ODFL - Old Dominion Is Set To Fly Higher

Summary

- In this article, we start by assessing the many reasons that make Old Dominion an outperforming trucking company that never seems to trade at an attractive price.

- The company benefits from a superior business model, allowing for high margins, strong pricing, and a very healthy balance sheet.

- Demand in the industry seems to be bottoming. While I believe that ODFL remains significantly undervalued, I'm looking for a buyable correction before I add the stock to my portfolio.

Introduction

Old Dominion Freight Lines ( ODFL ) has been on my watchlist for a very long time. More recently, I have watched the stock like a hawk since the start of market weakness in 2022, as I believe that the stock is a perfect fit for my dividend growth portfolio. The problem is that Old Dominion is one of the stocks that never seems attractively valued.

The company has the single most efficient business in less-than-truckload ("LTL") trucking and a dividend scorecard that screams outperformance.

What makes pulling the trigger on ODFL so hard is the fact that we're either going to end up in a nasty recession or somehow in a scenario where the Fed manages to keep the current stock market momentum going.

It gets even trickier as industry insiders are seeing a return of demand growth, despite leading economic indicators pointing towards more pain ahead.

In this article, we will talk about the reasons that make ODFL so powerful and new macroeconomic developments that could send ODFL shares flying.

So, bear with me!

ODFL Is "Never" Cheap

One of the reasons why I don't buy investments with a very high yield is because I believe that I can always sell my dividend growth stocks and move to high income when I have to.

Using Main Street Capital ( MAIN ) as an example, the stock has always yielded close to 6%. Yes, good timing can give you a better entry, but if you needed a high yield, you didn't have to wait for a rare opportunity. On a side note, this is just an example, not a recommendation to buy MAIN.

Buying high-quality dividend growth stocks is different. Old Dominion Freight Lines is a prime example of that. The stock has surged more than 4,800% since 2009. This outperforms the S&P 500 and many well-known growth stocks by a mile. During its upswing, the stock has been extremely cyclical, with unattractive valuations before each steep stock price drop. In 2015, the stock was trading at 12x EBITDA. A lot of investors believed it was too expensive for a trucking company in a highly competitive industry. The worst part (for people who didn't invest) is that the valuation increased along with the stock price. After the pandemic, the stock was trading at more than 20x EBITDA. Heck, even before the pandemic, the stock was trading at more than 15x EBITDA.

The same goes for the price/earnings ratio to give you another valuation metric. The longer-term median looks to be close to 28x earnings. That's fair, but it needs to come with consistently high growth rates. A lot of investors are not willing to take that risk and/or have entirely different strategies.

What makes ODFL so powerful is that there's a good reason for this valuation.

ODFL's Business Is Superior

I often write that I avoided trucking exposure in my dividend growth portfolio because trucking is highly competitive, very capital intensive, and often subject to razor-thin margins.

That's also the reason why I own three railroads in my portfolio. I like their ability to transport goods more efficiently, resulting in high free cash flow and all the benefits that come with that.

The good thing is that there's one major advantage when it comes to a highly fragmented industry. Companies that have figured out how to outperform can quickly gain market share. That's why I invested in self-storage real estate, and it's the reason why I want to add the ODFL ticker to my portfolio.

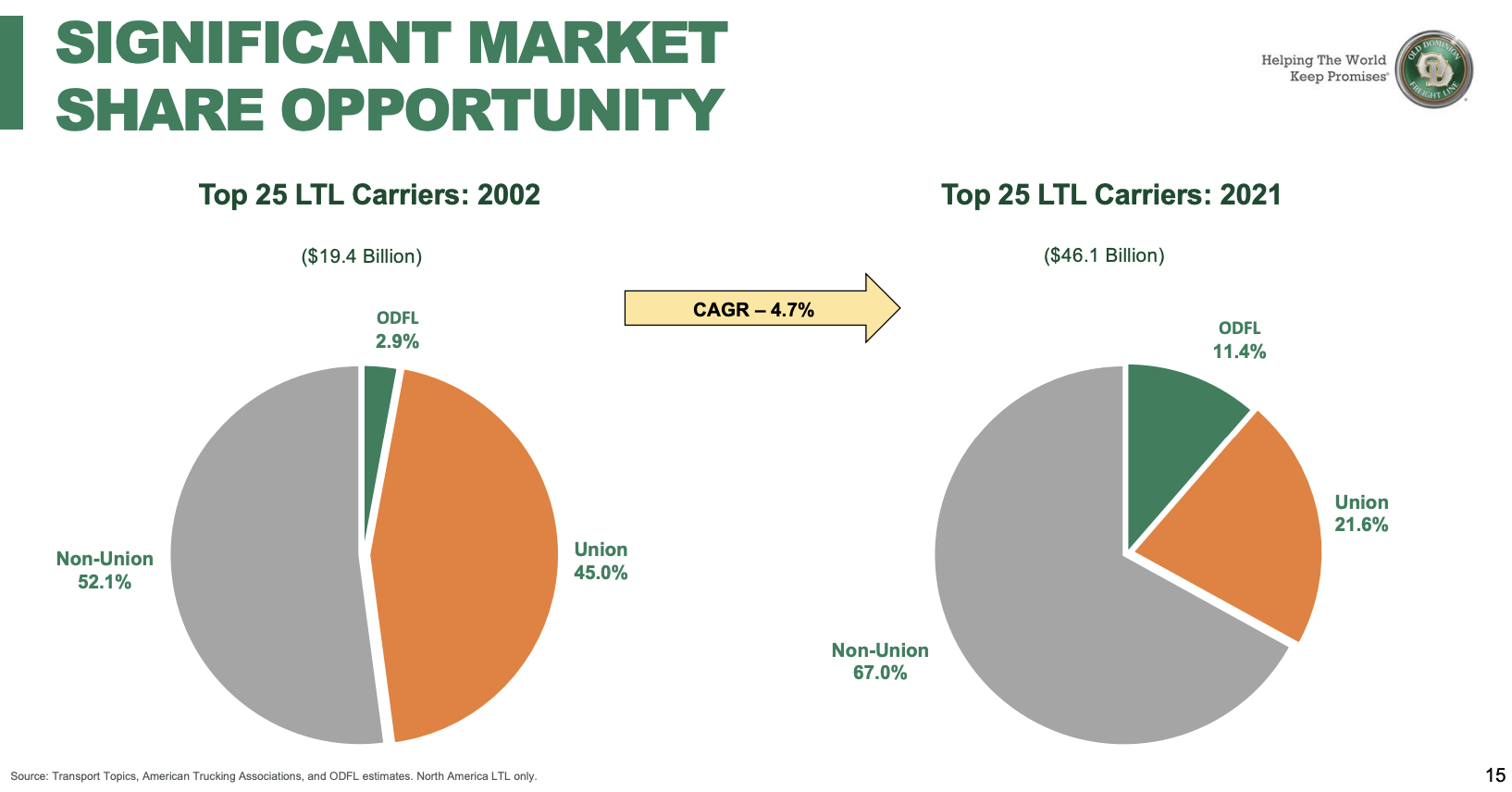

In 2002, the carrier had a 2.9% market share in a $19.4 billion market. Back then, that was already an impressive number. Now, that number has increased to 11.4% in a market worth close to $50 billion. In the Pacific Northwest, the company has a 14.9% market share. Unfortunately, that market is worth only $1.2 billion. In the Midwest, the nation's largest LTL market, the company has a 12.6% market share.

{kind=link}

Essentially, the company believes that its success is based on six pillars:

- A long history of significant revenue growth and profitability.

- Ongoing opportunity to win market share.

- Superior customer service delivered at a fair price.

- Capacity to grow supported by an unmatched investment in its network and equipment.

- Experienced and motivated employees.

- Commitment to delivering superior long-term shareholder returns.

Creating fancy lists is easy. However, Old Dominion has the numbers to back it up. The company indeed has a history of tremendous revenue growth, profitability, and high shareholder returns.

Since 2002, the company has compounded its revenue by 12.4% per year. This is done entirely organic, meaning the company has not acquired competitors to speed up the process of gaining market share. The company has spent nothing on cash acquisitions over the past ten years.

{kind=link}

Old Dominion has figured out how to gain market share, which means there is no good reason to spend billions on buying often less profitable peers.

According to the company :

Competition in our industry is based primarily on service, price, available capacity, and business relationships. We believe we are able to gain market share by expanding our capacity in the United States and providing high-quality service at a fair price.

Between 2011 and 2021, the company has grown the number of service centers by 16% to 251. The average service center growth rate in the industry was -5% during this period. This allowed the company to boost the number of shipments per day by 79%. The industry average was a decline of 3%.

{kind=link}

Thanks to consistent investment in services, the company was able to boost customer satisfaction and gain pricing power.

To give you a few examples:

- 70% of ODFL shipments are next or second day.

- On-time service has improved from 94% in 2002 to 99% in 2022.

- The cargo claims ratio has dropped from 1.5% in 2002 to 0.2% in 2022.

- The company has won the Mastio Quality Award 13 years in a row.

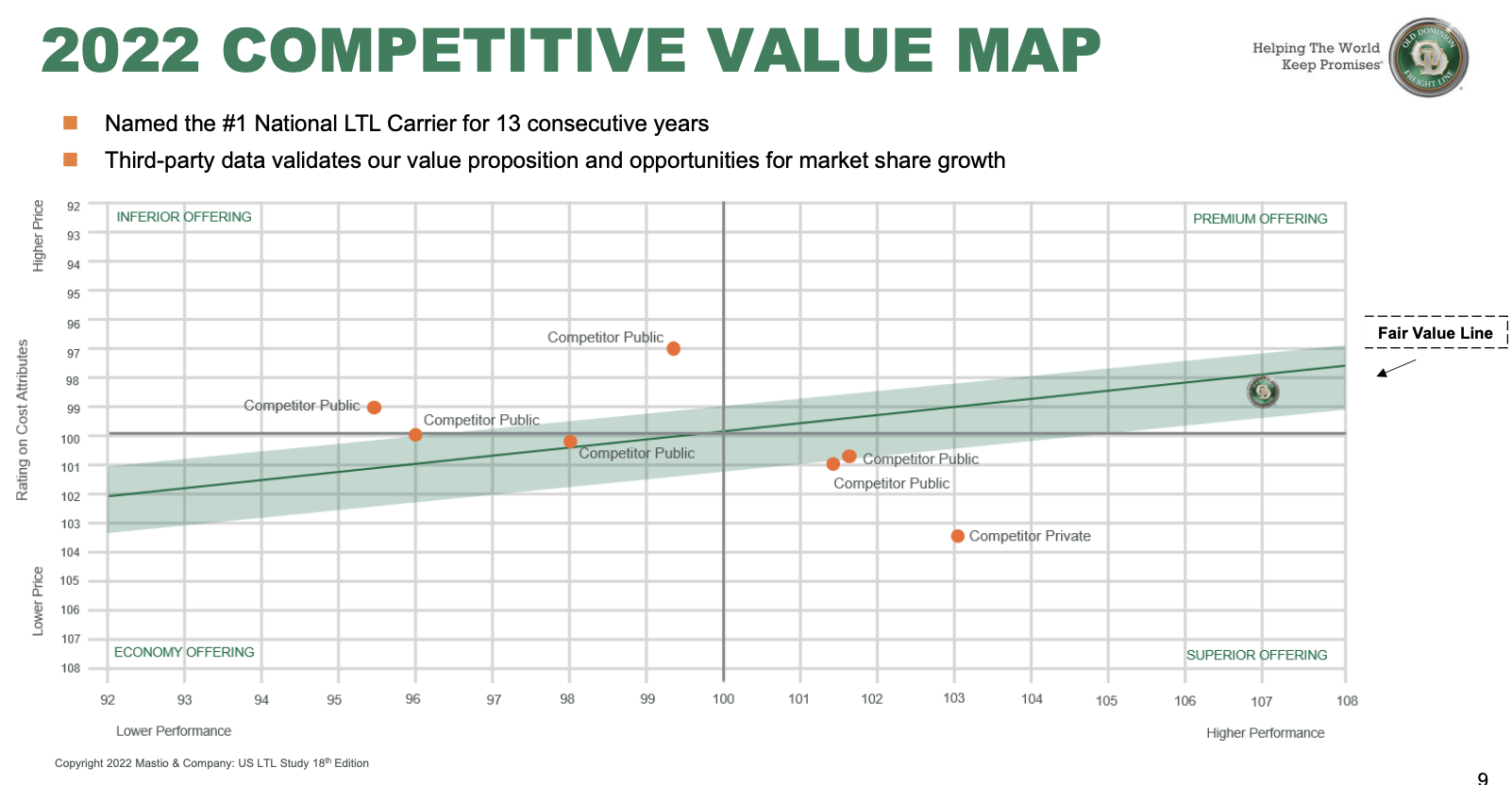

Concerning pricing power, the company sees itself in a position where it can charge above-average prices thanks to superior service. Relying on the data below, we see that the company is offering similar prices compared to companies with worse performance.

{kind=link}

Not only that, but even more important to mention is that ODFL is incredibly profitable.

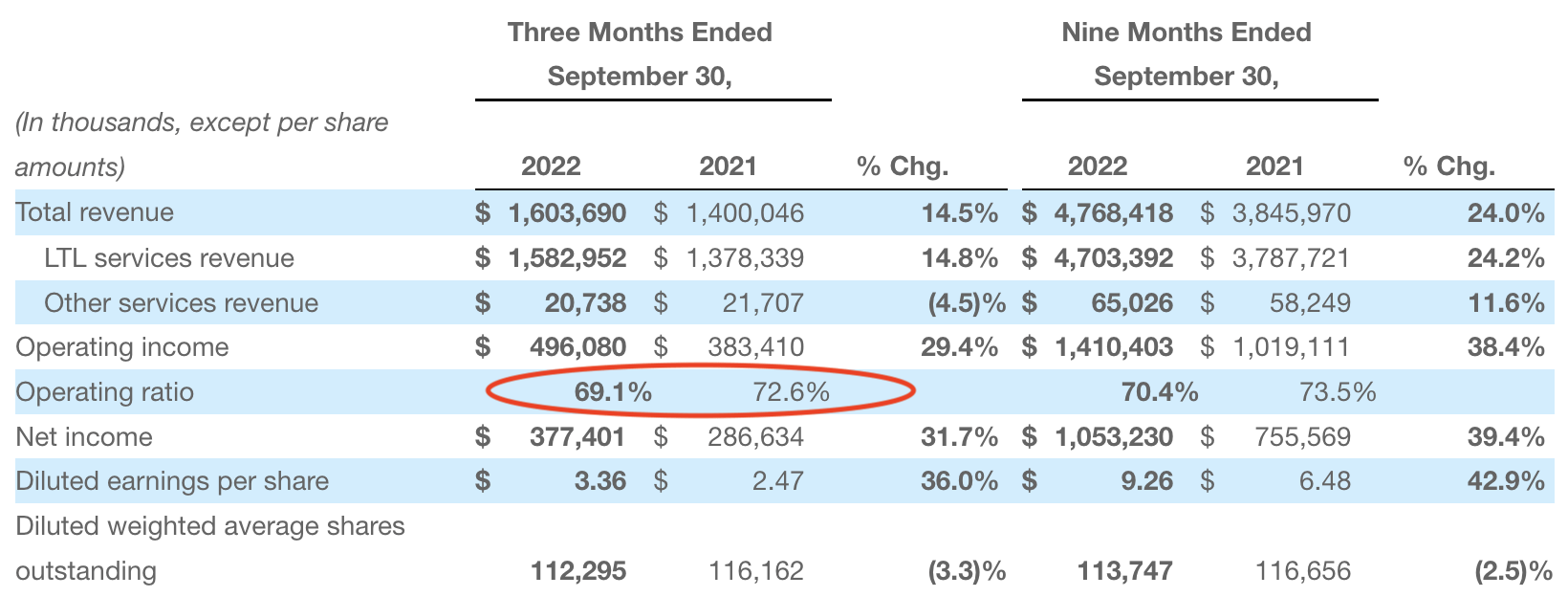

In the third quarter, the company lowered its operating ratio to 69.1%. This means that 69.1% of revenues went toward operating expenses. That seems like a lot, yet it is extremely profitable. A lot of trucking companies have operating ratios of more than 90%. Many are struggling to remain profitable.

Also, as railroads were hit by operating inefficiencies, a lot of Class I railroads reported operating ratios of roughly 60%. The fact that ODFL was less than 10 points away from railroads is truly amazing.

{kind=link}

According to the company :

Our third quarter operating ratio improved to 69.1% with improvements in both our direct operating cost and overhead cost as a percent of revenue. Many of our cost categories improved as a percent of revenue during the quarter, although our operating supplies and expenses increased 300 basis points due primarily to the rising cost of diesel fuel and other petroleum-based products as well as the increased cost for parts and repairs to maintain our fleet.

We more than offset the impact of this increase with the improvement in our salaries, wages and benefits and purchase transportation. The improvement in these expenses as a percent of revenue reflects our best efforts to effectively match all of our variable costs with current revenue and volume trends.

In this case, the company's operating ratio improved despite diesel shortages, labor issues, and overall high inflation. In this case, it helps that LTL shipping companies have better access to employment as the work is simply more pleasant than working for a truckload company. Moreover, while ODFL did see higher costs, it outperformed its peers, resulting in new business growth and higher efficiencies.

Strengths Despite Weakness

As most know by now, the (global) economy isn't doing so well right now. Both the ISM manufacturing and non-manufacturing index are now in contraction territory, inflation is still high, and the Fed is looking to continue its hawkish endeavor despite these issues.

Wells Fargo

As LTL trucking companies are highly dependent on industrial production, one can imagine that these companies are now in a much different position compared to 2020 and 2021, when trucking shortages and high demand were favorable for both volumes and rates.

On December 5, Old Dominion Freight Lines updated us on its fourth quarter. The company saw a decrease of 8.6% in LTL tons per day. This was due to 7.3% fewer shipments per day and a decline of 1.4% in LTL weight per shipment.

However, revenue per day increased by 7.3%. Quarter-to-date, LTL revenue per hundredweight and LTL revenue per hundredweight, excluding fuel surcharges, increased 17.3% and 8.6%, respectively, as compared to the same period last year.

The company mentioned both a soft economy and its ability to use its superior business to its advantage (pricing):

"We believe the year-over-year decrease in volumes is primarily due to continued softness in the domestic economy, as customer demand for our superior service has remained consistently strong. Our ability to provide superior service at a fair price adds value to our customers’ supply chains while also strengthening our customer relationships. We remain focused on this fundamental element of our long-term strategic plan, and we believe the disciplined execution of our plan will continue to support our ability to win market share and increase shareholder value.”

Hence, we're now in a situation where ODFL shares are less than 14% below their all-time high. The market is underperforming ODFL by more than 300 basis points. That's truly remarkable.

Add to this that Graig Fuller , CEO at FreightWaves, came out mentioning returning strength in the trucking industry.

Over the past week, we’ve spoken with numerous freight executives who have mentioned that the first two weeks of the first quarter are shaping up better than expected, granted, expectations were incredibly low after such a weak peak.

Going into the quarter, executives we spoke with predicted a significant collapse in freight for the first quarter, with a seasoned veteran executive of a large trucking technology firm predicting that the first quarter would be the worst in his four-decade career. It was a fair bet considering how challenging the second half of the 2022 was for most in the freight market.

The truckload spot rate has bounced back to $1.98 per mile, after falling to $1.67 in November of 2022.

FreightWaves

Tender volumes also suggest that the market is not seeing gloom and doom. The Outbound tender Volume Index has improved after briefly dipping below 2019 and 2020 levels.

FreightWaves

To quote Mr. Fuller one more time:

If the first few weeks of the new year are an early omen, then the freight market may have bottomed in the fourth quarter and carriers can look forward to a far less volatile market in 2023.

Valuation

Another benefit that comes with the company's outperforming organic growth and high efficiency is high free cash flow, resulting in a very healthy balance sheet. Since 2017, ODFL does not have a balance sheet with net debt (gross debt minus cash). The company is expected to end 2023 with close to $800 million in net cash.

EBITDA is expected to dip to $2.0 billion, with EBITDA margins remaining above 32%.

{kind=link}

Using 2023 numbers and ODFL's $34.8 billion market cap, we get an implied enterprise value of $34.0 billion. That's 17.4x EBITDA.

I believe that this value is fair. It's not deep value, yet it incorporates strong and rising operating profitability on a long-term basis.

The only problem I see is that we're somewhat in an economic no-man's land. Economic growth is rapidly declining, yet stocks are rebounding. The market is betting on a dovish Fed. The question is if we get a dovish Fed. Given how sticky inflation is, that is unlikely.

Yet, transportation volumes are bottoming, providing fertile ground for higher industry expectations. If we're indeed past the demand bottom in trucking, ODFL's stock price is poised to move to at least $400-$500 per share. On a side note, that's where I see the fair value, anyway.

FINVIZ

My strategy remains to wait for a move lower. While I do not disagree with Fuller that demand may bottom at very low levels, I believe that the market will offer us a new correction opportunity soon.

The market is pricing in a return to normal way too quickly, in my opinion. While the Fed will eventually pivot, I believe it will have to cool expectations in the weeks and months ahead.

Hence, while my bullish title reflects the longer-term opportunities, I do expect a buyable correction this year.

Takeaway

In this article, we discussed Old Dominion Freight Lines. This truly unique trucking company comes with an excellent business model, high margins, great pricing opportunities, and high expected future growth.

The stock is even trading at a reasonable valuation. Hence, I believe the stock could fly if demand is indeed bottoming.

The only reason why I remain cautious is that I'm not buying into the market's euphoria right now. I believe that a hawkish Fed will provide long-term investors like myself with another opportunity to buy great stocks at better prices. The Fed is more than likely going to hike more aggressively than expected in a weakening (global) economy. That could keep trucking volumes from taking off.

That's the only reason I'm remaining on the sidelines.

Once demand is allowed to improve (meaning the Fed is taking its foot off the brake), I believe that ODFL shares will fly.

(Dis)agree? Let me know in the comments!

For further details see:

Old Dominion Is Set To Fly Higher