OKENF - Okeanis Eco Tankers: Riding The Upcoming Crude Tanker Bonanza

2023-08-10 04:13:16 ET

Summary

- Okeanis Eco Tankers owns the youngest, most fuel-efficient fleet of VLCC-class crude tankers of all its publicly listed peers.

- The supply set-up for crude tankers has never been better, with just 4% of existing supply on the order book up to 2026.

- High steel prices and stricter environmental regulations should also incentivize scrapping, placing further pressure on vessel supply.

- Oil demand is expected to ramp up, while increasing production and refinery dislocation will support ton-mile demand.

Editor's note: Seeking Alpha is proud to welcome ZY Capital as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis and Recommendation

Okeanis Eco Tankers (OKENF) (OSLO:OET) is a young crude tanker owner among more established, bellwether names such as Euronav (EURN) and Frontline (FRO). It owns the most attractive fleet and is appropriately leveraged to capture the multi-year upcycle in charter rates as suggested by the almost non-existent orderbook. With consistent outperformance against benchmark rates, a fantastic dividend policy and significant management ownership, I believe OET is poised to outperform in the upcoming crude tanker bonanza.

Industry Overview

Crude tanker owners, and this should hold true for most of shipping, are at the absolute mercy of supply and demand. The greatest peaks and troughs in the market have been characterized by severe under/oversupply of vessels in the market.

And this is exactly the cyclicality of shipping - owners are flush with cash at the height of the boom, ordering more ships which lead to oversupply and poor rates, incentivising scrapping which tightens supply and causes rates to skyrocket.

Crude tankers are used to carry crude oil and dirty petroleum products, and are classified by their sizes. VLCCs (2 million barrels) are the largest of them all, followed by Suezmaxes (1 million+ barrels) and Aframaxes (600,000 barrels). Larger vessels usually have better unit economics while smaller vessels have the flexibility to enter any port/ canal due to the small draft.

Tankers are usually chartered out for some form of "day rate", of which there are two main types :

- Time Charters - typically longer-term (multiple years), where the charterer is responsible for all voyage-related expenses such as port fees, bunker costs etc.

- Spot Charters - typically single trips, where the owner is the one responsible for all voyage-related expenses on top of regular operating and financing costs.

A simple analogy would be that a time charter is like renting a car, whereas a spot charter is like taking a cab. As you can probably guess, time charters are more stable and more accurately reflect long-term outlook rather than short-term sentiment.

It is also important to note that different owners have different percentage of their fleet on time versus spot charters, which can skew accounting revenue comparisons as spot charter rates include voyage-related expenses. Therefore, it is common to see these companies publish their time charter equivalent ((TCE)) earnings, which is essentially gross charter revenues net of any voyage-related expenses incurred.

The Baltic Exchange governs the major routes and publishes the Baltic Dirty Tanker Index which can be used to gauge how average rates have moved daily. Some major routes are also scrutinized traders, such as the TD3C which is a VLCC route between the Middle East and China, but that is a topic mostly for traders and charterers.

Business Overview

Okeanis Eco Tankers was listed back in 2018 with some vessels under construction that have all been delivered since.

Today, the company owns 6 Suezmaxes and 8 VLCCs, all of which are eco-designed and scrubber-equipped. It has a market capitalization of about US$750 million with an equivalent amount of long-term debt.

In Q1 2023 , the company reported $70.8k fleetwide TCE and $74.4 million in EBITDA. EPS was $1.60 and the company announced its decision to pay out the $1.60 in its entirety as a dividend, equivalent to an annualized yield of 28%.

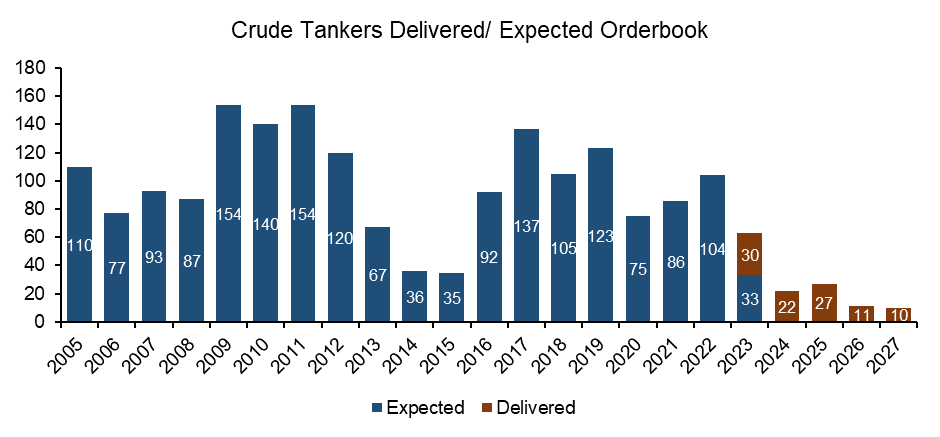

Tanker orderbook are at multi-decade lows

Ask anyone and they will probably tell you about the extreme cyclicality in shipping, like I've mentioned in the industry overview section above. The shipping industry collectively is not known for making the best capital allocation decisions, often overordering and directly contributing to the next crash in rates. See the containership owners immediately after the exceptional year they had in 2021 for a recent example.

Therefore, the supply of vessels is something shipping investors scrutinize to identify any long-term opportunities in the industry. One very important indicator is the orderbook as a % of the existing fleet which is the new supply entering the market. As it stands, the tanker orderbook is at 4% , a level we have not seen for decades, and it is getting everyone riled up.

{kind=link}

Of course, owners with excess cash can still place orders for new ships - these are necessary capital expenditures to maintain and grow their fleets. However, ordering has slowed down significantly for the following reasons.

Newbuild prices are extremely high , due to the sharp increase in raw material and labour costs. A VLCC that cost $90 million in just 2018 now costs over $130 million in today's market for a 50% increase. Even the most irresponsible owners would run the numbers and find that the assumptions required to justify such a purchase to be challenging.

Shipping is usually a leveraged business (to the tune of 60-70% LTVs) and the interest rate environment has made ordering unsavoury. Financing costs comprise a significant cost of operating a ship - higher interest rates would further jack up the breakeven costs when combined with the high purchase price.

Shipyard Capacity (Arctic Securities)

Shipyard capacity is down significantly , with some 2/3s of shipyards shuttered in the aftermath of the poor market in the early 2010s. Whatever capacity is left has been taken up by the orders of large and complex ships like LNG/LPG carriers as well as containerships. There are minimal delivery slots available through to 2026 hence owners are less willing to build new ships but rather purchase existing ones to bolster fleet capacity.

Environmental regulations pose great uncertainty in shipping. With talks of getting to net zero by 2050 , the shipping industry has been experimenting with alternative fuels like ammonia and LNG but none have emerged as the dominant option yet . Ships are multi-decade investments and owners are hesitant to place orders for newbuilds that become uncompetitive before their lifetime.

All these external conditions pose headwinds for new ordering, and it is reflected in the orderbook. I am personally more inclined to trust these reasons over self-imposed restrictions by shipowners who are a fickle bunch.

Supportive environment for vessel scrapping

Scrapping refers to the retirement of vessels for their steel value at scrapyards. This is typically done when the vessel approaches the end of their useful life or when prevailing rates make it uneconomic to continue operating such vessels. This is the other side of the tanker supply picture.

Vessels lose value rapidly as they age, a function of the competitive market as well as regulations requiring expensive special surveys to verify their seaworthiness every few years.

Tanker Survey Schedule (Euronav)

{kind=link}

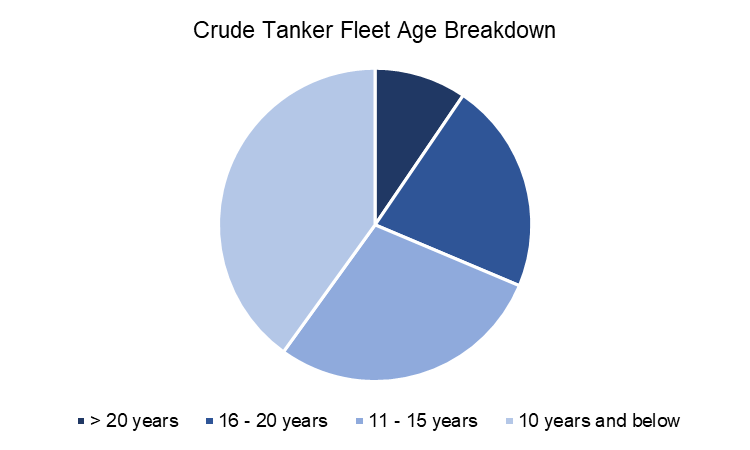

In a regular market, scrapping occurs happens at the 20-year mark. Steel prices have also risen in recent years, with VLCCs commanding nearly $20m in steel value if they head to the breakers today.

However, scrapping activity has been muted recently due to the strong rate environment. Older vessels have the unsavoury (but profitable) option of carrying sanctioned oil from countries like Iran and Russia, also known as the shadow trade , giving owners an alternative to continue operating their vessels.

{kind=link}

This market has reduced scrapping and 32% of the current tanker fleet is aged 16 years or more. With such an old fleet in operation, it just takes a small nudge for owners to start selling their tankers for scrap should the shadow trade demand fade.

Ton-mile demand growth is expected to be resilient

While supply is the dominant force in the tanker trade, I think that demand for oil transportation should also hold up in the near-term. This comes in the form of ton-miles which means that both volumes and distances can drive up demand for tankers.

The concept of peak oil is unavoidable when deciding to invest in owners of tankers. I do not profess to be a specialist in this area and choose to defer to official forecasts of oil demand. The IEA has projected oil demand to rise by another 2% to ~102mmbd and we are on track to reach those forecasts. That said, I don't believe the tanker market is reliant on any significant demand side tailwinds for us to enter another boom.

This year, OPEC+ has repeatedly announced production cuts and extensions which puts pressure on volumes transported. With Brent oil trading safely in excess of $80/bbl, I think that this should push OPEC+ towards restoring production - otherwise they'd have sacrificed their oil revenues to the benefit of other producers.

Another reason to be optimistic is the overall realization that exploration & production activity has to continue. Shell, BP and other oil majors have reversed their stances on fossil fuels and have allocated significant capex in this area. Offshore exploration is making a comeback especially around the Atlantic where most incremental supply is expected to come from. This is overall bullish for crude tankers because Atlantic barrels have to travel further to additional refinery capacity in the Far East, boosting ton-mile demand .

OET has the most attractive fleet you can own

So why OET compared to the other tanker owners? I have repeated the fact that OET's tankers are young, eco-designed and scrubber-fitted (i.e., the most environmentally friendly). I dislike it when product attributes are rattled off without further explanation, so let me show you why this fleet is desirable.

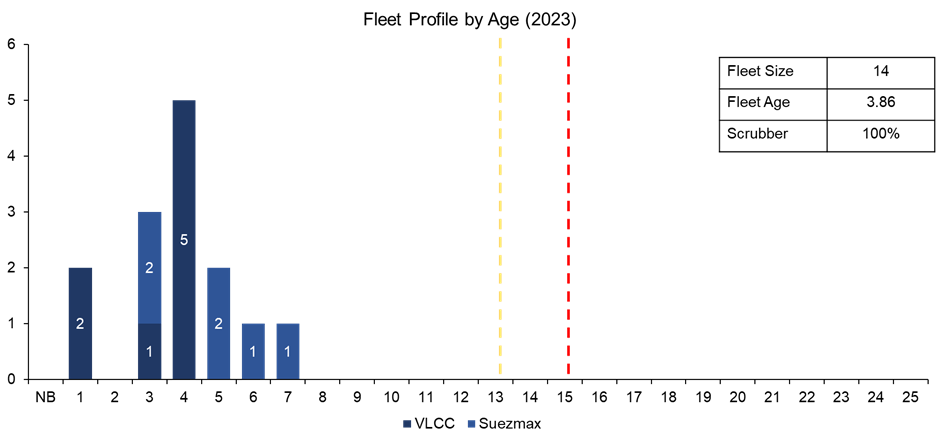

Young vessels have an edge as they are typically more seaworthy and hence cost less to insure. The benchmark age is around 15 years old, after which it becomes significantly less competitive when competing for charters. Every charter is a miniature market where charterers get to select the most appropriate vessel to carry their cargo, and age is often an important criterion to minimize the risk of loss of cargo at sea.

{kind=link}

OET's fleet profile is shown in the chart above. Any vessels that fall on the right of the red line are less competitive and positioned for scrapping, while vessels between the yellow and red lines will reach the 15 year old mark in the next 3 years. As you can see, OET's vessels are very young and should remain very attractive to charterers in the near to medium term.

Eco-designed refers to vessels that are built around the early 2010s, specifically designed to be hydrodynamic. Design variations can range from bow shape to the type of engine and can result in ~10 tons of fuel savings daily. This means thousands in fuel savings everyday - nothing to scoff at when we consider entire fleets operating all year round.

Scrubber-fitted vessels allow owners to burn cheaper high-sulphur fuel oil [HSFO] compared to the more expensive very low-sulphur fuel oil [VLSFO] as mandated by IMO. Owners had to make the decision to retrofit their vessels for ~$2-3 million with scrubbers to benefit from fuel cost savings. While the VLSFO-HSFO spread has come down to <$100/ton, this was historically a very profitable decision with spreads exceeding $200/ton. OET opted to retrofit its whole fleet with scrubbers a few years ago and that has more than paid off the investment. Therefore, this acts as an additional layer of optionality for OET to capture the spread going forward.

As you can see, having a young and decked out fleet like OET gives it an edge when competing for charters. Fuel savings (in both cost and volume) should also translate to premiums above the benchmark rates.

Besides, OET's management has proven to be shrewd owners capable of repositioning their vessels opportunistically to capture better spot rates for their vessels. Each route is a mini-market which can see over/underperformance versus the benchmark BDTI and you want owners who have the foresight to capture this premium. OET has consistently reported TCEs higher than its peers in the crude tanker segment.

Okeanis Eco Tankers Q1 2023 Presentation

{kind=link}

OET's management is aligned with investors as the controlling family has a ~57% stake in the company. It has also stated that with minimal capex requirements, unattractive newbuild economics, its goal is to return as much cash to investors in the form of dividends. I believe this as they recently paid out 100% EPS in Q1 2023 for an annualized yield of almost 28%. This is actual cash returned to you, as a shareholder, rather than questionable choices like investing in new ships at cycle-high prices.

Risks

As OET has positioned its fleet to be 100% on spot, the biggest risk is a catastrophic event that reduces crude oil transportation demand, which would see spot rates crater. While the global economy continues to flirt with recessionary indicators, I believe that short of another pandemic (knock on wood), risks are skewed to the upside. The biggest recessions have seen just minor dips in oil demand, while vessel supply is set to tighten even more.

While the OPEC+ cuts act as a near-term headwind, I do not see this having an outsized impact. Oil prices have been trending higher, and they will soon have to turn on the taps again (otherwise what was the point of all those cuts?). There is also the medium-term view that incremental supply in the Atlantic will replace OPEC+ barrels and further drive ton-mile demand for tankers.

Another concern is the potential easing of Russian sanctions, which was a major driver of 2022's outstanding charter rates. I believe that OET is not fundamentally reliant on Russian sanctions because Russian ports cannot accommodate the larger vessel classes in OET's fleet. Sanctions have lifted Aframax charter rates to near all-time highs and I would also steer clear of owners reliant on the sanction situation.

Valuation

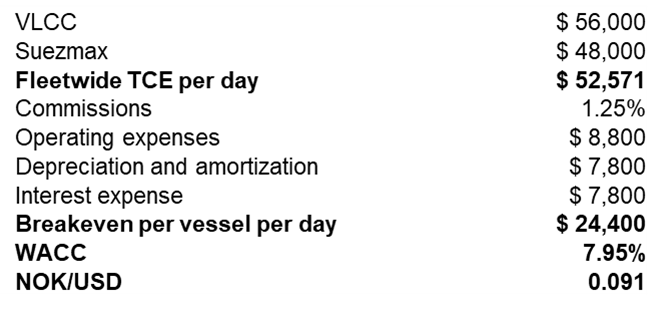

I value each of OET's tankers using a DCF of their earnings and add net interest-bearing debt to find its valuation on a P/NAV basis. Key assumptions in my DCF valuation are in the table below:

{kind=link}

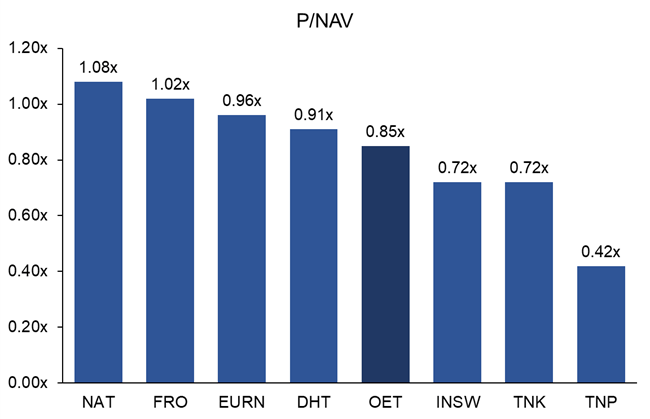

I arrived at a NAV/share of NOK 285 which means that OET is trading at roughly 0.85x NAV at today's share price of NOK 253.5. I believe this is a good entry point for investors who want exposure to the upcoming crude tanker market, with an attractive fleet as well as sensible management that is creating shareholder value.

{kind=link}

I have also estimated P/NAVs for OET's peers in the crude tanker space - as you can see, the stock trades in line with the industry average and below the more prominent names like Frontline, Euronav and DHT Holdings (DHT). This valuation gap does not reflect the true quality of OET's business. Management is arguably comparable to the bigger names, while its fleet is unrivalled on any metric, and this translates to outperformance in the charter rates it can command.

I fully expect P/NAVs to rise across the board and for the valuation gap between OET and the US-listed names to close as more investors pay attention to the crude tanker segment. Therefore, I think that OET deserves to trade at 1.0x P/NAV or about NOK 285 per share.

Recommendation

I believe that the supply and demand set-up in the crude tanker space is the best we've seen in decades, and we are at the cusp of another great cycle. OET, hands down, owns the most attractive fleet for exposure to the crude tanker market. With young vessels trading on spot, minimal capital requirements and a friendly shareholder policy, this means that you can count on significant dividends and capital appreciation in the next 2-3 years.

For further details see:

Okeanis Eco Tankers: Riding The Upcoming Crude Tanker Bonanza