OLPX - Olaplex: Trying To Find A Bottom

2023-06-01 11:48:45 ET

Summary

- Olaplex faces declining revenues and rising costs, with 2023 being a rebuild year for the company.

- The company is launching new products and expanding into international markets, which could help offset demand issues.

- Despite potential growth opportunities, investments will weigh on margins, and consumer spending headwinds could create further downside risk.

After an extremely strong 2021, Olaplex ( OLPX ) has rapidly transitioned from firing on all cylinders to calling 2023 a rebuild year. Revenues are declining and costs are rising as the company invests to try and build a more sustainable organization. Earnings are set to continue falling, which could keep the stock price low in the near term, and the situation could be exacerbated by consumer spending headwinds.

First quarter results were ahead of management expectations, despite being objectively poor. Weak results have been attributed to a number of factors, including:

- The macroenvironment

- Increased competition

- Increased discounting

- Brand misinformation

Despite these headwinds, Olaplex believes that the category and its business both remain strong. Olaplex continues to introduce new products, which may offset some of the company's demand problems. No. 4D Clean Volume Detox Dry Shampoo was launched in the first quarter and the product is reportedly performing well. 4D is the number one dry shampoo at Sephora and launched with other Specialty Retailers and DTC partners in early May.

Olaplex launched its first product outside of the hair care category in March. Lashbond is an eyelash-enhancing serum that promotes the appearance of thicker lashes. Performance has reportedly been strong, with Lashbond already a top 10 beauty SKU for Space NK in the UK. Olaplex has been promoting the potential of its technology in adjacent categories for over 12 months, so this is an important step in expanding the company's addressable market.

International markets are another potential growth area, as Olaplex is currently relatively under-penetrated. Olaplex is rolling out into roughly 280 additional Douglas stores across Germany and the Netherlands. The company is also partnering with Dufry to enter 12 UK airports. Olaplex also currently has a limited presence in Asia, the Middle East, and Latin America, providing additional potential growth opportunities.

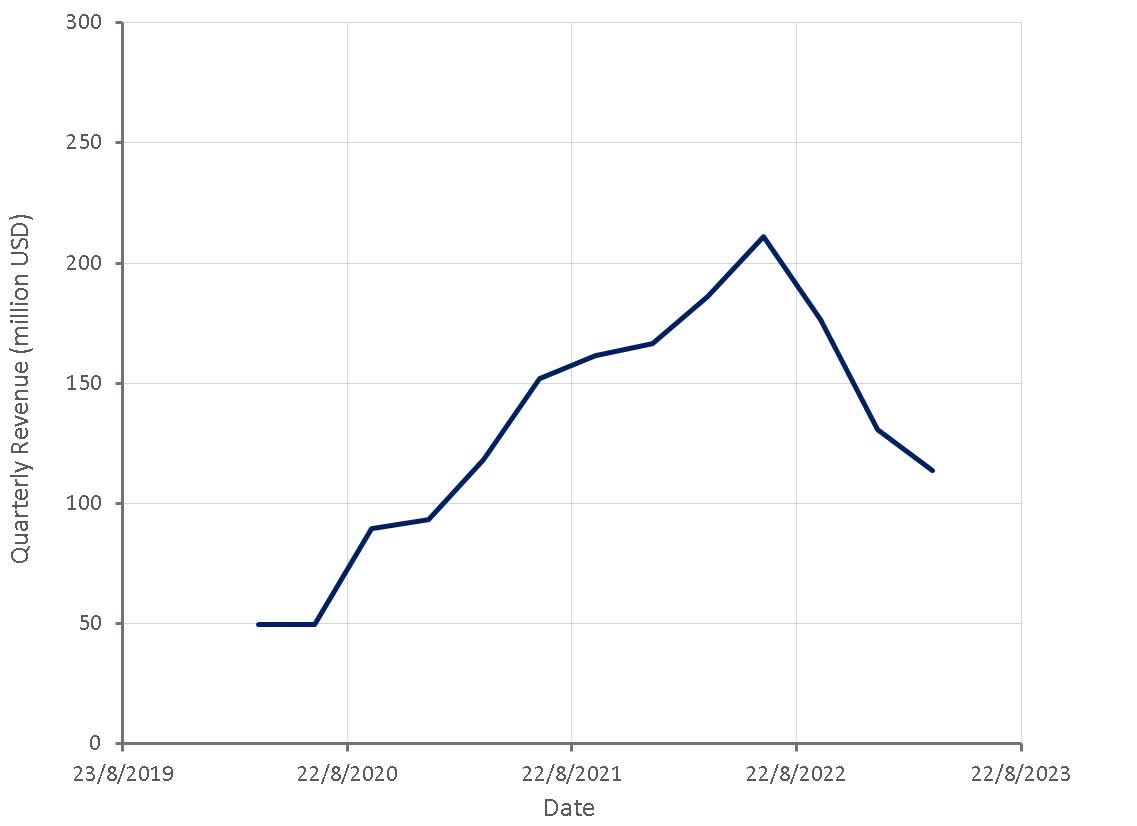

First quarter sales declined on the back of lower consumer demand, excess customer inventories, and a difficult comparable period in 2022. Customer inventory rebalancing had an estimated impact of around 21 million USD, and the shipping of inventory in preparation for the Ulta Beauty ( ULTA ) launch added approximately 10 million USD in the first quarter of 2022. Correcting for these effects implies a -23% growth rate YoY, which is somewhat better than the actual -39% recorded.

International sales were flat YoY in the first quarter and the US was down around 60%. The inventory rebalancing and Ulta Beauty launch specifically impacted the US.

Revenue in 2023 is expected to be approximately -15% YoY, although Olaplex expects to return to growth in the fourth quarter. This should help to reverse some of the company's current issues, but it is dependent on the macro environment remaining reasonably stable.

Figure 1: Olaplex Revenue (Created by author using data from Olaplex)

{kind=link}

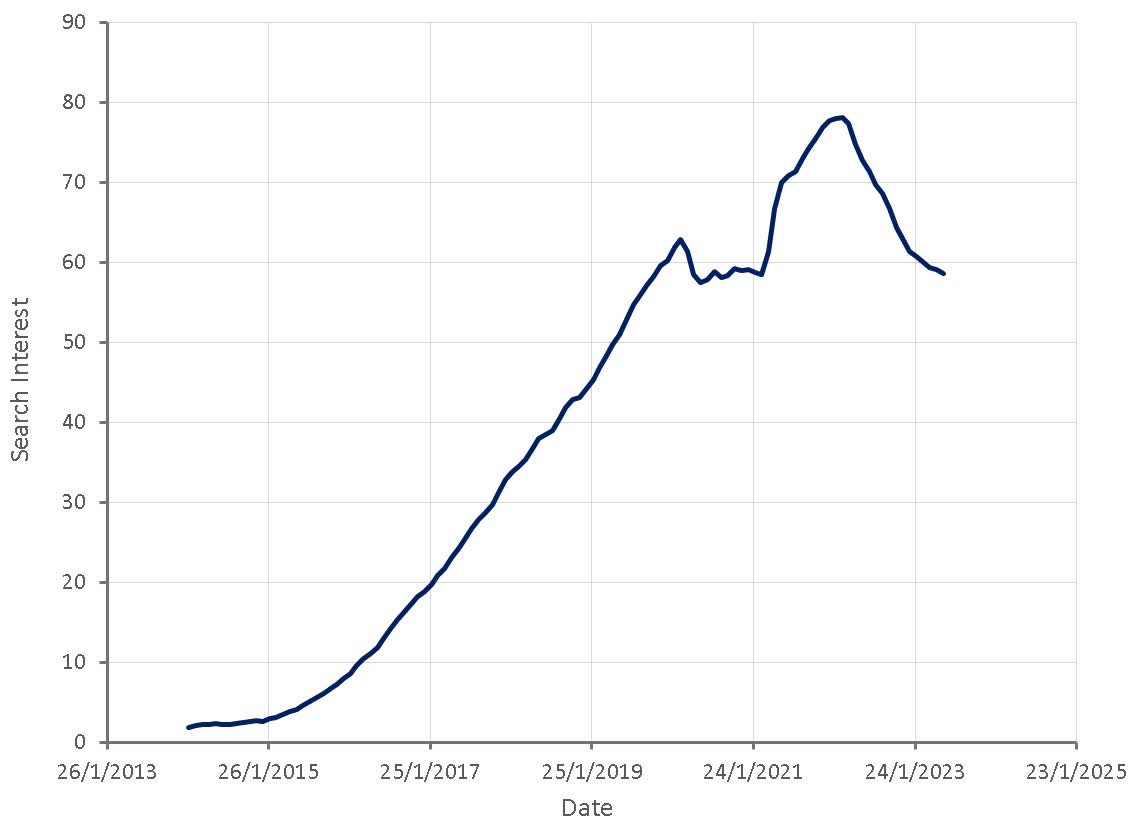

Internet search data indicates that 2021 and 2022 were large bubbles for consumer interest in hair stylists. This likely provided unsustainable tailwinds for Olaplex that are now in the process of unwinding. While the negative trend appears to be easing, the Pro channel may not be a source of growth for some time.

Figure 2: "Hair Stylist" Search Interest (Created by author using data from Google Trends)

{kind=link}

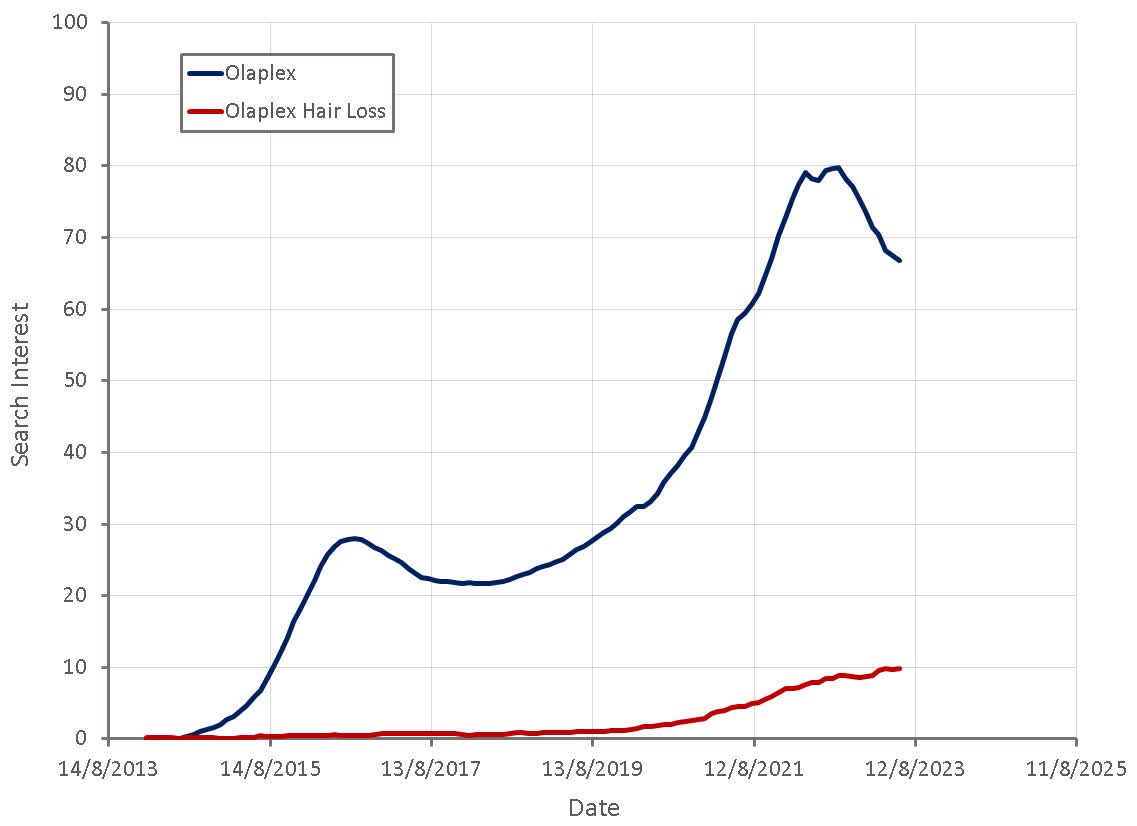

Product concerns continue to hang over Olaplex and management clearly believes that this is impacting sales, as the company is investing in initiatives to try and correct brand misperceptions. This is somewhat at odds with management discussions of brand strength, though. According to a third-party brand tracking, Olaplex reportedly showed consistently robust metrics through March. Search interest for "Olaplex" + "hair loss" has been increasing, but this appears to predate most of Olaplex's growth problems.

Figure 3: Olaplex Search Interest (Created by author using data from Google Trends)

{kind=link}

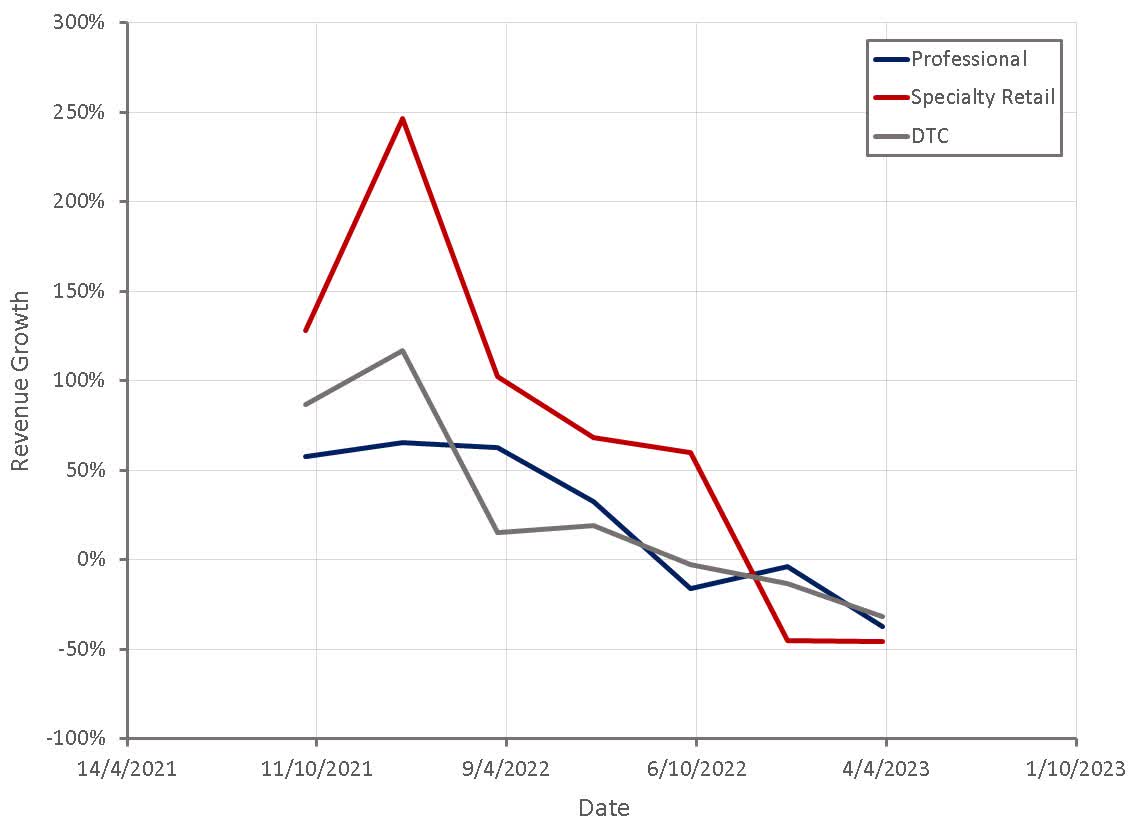

Olaplex's sales were down significantly across channels in the first quarter. Front of salon sales were down 9% YoY in the fourth quarter, indicating that soft demand is not just an Olaplex issue.

Figure 4: Olaplex Revenue Growth by Channel (Created by author using data from Olaplex)

{kind=link}

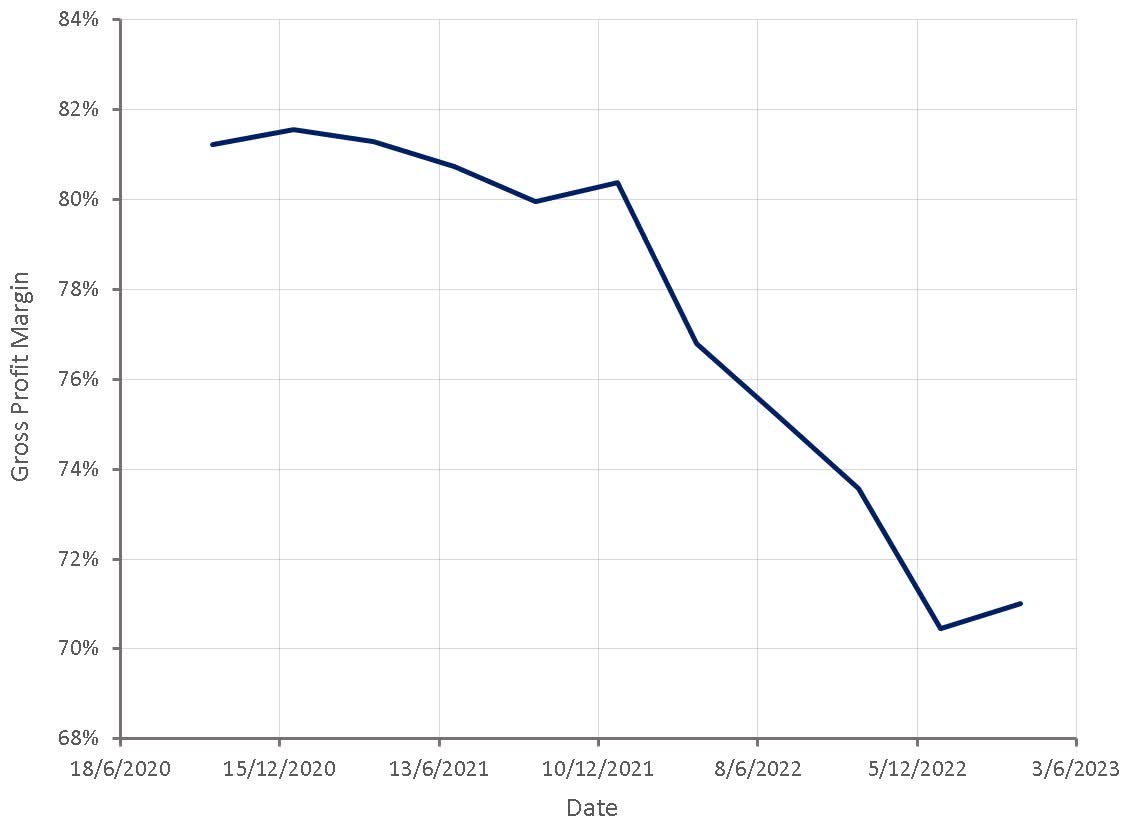

Olaplex's gross profit margin has contracted significantly over the past year due to a combination of:

- Lower sales

- Increased warehousing and distribution costs

- Increased inventory obsolescence reserves

- Increased product costs

- Increased sampling

- Unfavorable customer mix

This has been somewhat offset by price increases and a favorable channel mix.

Figure 5: Olaplex Gross Profit Margin (Created by author using data from Olaplex)

{kind=link}

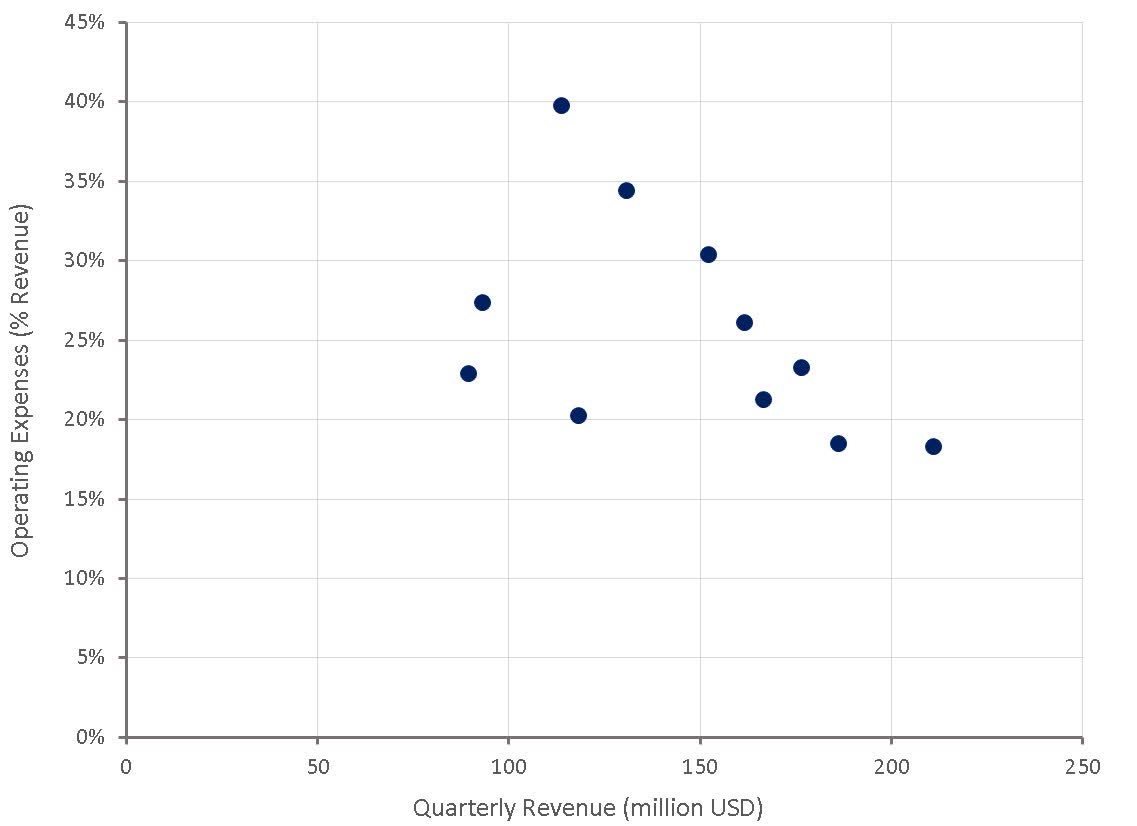

The burden of Olaplex's operating expenses is also increasing as the company continues to invest in the business and sales decline. Sales and marketing investments include education, strengthening Pro and Retail partnerships, and improved PR. Olaplex is also implementing a full-funnel marketing approach this year to generate awareness and support brand health. Sales and marketing are expected to increase from 6% of sales in 2022 to 12% of sales in 2023.

Figure 6: Olaplex Operating Expenses (Created by author using data from Olaplex)

{kind=link}

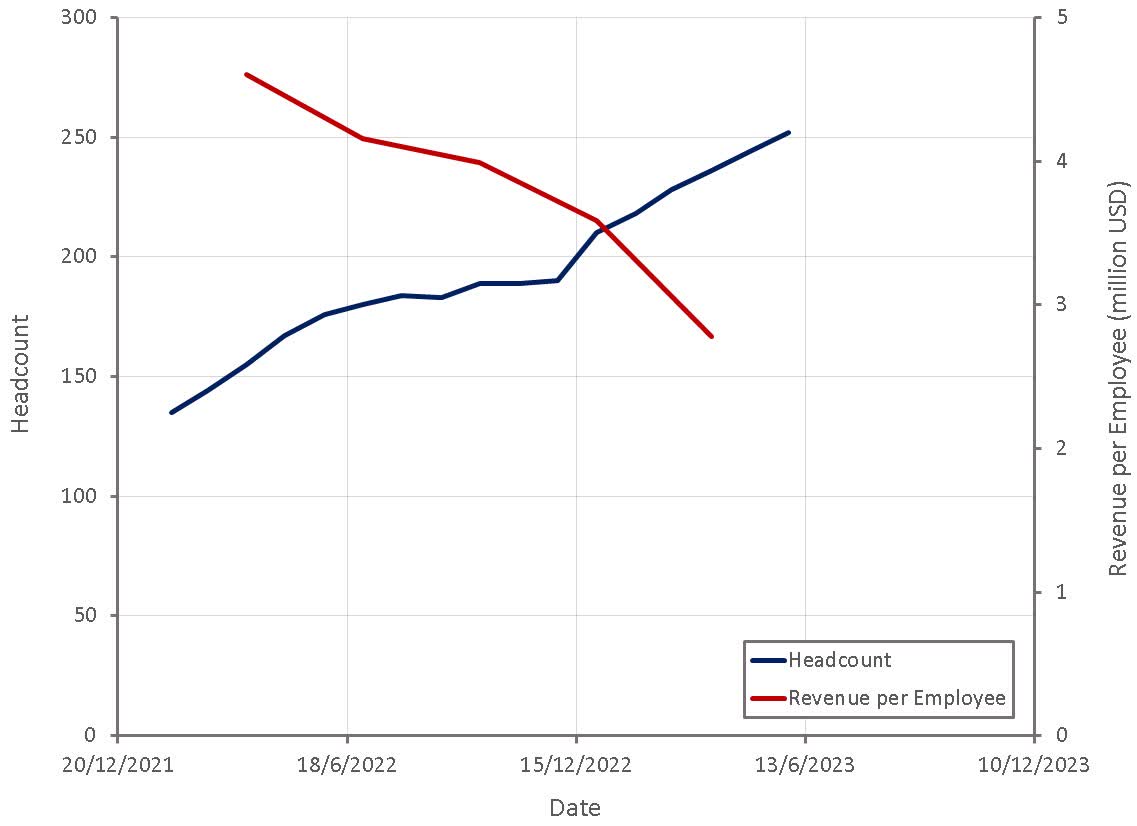

Olaplex plans on continuing to build its team in 2023 and hiring has been solid in support of this, despite declining revenue and profitability. This will contribute to lower profit margins going forward, although Olaplex's revenue per employee remains extremely high.

Figure 7: Olaplex Employees (Created by author using data from LinkedIn and Olaplex)

{kind=link}

{kind=link}

Olaplex's stock looks superficially cheap, but revenues will continue to decline and margins will likely compress further. Geographic expansion, new products, and expansion into adjacent categories are all potential growth opportunities, but this will require investments that will weigh on margins. The current valuation is probably reasonable given what Olaplex's profits are likely to be in 2023. Consumer spending could weaken in the second half of 2023 with savings coming under pressure and student loan repayments restarting, which creates further downside risk.

For further details see:

Olaplex: Trying To Find A Bottom