OLPX - Olaplex: Undervalued Beauty Gem With Big Potential Upside

Summary

- Olaplex manufactures and sells hair care products. The brand blew up in recent years on social media due to the quality of its products but has faced scrutiny also.

- Olaplex's financial performance has been fantastic, operating with an EBITDA margin of 63% and a NI margin of 38%. This is far superior to any of its peers.

- The business is facing slowing demand and the necessity to refocus on growth, but we believe this is only temporary with no systemic issues.

- Olaplex's peers are trading at an average EBITDA multiple of 30x, with Olaplex only at 9x. Our view is that the business has an impressive 77% upside from here.

- Olaplex is one of our highest conviction plays in the coming year.

Company description:

Olaplex Holdings (OLPX) manufactures and sells hair care products. The company offers shampoos and conditioners, as well as other products such as oil, for use in the maintenance and protection of hair. The company distributes its products to professional hair salons, retailers, and consumers.

Olaplex is an interesting product as the company advertises incredible results, is backed by patents, and has reviews to back it up. I have been using the product for over a year and can testify that it is the real deal. It is expensive, but it actually works. The company blew up on TikTok in recent years and developed a cult fan base. Initially targeted at Salons and Hairdressers, the company saw an opportunity to expand to an at-home range. By 2021 , the product became the hottest haircare brand in the world, overtaking Dyson and also becoming Sephora's best-selling product.

Things have changed since March '22. The company was forced to remove Lilial from its best-selling product, No. 3, due to its links to infertility in animals. The European Commission in 2019 stated it "cannot be considered as safe". Consumer opinion on the brand changed rapidly and just as Tik Tok built the brand up, many began tearing the brand down. Olaplex has still performed well, as they stressed that the fragrance was not an active/functional ingredient and so did not impact its effectiveness.

If this wasn't bad enough, in recent weeks, 30 women have filed a lawsuit against the business claiming the product caused serious injury to their hair. Olaplex has been quick to deny these allegations but it looks like the business will go through another cycle of bad press as the media begin to run with this story.

Olaplex's share price has had an unfortunate time since it first joined the stock market, losing 76% of its value in just over a year. This has been driven by the scandal mentioned above, as well as the outlook of the business changing, resulting in investors changing their view of the business.

Investment thesis:

Olaplex is experiencing a host of issues right now and facing an exodus of many customers, especially if this current lawsuit has any credence. This will likely contribute to a near-term bottoming of the stock price. The company does have a fundamentally strong foundation, however, and has the scope to generate substantial returns for investors. The real question here is one of risk and reward, how big is the reward and what is the current risk investors are taking? This paper seeks to assess these factors.

Financials:

Olaplex Financials (Tikr Terminal)

Olaplex has performed incredibly well during the last few years, producing growth and profitability at impressive levels.

Revenue has grown at a CAGR of 71%, driven by the rapid rise of the brand in social circles and success in selling the value of its product. We should note that this has slowed right down in the most recent period, one of the reasons the stock price has declined, suggesting that revenue cannot grow at the current level.

One of the reasons we think growth has slowed down is due to the business relying on word-of-mouth/social media marketing to progress this far. This has been highly successful but the business is clearly feeling the effects of not conducting traditional spending. For example, L'Oreal (LRLCY), an established market leader, spends almost 50% of its revenue on S&A expenditure. Olaplex on the other hand is spending 14% in the LTM period. It is highly likely that management will need to increase their spending, which will contract margins, but is likely required in order to grow the business.

The company's current profitability profile is incredible. With Net Income and FCF margins in the 30% region, it's generating substantial returns on capital, even if it is at a small base. Our view is that Management should compromise some of this to kickstart growth, with anything above 20% being equally as attractive if partnered with better growth.

Olaplex has experienced a decline in its inventory turnover, reiterating that demand is slowing. In the most recent quarter, sales were up only 9.2% compared to the prior period. Sales to professionals were down 16%, DTC was down 2.6%, with specialty retail (60.1%) driving growth. Further, the company's CCC cycle has increased by over 50 days. Thankfully the company is cash rich and so this is not a concern but the company should look to improve its operational management.

From a credit perspective, we see nothing of concern. The company is generating cash but may need to raise further debt to fund expansion. The company has a comfortable Net Debt / EBITDA ratio of 0.9x and sufficient coverage of interest payments.

Outlook:

Going forward, our view is that Management will turn their focus towards investing in marketing, as the business otherwise faces stagnating demand. The product is good but expensive and so the key is to get it into the hands of consumers to try, once this happens, the change of demand becoming sticky is far more likely. Therefore, we would expect revenue growth in the region of 10-20% in the coming 5 years, with FCF margin declining to the low 20s.

Relative performance:

{kind=link}

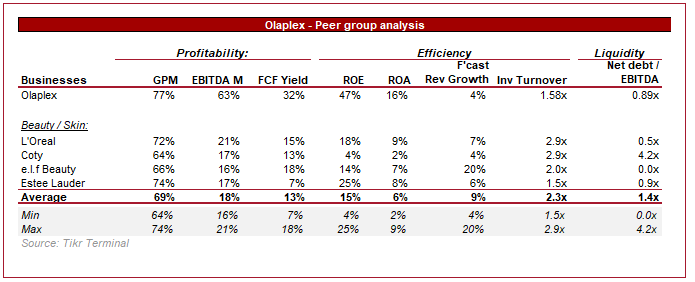

Presented above is a comparison of several beauty / skin businesses and illustrates how Olaplex was able to achieve a premium valuation initially. The peers are generating impressive returns while achieving 5%+ growth, yet Olaplex outperforms them all. Even if margins are to contract, the business would likely remain a market leader in this space.

Macro backdrop:

We are currently experiencing decade-high interest rates, driven by supply-side problems stemming from exiting lockdown and historically relaxed economic policy. This has been a serious issue for consumers globally as they have seen their cost of living increase substantially, with an unequal rise in wages. This is a problem for Olaplex, and one of the reasons it has seen slowing demand. If consumers have less income remaining after meeting their required expenses, they are less likely to spend on non-essential products. Although Olaplex's products are routine-based, one can easily stop using it for a month, or use it every 2 washes, etc, thus easily allowing for usage to be reduced. It's not like face cream which needs to be used daily.

This has been compounded by the economic response to raising interest rates, as now consumers find it far more difficult to borrow, in order to fund their lifestyle. This has not stopped credit card debt from reaching all-time high levels but is clearly not sustainable for most consumers. We worry about how such luxuries will remain robust when consumers are struggling to the degree they are.

Looking ahead, we believe interest rates will rise one or two more times, but only marginally, to finally put the nail in inflation's coffin. This will still mean several more quarters of inflated rates and inflation, which will only compound the struggles faced by consumers. For this reason, we would forecast a tough year for Olaplex in 2023, and given its relative underspending in marketing, this could swing the business to negative growth.

Beauty:

Beauty is a fantastic industry in our view because it operates similarly to a SaaS business. If a consumer likes a product, say Shampoo, they will continue to buy it every few weeks until they are given a reason not to. Further, Olaplex is aimed at women, who tend to shop 59% more than men.

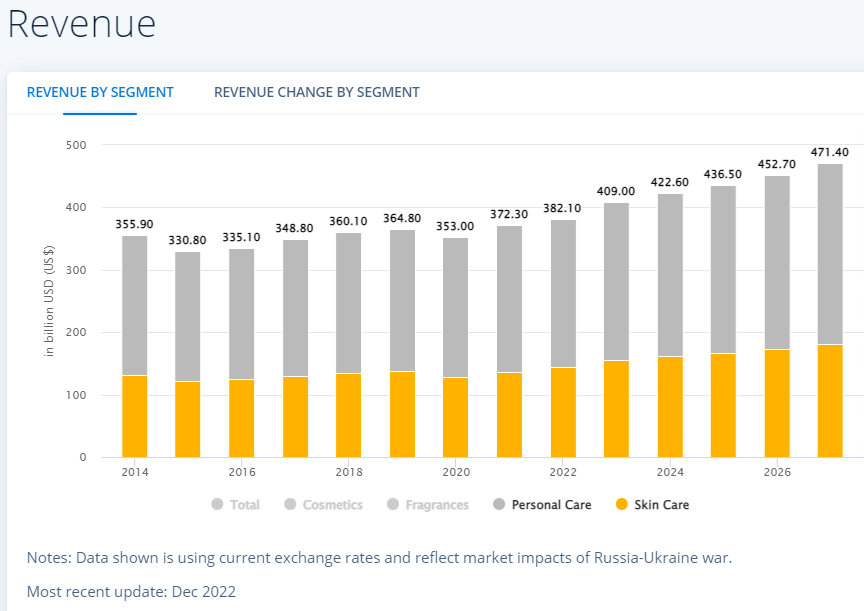

Statista is forecasting personal and skin care to grow at 4.3% in the coming 5 years, reflecting what is impressive growth for a mature industry.

{kind=link}

The beauty of this industry is that it can be relatively sticky, with consumers unwilling to compromise on the products they purchase regularly. We mention this because the question many will have, as we did above, is how impacted will the company be in the next 24-36 months as we feel the effects of inflation. Using L'Oreal as an indicator, the business experienced a 0.4% decline in sales in '09 and usually saw sales growth dip slightly as a result of GDP slowing. That said, the business in general has been very resilient over time and bounced back quickly every time. For this reason, we do not expect a major shock to the business.

Another attractive trait of the industry is that margins remain sticky. Since 2005, L'Oreal's EBITDA margin has fluctuated between 19.5%-22%. Given the level of competition in the market, the level of innovation, and changing consumer trends, one would expect product pricing to gradually decline over time. This has not been the case, with businesses able to increase prices as required to maintain margins.

We are big fans of the fashion/beauty industry as they have the characteristics to produce compounders due to the fundamental quality and rigidity of the industry. Olaplex looks to have found its place here.

Valuation:

Peer group valuation (Tikr Terminal)

Presented above are the valuations of the beauty businesses we assessed earlier, unsurprisingly they are trading at a rich valuation.

Olaplex on the other hand is not. The business is only trading at 9x EBITDA, with analysts currently believing the upside to be 40%. This is a bizarre valuation as it suggests Olaplex will decline in profitability down to the level of its peers, as the EV/Revenue multiple is in line. We struggle to see this occurring given the margin superiority.

Our fair value is a conservative 15x, which reflects the premium nature of Olaplex meaning it will not gain a mass following, and the fact its margins will need to contract. Even then, the business likely deserves a higher multiple.

We believe the current valuation is a reflection of investors changing their view on the company's growth, as it won't continue at 50% anymore - we know that now. However, the business is clearly oversold.

Risks:

We see three key risks with investing in Olaplex:

- A genuine problem with their products - The lawsuit is interesting becomes millions of people have used the products for years yet we are only now seeing a case. This is not to say it is unfounded, but until further details are provided, we would lean toward this being a non-starter. This may cause short-term negative sentiment around the business but this just represents an opportunity to buy more stock. Should any news suggest there is credence to this case, however, investors should be quick to sell.

- Product differentiation - Olaplex currently only has a handful of products. They are seeking to develop and produce more, however, consumers are only coming for a few of them. This creates concentration and reliance on a few products, risking obsolescence if a competitor releases a better product.

- Earnings - As we have established, the business is facing headwinds and will likely report shaky earnings in the coming quarters, including for FY22. This has the opportunity to compound negative sentiment around the business. For us, as long as we do not see a fundamental change in what we have explained in this paper, it only serves as an opportunity. A poor FY23 is already priced in.

Final thoughts:

Olaplex is a revolutionary product that has rightly gained industry notoriety and the growth that comes with it. It has been far from smooth sailing but the business has done what it can to respond. The recent lawsuit will once again bring negative sentiment around the business, alongside the temporary headwinds that come with an economic slowdown. However, our view is that the slowdown is priced in and then some, even if markets choose to respond negatively to the upcoming earnings. As for the lawsuit, customers have been using the product for years and are happy.

The real differentiator is their incredible margins, which we believe the business can maintain. Investment in expansion is required, but Olaplex still finds itself with superior margins. Long-term, beauty will perform well and investors should receive outsized returns. Based on our valuation, we see a 77% upside.

Returning to the question we began with, is the risk worth the reward? For anywhere close to 77%, it certainly is in our view.

For further details see:

Olaplex: Undervalued Beauty Gem With Big Potential Upside