APA - Oil's Plunge Will Likely Set Crude Up For A Significant Rebound

2023-05-05 06:30:57 ET

Summary

- Oil prices have taken a beating in recent days, with crude prices falling over 14% so far this year.

- This has been caused by concerns surrounding the global economy, but action is likely overplayed at this point.

- The dollar may be having a role to play here and that, combined with fears about the economy, could continue to push crude down near term.

- But fundamentals are current on the bulls' side at this time and prices should recover.

The past couple of days have been very difficult for investors in the energy sector. Crude prices have fallen significantly as investors fear continued rising interest rates and economic uncertainty. In the near term, investors should not be surprised if downside continues. But in the grand scheme of things, this pain will likely be short-lived. For those who still insist on investing in the oil and gas sector, allocating capital toward safer companies like pipelines might be the best way to go. But as prices drop, it would be a wise idea for market participants to bargain-buy the companies that are most exposed to energy price fluctuations. Perhaps the most significant players would be those in the exploration and production space.

Recent pain

{kind=link}

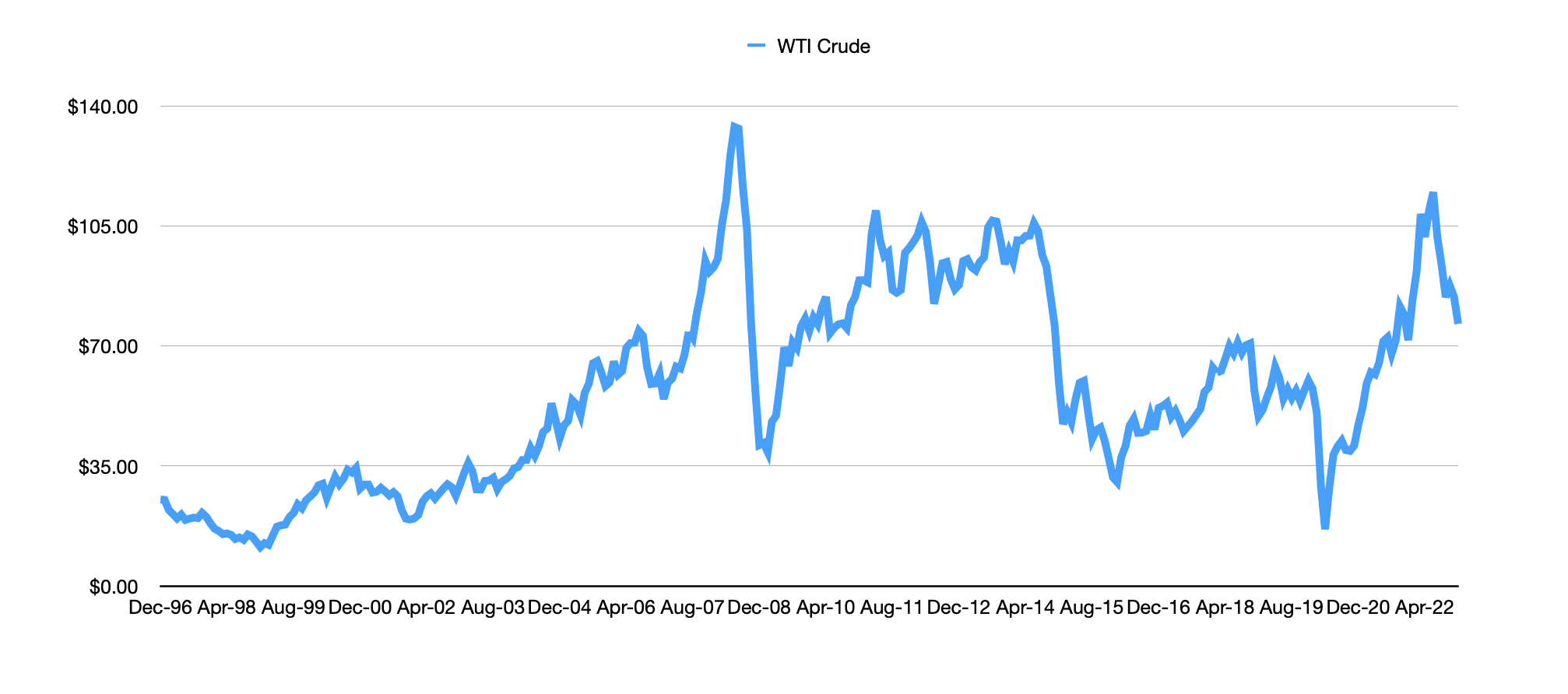

2023 is proving to be a rather difficult year for investors in the energy sector. From the middle of last year through the end of last year, natural gas prices plunged by more than half. And now, oil is experiencing downside. After peaking at $123.64 in March of last year, WTI crude prices plunged 44.5%, settling at $68.60 per barrel as I write this. Year to date, WTI crude prices are down 14.4%. A good portion of this decline has taken place over the past few days. Since the end of April, WTI crude prices are down 10.7%. Much of this drop seems to be attributable to growing concerns over the state of the economy. The banking sector continues to rumble with the collapse of First Republic Bank ( OTCPK:FRCB ) and concerns that PacWest Bancorp ( PACW ) might very well be next. In addition to this, the Federal Reserve decided to raise interest rates and other 0.25%. In recent comments , Chairman Jerome Powell seemed dismissive regarding the collapse of Silicon Valley Bank that started this mess and he indicated that a higher for longer interest rate environment is probable.

Given these developments, investors would be right to wonder what the future holds for crude. In the event that the economy suffers, we would likely see a downward revision in crude consumption. Even a small move in consumption can prove rather painful. Consider that WTI crude prices averaged $105.79 per barrel in June of 2014. By February of 2016, prices were down to $30.32 per barrel. This was caused by production outpacing consumption by only 1.8% in 2015, with forecasts of continued, but smaller, outpacing in 2016. Prices remained low for multiple years after that as well. Part of the problem is that the price elasticity of demand for crude is quite low and the significant lead times and investments required to produce it makes cutting output a long and painful process.

To those who follow the oil data that's out there rather closely, this recent pricing action may seem peculiar. In March of this year, Russia announced that it was cutting its daily production by 500,000 barrels. This was followed up in early April with the news that OPEC+, excluding Russia, was cutting its daily production by another 1.16 million barrels. Around that time, I wrote an article that looked at data provided by both the EIA (Energy Information Administration) and OPEC. The EIA data indicated that we were moving in the direction of having a surplus of crude. On the other hand, the OPEC data indicated the exact opposite. Given this OPEC cut, it seems clear to me that the group of countries is of the opinion that perhaps the picture was not as rosy as they previously thought.

{kind=link}

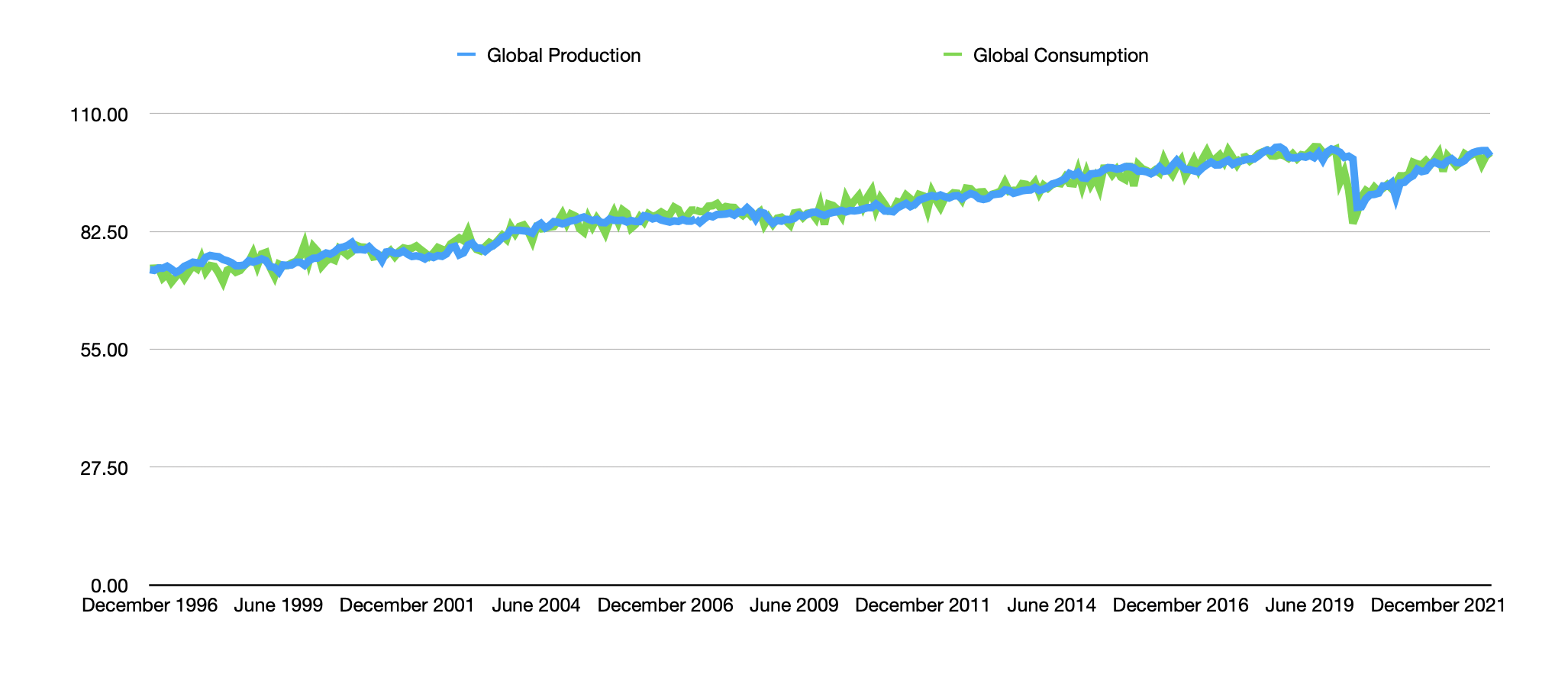

Running the data, however, I start to wonder whether there is any reason to be concerned. In researching for this article, I looked at both the OPEC data and the data provided by the EIA. If we assume that all of their forecasts and other estimates are correct, and that both Russia and OPEC cut production in the amounts that they claimed they would, then the second quarter of this year, according to OPEC, should see oil demand exceed supply by 0.50 million barrels per day. For the third quarter, this should grow to 2.06 million barrels per day, while for the final quarter of the year it should be 2.64 million. Even if we assume that the EIA data is accurate, we should go from having excess demand of 0.35 million barrels per day in the second quarter to 1.05 million barrels per day by the end of the year. This implies rather significant inventory declines if we don't see a corresponding drop in demand.

{kind=link}

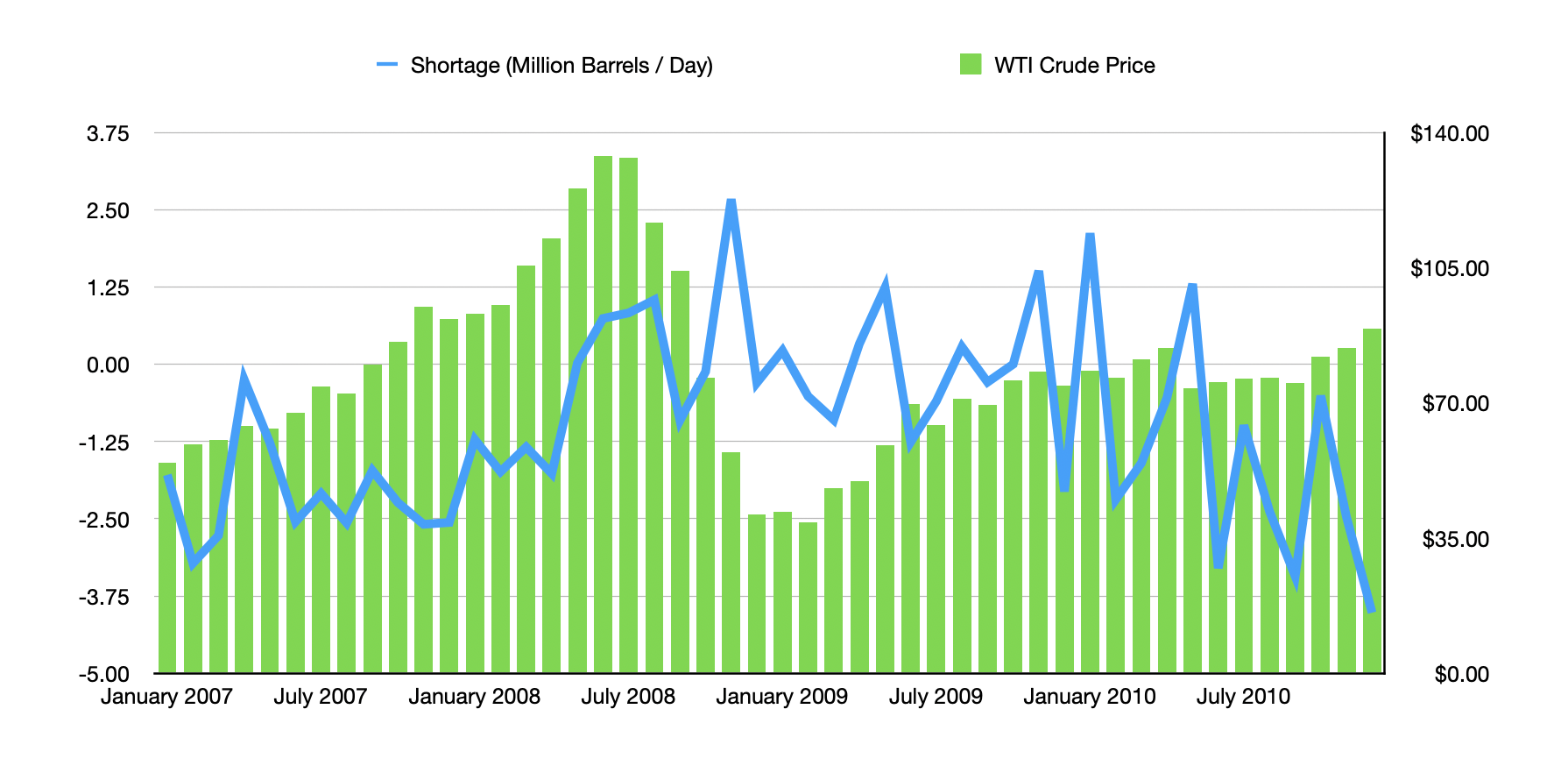

This is not to say that we can't experience or won't experience a drop in oil prices. Quite the contrary. I would like to ignore what happened during the COVID-19 pandemic because that was a self-imposed shutdown of the global economy that resulted in a plunge of oil consumption. Prior to that, the last big economic crisis that we experienced involved the 2008 and 2009 financial collapse. But the data for that time period actually looks interesting as well. For instance, WTI crude prices continued to rise until about the middle of 2008. Prices then plunged as the global economy started to suffer. Despite this, the amount of oil production could not keep up with demand, with the shortage of oil as measured by barrels per day actually climbing until late that year. But we didn't really see a real start to the decline in the daily shortage until late 2009.

Author - Federal Reserve & EIA Data Author - Federal Reserve & EIA Data

{kind=link}

{kind=link}

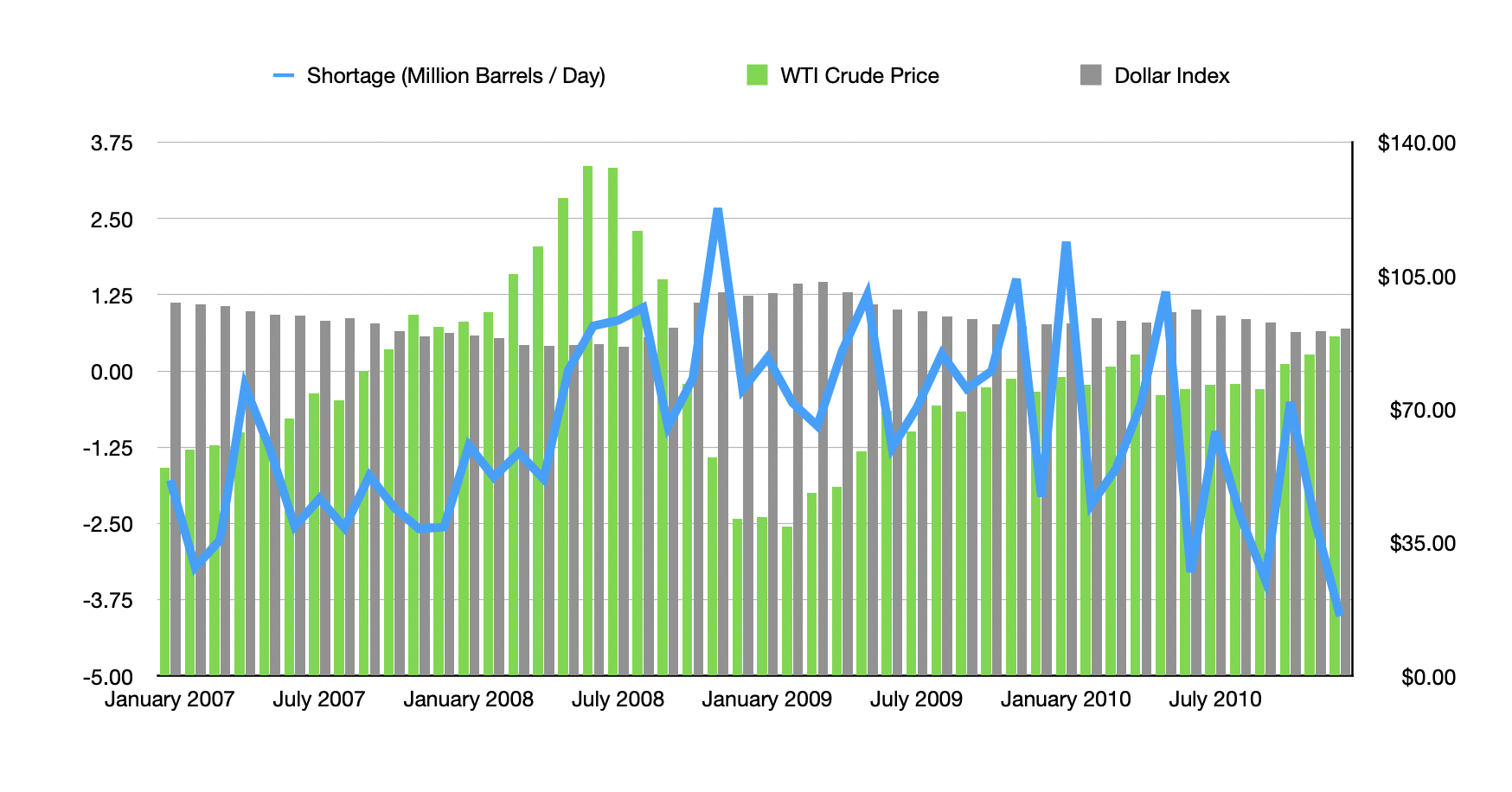

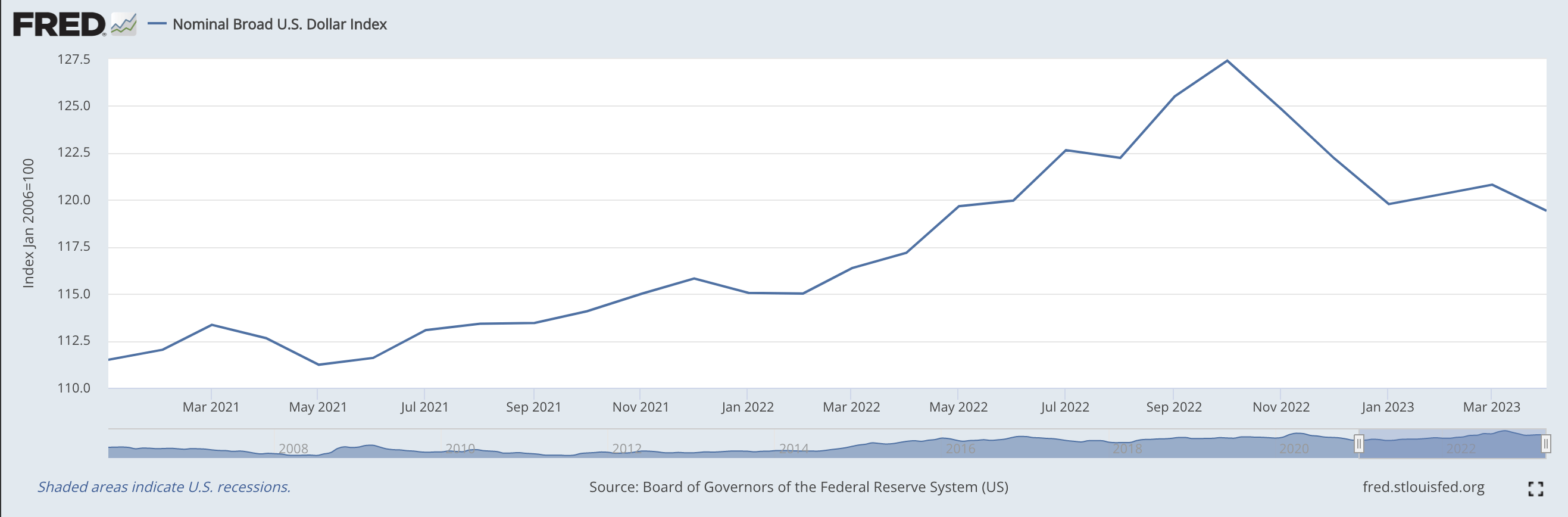

There are other aspects to the oil markets, however. While the balance between supply and demand is ultimately the most important factor, another one is the strength of the dollar. And as you can see in the chart above you can see how this looks next to the prior chart. As the dollar showed weakness in the early days of the financial collapse of 2008 and 2009, crude prices increased. In the chart below, you can see that the dollar has been strong as of late. High interest rates and the relative health of the U.S. economy are responsible for this. But what it does suggest is that, in the short run, weakness in pricing could be driven by that.

{kind=link}

Takeaway

At this moment, it's clear that the bears are having their day. And in truth, we could see that trend continue for the near term. Absent a significant weakening of the global economy, it's difficult to imagine oil prices needing to decline. In fact, it's likely that we are going to be dealing with a more severe shortage of crude over the next few months that could set us up for even more bullish conditions moving forward. The strengthening dollar, combined with an overreaction by market participants in the face of economic circumstances, will likely offset this in the near term. But absent a significant deterioration in demand, I do believe that the outlook from here is largely bullish.

For further details see:

Oil's Plunge Will Likely Set Crude Up For A Significant Rebound