OKENF - Okeanis Eco Tankers: Top Choice For Crude Tanker Exposure

2023-03-28 17:14:52 ET

Summary

- Dirty tanker rates are expected to remain structurally elevated because of the consequences of the war in Ukraine.

- Okeanis Eco Tankers Corp. is a best-in-class owner and operator of crude tankers.

- Okeanis ticks all my boxes: trades at a cheap valuation, is leveraged, has a modern fleet, excellent management, and a generous dividend policy.

Okeanis Eco Tankers Corp. ( OKENF , OET.OL) is a crude tanker company, operating a modern fleet consisting of six Suezmax and eight VLCC vessels. It is my top choice to capitalize on the on-going crude tankers bull market.

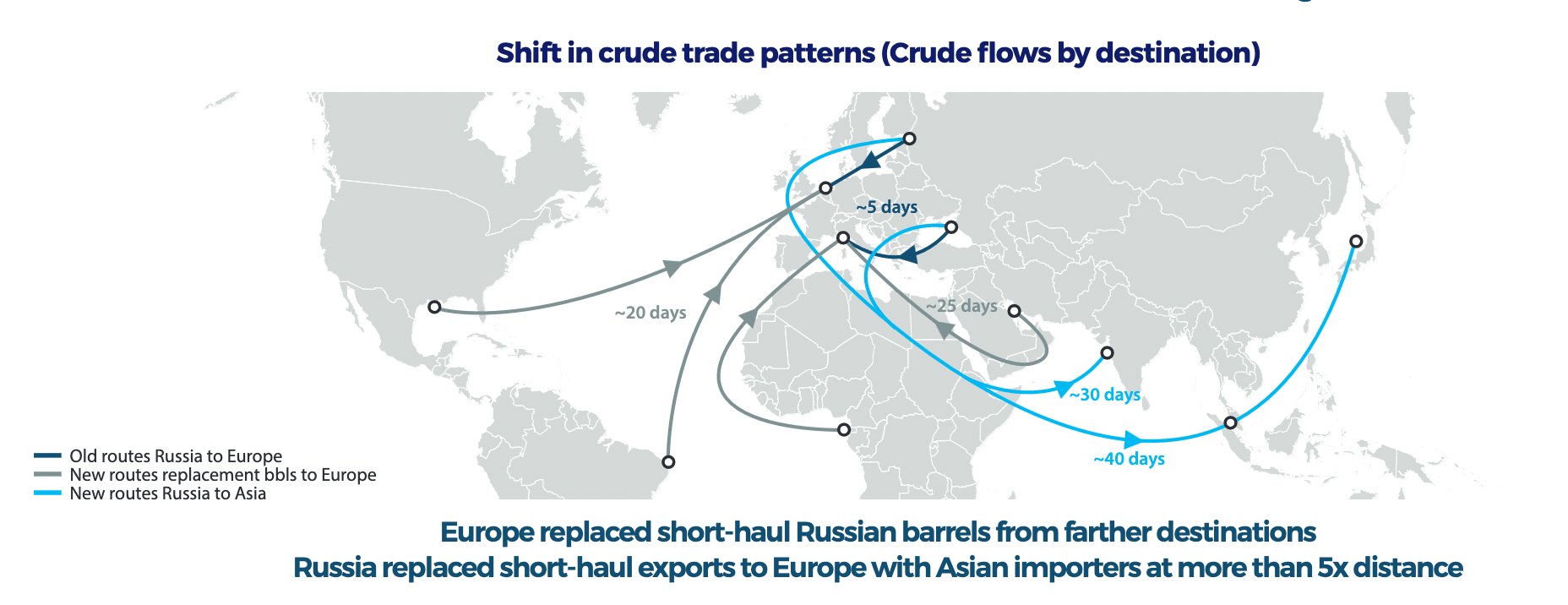

Let us revise the bull case for dirty tankers. The war in Ukraine has caused a rerouting of crude oil voyages, leading to an increase in tonne miles, and, therefore, also charter rates. The EU has imposed sanctions against both the import of Russian crude into Europe, and the transport of Russian crude to third countries (unless the respective crude oil is purchased below the $60 per barrel price cap). Such policy was meant to restrict revenues to the Russian government used to finance the war in Ukraine; however, it has also had the side effect of disrupting crude trade flows. European countries are replacing Russian barrels with new imports from further away regions, such as West and South Africa, and the Middle East, while Russia is shifting its exports towards India and China.

Shift in crude trade patterns (Company's presentation)

{kind=link}

The crucial point is that Russian crude is continuing to flow to the market (partly bypassing sanctions with the help of the tanker shadow fleet ), albeit on longer trade routes. European sanctions were designed to put pressure on Russia, but at the same time make sure that Russian production is not shut off and the oil market is not thrown into a deficit.

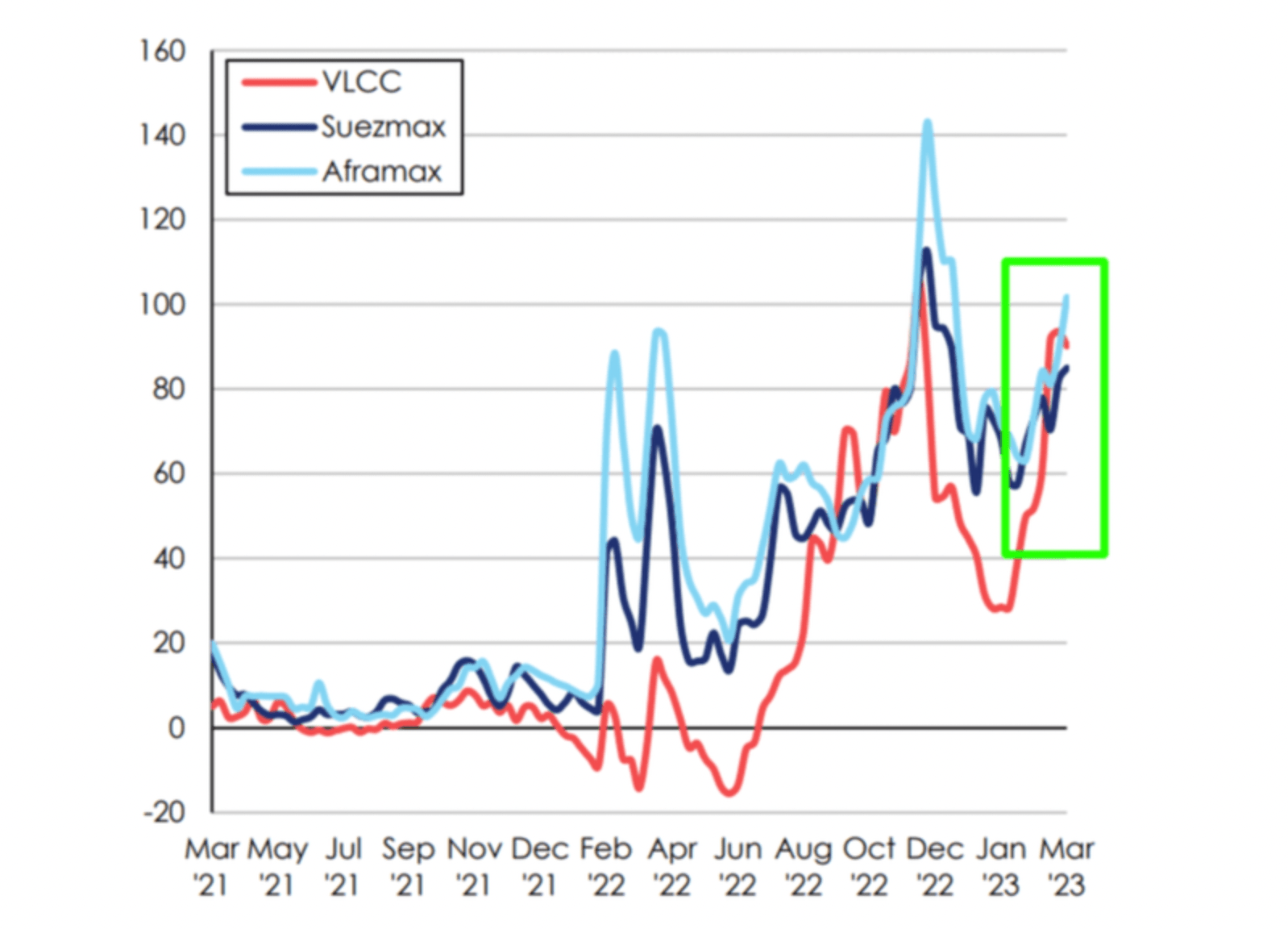

The objective was achieved, as Urals oil is now trading at a hefty discount to Brent, but charter rates have exploded upon the introduction of the ban, on December 5. They have since relaxed a bit, but have shown remarkable strength over the past few weeks, in particular in the case of VLCC rates (which were also helped by China reopening its economy after the covid restrictions).

Crude tanker spot rates (Clarkson's)

{kind=link}

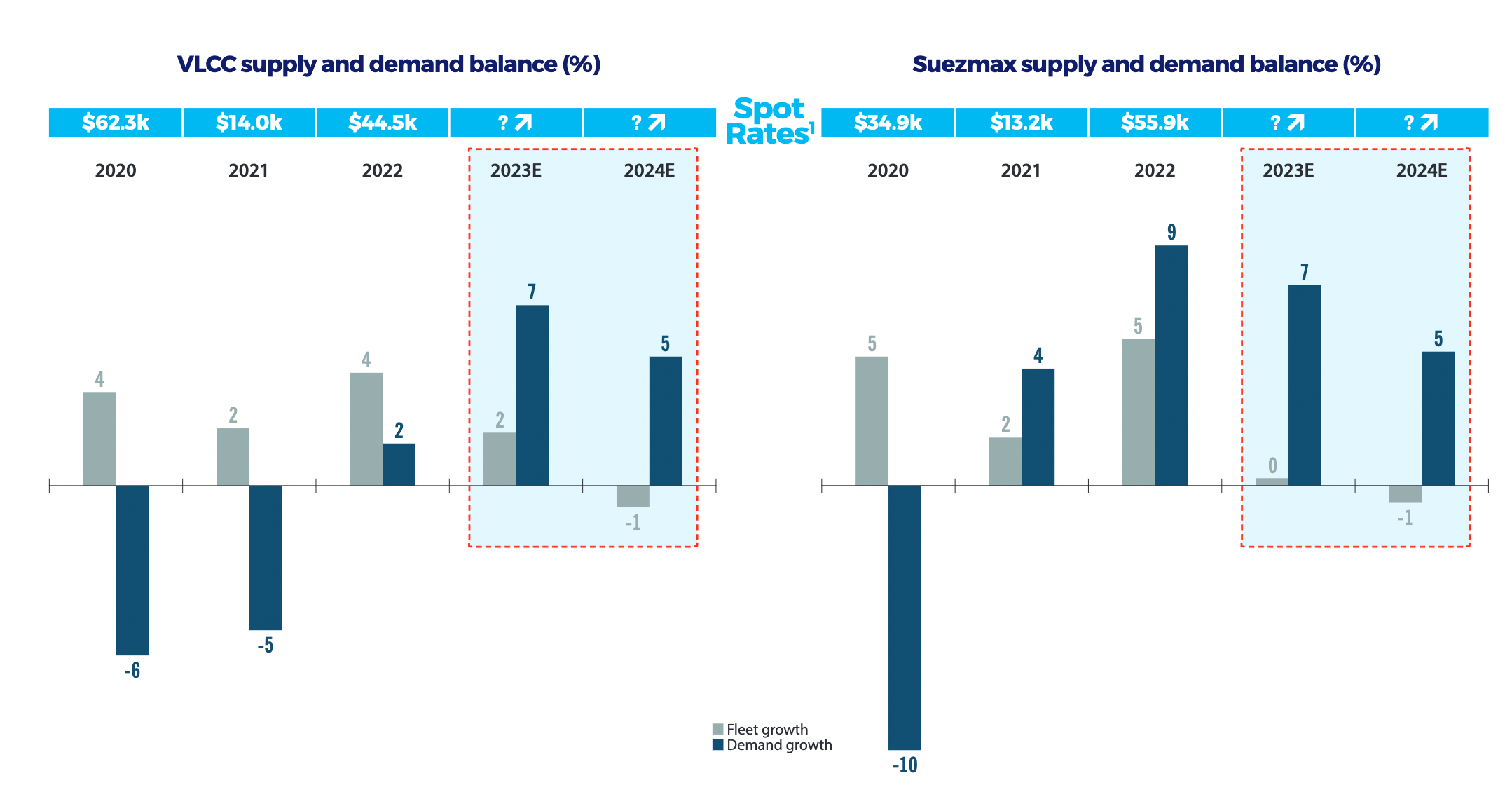

Dirty tanker companies are already exceptionally profitable in the current rate environment. Taking into account that demand is projected to outstrip supply in both 2023 and 2024, rates could certainly move even higher.

Supply and demand growth vs charter rates (Company's presentation)

{kind=link}

The strong sector outlook is already partially reflected in the share prices, with many companies having multi-bagged over the last twelve months. One should also keep in mind that the tanker market is highly cyclical and rates tend to mean revert over sufficiently long times, as higher rates attract new supply, which in turn leads to a decline in profitability.

However, there are reasons to believe the current rates are here to stay, at least for the next few years, for the following reasons.

- First of all, the increase in rates is a structural consequence of the rerouting of trade flows caused by the sanctions against Russia. It seems improbable that such sanctions will be withdrawn any time soon. Even if a peace deal can be brokered in the near future, Russian oil will continue to be shunned by Western nations. In other words, a return to the previous status quo is unlikely.

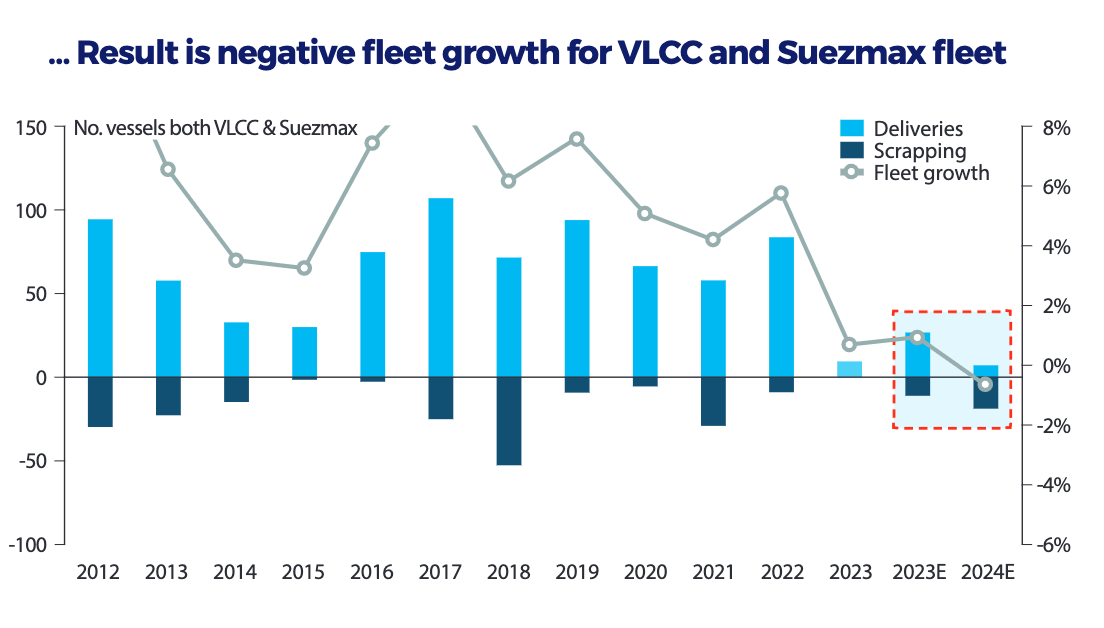

- Second, growth of the crude tanker fleet will be modest over the next few years, as the orderbook is at historical lows. Asian shipyards are already at maximum capacity, with the new supply mostly going into the container sector. On the other hand, very limited supply is going to enter the crude tanker sector. This is going to be supportive of rates, especially in conjunction with the fact that the fleet is aging and replacement costs are skyrocketing because of inflation.

Crude tanker orderbook is at historical lows (Company's presentation) Crude tanker fleet is ageing (Company's presentation) The net effect is modest growth, turning into negative growth starting from 2024 (Company's presentation)

{kind=link}

{kind=link}

{kind=link}

- Third, a further long-term bullish fundamental is represented by the enforcement of ESG policies . Shipping companies are under pressure to reduce their greenhouse gas emissions. The International Maritime Organization ((IMO)) has introduced a Carbon Intensity Indicator ((CII)) rating scheme, that classifies vessels into 5 classes (from A to E) based on the amount of CO2 emitted. In addition, it has defined an Energy Efficiency Existing Ship Index ((EEXI)), which measures energy efficiency compared to a baseline. The objective is to reduce carbon intensity from all ships by 40% by 2030 compared to 2008. The introduction of the CII and EEXI schemes is the stepping stone to forcing shipping operators to reduce emissions through new regulations. As an example, starting from February 1, 2023, operators will be required to submit CII ratings for all ships over 5000 tonnes. Any ship that obtains a D rating for three consecutive years (or E for just one year) will have to take corrective actions to achieve at least a C rating. Such regulations are going to increase costs especially for old, inefficient vessels, while they represent a competitive advantage for operators of more modern, eco vessels. Since the easiest way to reduce emissions is to lower speed, the tanker fleet will be forced to go slower on average, which is going to increase voyage lengths. In particular, eco ships will command a premium, since they will be able to travel faster than non-eco ships, a considerable advantage especially in a bull market.

Of course, there are also risks to the thesis. In my view, the main risk is that charter rates collapse as oil demand plummets because of a monetary-policy induced recession. In recent weeks, crude oil prices have notably weakened. Interestingly, tanker equities have traded in a correlated way with oil prices. This is counterintuitive, since lower oil prices imply lower bunker fuel prices, i.e., lower costs for tanker companies. In addition, lower oil prices (all other things being equal) imply a stronger demand for crude, as for instance refiners margins increase. Is the oil market really anticipating a recession and a demand drop? It is difficult to say with any degree of certainty. In my opinion, if such an event were to happen in the near future, it would offer an excellent entry opportunity, given the long-term bullish fundamentals.

Let us assume that the current bull market is going to continue over the next 3 years. How do we play it? I tend to evaluate tanker companies based on the following considerations:

- Leverage : in a bull market, the higher the leverage the better.

- Shareholder returns : the company should have a clear strategy to return capital to shareholders. Near the top of the cycle, dividends are to be preferred to share buybacks. Unwarranted expansion of the fleet is also a clear red flag.

- Modern fleet : eco vessels command a premium, and the advantage compared with older vessels is only going to increase with time. This is why I consider it essential to invest in companies with a low fleet age, even if this means sacrificing some leverage.

- Management : shipping is a volatile and often capital-destroying business. I want my capital to be in the hands of management who is competent and has skin in the game.

- Low valuation

I believe that Okeanis represents a good compromise between all criteria.

To start with, the company is sufficiently leveraged. According to the company's definition (leverage = net debt divided by net debt + book equity), leverage stood at 61% at the end of 2022. In fact, this is a quite high ratio among comparable dirty tanker companies. During 2022, total debt increased to $739 million, up 28% compared with 2021, as the company acquired two new VLCC vessels in anticipation of strong market conditions. In addition, Okeanis is leveraged to spot rates, by keeping around 80% of its fleet in the spot market, which allows it to capture the full benefit of lower fuel costs.

The company discloses the following sensitivities of free cash flow and net income based on different rates environment. Last year was closer to scenario number 2, while 2023 (at the moment) is closer to scenario 4. If such conditions were to continue, Okeanis would generate 1.5 its entire market capitalization in free cash flow over the next 3 years.

Sensitivities (Company's presentation)

{kind=link}

Okeanis also has a generous dividend policy. In fact, it has the highest dividend yield among its peers. The company is incorporated in the Marshall islands, so that there is no withholding tax on dividends or returns of capital. For Q4 2022, Okeanis has declared a distribution of $1.25 to shareholders. This corresponds to an approximately 20% dividend yield (at current share prices). Besides, it is practically certain that Q1 2023 is going to be an even better quarter than Q4 (and, given where rates are trading at the moment, Q2 is shaping up to be another strong quarter). Thus, I would not be surprised to see even higher dividends in the near future.

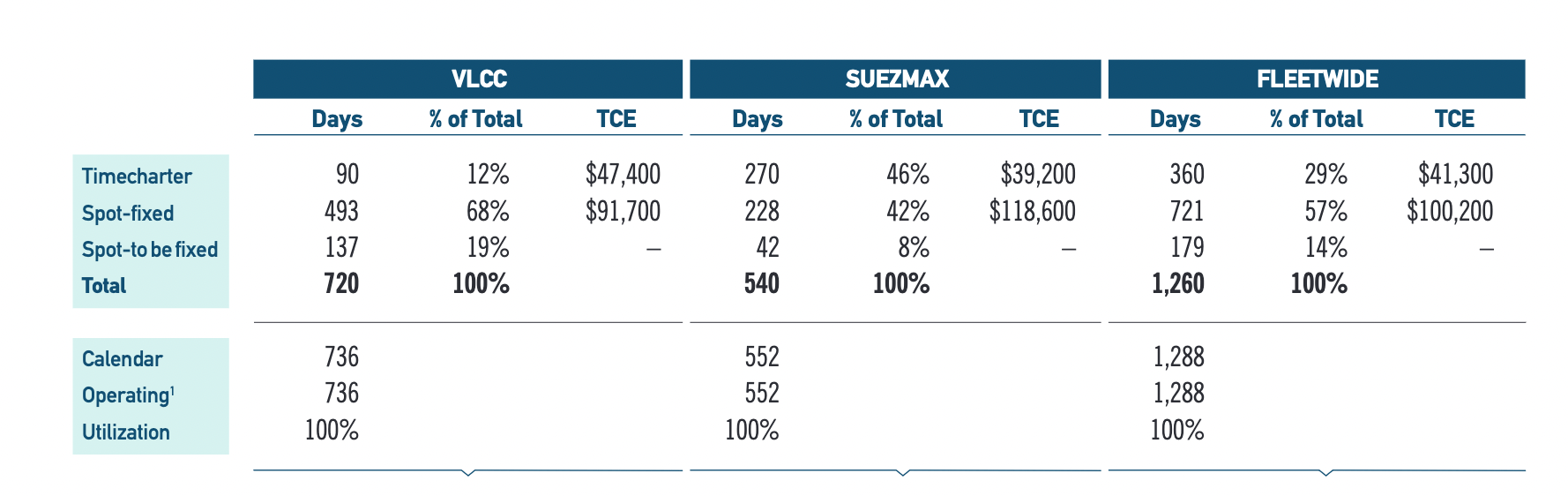

That Q1 2023 likely will be a record quarter is evidenced by the fact that the majority of the strong voyages fixed in Q4 were carried over to Q1, and that contracted spot rates are going to be higher during Q1 than Q4. In fact, we know already that for V LCCs 78% of available Q1 spot days were fixed at $91,700 per day, for Suezmaxes 84% were fixed at $118,600 per day. For comparison, during Q4 2022, the company achieved an average TCE of $63,800 per day ($65,400 for VLCCs and $61,600 per day for Suezmaxes).

Q1 2023 guidance (Company's presentation)

{kind=link}

A key competitive advantage of Okeanis is its modern eco-fleet. This allows the company to have lower costs than peers and makes it future-proof in connection with upcoming regulations.

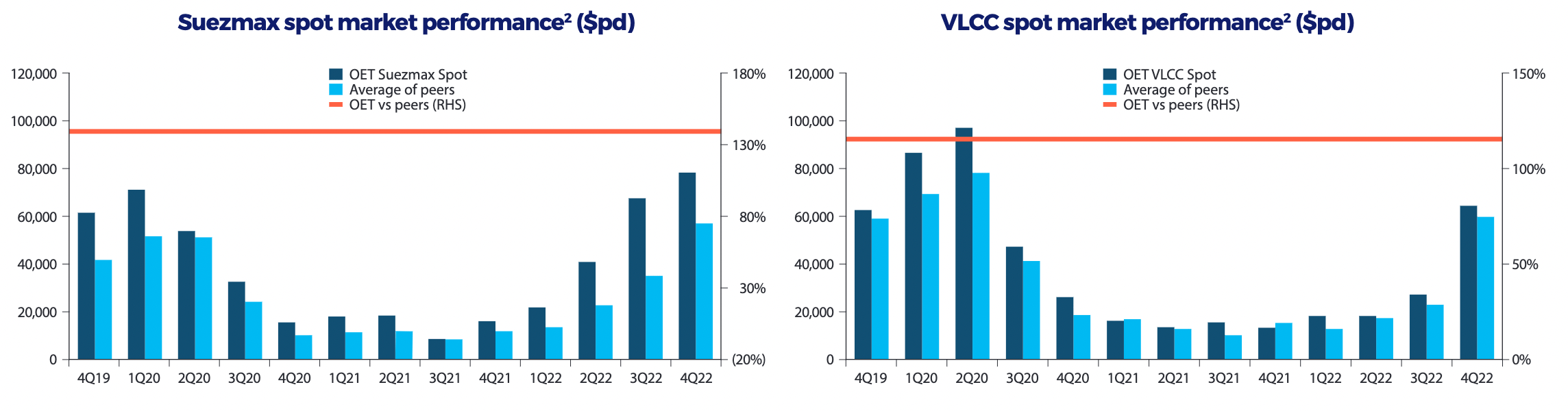

Management is certainly one of the best in the sector. This is also evidenced by the fact that Okeanis has consistently achieved better rates than peers. In addition, management is aligned with shareholders, with the Alafouzos family still holding a controlling stake (56.82%) of the company.

Spot market performance vs peers (Company's presentation)

{kind=link}

Finally, despite an almost 50% rise YTD, Okeanis Eco Tankers Corp. is not expensive. Adjusted EBITDA during 2022 was around $150 million, compared with a current market capitalization of around $760 million. More importantly, by any metric, 2023 is shaping up to be an even stronger year. If current conditions persist, Okeanis Eco Tankers can pay a sustainable annual dividend yield in excess of 25%. In conclusion, I see Okeanis Eco Tankers Corp. as a top choice among crude tanker companies, to take advantage of the current bull market over the next 3 years.

For further details see:

Okeanis Eco Tankers: Top Choice For Crude Tanker Exposure