XPO - Old Dominion Freight Line: Profiting From Yellow Corp's Bankruptcy

2023-11-13 09:54:18 ET

Summary

- Old Dominion is reinvesting its high ROIC into expanding, and growth rates are significantly higher than its competitors, allowing it to gain market share.

- The bankruptcy of one of its main competitors has left a void in the market and will benefit Old Dominion over the next years.

- The Congdon family who founded the company still holds about 18% of the shares and leading the business.

- Shares are slightly overvalued, and I am waiting for a drop in price to start a long position.

Investment Thesis

Old Dominion Freight Line ( ODFL ) is one of the market leaders in the less-than-truckload ((LTL)) industry, which has been enjoying tailwinds such as market concentration with increasing pricing power and a growing moat due to its network effects.

The company has been increasing its revenues above the market growth rate, it has a solid balance sheet with increasing returns on capital and an outstanding capital allocation by a highly experienced management team.

The recent bankruptcy of one of its major competitors will provide extra returns for ODFL and accelerate its market share gains over the next years.

Company Overview

ODFL was founded with a single truck in 1934 by the Congdon family, who still run the business, and thanks to its increasing network of service centers and the continuous reinvestment into the company while providing a superior service at a fair price, it has become the second-largest North American LTL motor carrier.

The company operates as a union-free organization and in addition to its core LTL services that generate over 98% of revenues , it also provides container drayage, truckload brokerage, and supply chain consulting services.

ODFL currently operates 256 service centers (~90% owned) and has primarily increased its size through organic growth.

{kind=link}

Source: ODFL August 2023 Presentation. Data from Transport Topics, American Trucking Associations, and ODFL estimates. North America LTL only.

Financials

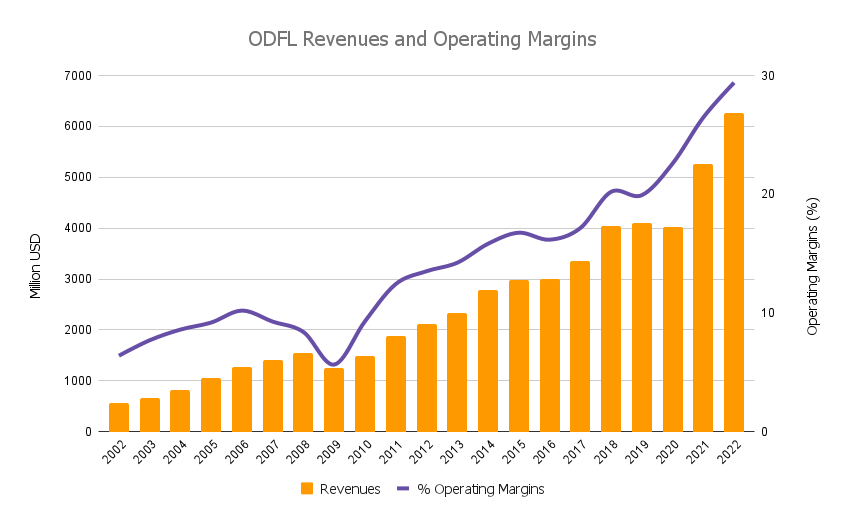

As shown in the chart above, the LTL average revenue growth has been at 5.1% CAGR, but ODFL has been more than doubling this growth rate and delivered a 12.8% CAGR over the same period.

{kind=link}

Source: Author (Data from ODFL Annual Reports)

What is even more impressive than the revenue growth rate is the increase in operating margins from less than 10% to the current 29.3% ( 3Q 2023 ) as the company expands its network and improves efficiency.

Since LTL motor carriers require an expansive network of local pickup and delivery service centers, as well as a large fleet of tractors and trailers, as the company becomes bigger, it makes it more difficult for smaller operators to effectively compete in the industry.

ODFL maintenance capital expenditures are at 5.5% for the first three quarters of 2023, slightly lower when compared to some of its peers such as Saia Inc. (NASDAQ: SAIA ) which stands at 6.24% or J.B. Hunt Transport Services, Inc. (NASDAQ: JBHT ) at 6.68%, which I consider as a sign of higher efficiency.

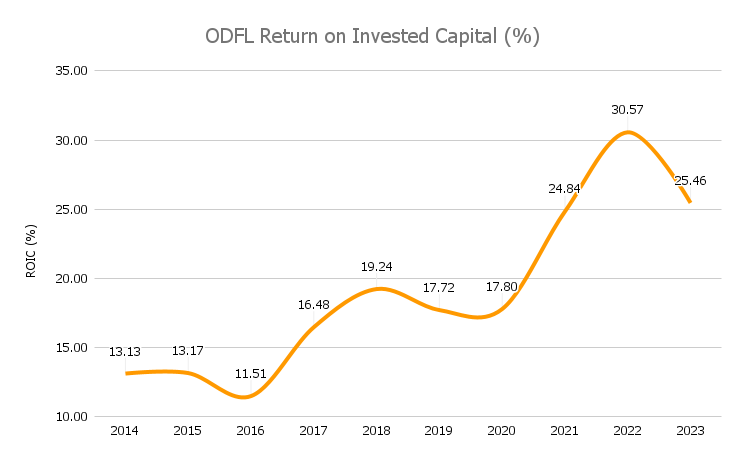

ODFL has more than doubled its service centers since 2002 (115 service centers and only 39% owned). By increasing the service center density, the amount of freight handled at a given service center location also increases and improves utilization of assets and other fixed costs, which have resulted in higher returns on invested capital.

{kind=link}

Source: Author (Data from ODFL Annual Reports)

Note: Data for 2023 is calculated based on last twelve months profits (from 4Q 2022 to 3Q 2023 included).

Balance

ODFL has an outstanding balance sheet which is straight forward and easy to understand. The company owns ~$4B in property and plant, of which approximately half of it are tractors, linehaul trailers and tires, while the other half are land and service center structure.

Source: (Data from Q3 2023 10-Q)

Receivables represent about 12.5% of assets (invoices are collected on average after 33 days), and other assets mainly compromises ODFL's technology , since the company heavily invests in state-of-the-art technology and innovative tools to improve efficiency and customer experience.

On the liabilities side, ODFL operates with negative net debt and only has $60M outstanding under its Senior B Notes at a 3.10% interest rate.

Other Non-Current Liabilities are obligations for the leased service centers and claims related to cargo loss and damage.

Capital allocation

{kind=link}

Source: Author (Data from ODFL Annual Reports)

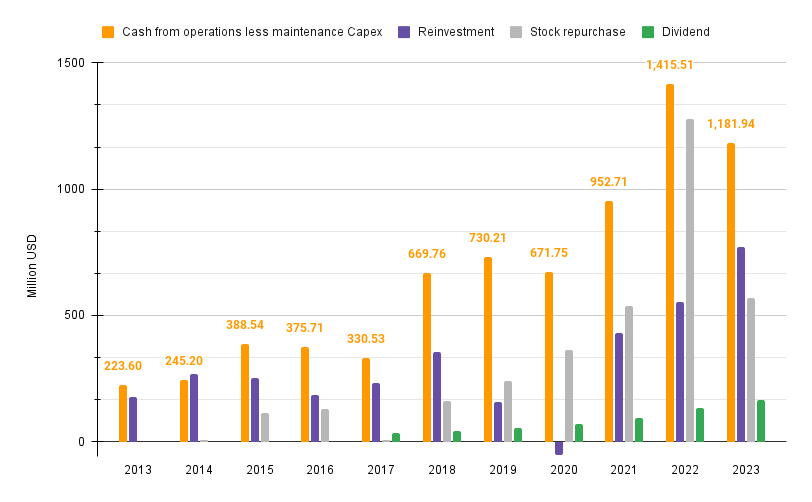

To evaluate ODFL capital allocation, I use cash from operations less maintenance capex. The company has been reinvesting into expanding the business on average 53% of its free cash from operations over the last decade, which I consider a high reinvestment rate.

As shown in the chart above, the company was conservative during 2020 due to the pandemic uncertainties, but reinvestment rates have increased since then and during the last twelve months they have been reinvesting above average, which I consider to be highly positive given the increasing returns on capital.

Since 2017, ODFL started paying cash dividends, which currently are at $0.4 per quarter (0.4% annual yield), on top of share buybacks, which is the main way of returning excess cash to shareholders. During 2022, the company took advantage of the decrease in share price and boosted its buybacks reducing the share count by almost 3%, but share buybacks have normalized lately.

Management

One of the most positive aspects of ODFL is the high skin in the game by management and the Congdon family since it avoids short-term thinking and gives me confidence that management is going to make the right decision over the long term.

In aggregate, the Congdon family still owns about 18% of the company , which is impressive for an over $40B company. The Executive Chairman of the Board is David S. Congdon, the grandson of the founders of the company, and currently owns 5.6% of the shares (valued at ~$2.6B) while receiving $5.5MM as cash salary, 90% of it based on performance. He started working at ODFL in 1978 and was the CEO since 2008 until 2018.

His father, Earl E. Congdon , who is currently 91 years old, holds the titles of Chairman Emeritus and Senior Advisor to the Company, with a stock ownership of 2.4% of total shares outstanding. He was the CEO from 1985 through 2007.

The current CEO of the company since June 2023 is Kevin M. Freeman, who owns approximately $11MM in shares and succeeded Greg C. Gantt (CEO from 2018 until 2023). Mr. Freeman joined the company in 1992 and before being promoted to CEO was the Vice President and COO, so he has extensive experience, knows well the business, and has been working closely with the previous CEO, so I have great confidence in his ability to continue ODFL's growth success.

Regarding compensation structure, despite I usually prefer more equity compensation, I think ODFL's design is perfect to align management's interest with shareholders. Base salary is just 8% of total compensation, and performance-based stock compensation is 18% of total compensation, based on gross margins and income growth, vesting over three years.

The other 74% of management's compensation is performance-based cash incentive paid monthly based on pre-tax income.

One aspect that surprised me positively, is that the stock ownership policy doesn't require the management to own so many stocks, and despite that, the skin in the game is huge given the size of the company, which tells us they are confident about future performance.

{kind=link}

Source: ODFL Proxy Statement 2023

Also, the company doesn't spend large amounts of money on presentations, so I don't feel like they are trying to sell me something as many publicly traded companies do. They make simple, even shabby, but revealing presentations.

The Trucking Industry

The LTL industry is mainly driven by the overall health of the economy, industrial production, and the demand for outsourcing logistics services, given that building a logistics structure is capital-intensive and not efficient for most companies.

Some studies suggest growth rates will accelerate over the following years to 7% CAGR due to the continued increase in e-commerce and the flexibility LTL shipping provides, while others expect growth rates to be on average similar to the last decade at 5% CAGR .

Some of the aspects that explain ODFL's outstanding performance over the last decades are the increasing concentration and higher efficiency of operations.

Market concentration

On the concentration side, currently, 80% of the LTL capacity is controlled by the top 25 LTL carriers, allowing for higher pricing power and the reduction of cyclicity during weak economic periods.

This has been a multidecade process after the Motor Carrier Act of 1980 which lifted restrictions on routes, commodities, and tariffs. The capitalist forces have done their job eliminating the weakest players and increasing the market share for the most efficient companies such as ODFL.

This brings us to the next point, the efficiency and the difference between unionized against non-unionized companies.

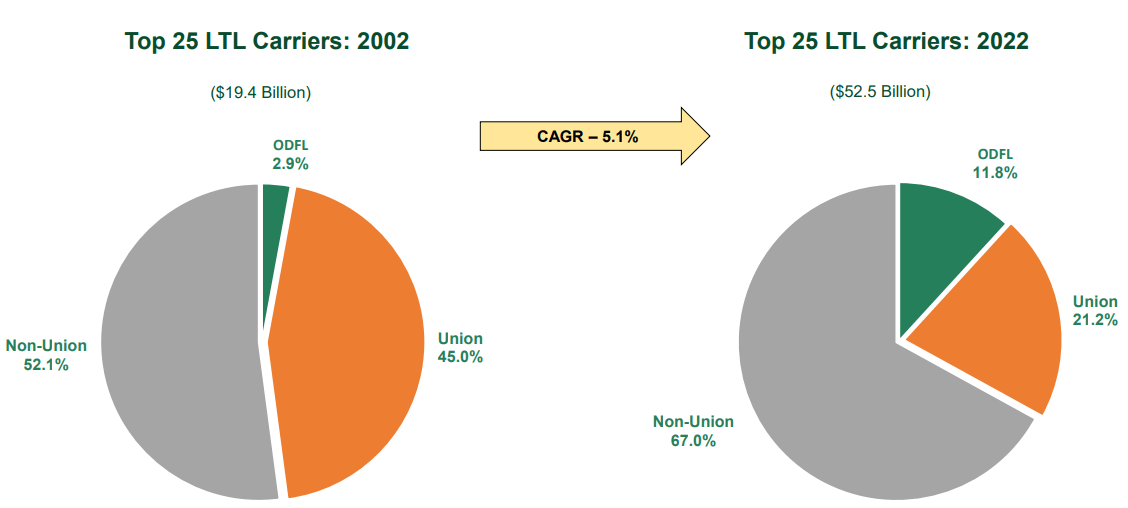

Efficiency and competitors

In 1996, of the top 10 LTL carriers 70% of the revenue resided with unionized companies, whereas in 2004 , the unionized carriers controlled only 43% of the revenue and this has reduced even further in recent years.

I believe unions make less sense nowadays compared to some decades before since they were designed to protect driver's rights, but their job has changed significantly since then. Truck drivers are benefiting from more efficient organizations and technology developments such as routing system s, electronic logging devices ((ELD)), and art ificial intelligence, which reduce driving times and improve their overall experience.

If we take a look at the evolution over the last decade for the shipments per day, we can see that the decrease has been significantly higher at unionized organizations such as Yellow, which I will review in the next section, and TForce Freight. XPO (NYSE: XPO ) is partially unionized, which also had a decrease in shipments per day.

ArcBest Corp. (NASDAQ: ARCB ) is the only unionized company that had an increase during the period, but smaller when compared to non-union companies such as FedEx (NYSE: FDX ), Saia, or ODFL.

{kind=link}

Source: ODFL August 2023 Presentation

When analyzing the industry from a return on capital perspective, growth, and ability to deploy capital into expanding, overall I would state it is enjoying tailwinds, but ODFL stands out from its competitors with higher income per employee, margins, and return on capital, followed by Saia, which suggests it will continue increasing its market share.

{kind=link}

Source: Seeking Alpha

The Yellow Corp. Situation

After almost 100 years in the business, Yellow Corp. (YELLQ) announced its bankruptcy in August this year, leaving 30,000 people out of work following many years of decline and the Teamsters' negative to allow further operational changes .

The company was of a similar size as ODFL and held an approximately 10% market share in the LTL industry, so this bankruptcy could have significant effects and could benefit the rest of the companies that remain in business.

For ODFL I believe this is great news from many points of view. The first and most obvious point is the gain in volumes and market share since Yellow Corp.'s volumes will be absorbed by its competitors.

The second aspect I would highlight would be the release on wages pressure since many drivers became available for work and this will help ODFL to find new employees when needed and reduce the pressure to increase salaries to retain employees.

Finally, about 290 service centers will become available for sale following the bankruptcy process, probably at some discount, which will provide extra returns on capital for its competitors.

We want to be measured with our approach and continue to believe that slow and steady wins the race. So we didn't try to go out and immediately win as much share as was out there in the market, but we're trying to do it in the right way.

(Source: Q3 2023 Earnings Call . Adam Satterfield, Executive Vice President of Finance and Chief Financial Officer)

Expected Growth

For the full year 2023, revenues are expected to decrease slightly to $5.88B (-6% YoY) due to a decrease in volumes, since the price per hundredweight has increased 3.1% in the 3Q 2023 on a YoY basis. Net income margins should normalize given the rapid increase during the last two years and EPS is expected to be $11.2 per share for the full year. For the last quarter of the year, margins will slightly decrease, but this is no reason to worry because ODFL increases wages in September.

For the following years, management is expecting an increase in volumes and continuing to improve margins.

We believe in a long-term consistent approach to pricing. And we try to target obtaining 100 basis points to 150 basis points of price above cost each year. We've had some cost pressure this year, and that's evident in our numbers. But I believe that that starts improving as we go into next year, especially if we can get a little bit of volume recovery.

(Source: Q3 2023 Earnings Call. Adam Satterfield, Executive Vice President of Finance and Chief Financial Officer)

After 2024, I am assuming a conservative revenue growth rate of 8%, above the industry growth rate, but under the 11.5% average ODFL's growth rate during the last decade. Regarding margins, I will use the management's low guidance of 100 basis points on operating margin improvement per year.

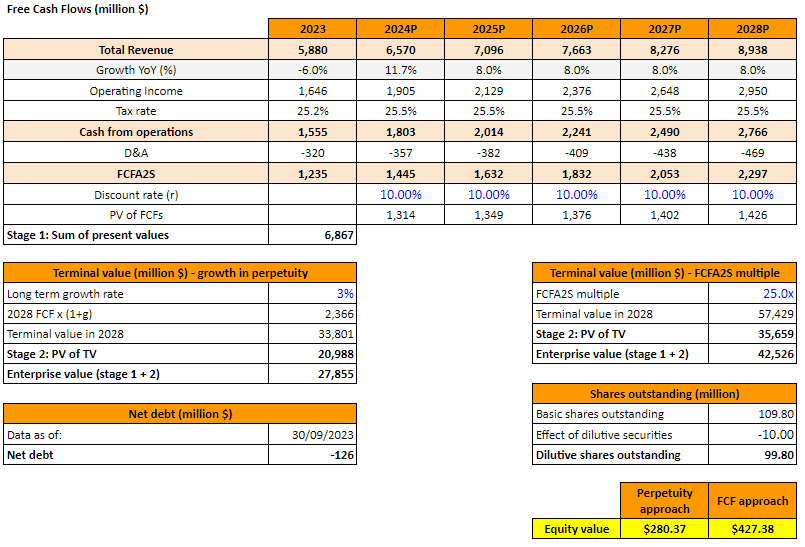

Even though I prefer to value companies using free cash flow, I believe it wouldn't be the most accurate way of doing so in ODFL's case given the high reinvestment rate, accounted as capital expenditures. I am going to use free cash flow available to shareholders, calculated as operating cash flow less maintenance capex.

{kind=link}

Source: Author

Using a 10% discount rate and assuming the company continues decreasing the share count by 2% annually, the average fair price is at $353 per share, suggesting the stock is currently slightly overvalued.

Despite rating ODFL as a hold, I expect the company to outperform the market, providing investors with double-digit returns in the 12.5% to 15% range, due to its high returns on capital and reinvestment rates.

Valuation

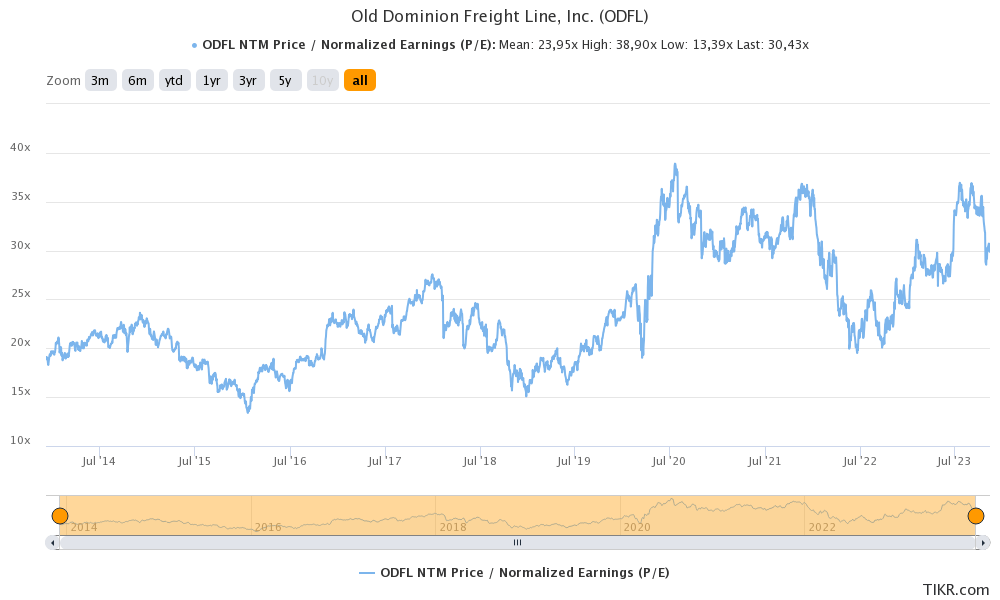

From a valuation multiple perspective, ODFL is currently trading at a higher valuation multiple when compared to Saia or XPO, which I believe is reasonable given the superior quality of the business.

{kind=link}

Source: TIKR.com

As shown in the chart above, ODFL is trading at its high valuation range, considerably above its average multiples, suggesting we could wait for a decrease in price to start a position in the company.

I consider ODFL the market leader of the LTL industry and expect it to continue gaining market share and deliver superior returns than the average company over the upcoming years, and I am placing my buy order at a 25x NTM EPS, or $340 per share.

Risks

The main risks I see for ODFL are:

- If employees were to unionize : This is the major risk, given that ODFL employees are not unionized. Wages would increase, affecting margins and efficiency. Given the recent developments with Yellow Corp., it doesn't seem likely in the short term. Also, reviews from employees are positive and above the competition:

Source: Glassdoor

- Tech developments: If ODFL is not able to keep up with tech improvements it would have serious implications for its growth strategy performance and could lose market share. I don't assign it a high probability given the focus and investments on new developments.

- Prolonged economic slowdown: ODFL has a strong balance sheet and I believe it can even profit from recessions and continue gaining market share on expenses of its competitors as we have recently seen, but if prices were to remain high for a long period, the company would see its profitability damaged and valuation multiples would decrease, reducing mid-term returns for shareholders.

Conclusion

The LTL industry is consolidating and Old Dominion Freight Line is in a perfect position to gain even more market share over the next years since it provides a superior service at a fair price and is run by an experienced management with high skin in the game.

Its balance sheet is strong, it is increasing its efficiency and returns on capital, while it still has room to deploy its cash from operations into expanding the business, which will provide its shareholders with superior returns, overperforming the market.

Finally, ODFL is trading at higher multiples than its competitors, and I am willing to pay the premium. Still, I believe it is slightly overvalued and will wait for a correction to start a position at around $340-$360 per share, which I believe is the fair price.

For further details see:

Old Dominion Freight Line: Profiting From Yellow Corp's Bankruptcy