ODFL - Old Dominion Freight Line Stock Is Extremely Overvalued

2023-07-06 15:05:12 ET

Summary

- Old Dominion Freight Line, Inc.'s earnings have probably peaked this cycle, but the stock price is ignoring it.

- Even using generous assumptions, Old Dominion stock is overvalued based on long-term earnings expectations.

- This has been a great growth stock to own the past several years, but many of the catalysts for that growth were temporary.

Introduction

The amount an investor pays for a stock has a direct correlation to the future returns of the investment for that investor. The more one pays, the fewer shares they can buy with the same amount of money. Paying too much for future earnings can produce very poor returns even if the businesses themselves are very high quality.

I have tracked Old Dominion Freight Line, Inc. ( ODFL ) for several years in my Investing Group, The Cyclical Investor's Club, but I haven't previously written publicly about it. Right now, the stock appears overvalued enough to write a warning article about it, though, so that is what I'll do in today's article.

Old Dominion's Historical Earnings Cyclicality

The valuation method I use for Old Dominion first checks to see how cyclical earnings have been historically. Once it is determined that earnings aren't too cyclical, then I use a combination of earnings, earnings growth, and P/E mean reversion to estimate future returns based on previous earnings growth and sentiment patterns. I take those expectations and apply them 10 years into the future, and then convert the results into an expected CAGR percentage. If the expected return is really good, I will buy the stock, and if it's really low, I will often sell the stock. In this article, I will take readers through each step of this process.

Importantly, once it is established that a business has a long history of relatively stable and predictable earnings growth, it doesn't really matter to me what the business does. If it consistently makes more money over the course of each economic cycle, that's what I care about - numbers over stories.

{kind=link}

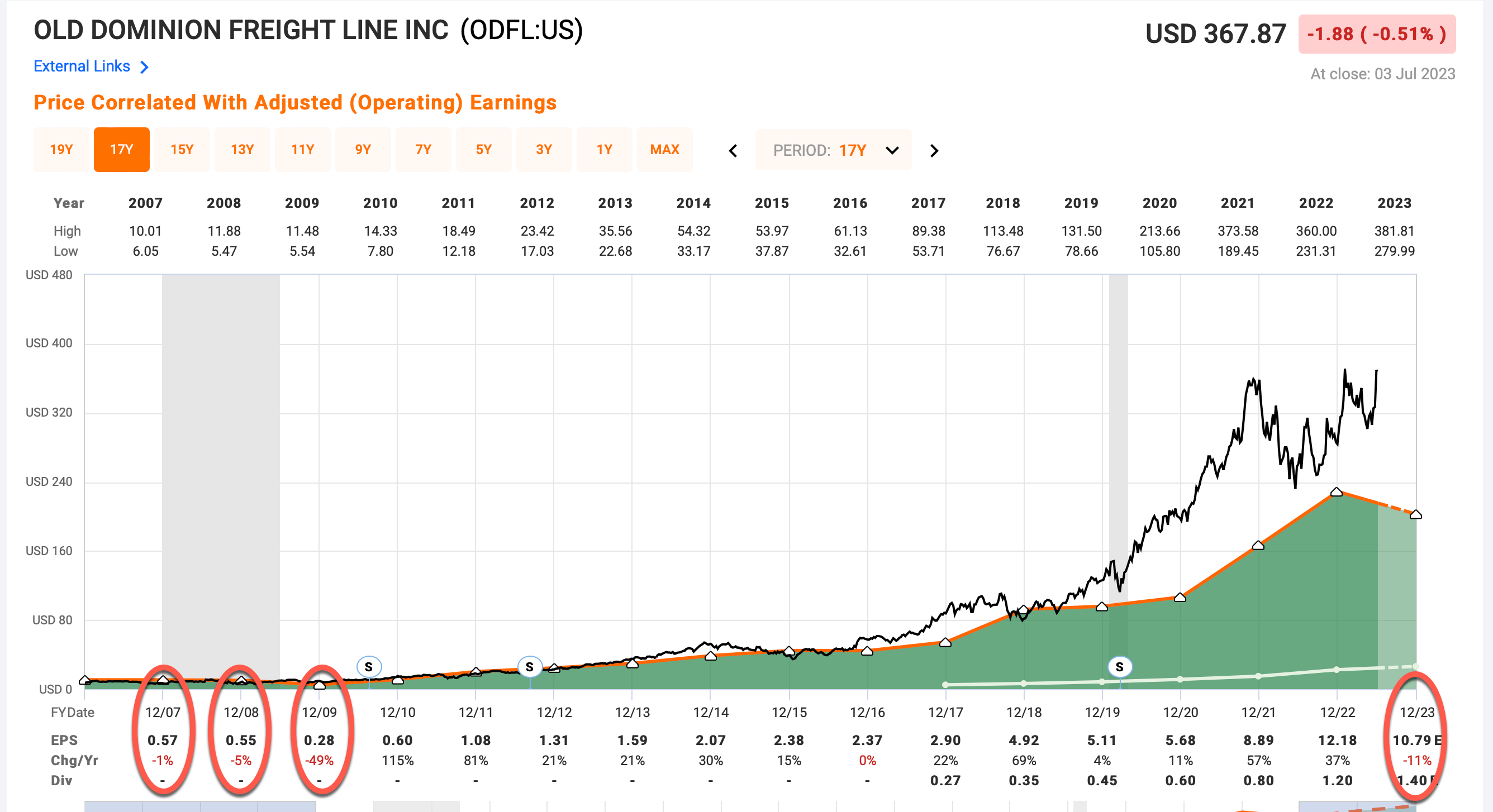

Since 2003, Old Dominion has only had 3 years of negative EPS growth, and this year is expected to be negative as well. All of the previous negative growth years occurred during the 2007-2009 recession. The main reason I check historical earnings patterns is to help determine the cyclicality of the business's earnings, which are represented by the dark green shaded area in the FAST Graph above. If earnings have a history of falling more than -50% off their peaks, then usually I categorize the business as deeply cyclical and I do not use earnings for my valuation estimates due to their volatility.

ODFL is right at that -50% threshold, but since the Great Recession was a particularly bad recession and ODFL has had pretty stable earnings since that time, I feel comfortable using earnings to value the stock as long as we take into account the sort of recession decline that might happen. Already this year we see what could be the beginning of an earnings growth decline. Interestingly, back in 2007 ODFL's initial earnings weakness was a good leading indicator of the future economic recession. ODFL had no false positives since that 2007-2009 recession. Now we see the initial signs of a decline in 2023. This should at least send up a caution flag for investors.

All that said, I'm going to treat ODFL as a moderately cyclical business for this analysis and use an earnings and earnings growth-based approach, and then include a recession factor after the basic analysis is complete.

Market Sentiment Return Expectations

In order to estimate what sort of returns we might expect over the next 10 years, let's begin by examining what return we could expect 10 years from now if the P/E multiple were to revert to its mean from the previous economic cycle. For this, I'm using a period that runs from 2015-2023.

{kind=link}

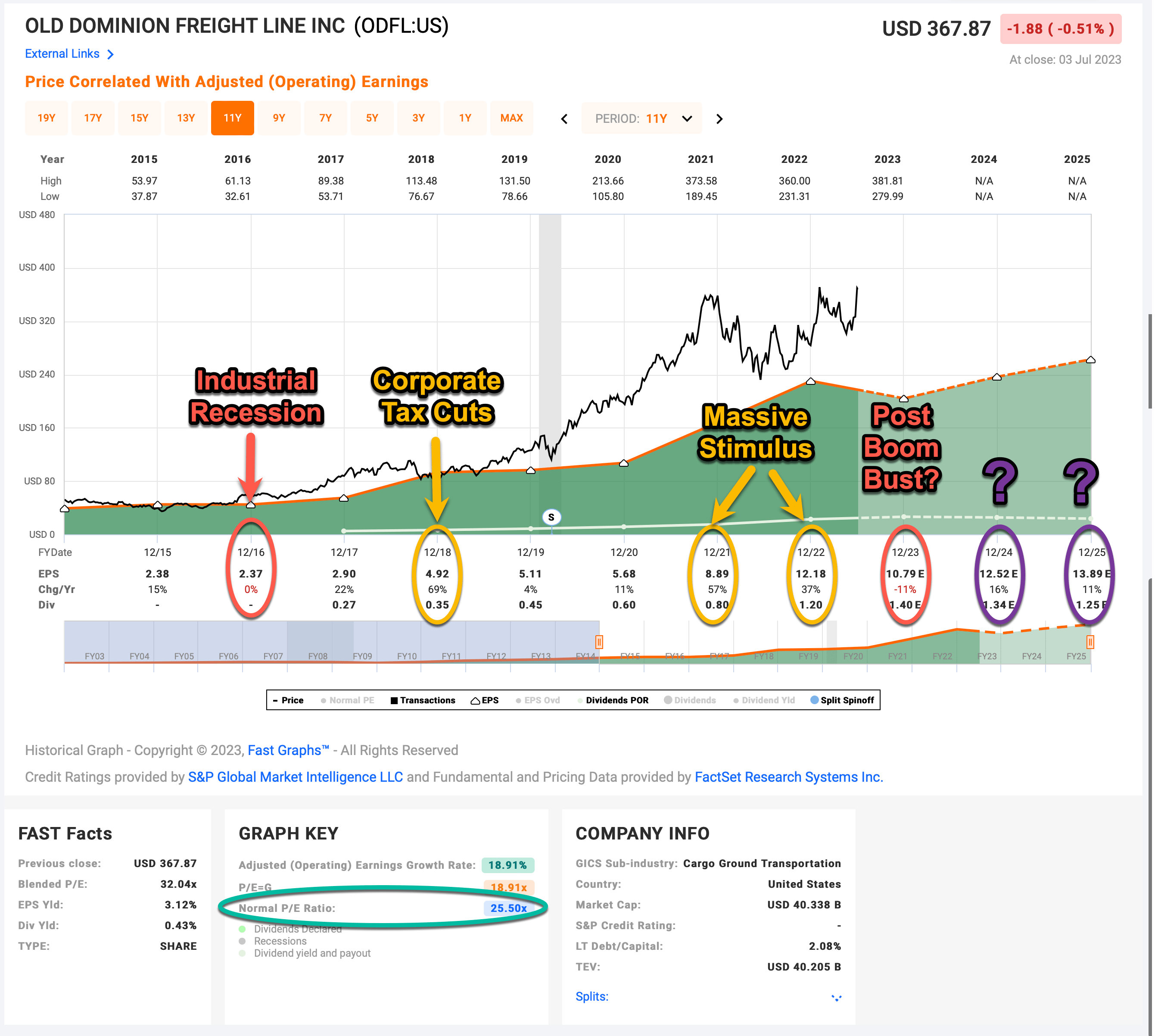

ODFL is an interesting stock to look at because its earnings represent what I think is a good look through on the goods economy of the U.S., and, ODFL's various earnings patterns are pretty easy to interpret. In 2016 they had a flat growth year as the industrial part of the economy, including a big down cycle in energy, was in recession. In 2018 they had a big earnings spike after corporate tax cuts, which should be considered a one-time boost to growth. Then, after massive government stimulus in 2020 and 2021, the following two years had similarly huge EPS growth. Again, this was the result of temporary government stimulus. After student loan repayments begin three months from now, that stimulus will be over.

I point out the macro reasons for these huge earnings growth years so readers know that, even though this will be a bearish article, I'm being very generous with my earnings growth assumptions because I will assume the period we recently experienced since 2015 will be similar to the next 10 years. The odds are, actually, earnings will not grow as fast as they have in recent years because we can't count on more tax cuts and stimulus.

Also worth noting is that right now analysts expect earnings growth to resume in 2024 and 2025. I would take those predictions with a grain of salt, though. While anything is possible, the odds are ODFL doesn't meet these expectations, especially if there is a recession.

ODFL's average P/E from 2015 to the present has been about 25.50 (the blue number circled in green near the bottom of the FAST Graph). Using 2023's forward earnings estimates of $10.79 it has a current P/E of 33.85. If that 33.85 P/E were to revert to the average P/E of 25.50 over the course of the next 10 years and everything else was held the same, Old Dominion's price would fall and it would produce a 10-Year CAGR of -2.79% . If the P/E reverts sooner than 10 years, the returns would be significantly worse.

Business Earnings Expectations

We previously examined what would happen if market sentiment reverted to the mean. This is entirely determined by the mood of the market and is quite often disconnected, or only loosely connected, to the performance of the actual business. In this section, we will examine the actual earnings of the business. The goal here is simple: We want to know how much money we would earn (expressed in the form of a CAGR %) over the course of 10 years if we bought the business at today's prices and kept all of the earnings for ourselves.

There are two main components of this: the first is the earnings yield and the second is the rate at which the earnings can be expected to grow. Let's start with the earnings yield (which is an inverted P/E ratio, so the Earnings/Price ratio). The current earnings yield using 2023's earnings expectations is about +2.95%. The way I like to think about this is, if I bought the company's whole business right now for $100, I would earn $2.95 per year on my investment if earnings remained the same for the next 10 years.

The next step is to estimate the company's earnings growth during this time period. I do that by figuring out at what rate earnings grew during the last cycle and applying that rate to the next 10 years. This involves calculating the historical EPS growth rate, taking into account each year's EPS growth or decline, and then backing out any share buybacks that occurred over that time period (because reducing shares will increase the EPS due to fewer shares).

During this time period, Old Dominion bought back about 15% of the company. I will make adjustments for these buybacks along with the -11% EPS decline expected this year. I will not make adjustments for the 3 years of temporary or one-time stimulus in 2018, 2021, and 2022, so in that respect, I'm being very generous with the earnings growth rate. I will also not include a recession expectation. Instead, I will adjust for a potential recession later in the analysis. When I do all that, I get an overall earnings growth rate estimate from 2015-2023 of +18.62%. This is an extremely fast earnings growth rate, which I'm sure has contributed to the popularity and high valuation of the stock in recent years.

Next, I'll apply that growth rate to current earnings, looking forward 10 years in order to get a final 10-year CAGR estimate. The way I think about this is, if I bought ODFL's whole business for $100, it would pay me back $2.95 plus +18.62% growth the first year, and that amount would grow at +18.62% per year for 10 years after that. I want to know how much money I would have in total at the end of 10 years on my $100 investment, which I calculate to be about $185.15 including the original $100. When I plug that growth into a CAGR calculator, that translates to a +6.35% 10-year CAGR estimate for the expected business earnings returns.

10-Year, Full-Cycle CAGR Estimate

Potential future returns can come from two main places: market sentiment returns or business earnings returns. If we assume that market sentiment reverts to the mean from the last cycle over the next 10 years for Old Dominion, it will produce a -2.79% CAGR. If the earnings yield and growth are similar to the last cycle, the company should produce somewhere around a +6.35% 10-year CAGR. If we put the two together, we get an expected 10-year, full-cycle CAGR of +3.56% at today's price.

My Buy/Sell/Hold range for this category of stocks is: above a 12% CAGR is a Buy, below a 4% expected CAGR is a Sell, and in between 4% and 12% is a Hold. With a +3.56% 10-year CAGR expectation, that would make ODFL stock a "Sell" at today's prices, even using very generous earnings growth estimates.

Recession Considerations

Whenever I write a bearish article, I try to make as generous assumptions and estimates as I realistically can, and that is what I've done with ODFL stock so far. But there are additional risks here that need to be mentioned, both for current ODFL shareholders and for those investors who are watching the stock for a potential entry point as I am. Given the removal of ongoing U.S. stimulus and a decline in the U.S. goods economy (services remain strong), and with most forward-looking indicators pointing toward a recession, chances are, if ODFL stock significantly sells off, it will be because the economy is going into a recession.

The prices I aim to buy stocks during a recession are usually lower than what I would be willing to pay mid-cycle. I have found examining what stocks have done during previous recessions to be a good guide for what they are likely to do during future recessions. Because of this, I use what I call a "Recession P/E" to help guide this process. I used a process similar to this in March 2020 and was able to buy some very high-quality businesses at extremely good prices. Here is how it works.

I take the lowest stock price during the previous recession and create a P/E metric using the peak earnings. Then I add 20% to that number and that's the "Recession P/E" level I would be willing to buy the stock at using this cycle's peak earnings. So, if a business had peak earnings of $1 per share in 2008 and the stock price bottomed at $10 per share, it would have had a bottom-price/peak-earnings of 10. Increasing that by 20%, I would be willing to buy at a 12 P/E this time around based on peak earnings to the current price. (Of course, each investor can decide how conservative they want to be, so some might want to buy within 10% of the recession P/E while others might want to buy within 30% if they were more optimistic or more concerned about missing the opportunity.) In March 2020, I used 20%, and that's my basic multiplier, but I do adjust it based on additional circumstances. Some industries, like health insurance companies traded at low-single-digit P/Es in 2009 and I think that's unlikely to repeat, so I'm more generous with them. Certain businesses this time around that massively benefited from COVID or stimulus money I would be less generous, so there is room to make individual judgment calls and adjustments regarding the multiplier.

The Recession P/E is just a guide to help us from buying way too soon in a down cycle, or missing out on opportunities because the current earnings expectations get way too negative during the heart of a recession. It doesn't have much precision. But it is useful.

{kind=link}

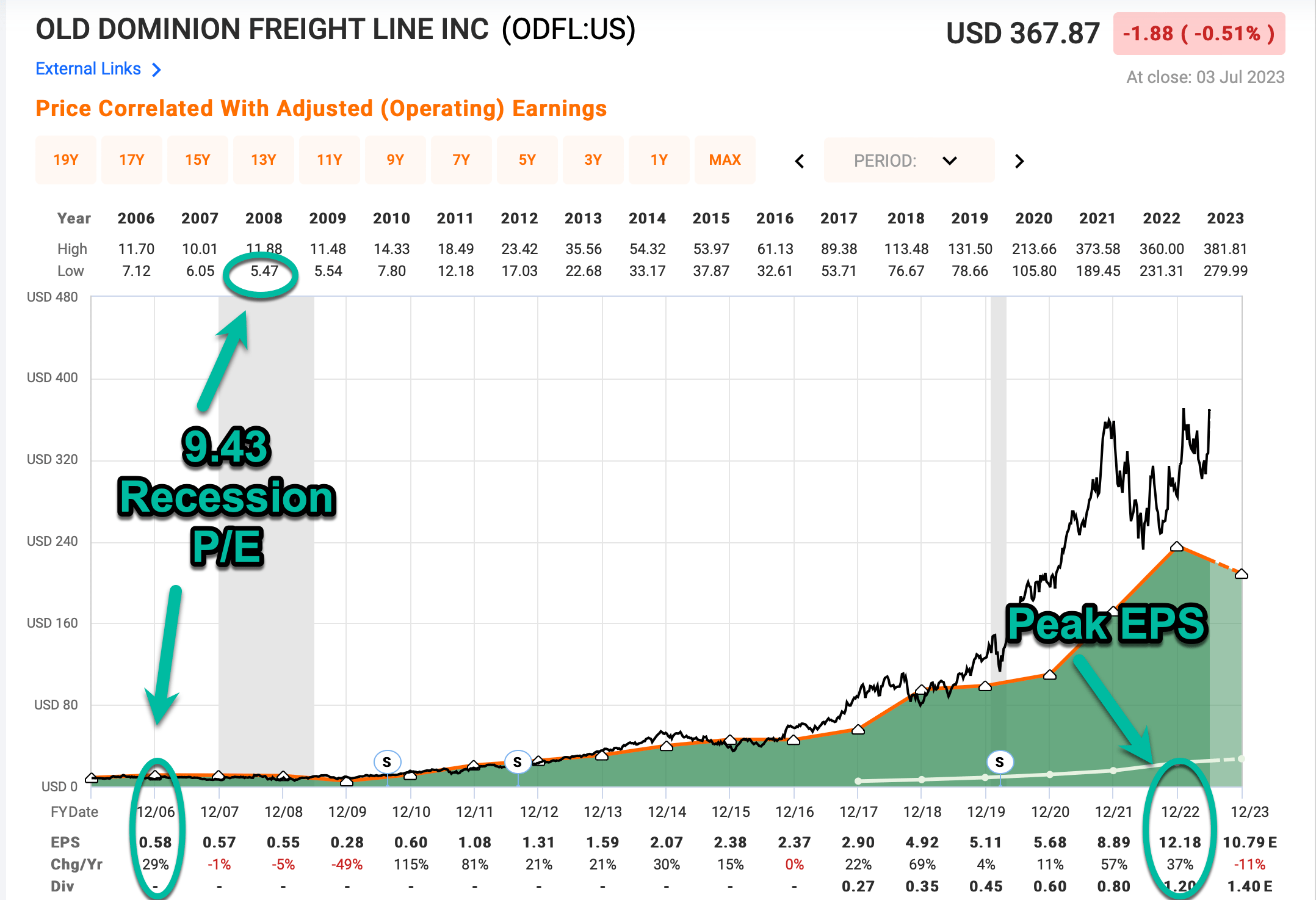

Okay, going back to the last "real" recession in 2009, we see ODFL had peak earnings in 2006 of $0.58 per share and the price ultimately bottomed at $5.47 in 2008. This results in a Recession P/E of 9.43. If we increase this by 20%, we get a Recession P/E buy price target of 11.32. Currently, during the more recent down cycle, EPS peaked at $12.18 per share. If we multiply that by 11.32 we get a recession buy price of $136.78 this time around unless ODFL posts earnings higher than $12.18 per share. This buy price is obviously much lower than the current price of $367.87, and I'm sure some readers will declare the price could never fall to $136 even during a recession.

I think it's worth pointing out that the stock price fell below $232 just last year and we didn't even have a recession. If earnings simply fell back down to pre-stimulus levels of $6.00 per share they would be halved from last year's earnings. And $6.00 or $7.00 of earnings should probably be investors' base expectation given how far earnings fell from 2007-2009 and how much more stimulus from the economy is currently being withdrawn compared to 2008. At $136 per share and $6.00 of earnings, ODFL would trade at a P/E of about 23. Many investors will think the stock is expensive at that price if earnings do fall that far. Importantly, I do think that $136 price is below fair value for the stock, but I try to buy stocks when they are below fair value because I aim for above-average returns.

Conclusion

While predicting the degree of any downturn for any particular stock is difficult to do with much precision, the odds are very high ODFL's earnings have likely peaked this cycle and will have some sort of earnings recession. The current high stock price does not reflect this, which makes the stock a "Sell" at its current price.

If we avoid recession, and ODFL's earnings grow at the same rate they have since 2015, ODFL would be a good buy under $300 per share. But, as I pointed out, much of ODFL's strong growth can be explained by temporary or one-time tax cuts and government stimulus, and the odds of a "goods recession" are very high over the next 12-18 months. For this reason, I wouldn't be a buyer personally until the Old Dominion Freight Line, Inc. stock price was closer to $136 per share.

For further details see:

Old Dominion Freight Line Stock Is Extremely Overvalued