OLPX - Olaplex: Another Haircut

2023-08-10 06:47:46 ET

Summary

- Olaplex's second quarter earnings were disappointing, with a decline in net sales and weak performance in the Professional and Specialty Retail channels.

- Increased competition and negative brand perception have impacted Olaplex's business, adding to the problems caused by customer inventory destocking.

- Olaplex's stock may now appear undervalued, but this could prove illusory. Investors should not expect a rapid return to prior levels of profitability and growth.

Olaplex's (OLPX) second quarter earnings were disappointing across most metrics, adding to the company's fall from grace since listing nearly 2 years ago. I highlighted the risk inherent in Olaplex's stock last year, and most of these risks have come to fruition to a surprising extent. Investors are now left to wonder how much of the company's current predicament is the result of temporary headwinds and how much represents a new normal. While it may be tempting to assume a rapid return to growth and improvement in margins, competition is increasing, and recent cost increases are likely to prove sticky. Given the probability of permanently lower margins going forward, and uncertain growth prospects, Olaplex's stock is still not an obvious buy, even at current prices.

Headwinds and Response

Olaplex's business is reportedly being negatively impacted by increased competition and misinformation. This has had an outsized impact on the Professional channel, where Olaplex believes some stylists now have a lower opinion of the brand. While the negative buzz around Olaplex potentially causing hair loss appears to be falling off, this is the first time that Olaplex has called out competition as an issue.

Customers also still have elevated inventory levels in the Specialty Retail and Professional channels, with destocking contributing to weak demand. In the first half of 2023, Olaplex's net sales declined 44% , while sell out at key accounts was down approximately 26%. This trend was moderately worse in the second quarter than the first quarter. Olaplex believes that customer inventory levels are normalizing though, which should reduce this problem going forward.

To try and combat competition and negative brand perceptions, Olaplex is increasing its investments in upper funnel marketing to try and build brand equity. Olaplex is also increasing support for the professional community.

Financial Analysis

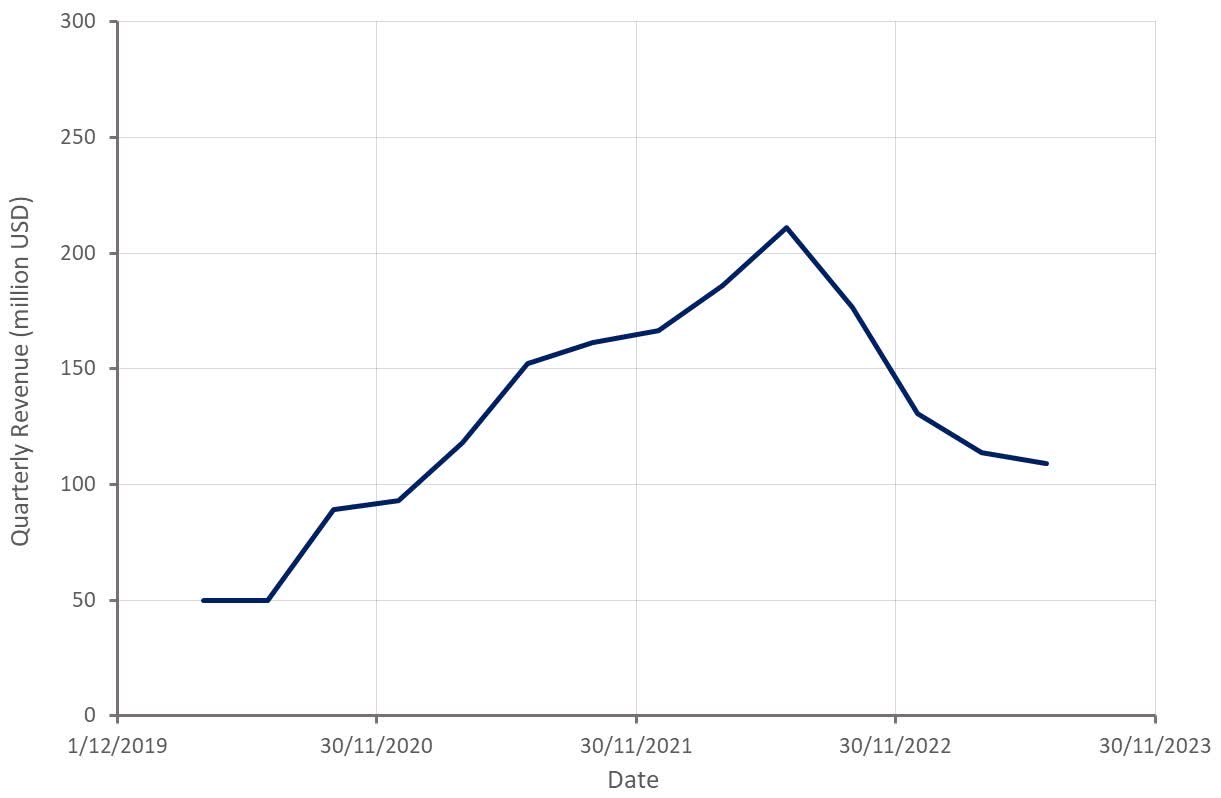

Net sales in the second quarter were only 109 million USD , which was below expectations of a modest sequential improvement from the first quarter. This represents roughly a 48% decline YoY and a 4% decline sequentially. Net sales decreased 58.7% YoY in the US and 34.0% internationally.

Olaplex is now only expecting 445-465 million USD net sales for FY2023, which would be a 35% decline at the mid-point. The reduction in guidance was attributed to an expectation of lower gains from new product introductions and increased distribution.

Figure 1: Olaplex Revenue (source: Created by author using data from Olaplex)

{kind=link}

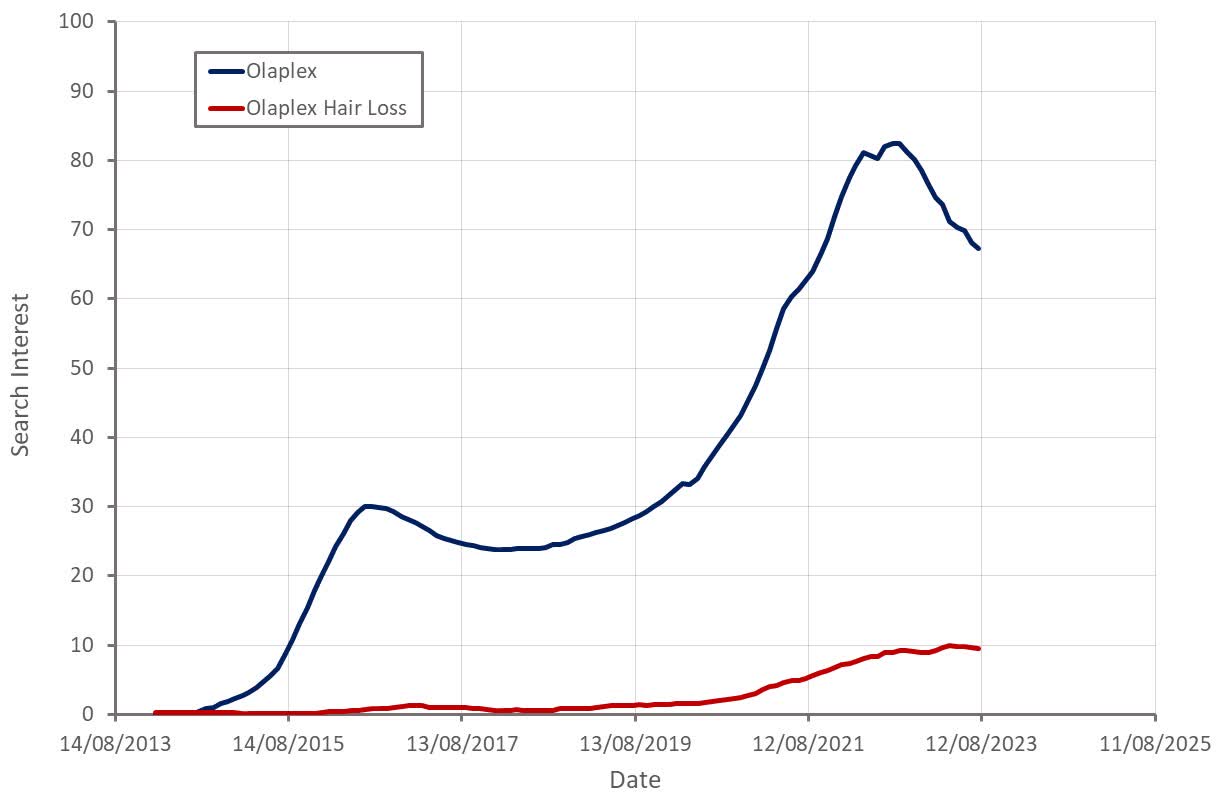

Allegations of Olaplex causing hair loss still appear to be a concern for management, although this issue may now largely be behind the company. Search interest related to Olaplex causing hair loss is falling, and Olaplex's motion to sever and dismiss claims that its products cause hair loss has been granted . How much damage has been caused to the brand already, and whether sales growth now reaccelerates remains to be seen.

Figure 2: Olaplex Search Interest (source: Created by author using data from Google Trends)

{kind=link}

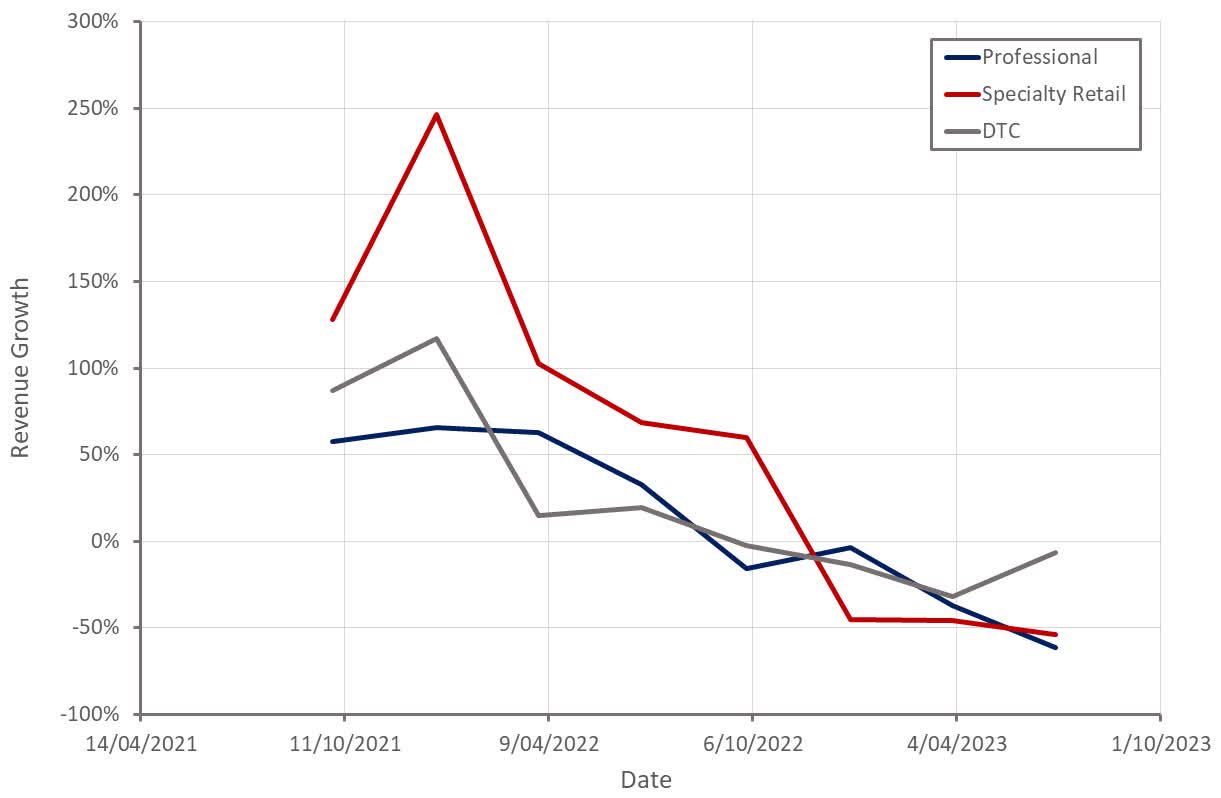

Sales were weak across channels in the second quarter, with the Professional and Specialty Retail channels performing particularly poorly. The Professional and Specialty Retail channels experienced softer demand and some customers right sized their inventory positions in response to current trends.

Figure 3: Olaplex Revenue Growth by Channel (source: Created by author using data from Olaplex)

{kind=link}

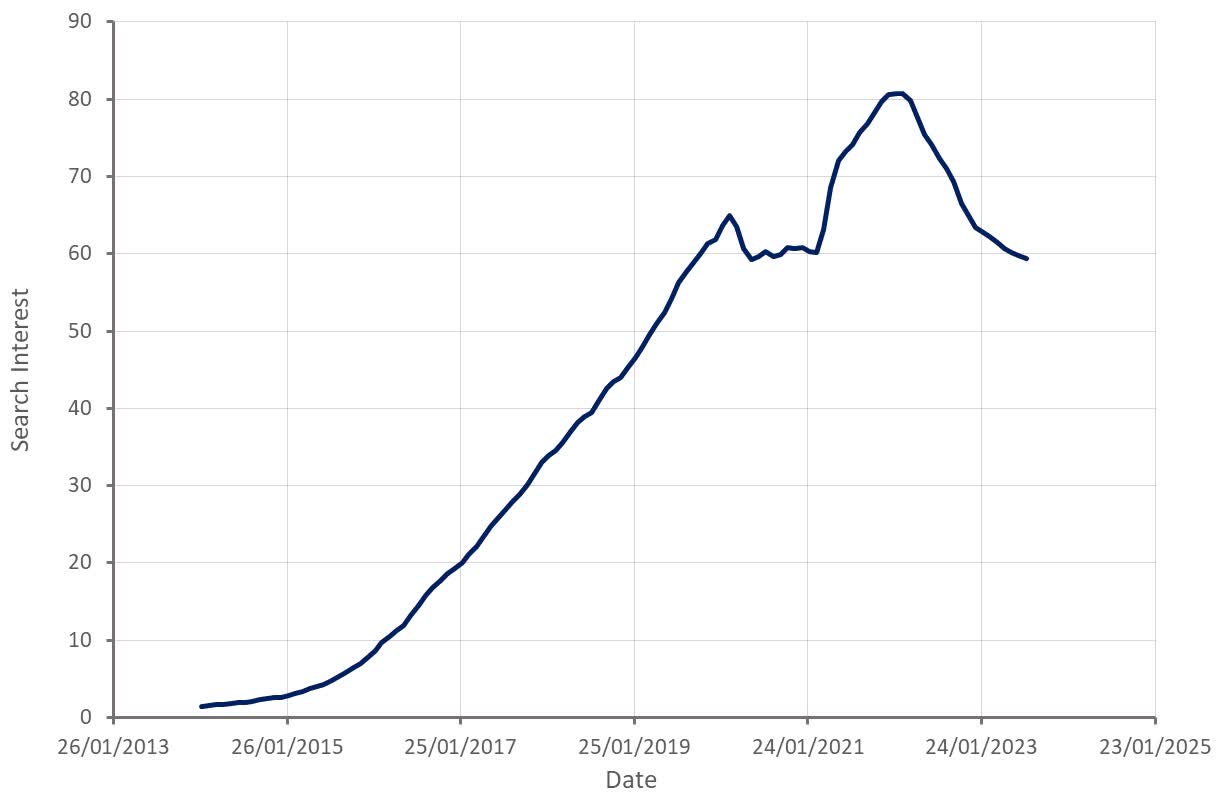

Sales through the Professional channel were likely boosted post-pandemic by the strong economic environment, and the fact that demand was suppressed during lockdowns. This has been correcting over the past 18 months, a process which now appears to be largely over. This could result in better sales through the Professional channel going forward, dependent on customer inventory levels and the macro environment.

Figure 4: Hairdresser Search Interest (source: Created by author using data from Google Trends)

{kind=link}

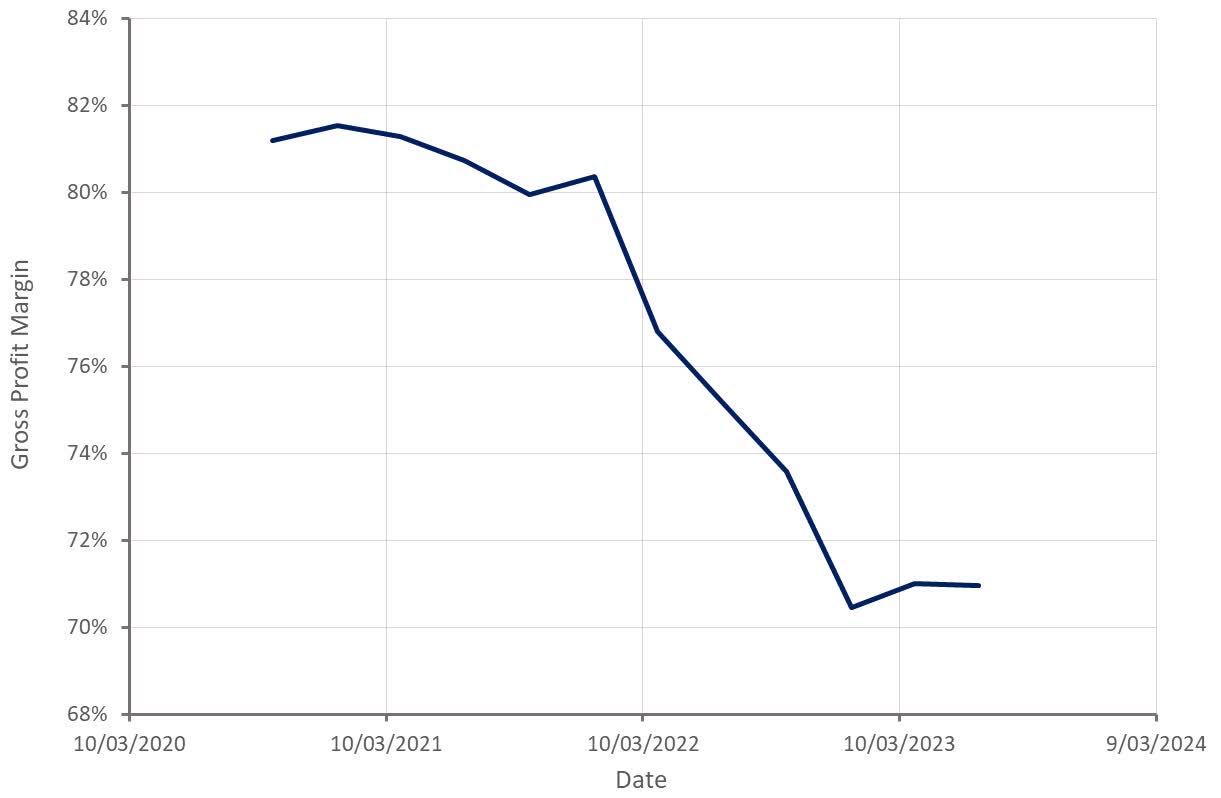

In addition to weak sales, Olaplex's margins have been under pressure. While gross profit margins have been fairly flat in recent quarters, they are still well off their peaks. Olaplex is expecting a return to mid-70s gross margins next year but given the reasons for lower margins, this is not clear. Competition and a mix shift away from DTC could prevent margins from rebounding in 2024.

Table 1: Contributors to Gross Profit Margin Changes (source: Created by author using data from Olaplex) Figure 5: Olaplex Gross Profit Margin (source: Created by author using data from Olaplex)

{kind=link}

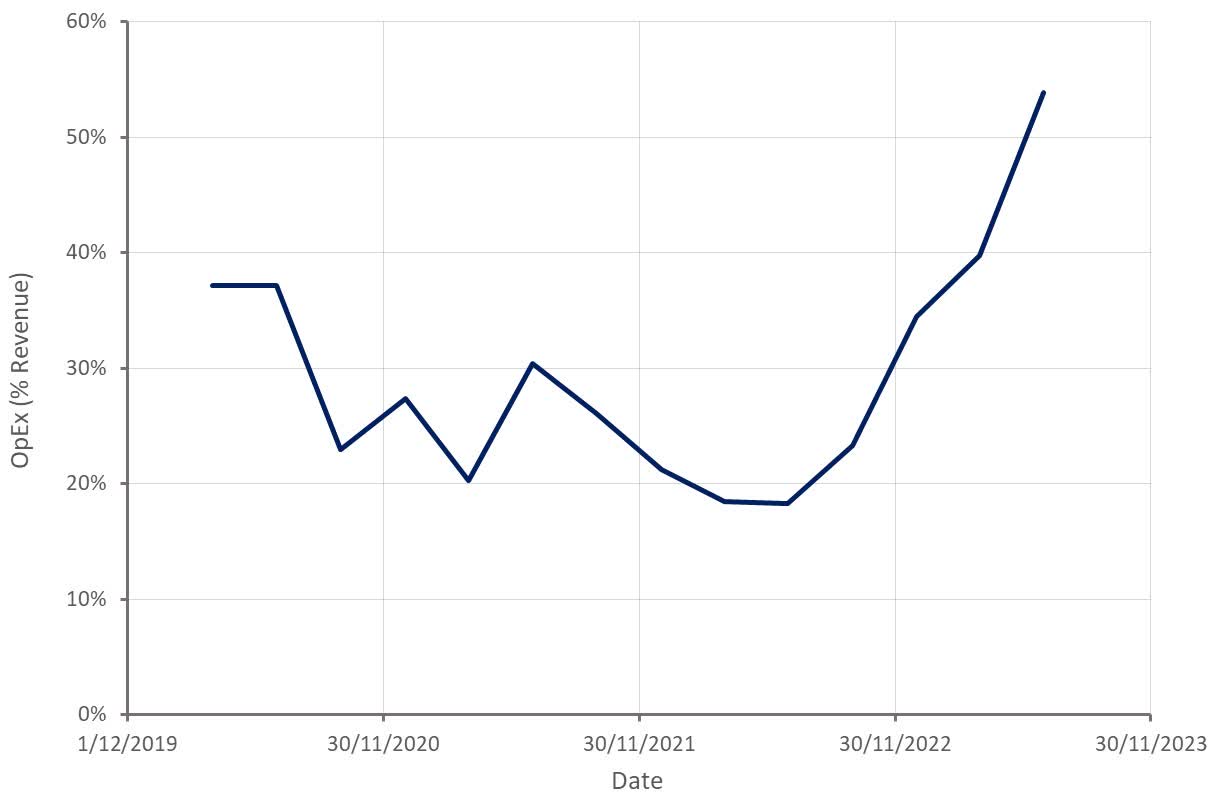

In addition to lower gross profit margins, the burden of operating expenses has been rising rapidly, causing operating profit margins to fall sharply. The rise in operating expenses has largely been attributed to marketing and an expanded workforce.

While operating profit margins are likely to rebound at some point, they are unlikely to return to their pandemic highs. In the past Olaplex had a skeleton workforce supporting a product that sold itself. Increased competition and a softer demand environment are forcing Olaplex to invest more heavily in its business. Olaplex's headcount is now increasing rapidly as the company builds out the internal capabilities befitting a multi-billion dollar operation.

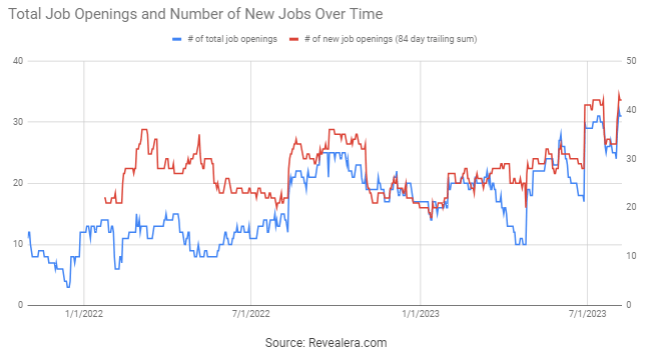

Figure 6: Olaplex Operating Expenses (source: Created by author using data from Olaplex) Figure 7: Olaplex Job Openings (source: Revealera.com)

{kind=link}

{kind=link}

Valuation

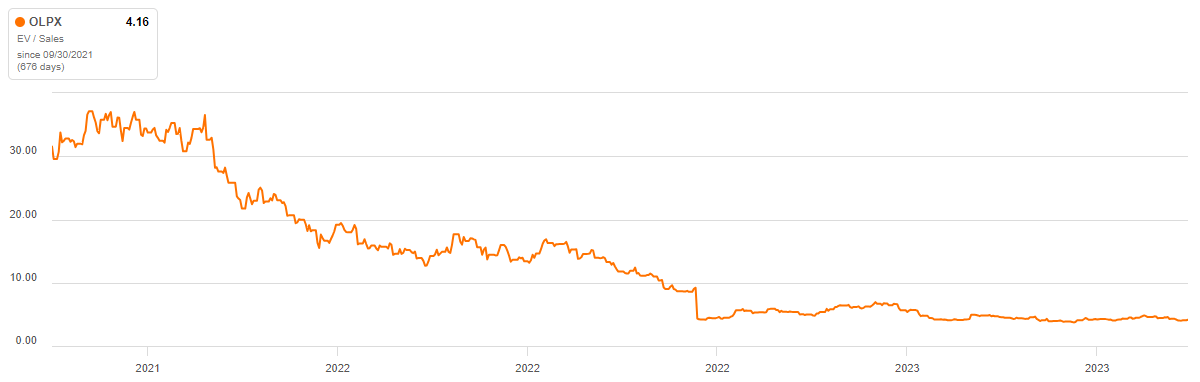

Olaplex's stock has appeared inexpensive based on its PE ratio since October 2022. Despite this, the stock has fallen significantly as earnings have continued to evaporate. Olaplex's operating margins were extremely high in the past, which helped to cover for the company's fairly large debt position. The combination of falling revenue, falling gross profit margins, rising operating expenses and large interest costs caused Olaplex's net profit margin to fall into the single digits in the second quarter.

Income should recover from current levels, but the amount of leverage inherent in the business makes it difficult to estimate what a normal level of income is. If growth rebounds in 2024, income will increase rapidly, and the stock could prove deeply undervalued. If demand remains soft, the stock could still fall a lot further, as there would be little in the way of earnings to support the stock.

Figure 8: Olaplex EV/S Multiple (source: Seeking Alpha)

{kind=link}

For further details see:

Olaplex: Another Haircut