OKENF - Okeanis Eco Tankers: A Soft Quarter But The Long-Term Picture Is Unchanged

2023-11-13 12:19:43 ET

Summary

- Okeanis Eco Tankers reported Q3 2023 results, falling below expectations and providing weak guidance for Q4.

- The Q3 earnings decline was due to lower time-charter equivalent revenues, as a consequence of several short-term factors.

- The long-term outlook for crude tankers remains unchanged.

- Okeanis is likely set to deliver among the highest total returns in the sector by the conclusion of the present cycle.

Okeanis Eco Tankers (OKENF) (OSLO:OET), the owner of six Suezmax and eight VLCC vessels, just reported its Q3 2023 results. While the results fell below expectations and may seem underwhelming at first glance (especially considering the somewhat disappointing Q4 guidance), a closer examination beyond the headlines reveals that Q3 was still a solid quarter. More significantly, the best may be yet to come.

Given the shipping sector's substantial volatility, quarter-to-quarter fluctuations often contain more noise than signal. The focus should thus primarily be directed toward assessing the current stage of the cycle investors find themselves in. The good news is that the long-term outlook for the crude tankers trade remains largely unchanged.

With strong insider ownership, capable management, reasonable leverage, a generous dividend policy, some of the lowest breakevens in the sector, and a young scrubber-fitted eco fleet, Okeanis is likely set to deliver among the highest total returns in the sector by the conclusion of the present cycle.

Q3 2023: a soft quarter

Q3 results were unremarkable, particularly when compared with the exceptional Q2 performance, as seasonality exerted downward pressure on rates, exacerbated by a notable underperformance in the Suezmax segment.

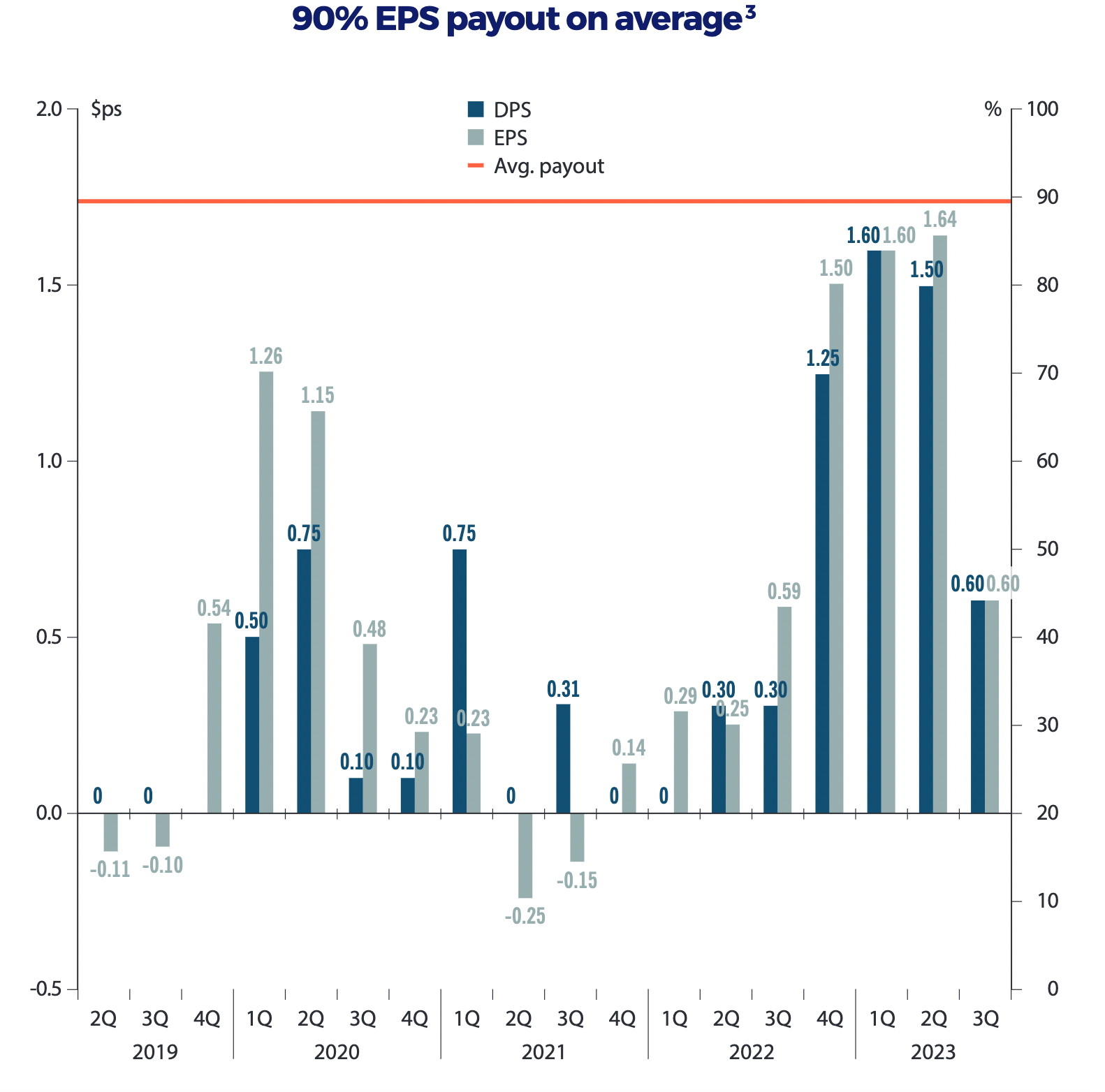

Starting from the bottom line, Okeanis declared adjusted EPS of $0.63 in Q3 2023, down from $1.65 in Q2 2023, but close to last year's results of $0.59 in Q2 2022.

In line with Okeanis' practice of distributing nearly all earnings to shareholders through quarterly dividends, the dividend for Q3 will be $0.60 per share, a decline from the $1.50 per share in the preceding quarter.

OET dividend per share (DPS) and earnings per share (EPS) (Company's Presentation)

{kind=link}

The primary contributor to the reduced earnings was a decline in time-charter equivalent (TCE) revenues. The average TCE stood at $57,900 for VLCCs, a decrease from $71,600 in Q2, and $35,300 for Suezmaxes, down from $72,600.

While Okeanis has a track record of outperforming peers commercially, this quarter presented a more mixed picture. As shown in the table below, comprising data from peers who have already reported Q3 results, Okeanis secured solid fixings in the VLCC sector but slightly underperformed in the Suezmax sector.

| ($/day) |

| Euronav |

| Okeanis |

| International Seaways |

| DHT Holdings |

| VLCC (spot) |

| 42,250 |

| 57,900 |

| 40,961 |

| 44,700 |

| VLCC (timecharter) |

| 48,250 |

| - |

| 35,319 |

| 35,500 |

| Suezmaxes (spot) |

| 42,750 |

| 38,700 |

| 38,708 |

| - |

| Suezmaxes (timecharter) |

| 30,250 |

| 29,700 |

| 30,973 |

| - |

The reason for the relative underperformance was the scheduled dry-docking maintenance of the two Suezmax vessels, Kimolos and Folegandros, in Turkey. This strategic decision aimed to capitalize on softening rates in the Mediterranean. Unfortunately, rates continued to weaken, leading to the two vessels being fixed at a lower rate post-dry-docking compared to the rest of the fleet.

In any case, the fundamental cause of the lower earnings was the widespread weakening of rates during Q3. Specifically, VLCC rates decreased from the low USD 40,000s per day to the low/mid USD 30,000s per day by the quarter's end. Suezmax rates witnessed an even more significant drop, falling from the high USD 30,000s per day to the low/mid USD 20,000s per day.

Several factors contributed to this trading pattern. Firstly, there was a reduction in activity in the refinery sector due to maintenance programs. Additionally, there was a continued drawdown of inventory as oil prices increased in response to OPEC+ production/export cuts, particularly from Saudi Arabia. Lastly, there was a softening in demand, as global GDP growth faced challenges from higher interest rates.

Except for the last factor, all other factors are set to reverse in the next few months, with the added benefit of seasonality coming into play. The winter months typically witness an upturn in freight rates for various reasons, including increased exports from Saudi Arabia due to cooler weather reducing domestic demand for air conditioning, heightened demand from refineries coming out of maintenance season, and longer wait times at ports and canals.

Stronger quarters ahead

Guidance for Q4 was mostly in line with the weak Q3, with 90% of spot days for VLCCs already fixed at an average TCE of $40,900, and 35% of spot days for Suezmaxes fixed at a significantly better TCE of $56,600. Seasonal factors, OPEC production cuts, and softening demand have continued to exert downward pressure on rates throughout the ongoing quarter.

However, there has been a significant strengthening of rates in the last few days. Consequently, it was mentioned during the conference call that the management anticipates fixing the remaining days at materially higher rates.

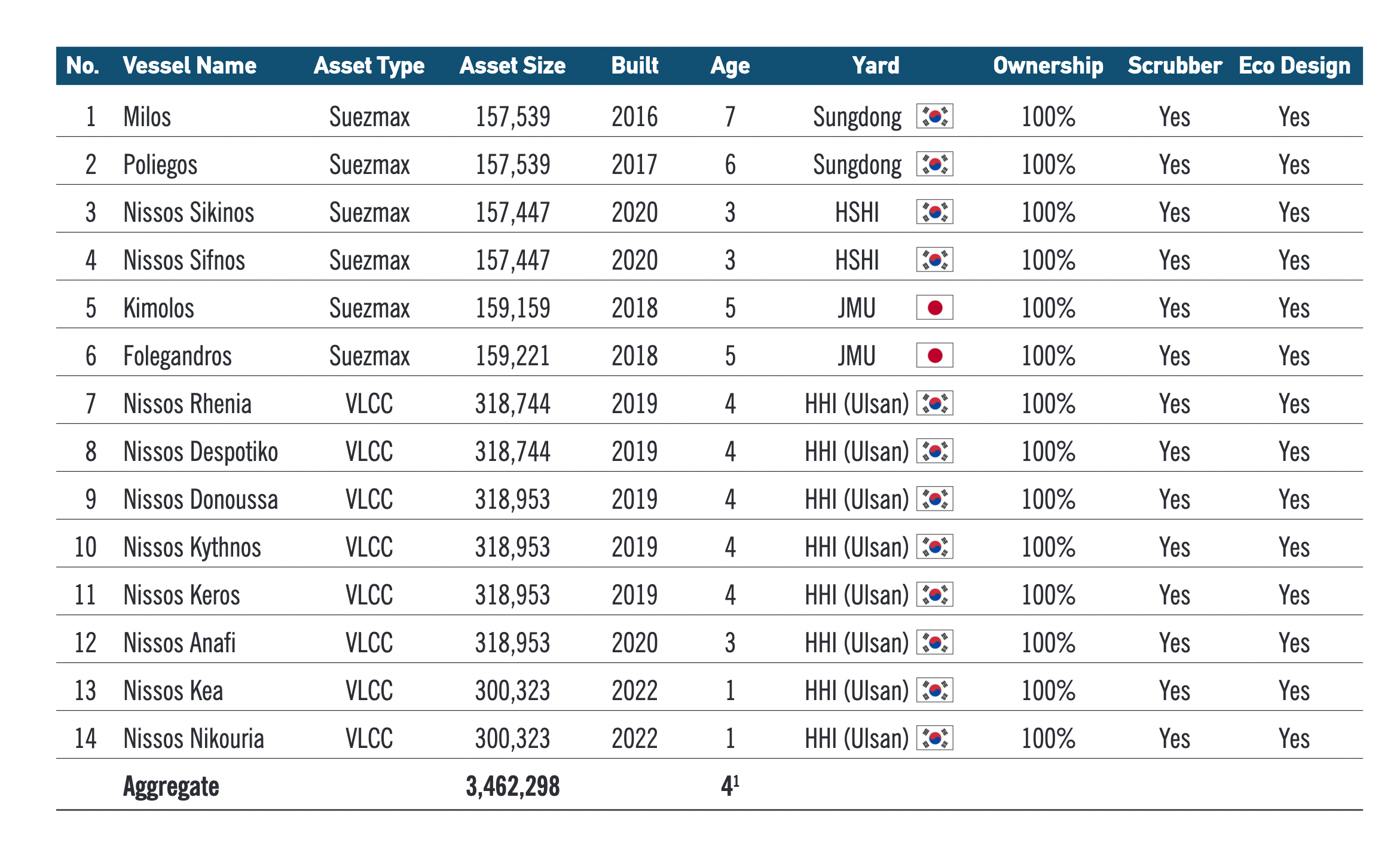

It is worth noting that Okeanis possesses six Suezmaxes and eight VLCCs.

All OET's tankers have eco design and are scrubber fitted (Company's Presentation)

{kind=link}

All eight VLCCs have been trading in the spot market, while two Suezmaxes (Nissos Sifnos and Nissos Sikinos) have been under timecharters during Q3. Both are going to be redelivered by December. Therefore, 100% of the fleet is going to trade in the spot market starting next year. Although this may increase revenue volatility, trading in the spot market is likely to be advantageous, given that spot rates have generally been higher than longer-term rates, coupled with the added benefit of exposure to potential spikes in the event of geopolitical disruptions.

Finally, a significant catalyst in the next quarter will be the listing on the NYSE (under the ticker ECO). While the exact timing of the listing is yet to be determined, it is expected to take place in December 2023. The new listing will enhance liquidity and potentially enable the stock to trade at a higher multiple, thanks to the expanded investor reach.

The big picture

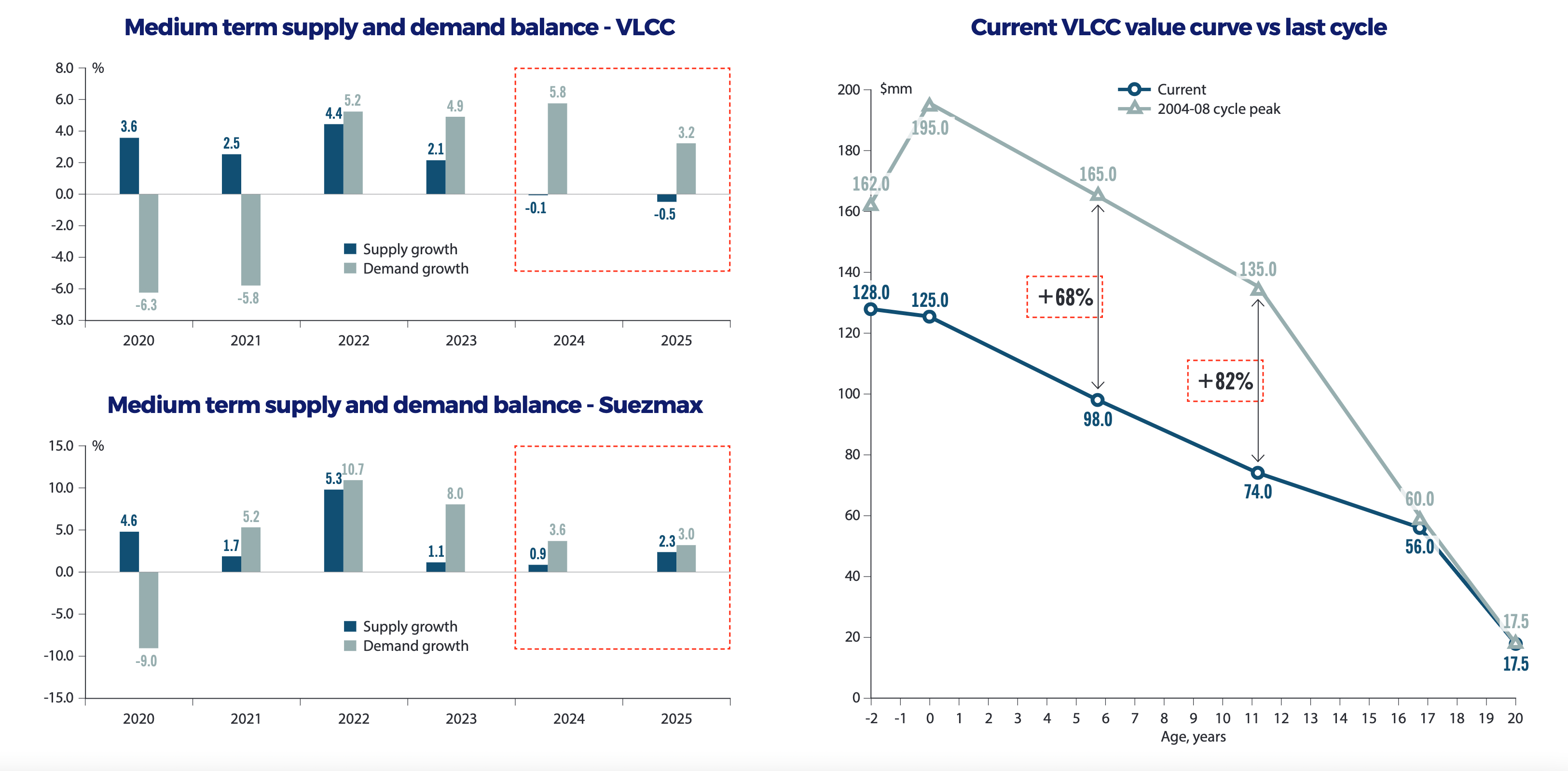

The big picture remains extremely supportive for crude tankers over the next few years. This stems from a historically low orderbook , especially for VLCC vessels, coupled with robust demand growth, and increasing voyage lengths, because of stricter environmental regulations and higher geopolitical risk premia. The return of Venezuelan barrels to the market could provide a further catalyst, opening the door for the mainstream fleet to take over from shadow fleet operators.

The following visualization shows that the net supply growth for VLCC vessels (new deliveries minus scrapping) is forecasted to be negative over the next two years, while growth is expected to remain robust. It is therefore difficult to imagine scenarios where tanker earnings do not remain sustained, which in turn will be positively reflected on net asset values. The same picture reveals also that, especially for newer ships, there is still a lot of potential upside compared with the previous 2004-2008 upcycle.

{kind=link}

That the bull market is going to continue for the foreseeable future appears to be also the conviction of most management teams in the sector. Here is a statement from the Q3 Earnings Press Release of International Seaways (NYSE: INSW ).

We expect the tanker markets' attractive supply and demand dynamics to continue to drive strong tanker earnings for the foreseeable future. Supply side growth remains limited due to evolving regulations and limited newbuild capacity in the near term at shipyards while the world fleet continues to age. Positive tanker demand fundamentals are supported by increasing oil demand and higher tanker utilization from the shifting global energy trade, with geopolitical tensions driving further focus on energy security.

Here is a further statement from DHT's presentation concerning why the orderbook remains so small , despite improving earnings:

Following the few newbuilding orders that have been placed year-to-date, the activity seems to have dissipated with limited interest in ordering new large tankers. We believe this reflects several key factors impacting investment decisions, or lack of, hereunder high asking prices from ship builders requiring life-time earnings well above historical averages, long lead-time to deliver new ships, increased cost of capital, and no convincing arguments related to future fuels and technologies. This comes at a time when we think the global fleet is of a sufficient size to profitably service the industry in the foreseeable future.

Technical picture

The stock price has risen strongly over the last month, on the back of Okeanis operational overperformance and rising freight rates. The weak Q3 results caused a significant sell-off, with the stock closing down 10% on Thursday. Despite this recent sell-off, the price is still up month-on-month and the stock looks a bit overextended. While not demanding, the valuation has been getting pricier, with Okeanis closing the gap with other peers on a NAV-based viewpoint. Therefore, I don't see the current price as a compelling short-term entry point yet, but if the stock were to trade again down to around 250 NOK/share in the weeks to come, I would consider it as a buying opportunity.

{kind=link}

Conclusions

Okeanis reported results below expectations for Q3 and its guidance for Q4 also looks weak at first sight. However, there are reasons that explain all that. These reasons are short-term in nature. The long-term picture remains intact. I believe we have yet to see peak rates for this cycle. Okeanis is strongly positioned to deliver exceptional returns throughout. I plan to remain a shareholder for years to come, and I look forward to taking advantage of potential future volatility to add to my position.

For further details see:

Okeanis Eco Tankers: A Soft Quarter, But The Long-Term Picture Is Unchanged