OKTA - Okta: 33% Crash Equals A Buying Opportunity

Summary

- Okta is a cybersecurity company that is a leader in Identity Access management.

- The company produced strong financial results for the second quarter and beat analyst estimates for both the top and bottom line.

- Tepid guidance from management for Q3, spooked Wall Street and the stock has a huge sell off, plummeting by over 33% in a single day.

- The stock is undervalued relative to competitors and historic valuations and thus could offer a buying opportunity, once support is found.

Okta, Inc. ( OKTA ) is a leading cybersecurity company which specializes in identity management. The company recently announced mixed guidance for the third of 2022 and the stock price has been butchered by an eye-watering 33%. Despite this extreme stock market reaction, the company actually beat revenue and earnings estimates for the second quarter of FY23. In addition, the stock is now undervalued relative to historic multiples. In this post, I'm going to revisit the company's business model and then break down its second quarter results, before revealing the full valuation, let's dive in.

Secure Business Model

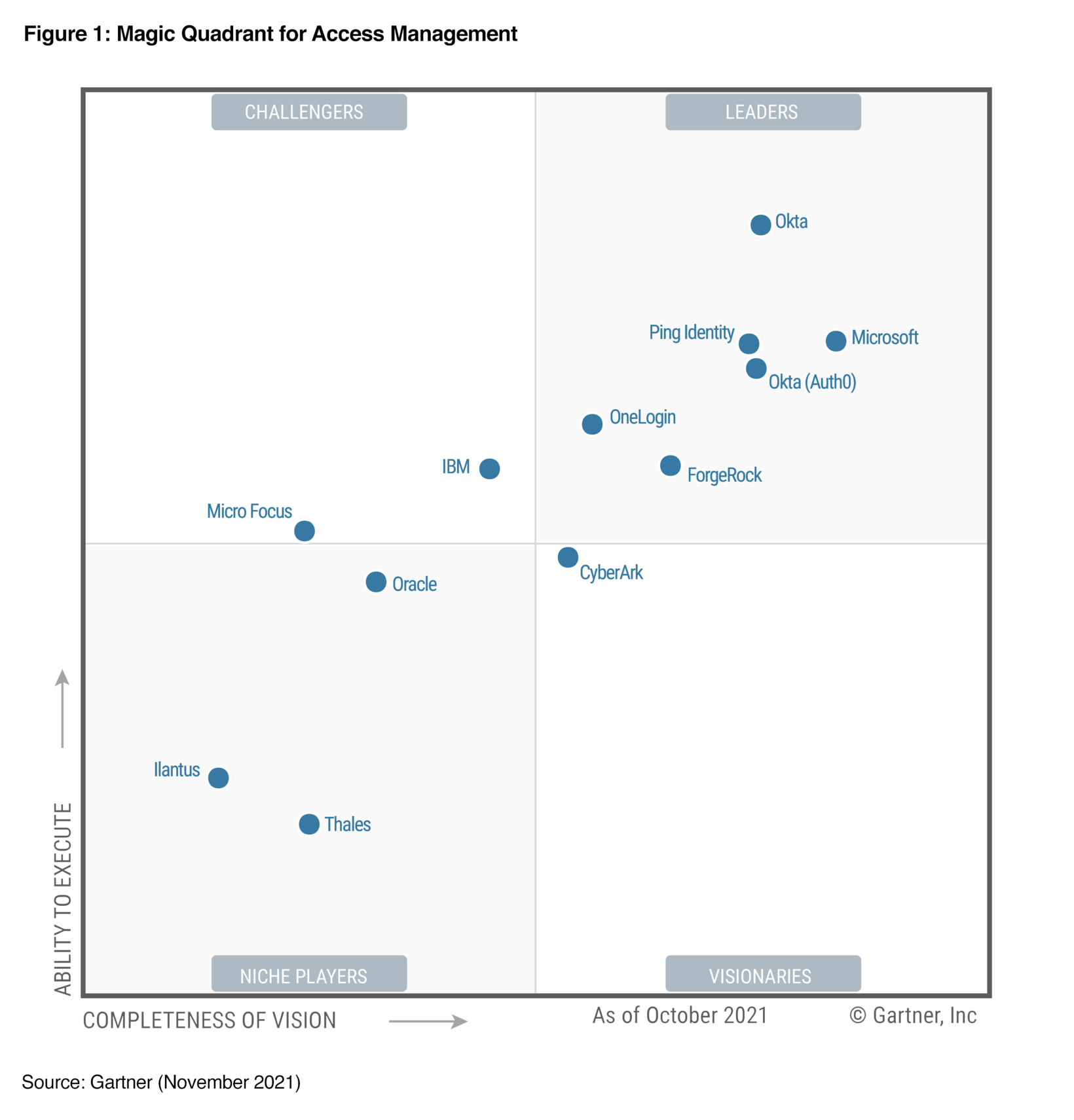

The word "leader" when referring to a company can get thrown around a lot, but in this case, it's extremely applicable. Okta ranks as a Gartner Magic Quadrant "Leader" in Identity Access management. This is the process of allowing only authorized users access to systems while preventing hackers from gaining entry.

Okta top right of Magic Quadrant (Gartner)

{kind=link}

User experience is often a major issue when it comes to access management. This makes complete sense as imagine a door with twenty locks, it will be very secure by also very annoying, as you have to remember the combination for twenty locks to gain entry. Okta solved this problem with its Single Sign On [SSO] solution. This enables users to access multiple applications with just one set of credentials, which vastly improves the user experience as it saves you having to remember many different passwords. In 2021, Okta acquired former competitor Auth0 for $6.5 billion in an all-stock deal. Analysts had mixed opinions about the deal, but I personally believe it was a solid acquisition (on paper at least) as by owning Auth0, the company can dominate the Single Sign On market.

As a quick test, if I Google "Single Sign On" from a private browser I get Okta showing up as the first result (via a paid ad), followed by OneLogin, Cloudflare, and Auth0. Now as Okta owns Auth0, it really owns ~50% of page one on Google. As an extra data point, Gartner reviews for "Access Management" software show Okta as number one, with the most ratings, and highest reviews.

{kind=link}

Okta has also entered the IGA (Identity Governance & Administration) and the PAM (Privileged Access Management), as they aim to disrupt legacy incumbents such as SailPoint Technologies ( SAIL ) and CyberArk Software ( CYBR ).

The company's platform also makes the job of IT admins much easier as its dashboard enables a view of all users, while also enabling fast onboarding of new users which can free up an admins time for higher-value tasks. Okta is also a cloud-first solution, which makes it perfectly suited for the modern enterprise which is digitally transforming. For example, let's say a legacy enterprise is moving its IT from on-site to the "cloud," which is basically someone else's data center, in order to take advantage of greater flexibility and cost savings. The company may have a legacy Identity Access Management software that is running on its servers but now wishes to opt for a cloud-native solution. If the enterprise is moving to Amazon Web Services (the world's most popular cloud provider) they can simply purchase Okta direct from the AWS marketplace . As the cloud industry is forecasted to grow at nearly a 16% Compounded Annual Growth Rate [CAGR] and reach over $1 trillion by 2028, Okta is in a prime position to secure application access.

The company is also poised to benefit from the secular shift towards "Zero Trust Security." Zero Trust is a security term that basically means by default users are "not trusted" when inside the network. For example, they are given "least privileged access" to only the applications they need. This is extremely important as if an attacker gains access to one application, like an old HR application, they could "move laterally" and gain access to the Finance applications and do a ransomware attack, without Zero Trust.

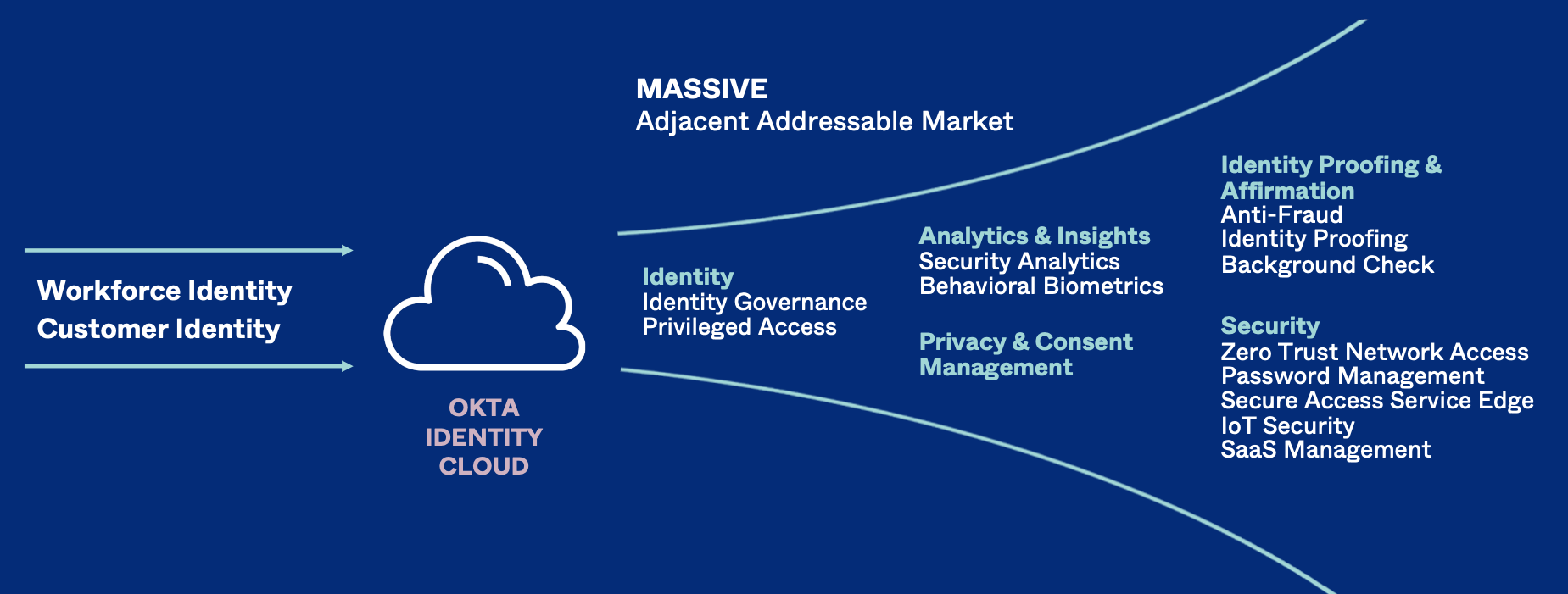

Okta Platform (Q2 Presentation)

{kind=link}

Second Quarter Earnings

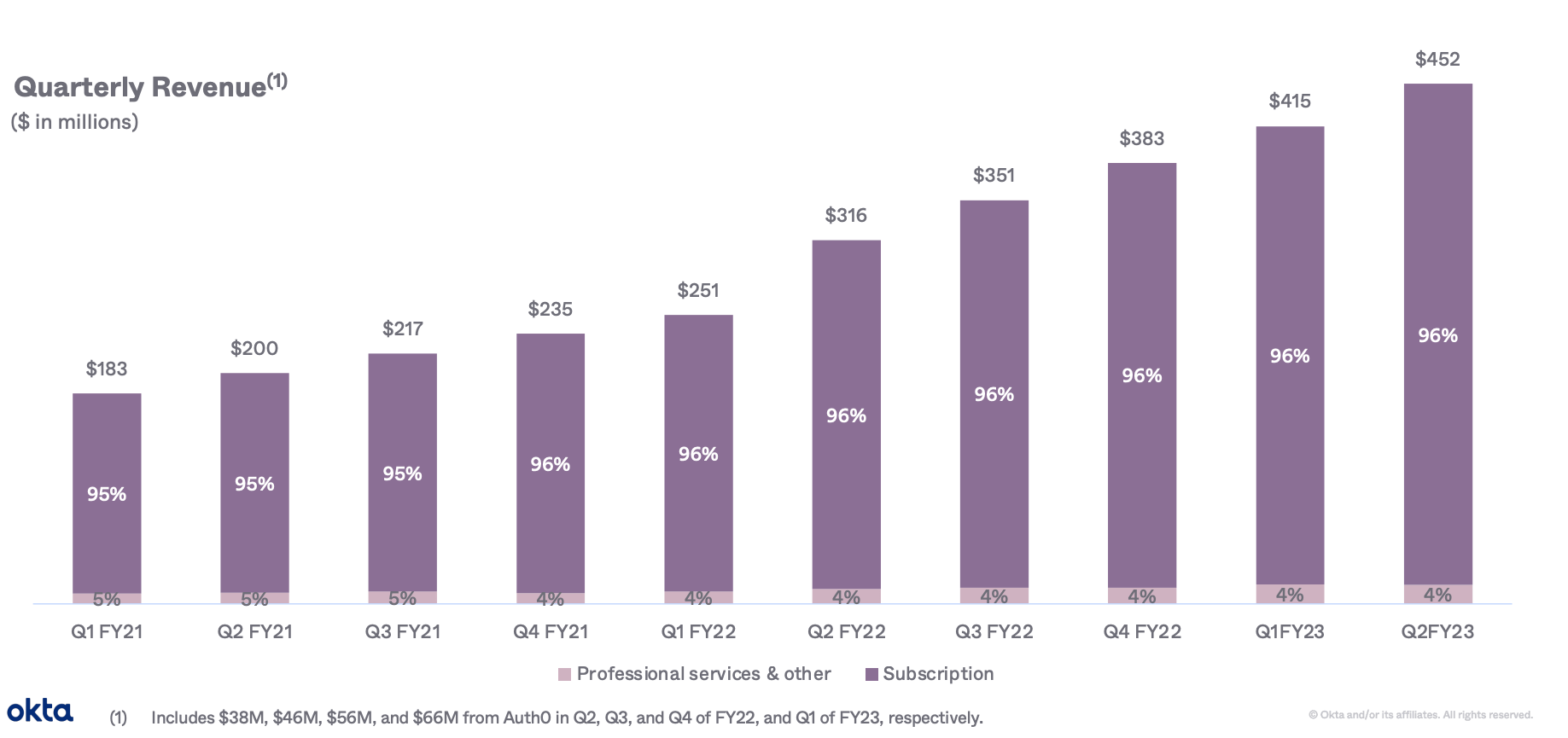

Despite the large market sell-off, Okta produced strong financial results for the second quarter of fiscal year 2023. Revenue popped by 43% year-over-year to $452 million and beat analyst expectations by $21.2 million. Subscription revenue also popped by 44% year-over-year and now makes up ~96% of revenue which is great to see.

Revenue (Q2 Investor Presentation)

{kind=link}

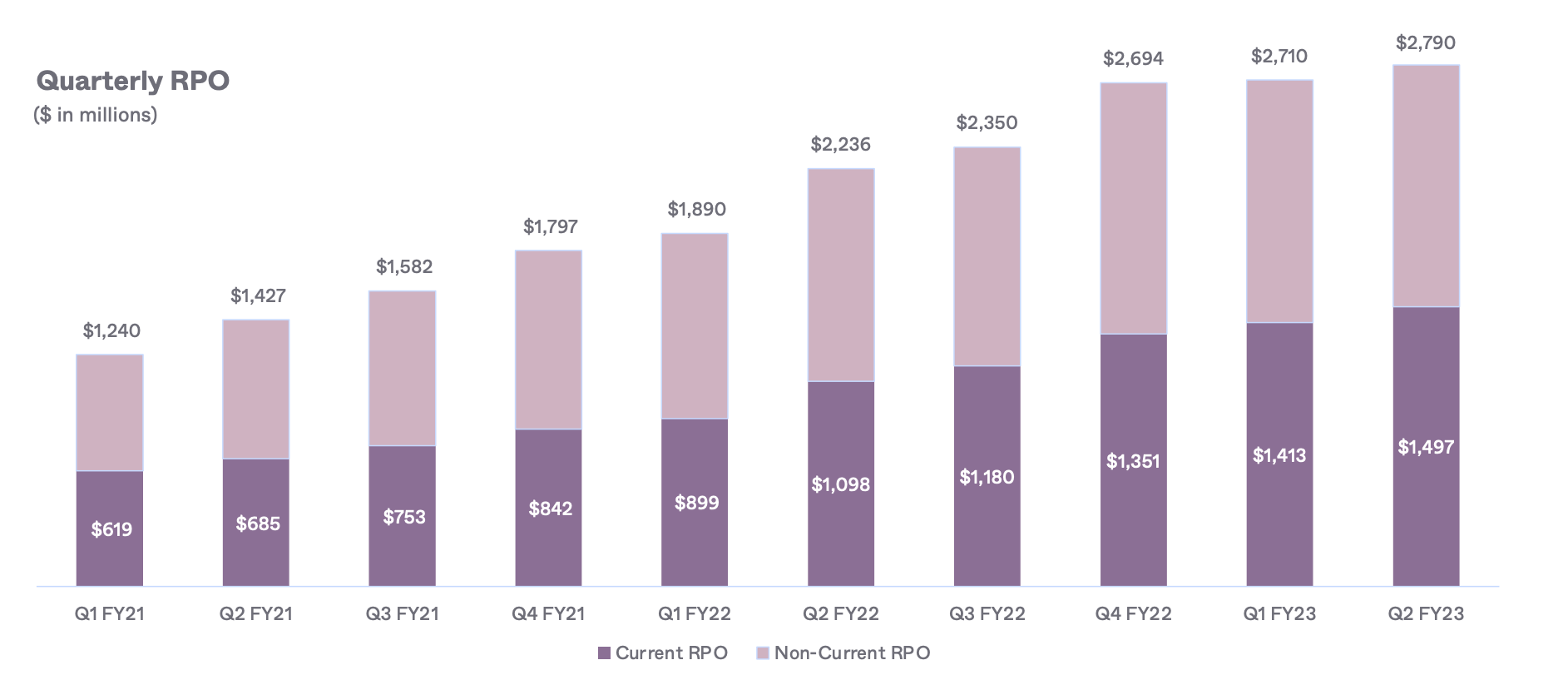

Remaining Performance Obligations [RPO] is a reliable indicator of future revenue as this is defined as contracted revenue but of which the service hasn't been provided yet. In this case, RPO was $2.79 billion which popped by 25% year-over-year. While the current RPO which is contracted revenue expected over the next year was $1.5 billion up 36% year-over-year.

{kind=link}

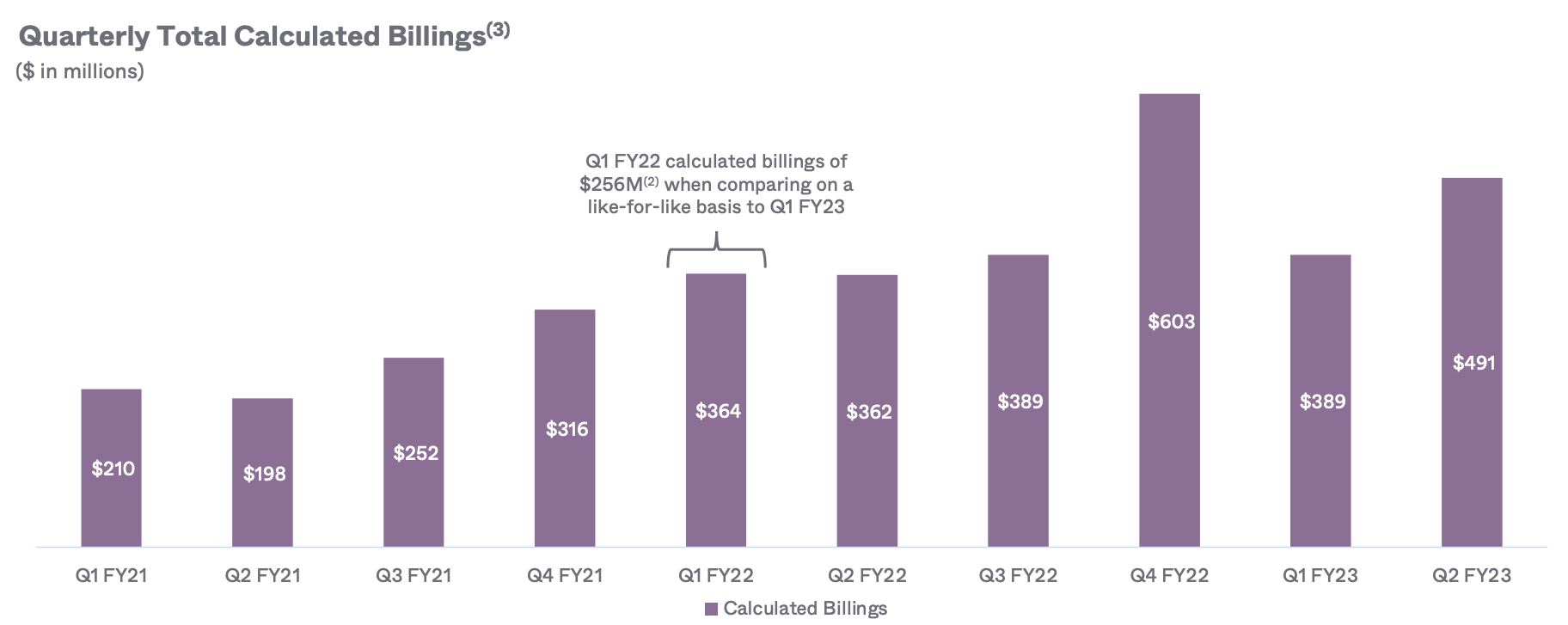

Total billings were $491 million, up 36% year-over-year. Some analysts were "underwhelmed" by this RPO, as they were expecting much more after the integration with Auth0 (more on this in the risks section).

{kind=link}

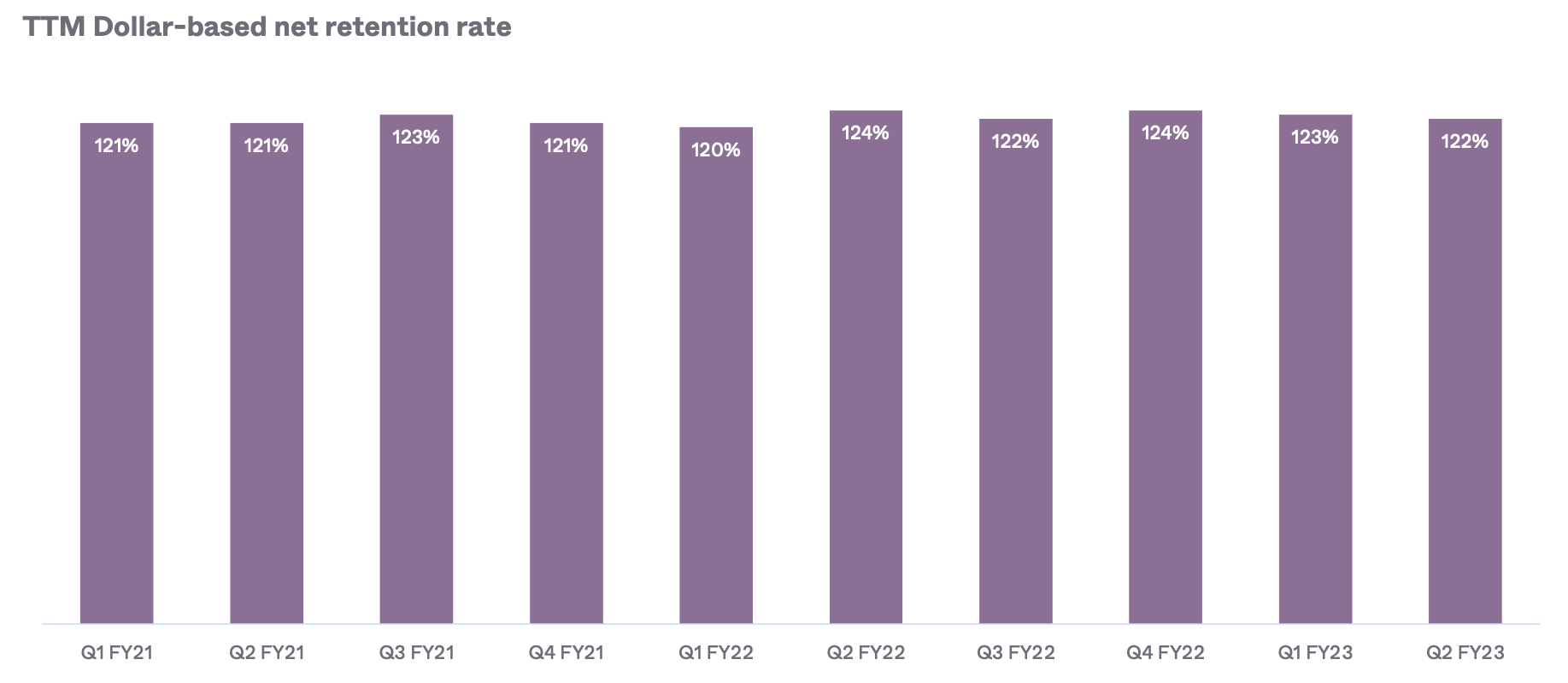

Okta has a super high dollar-based retention rate of 122% which shows customers are staying with the platform by finding it "sticky" and spending more. This was down 2% year-over-year, but I will put this down to general volatility, as that looks to have been the trend. I personally would like to see its dollar-based net retention rate growing, through more upsells.

Retention Rate (Investor Presentation)

{kind=link}

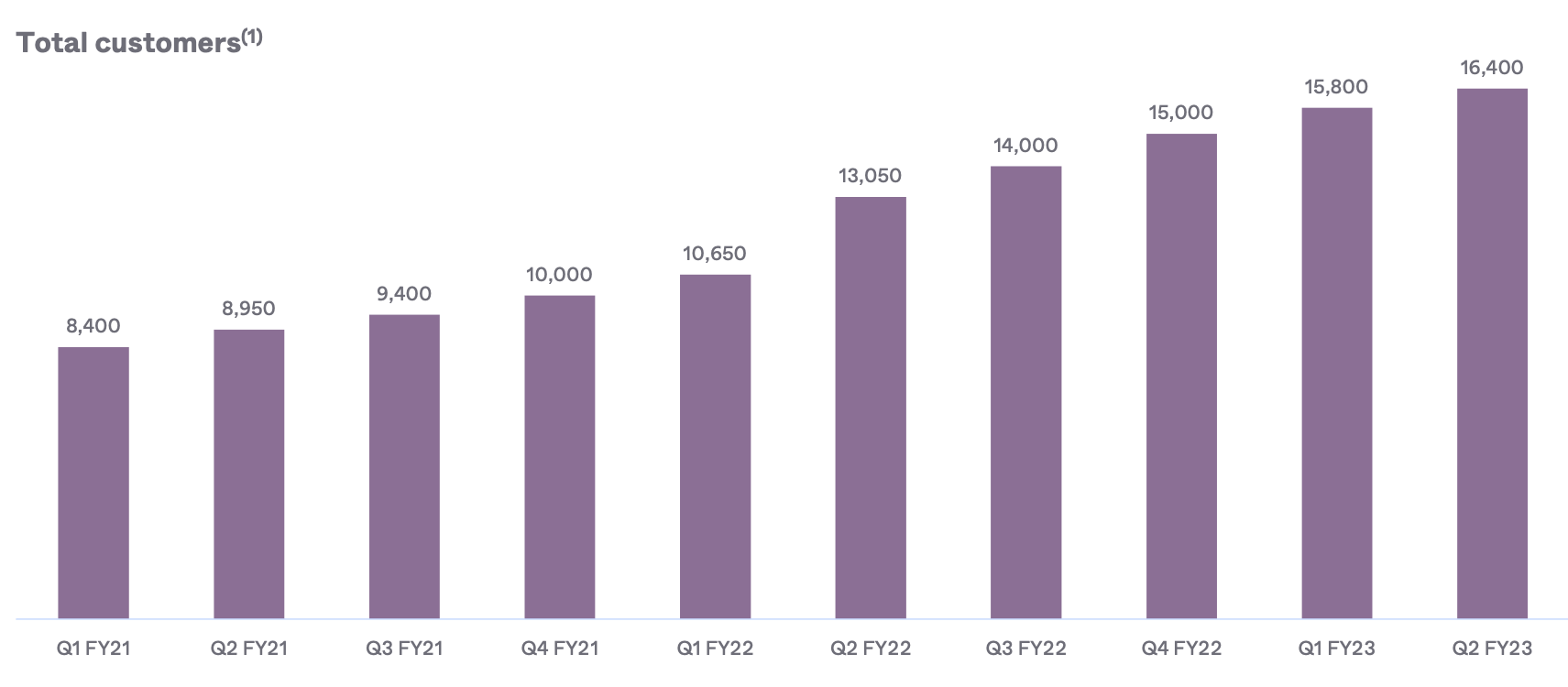

Okta had 16,400 customers as of Q2 which was up by nearly 26% year-over-year. Its customers include Zoom, Major League Baseball, Nasdaq, MGM resorts, Pret and many more.

{kind=link}

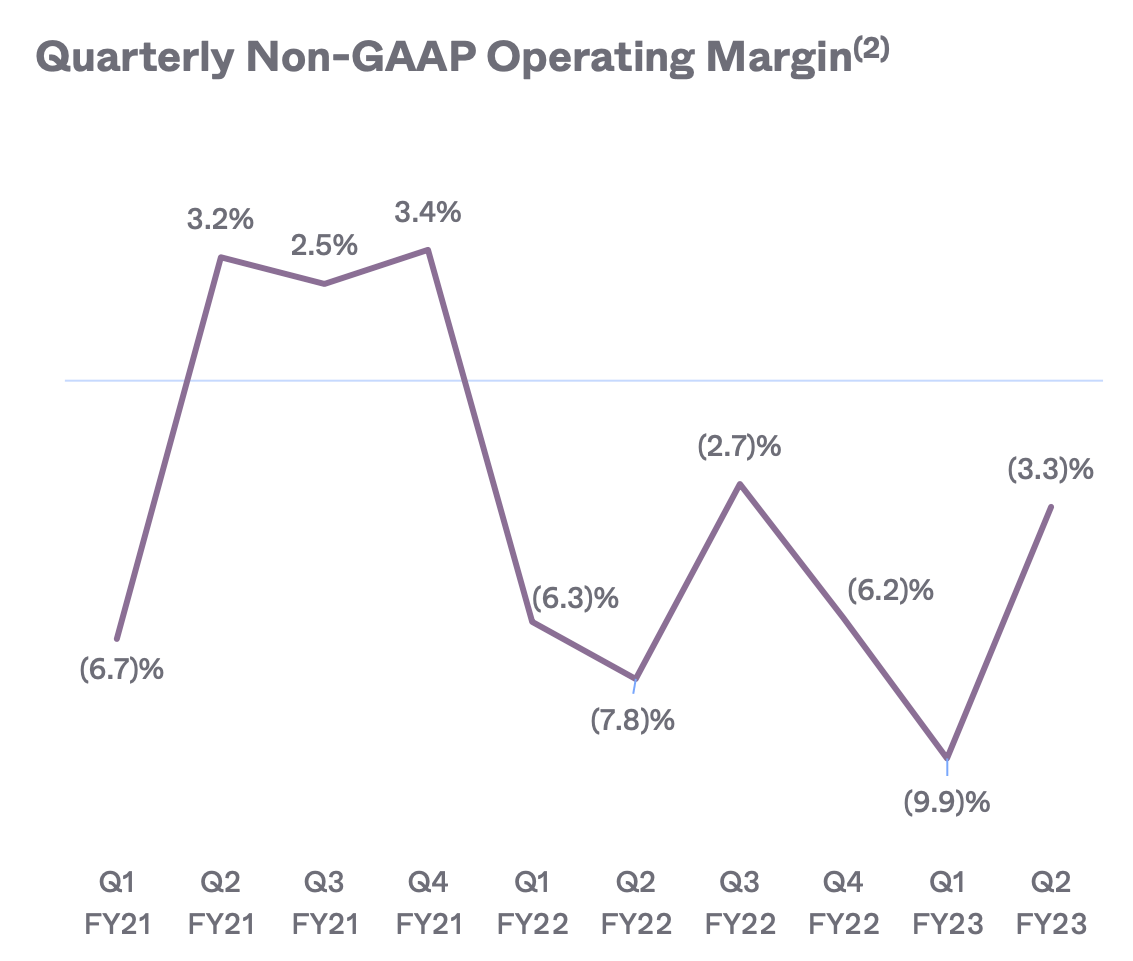

Okta's non-GAAP Gross Margin popped by 30 basis points year-over-year to 76.8% which is positive overall. Its GAAP operating loss narrowed to $208 million or 46% of revenue, compared to $263 million or 83% of revenue last year. On a Non-GAAP basis, the company's operating margin has been volatile but it has improved since last year and last quarter, which is a positive sign.

Operating Margin Non GAAP (Investor Presentation Q2)

{kind=link}

Earnings Per Share was -$1.34 on a GAAP basis which beat analyst estimates by $0.13. The company generated Net Cash from operations of $19 million. Free Cash Flow was minus $24 million or -5% of total revenue which was worse than the minus $4 million or -1% of revenue generated previously.

Poor Guidance

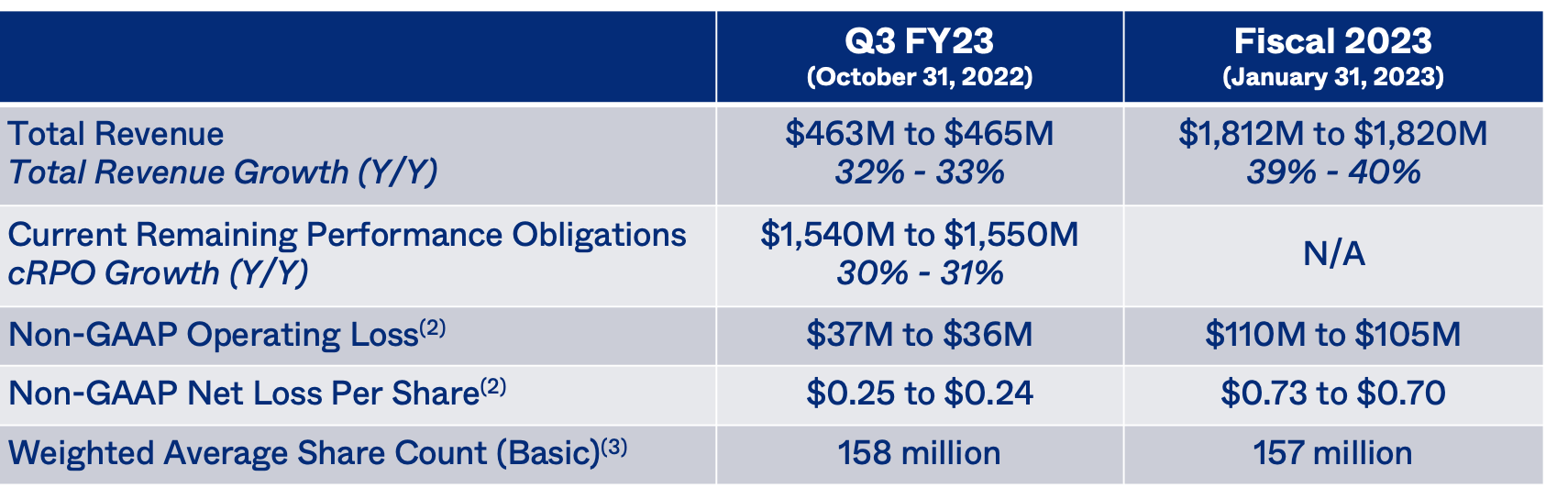

Moving forward, management's strategy is to expand internationally, reduce spending and improve profitability. They also plan to develop a go-to-market strategy for the combined Auth0 and Okta sales team. Despite the bold words Revenue growth is forecasted to slow to between 32% and 33% in Q3 FY23, with between $463m and $465 million expected. This would represent an increase of just 2.8% over the prior quarter, which would be ~one-third of the 9% growth rate achieved in the prior Q/Q. I believe this is the main reason the stock price has plummeted by 33%. Quarterly RPO is also expected to its growth rate to slow down to between 30% and 31% year-over-year. Down from the 36% rate generated previously.

Outlook (Okta Earnings Presentation)

{kind=link}

Losses are also expected to widen from a Non-GAAP operating loss of $15 million in Q2 to $37 million to $36 million in Q3 which isn't a great sign.

Okta has a stable balance sheet with $2.48 billion in cash, cash equivalents and short-term investments. In addition to $2.1 billion in convertible senior note debt. As this is "convertible debt" it means the owner could convert to equity which would dilute shareholders, which is a risk. The good news is just $5 million of this debt is current, due within the next 2 years.

Advanced Valuation

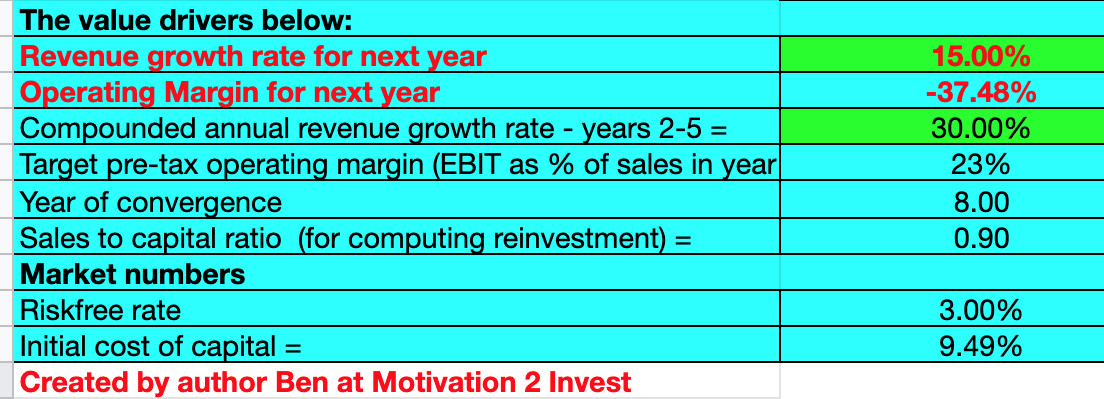

In order to value Okta, I have plugged the latest financials into my advanced valuation model which uses the discounted cash flow ("DCF") method of valuation. I have forecasted just 10% revenue for next year and then 20% for the next 2 to 5 years to be conservative.

Stock Investing Valuation (created by author Ben at Motivation 2 Invest)

{kind=link}

I have also forecasted its operating margin to grow over the next 8 years to 23%, as the company reaches greater scale and its upsell strategy starts to improve.

Okta stock valuation (created by author Ben at Motivation 2 Invest)

{kind=link}

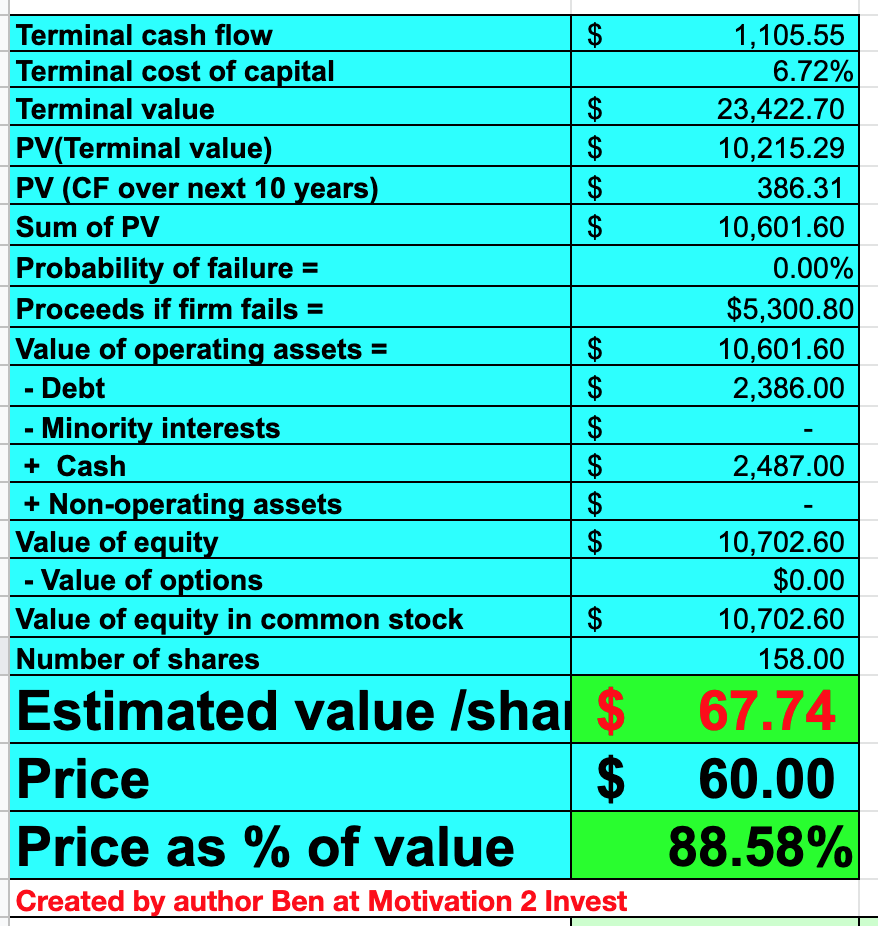

Given these factors, I get a fair value of $67 per share. The stock is trading at ~$64 per share at the time of writing and thus is undervalued.

As an extra datapoint, Okta trades at a Price to Sales ratio = 6.38 which is 74% cheaper than its 5 year average.

Okta is also trading at a Price to Sales [forward] ratio = 5.5, which is the cheapest cybersecurity stock in the sector (see purple line), relative to 6 other cybersecurity companies. The closest direct competitor to Okta on this list would be Cyberark software, which trades at a Price to Sales forward ratio = 9, which is more expensive than Okta.

Risks

Slow Acquisition Integration

Okta is experiencing higher attrition than expected from the Auth0 sales force, post-acquisition. This is because many Auth0 reps are used to working in a small company environment and they do not like the new structure and thus many have left. The company is also reevaluating its go-to-market strategy to avoid confusing customers with the Okta and Auth0 products effectively competing with each other to a certain extent. This acquisition has come with a lot of friction and meant that the company has had to hire new people to replace those which left (which adds extra cost).

Many analysts such as Gregg Moskowitz from Mizuho have slashed price targets for this reason, but still have a target of $110, which is significantly higher than the $60 share price at the time of writing.

Management has historically been conservative with revenue estimates, so hopefully that will continue. But given the forecasted recession, a pullback in new IT spending temporarily is likely.

High Stock-based Compensation

Okta paid out approximately $171 million in stock-based compensation, for the second quarter of FY23. Now although this is not a cash expense, it is still a form of expense and is a large portion of the company's Non-GAAP to GAAP reconciliation. As someone who has worked for many large technology companies in the past, I understand deeply that stock-based compensation is necessary to attract and retain the best talent. However, long term a company should show operating leverage in this metric and be able to pay employees from profits.

Final Thoughts

Okta is an industry leader in Identity Access management and the company has produced strong financial results in Q2. Management's tepid guidance has spooked Wall Street and as we head into a recessionary environment I expect more pain to come. But despite this, the 33% crash in stock price has opened up opportunities of value, and thus opening a position at these levels wouldn't be crazy, as a long-term investment. However, investors may wish to watch the technicals and wait for positive sentiment before diving in as the stock could fall further.

For further details see:

Okta: 33% Crash Equals A Buying Opportunity