EQIX - Oil Vs. Commercial Real Estate: One Is A Better Buy Today

2023-09-07 08:02:00 ET

Summary

- Timing anything in the markets over the next few months or quarters is extremely difficult, bordering on impossible to do with accuracy consistently.

- But investors can look at data and trends and surmise the kind of economic environment that is most likely to manifest over the next few years.

- Over the last two years, oil stocks have massively outperformed real estate stocks, but in the decade before that, the opposite was the case.

- Is the last two years a temporary anomaly or the new normal? I think it's temporary and about to reverse.

Oil up, REITs down.

That seems to be the story of publicly traded real estate investment trusts ("REITs") over the last few weeks. A rising oil price makes it more likely that headline CPI numbers stop falling or even rebound a little bit higher, which in turn makes it more likely that the Federal Reserve will keep their key interest rate high or perhaps raise it even higher.

In response, the market sours on real estate and other rate-sensitive stocks.

Over the past month or so, the primary risk on the market's mind (certainly, on real estate owners' minds) has shifted from an oncoming recession to persistently high inflation amid a muddling-through economy. The former probably would have ushered in a Fed pivot sooner, while the latter would spur the Fed to keep their policy rate high for longer.

This fear has led to more and more selling of REITs, even high-quality names with trophy real estate, top-notch management teams, and fortress balance sheets.

This offers a lesson in the attractiveness of diversification for long-term buy-and-hold portfolios.

Both year-to-date and since the beginning of 2022, my three largest oil & gas energy holdings--

- the Global X MLP & Energy Infrastructure ETF ( MLPX ),

- Canadian Natural Resources ( CNQ ), and

- Enterprise Products Partners ( EPD )

--have dramatically outperformed the Vanguard Real Estate ETF ( VNQ ).

What I really care about is my total, portfolio-wide dividend income stream continuing to grow regardless of what stock prices are doing. And it has. But it is easier to maintain peace of mind when at least something in my portfolio is going up while most of the rest is falling like a rock.

Of course, there have been a select few REITs that have continued to perform quite well since the beginning of 2022, a few of which have even outperformed the S&P 500 ( SPY ).

As you can see, based on total returns, VICI Properties ( VICI ), which I like to call the "Landlord of Las Vegas" for its ownership of about half the casino resorts on the famous Las Vegas Strip, has outperformed the market by about 15%. Las Vegas was and remains a prime beneficiary of post-COVID "revenge spending."

Meanwhile, after a severe pummeling during the pandemic, Welltower's ( WELL ) primarily senior living portfolio has rebounded strongly as memories of community spread in senior living centers fade in people's minds.

And though not quite outperforming, global data center owner/operator Equinix ( EQIX ) has put up a strong showing in its own right, fueled by a new surge in leasing volume from the artificial intelligence trend.

But these handful of well-performing REITs have been the exception rather than the rule.

In many cases, it has especially been the higher quality REITs that have borne the brunt of the selloff.

Compare, for example, the price performance of VNQ to:

- Alexandria Real Estate Equities ( ARE ) - Class A life science owner/developer

- Crown Castle ( CCI ) - owner of the largest telecom infrastructure network in the US

- Camden Property Trust ( CPT ) - blue-chip Sunbelt multifamily owner/developer with significant exposure to Washington DC

- Mid-America Apartment Communities ( MAA ) - the largest, lightest leveraged, most Sunbelt-concentrated multifamily REIT

- Rexford Industrial Realty ( REXR ) - owner/redeveloper of Class A infill industrial properties exclusively in the extremely supply-constrained Southern California market

All of these high-quality REITs have performed even worse than the poorly performing average for publicly traded real estate companies.

Of course, each of these REITs have their own unique headwinds or difficulties in addition to high interest rates.

- ARE is seeing a huge wave of supply of new life science properties coming to market, from both new development and redevelopment of existing traditional office buildings. Although ARE's long-tenured management team insists that its state-of-the-art buildings in the most innovative research clusters in the nation insulates the portfolio somewhat from the increasing competition.

- CCI is suffering over the next few years from lease cancellations due to the merger of T-Mobile ( TMUS ) and Sprint. The merged company is pursuing synergies by consolidating its tower leases. At the same time, 5G infrastructure investments from the major carriers have slowed down this year. But management still insists that CCI will return to 7-8% growth after the bulk of lease cancellations take effect in 2025.

- CPT and MAA both suffer from the same malady: a big wave of new supply coming to their Sunbelt markets. This will blunt rent growth even assuming population and job growth in these markets continues apace. But population/job growth is expected to continue indefinitely even as new supply will drop off sharply after 1H 2025.

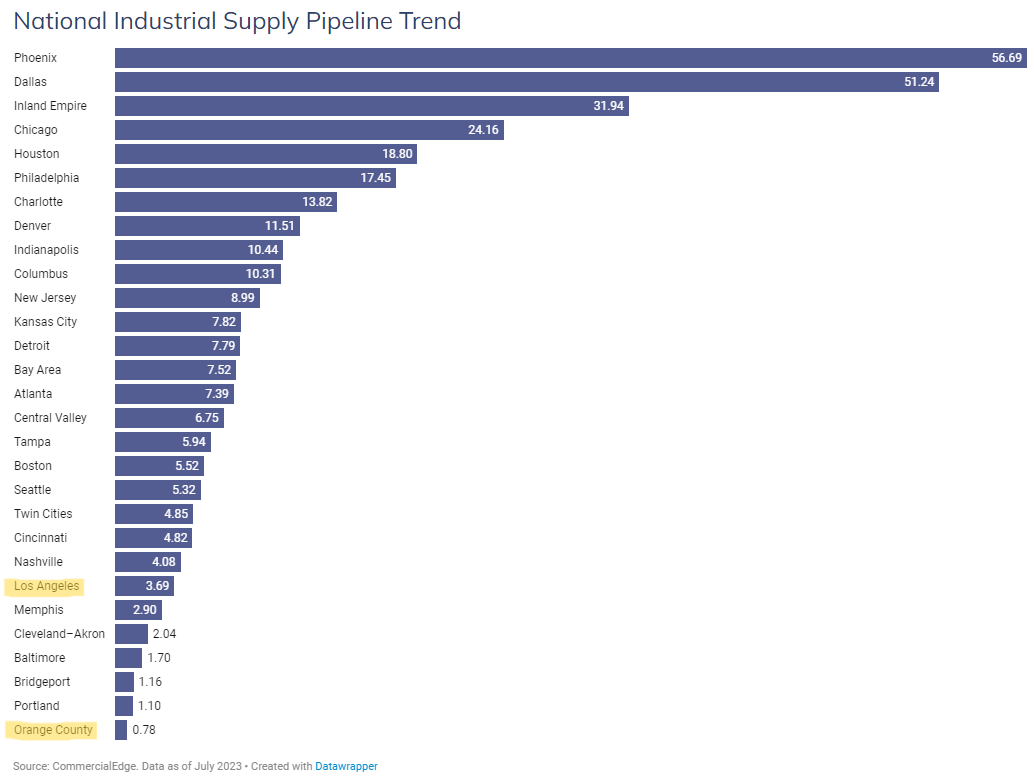

- REXR is not suffering from excess supply worries, unlike many of its industrial, multifamily, and life science peers. But the market does worry about heightened available sublease space and falling rent growth rates in Southern California. While this could be a slight cyclical slump, I'm not worried about the long-term value of REXR's urban infill properties. Compared to a national industrial vacancy rate of 4.4%, LA County's vacancy rate is 3.8%, while Orange County's vacancy rate sits at 3.5%. Plus, largely due to land cost and scarcity, the development pipeline of new industrial properties in SoCal is among the lowest in the nation.

CommercialEdge - National Industrial Report

{kind=link}

Yes, there are lots of properties being developed in the Inland Empire area, but these are mostly large warehouses used as initial hubs for imports from the Port of Los Angeles.

REXR's properties in Los Angeles, Orange County, and to a lesser extent, San Diego, have far less competition coming to market.

Despite the mild to moderate challenges presented above for each of these REITs, the biggest reason they have fallen more than the average for all REITs is the very fact that they're high-quality. Being higher quality previously resulted in a higher valuation multiple, which in turn led to further downside as interest rates rose and REIT fair valuations dropped accordingly.

Oil Vs. Commercial Real Estate: Better Buy Today?

Since the beginning of 2022, energy stocks ( VDE ) have massively outperformed commercial real estate ( VNQ ):

Since then, the environment has been uniquely favorable to energy while being uniquely unfavorable to CRE.

Consumers unleashed their huge pent-up, pandemic-era savings on travel, which obviously benefited energy, while oil & gas producers withheld investment on increased supply, preferring instead to focus on free cash flow.

Meanwhile, CRE suffered from rising interest rates, an increasingly restrictive capital-raising environment, and the beginning of a new wave of supply hitting the market after myriad projects were greenlit during the low-interest-rate, high-rent-growth period of 2021 and early 2022.

Candidly, I could see REITs continuing to underperform for a little while longer. I am not necessarily calling the bottom here. Interest rates are not coming down yet, and the price of oil continues to trend higher.

But when we look further out than the next 6 months to a year, the outlook for REITs improves dramatically against energy companies.

Why?

Consider this. The inflationary surge that peaked in early 2022 was primarily fueled by the incredible growth in the money supply from one-time fiscal spending.

The inflation followed with a lag, largely because the way the government measures housing inflation (the largest single component of CPI and PCE) lags real-time changes in home prices and rent rates by about a year.

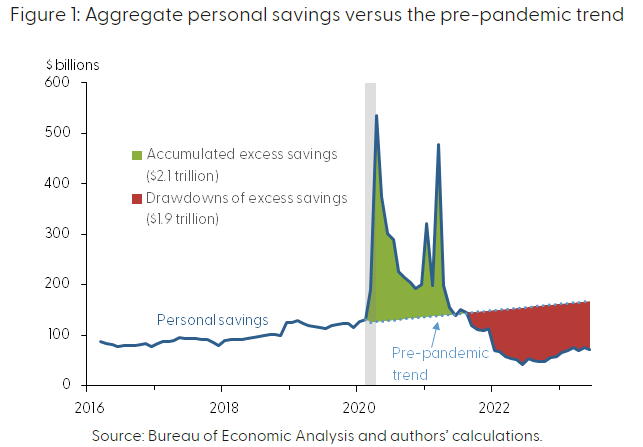

The point is, though, that the most fundamental fuel of consumer spending -- excess savings from fiscal spending -- is now gone.

According to the San Francisco Fed , pandemic-era excess savings had dwindled to about $190 billion by June 2023.

{kind=link}

The researchers believe that excess savings will have been completely depleted by about right now.

Perhaps this is why we are seeing credit card balances soar higher just to sustain the meager, pre-pandemic levels of consumer spending growth still occurring.

Everything on the consumer side is signaling an end to the wave of consumer demand that largely drove inflation.

It makes sense, then, that the 5-year TIPS/bond markets are pricing in a CPI of around 2% (considering that the PCE on which this is based is typically 25 basis points higher than CPI).

While higher than the level of inflation priced in before COVID-19, the bond market's 5-year expectation is still by no means troublesomely high. In fact, it's no higher than the Fed's target.

Thus, in contrast to the last two years being characterized by rising inflation and interest rates, I believe the next two years will be characterized by falling inflation and interest rates.

As such, in terms of oil versus commercial real estate, I think the coming years will look a lot like the 10 years prior to 2022:

I could be wrong or too early in my call, of course. But in terms of likelihood , I believe it's more likely that REITs will outperform energy stocks over the next two years than the other way around.

Bottom Line

One of the biggest mistakes an investor can make is presuming a presently occurring trend will continue forever.

I made that mistake once in assuming that inflation and interest rates wouldn't and even couldn't rise as high as they have in the last few years.

Right now, I think some investors are making the mistake of thinking that inflation and interest rates won't or can't come back down.

While I can't claim the ability to time the bottom in REIT stock prices, the five high-quality REITs discussed above look like phenomenally good values. I'm buying all five of them right now.

I believe REITs in general and those five high-quality REITs specifically will outperform the energy sector over the next two years.

For further details see:

Oil Vs. Commercial Real Estate: One Is A Better Buy Today