OKENF - Okeanis Eco Tankers: Another Record Quarter

2023-05-22 08:05:50 ET

Summary

- Okeanis Eco Tankers achieved impressive Q1 2023 results, setting new records in terms of revenues, EBITDA, and earnings per share.

- The disruptions caused by the ban on Russian oil, along with a record low orderbook and upcoming environmental regulations, provide medium- and long-term optimism for crude tanker rates.

- Okeanis is well-positioned to benefit significantly compared to its competitors due to its young and fuel-efficient fleet, strong management, leverage, and commitment to capital returns.

Introduction

Okeanis Eco Tankers (OKENF) continues to deliver impressive results, as Q1 2023 marked another consecutive record-breaking quarter in terms of revenue, EBITDA, and earnings per share.

I am drawn to Okeanis due to its operational excellence and shareholder-friendly approach. The company has consistently outperformed its peers and has a strong track record to support this. Moreover, it has adopted a strategy that sets it apart from other crude tanker companies, by maintaining a high, yet reasonable, level of leverage, while simultaneously returning nearly all of its free cash flow to shareholders through dividends. In my view, this approach of prioritizing capital returns over debt repayment, as long as market conditions remain robust, maximizes shareholder value.

Although the short-term outlook may carry uncertainties, such as a potential recession in the Western world and a slower-than-expected reopening in China impacting crude demand, it is crucial to focus on longer-term considerations, particularly the status of the orderbook. Not only are crude tankers going to benefit from historically low orderbook levels, but stricter environmental regulations will further restrict supply. With its 100% eco-scrubber fleet and a relatively young average vessel age of around 5 years, Okeanis is well-positioned to capitalize on this bullish market setup.

Okeanis has provided optimistic guidance for a strong Q2 based on secured rates. Its confidence is reinforced by the decision to distribute 100% of Q1 earnings as dividends, translating to an annualized dividend yield of approximately 28%. While future payout ratios may not remain at 100%, there are certainly reasons to be bullish about the company's future. With a capable management team and bullish orderbook dynamics, I anticipate that 2024 could be an even stronger year for Okeanis than the already exceptional 2023.

Q1 2023 results

Q1 2023 proved to be a strong quarter for Okeanis, as it achieved a record-breaking performance, with $74.4 million in adjusted EBITDA and $1.60 in adjusted earnings per share. It's important to note that the company currently holds a market capitalization of approximately NOK 8.1 billion ($740 million), equivalent to a price of around $20 per share.

The strong financial results were primarily driven by increased revenues. Fleetwide Time Charter Equivalent (TCE) reached $70,800 per day ($72,700 for VLCCs and $68,200 for Suezmaxes), compared with $63,800 per day in Q4 2022 ($65,400 for VLCCs and $61,600 for Suezmaxes). Although the TCE fell short of expectations based on guidance, this can be attributed to accounting standards, i.e. longer voyages resulting in a larger denominator in the TCE calculation.

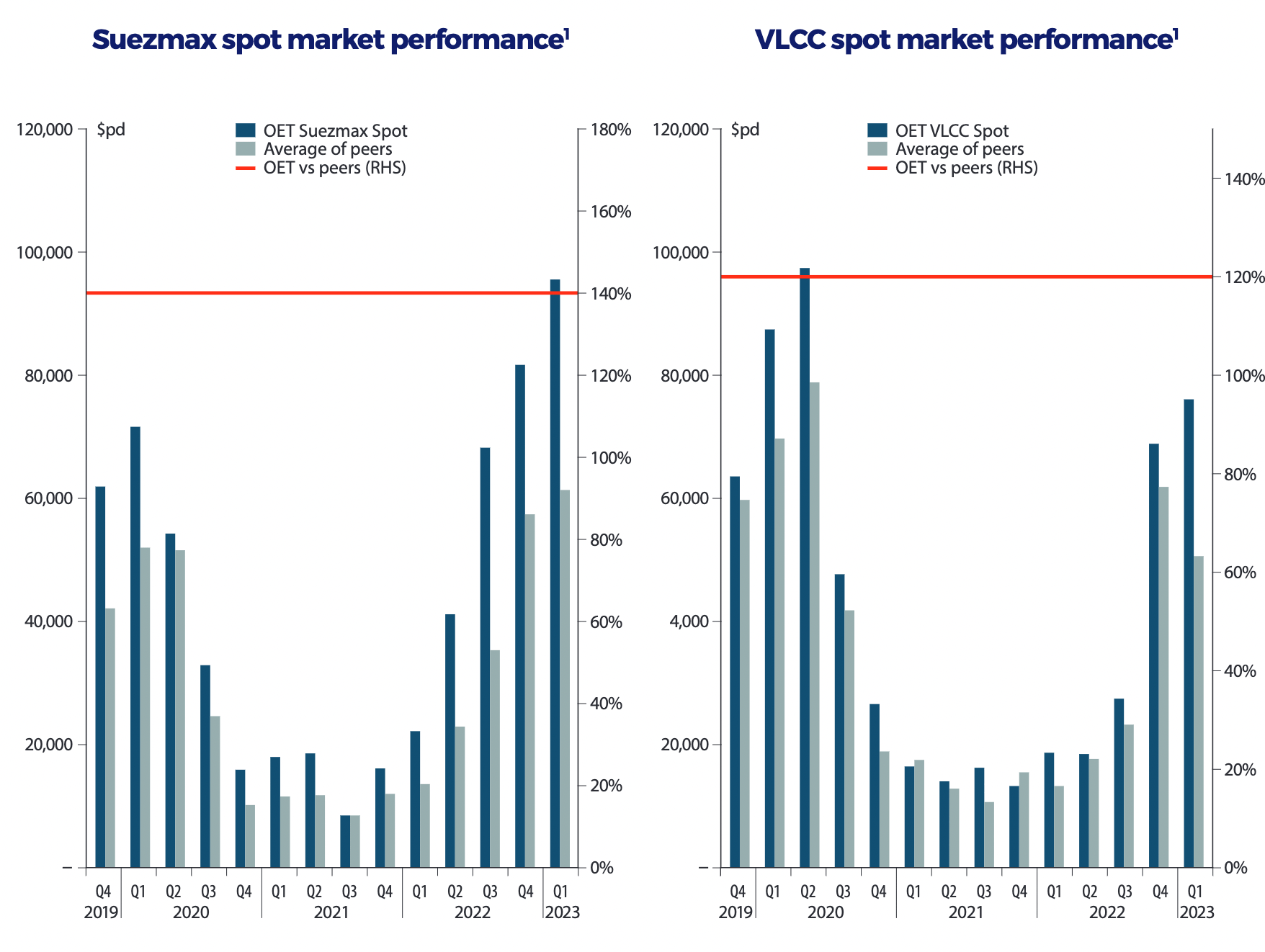

Throughout the quarter, spot rates declined from their peak in Q4 2022 but remained historically high. Okeanis successfully took advantage of the more favorable spot rates compared to timecharter rates by allocating 71% of its fleet to the spot market (87% for VLCCs and 50% for Suezmaxes). Furthermore, Okeanis was able to maximize fleet efficiency to achieve spot rates above the industry average.

Okeanis spot market outperformance vs. peers (Company's presentation Q1 2023)

{kind=link}

Operating expenses stood at $8,885 per calendar day, which remains one of the lowest in the sector. This was partly due to the fuel savings obtained from Okeanis' 100% scrubber-equipped fleet.

At the end of the quarter, Okeanis possessed a strong cash position of $118 million ($81 million at the end of Q4 2022). With $727 million in interest-bearing debt and total assets of $1.2 billion, the company maintains a reasonable level of leverage while distributing all its cashflow to shareholders.

The Q1 dividend of $1.60 per share, equivalent to 100% of adjusted EPS, reaffirms Okeanis' commitment to returning capital to shareholders and reflects the management's optimistic outlook for the future. This positive outlook appears to be justified in the near term, considering the strong guidance for the next quarter, with 72% of available spot days for Q2 2023 having already been secured at $75,500 per day for VLCCs, and 79% fixed at $96,500 for Suezmaxes.

The big picture

Finally, it is worth re-iterating what are the general motivations for being invested in crude tankers at the moment, despite the considerable appreciation in share prices over the last 12 months.

The tanker market is highly cyclical and is prone to boom-bust cycles. Environments of sustained high rates incentivize shipowners to increase supply via new orders. Delivery of new capacity suppresses rates. Because of the long construction times, it often happens that the new capacity reaches the market at the point of an economic slowdown, further contributing to a market collapse. This is what happened in the years leading to the Great Financial Crisis in 2008.

On the other hand, periods of low profitability lead to a contraction in the orderbook, which reduces supply and helps to balance the market. Recycling activity also picks up, leading to an increase in the average vessel age. In time, rates start improving and the cycle can start again.

Despite presenting some of the same general features, the current cycle also has some unique characteristics. The pandemic significantly reduced oil demand. Shipowners reacted by increasing recycling and delaying new orders. As the covid restrictions were removed, demand rebounded strongly, together with rates. Normally, this would have led to an increase in the orders for new builds which, however, did not happen for a combination of reasons.

Shipyards capacity was taken up by a wave of new orders for container ships, spurred by the high rates caused by covid-related supply chain disruptions. Container rates have since declined, but yards remain fully booked through 2026, which is bearish containers but also, as a second order effect, makes tanker supply more inelastic. As the most capital intensive sector within the shipping industry, crude tanker construction is particularly sensitive to inflationary pressures. Construction costs have risen by a third over the last two years. Because of rising construction and financing costs, and the uncertainty surrounding new environmental regulations, shipowners are more cautious at deploying their cash. Capital flows into the sector are likely to be further constrained in the coming years because of the looming threat of peak oil demand (oil demand has proven remarkably resilient in recent years despite prevailing narratives, and peak oil is likely to still be far into the future).

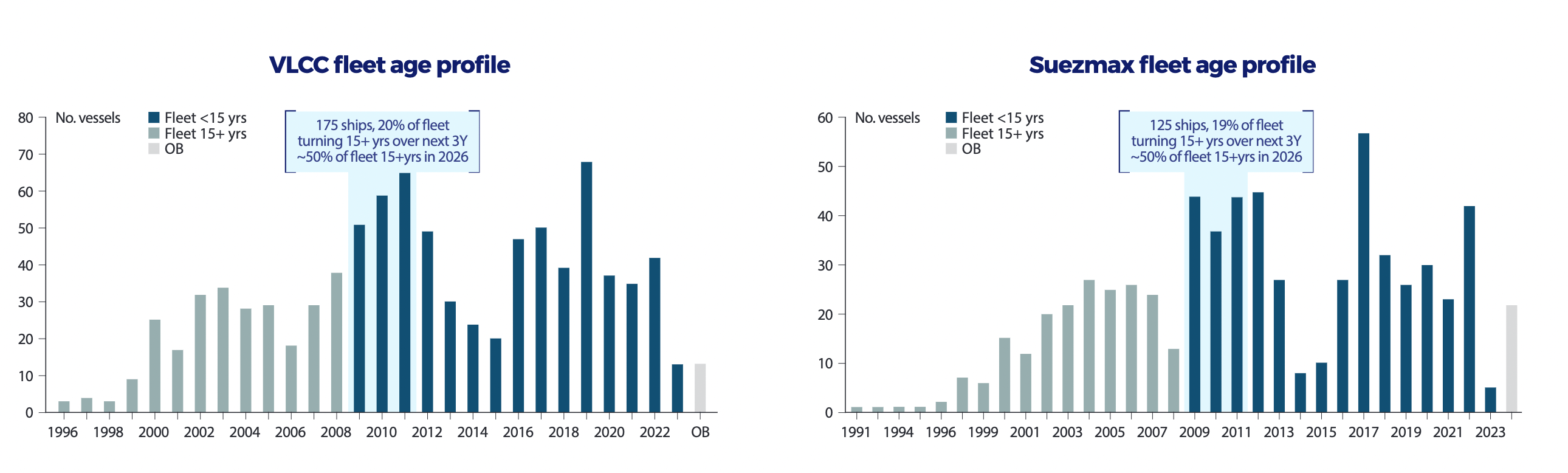

As a result, the current crude tanker orderbook is one of the most bullish on record. Not only constructions are not picking up for the reasons mentioned above, but the average fleet age is already quite high. The mass of newbuilds from the 2008-2010 boom will turn 15+ years old over the next three years. Recycling is also close to a peak.

VLCC and Suezmax fleet age profile (Company's presentation Q1 2023)

{kind=link}

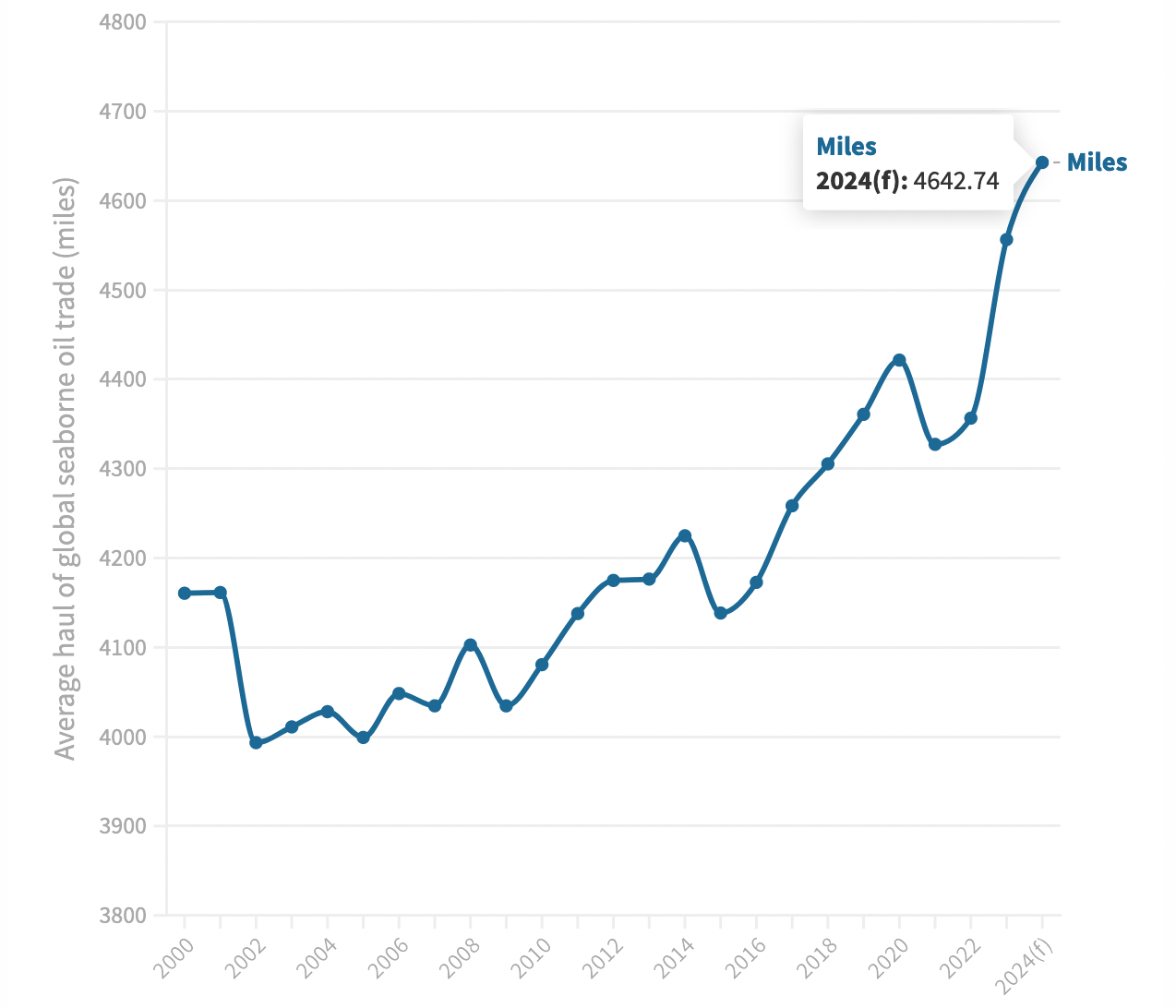

In addition to the status of the orderbook, other significant factors that impact the supply of crude tankers are the average speed and length of voyages. Environmental regulations such as the Carbon Intensity Indicator ((CII)) and Energy Efficiency Existing Ship Index (EEXI) are set to decrease average speeds for less fuel-efficient vessels, while environmentally friendly vessels equipped with scrubbers are likely to command a significant premium. Furthermore, the war in Ukraine and the subsequent EU ban on Russian oil are reshaping the landscape of crude trade routes. As Russia redirects its oil flows towards Asia and Europe explores alternative suppliers, the average distance traveled by tankers in 2024 is projected to reach nearly 4,700 miles, representing a 7% increase compared to 2021.

{kind=link}

Increase in crude miles travelled following the Russian oil ban (Clarksons Research)

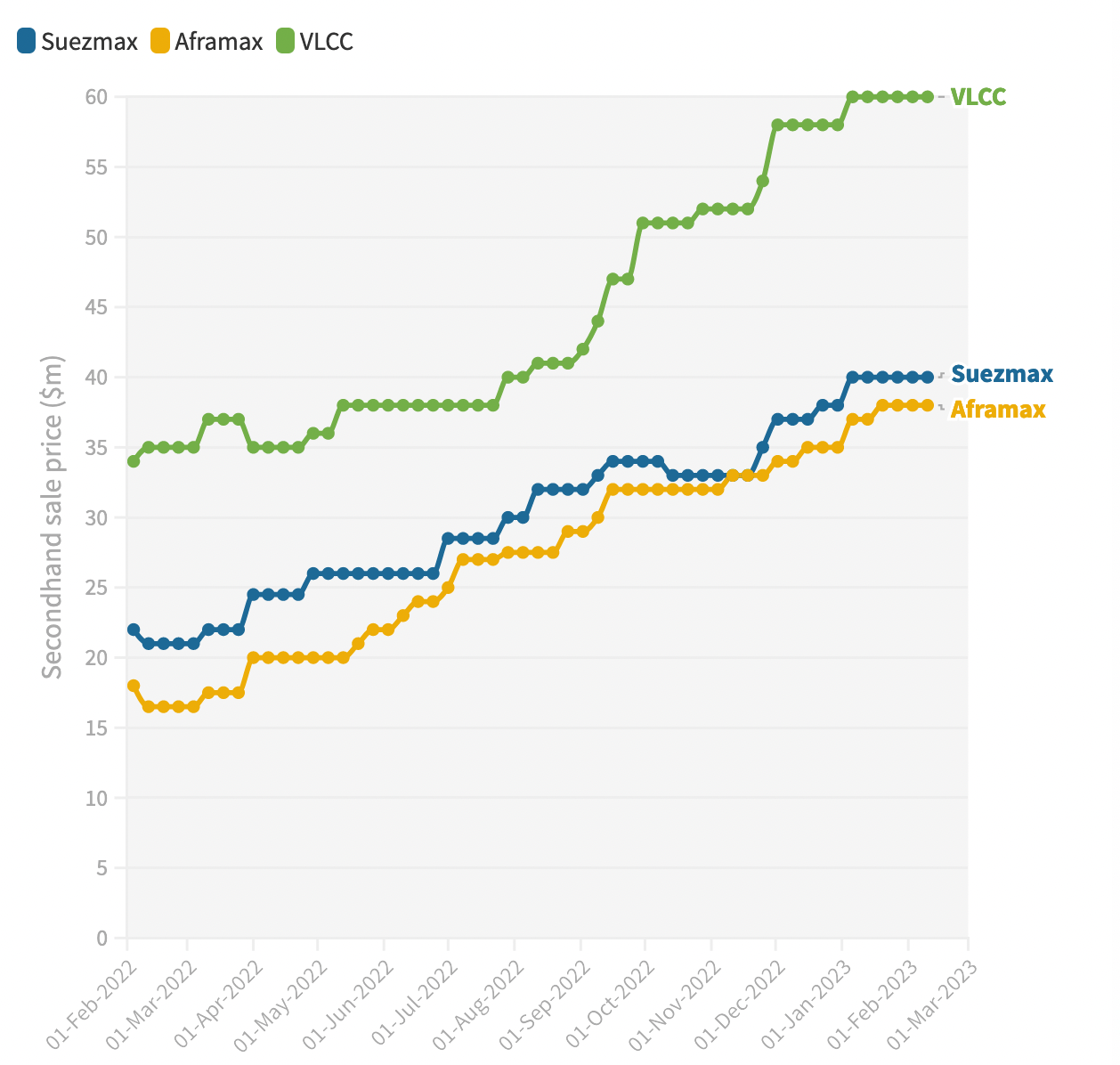

As ton-miles and revenues continue to rise, the valuations of crude tankers across all segments, including their net asset values, are also increasing.

{kind=link}

Considering all the aforementioned factors, it is probable that rates will remain at elevated levels for a period of at least 2-3 years. However, there are risks to this outlook, including a significant decline in oil demand and the lifting of sanctions against Russian oil. I consider both scenarios to be unlikely and believe in the continuation of the current trend.

Conclusions

Considering the strong operational performance, attractive capital returns, and a supportive rate environment in the medium and long term, I continue to view Okeanis as a key holding in my portfolio.

The forward dividend yield, currently exceeding 25%, is the highest among crude tanker companies. Dividends are distributed quarterly and are not subject to withholding tax. With the expectation that current rates will persist for the next 2-3 years, there is a substantial margin of safety.

The primary risk lies in the sector's high cyclicality and sensitivity to economic conditions. A downturn in oil demand resulting from a recession could pose a near-term challenge. Additionally, for non-Norwegian investors, the recent depreciation of the Norwegian krone (down over 10% against the Euro year-to-date) has presented an additional hurdle; however, this depreciation is also currently providing new investors with the opportunity to acquire valuable assets at a discounted price.

For further details see:

Okeanis Eco Tankers: Another Record Quarter