8.5 |

| 11.0 |

| 10.5 |

| Central Garden & Pet Company ( CENT ) |

| 14.8 |

| 22.9 |

| 9.7 |

| Spectrum Brands ( SPB ) |

| 63.2 |

| 17.5 |

| 51.0 |

| WD-40 Company ( WDFC ) |

| 44.0 |

| 134.8 |

| 31.1 |

| Reynolds Consumer Products ( REYN ) |

| 22.6 |

| 26.8 |

| 14.7 |

Takeaway

From all that I can see, the picture for shareholders of Oil-Dri Corporation of America looks upbeat. Although the company may not be as cheap as it was previously, it does look very affordable on a forward basis. Industry data is promising and management continues to make interesting investments. Add all of these factors together, and I do still think that some additional upside exists from here. This is not to say that it's a lot of upside. Clearly, the easy money has been made at this point. But I would say it's enough to warrant a soft 'buy' rating at this time.

For further details see:

Oil-Dri Corporation Of America: Upside Doesn't Stop Here