ONB - Old National Bancorp: A Quality Bank Investors Should Take A Close Look At

2023-10-05 11:57:42 ET

Summary

- Old National Bancorp has attractive growth potential in the banking sector, with growth in loans, securities, and cash, as well as increasing deposits.

- The company has expanded through acquisitions and mergers, becoming the 6th largest commercial bank in the Midwest.

- Despite increasing debt levels, Old National Bancorp has seen growth in net interest income and net profits, driven by higher spreads on loans and greater asset values.

- Shares aren't the cheapest, but they aren't bad, either.

Although nothing comes without risk, I have noted that there are some rather interesting prospects in the banking sector at this time. A brief banking crisis earlier this year caused a great deal of havoc, with some institutions failing outright and others experiencing significant downward pressure. The market still seems to be on somewhat shaky ground from a confidence perspective, with many of these institutions having yet posting a full recovery from a share price perspective. This has created some really attractive prospects. But not every company in this space is truly compelling.

One that is, however, even though it's not the cheapest from a valuation perspective, is none other than Old National Bancorp ( ONB ). With attractive growth, both on its top and bottom lines, as well as growing deposits and modest uninsured deposit exposure, the bank holding company warrants, in my mind, a soft "buy" rating.

Great growth

With a market capitalization of $4.17 billion as of this writing, Old National Bancorp is not exactly a large bank. But it is larger than most of the others that I have come to analyze. The company was not always this big, though. While organic growth has always been part of its history, the company has also not been afraid to engage in purchases and merger activities in order to expand. The biggest example of such a maneuver occurred in February of 2022, when the bank merged with First Midwest in what management described as a combination of equals. This has allowed the bank to become the 6th largest commercial bank headquartered in the Midwest and, with $48.5 billion in assets, one of the 30 largest in the country.

The institution operates 256 branches and 348 ATMs. Through these branches, Old National Bancorp engages in a variety of activities. Examples include, but are not limited to, accepting deposits, originating commercial loans, giving out loans for real estate and other means, extending lines of credit, and more. The company also offers wealth management, investment, and foreign currency services for its customers. However, the company is not afraid to sell off assets when they no longer are appealing to it. In November of last year, for instance, the enterprise sold off its operations of acting as a qualified custodian for health savings accounts.

{kind=link}

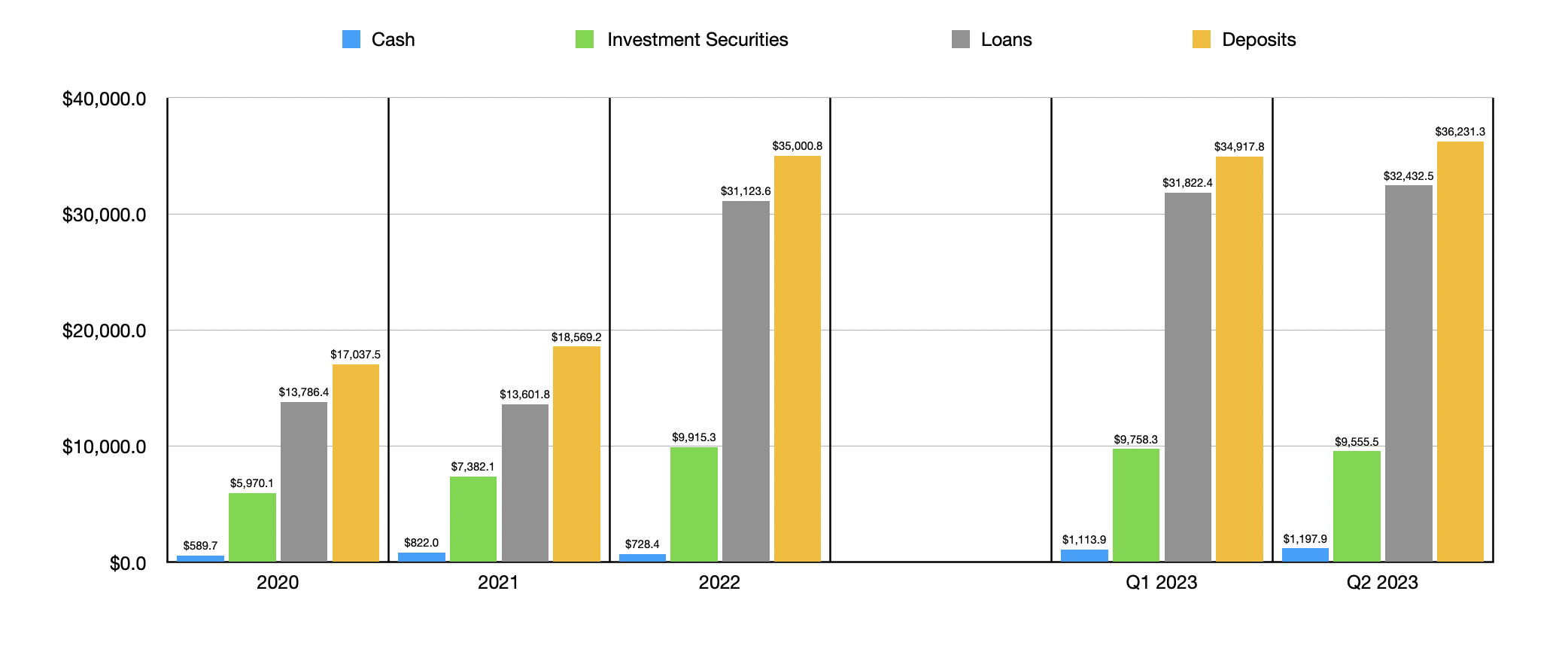

The company's growth, fueled largely by over 50 acquisitions since 1982, has allowed it to grow at a rather rapid pace. From 2020 through 2022, for instance, the bank saw the value of its loan portfolio balloon from $13.79 billion to $31.12 billion. The value of securities jumped from $5.97 billion to $9.92 billion, while cash and cash equivalents grew from $589.7 million to $728.4 million. As you can see in the chart above, the company's loan portfolio and cash have both continued to grow into the current fiscal year, with these figures climbing to $36.23 billion and $1.20 billion, respectively. The value of securities, meanwhile, has pulled back slightly to $9.56 billion.

{kind=link}

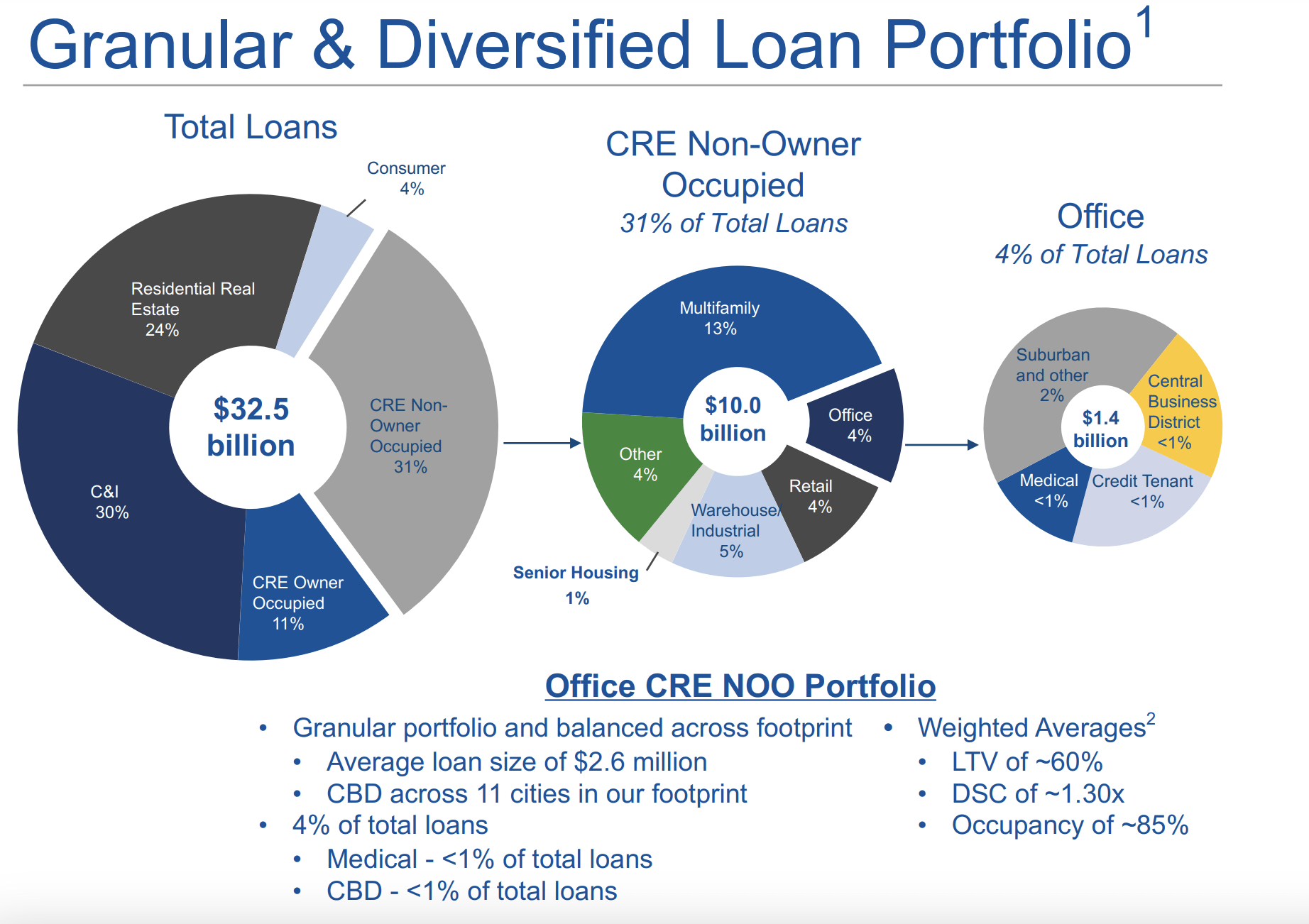

It should be mentioned that most of the company’s exposure from a loan perspective involves non-owner occupied commercial real estate. That accounts for $10 billion, or 31%, of its loan portfolio. Most of that, totaling 13% of its total loan portfolio in all, involves multifamily properties. But I do know that office space has been a concern that many investors have had this year. Fortunately, only 4% of its loans are dedicated to those particular assets. Commercial and industrial loans come in at a close second at 30%, while residential real estate totaled 24%.

This increase in loans, securities, and cash, was only made possible by a surge in the value of deposits on the company's books. Deposits totaled $17.04 billion in 2020. By 2022, they had more than doubled to $35 billion. The company did see a bit of weakness in the first quarter of this year, with the value of deposits dipping to $34.92 billion. But that seems to have been caused by the aforementioned asset sale. I say this because those particular assets had deposits totaling $382 million. Since then, deposits have resumed their growth. From the end of the first quarter of this year to the end of the second quarter , the value of deposits at the bank expanded by $1.32 billion to $36.23 billion. In addition to seeing this attractive growth, the bank also reported that less than 30% of its deposits are classified as uninsured. 30% happens to be the threshold that I use when splitting up the attractive prospects from the ones that are not attractive. So this is great to see.

{kind=link}

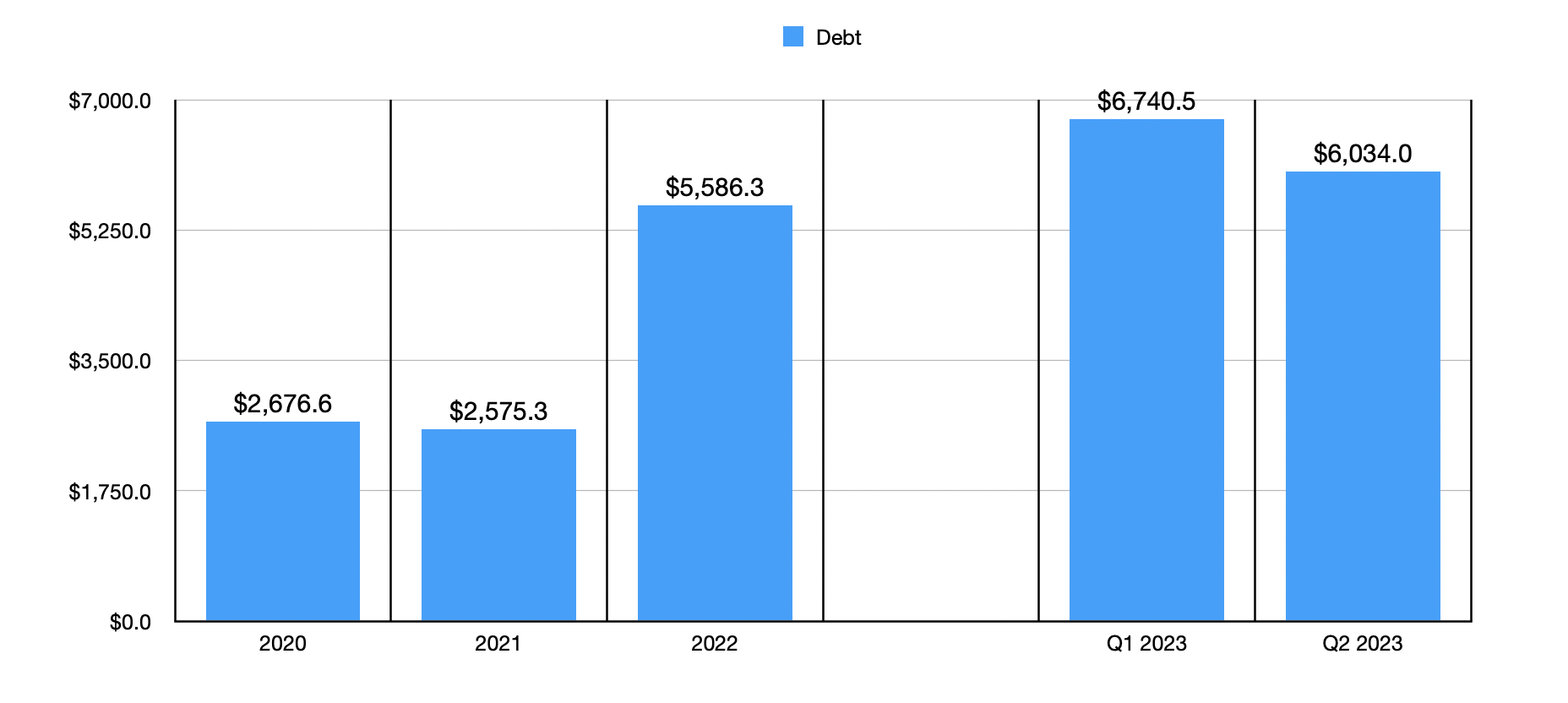

Perhaps the only negative about Old National Bancorp that I have seen involves its debt. Back in 2021, the company had $2.58 billion in debt on its books. This jumped to $5.59 billion by the end of 2022. We have seen this continue to climb, with the metric hitting $6.03 billion at the end of the second quarter this year after briefly touching $6.74 billion in the first quarter. These debt levels are not terrible for a bank this size. This is especially true as we need to look at the amount of cash and securities on its books. But it's also not fantastic.

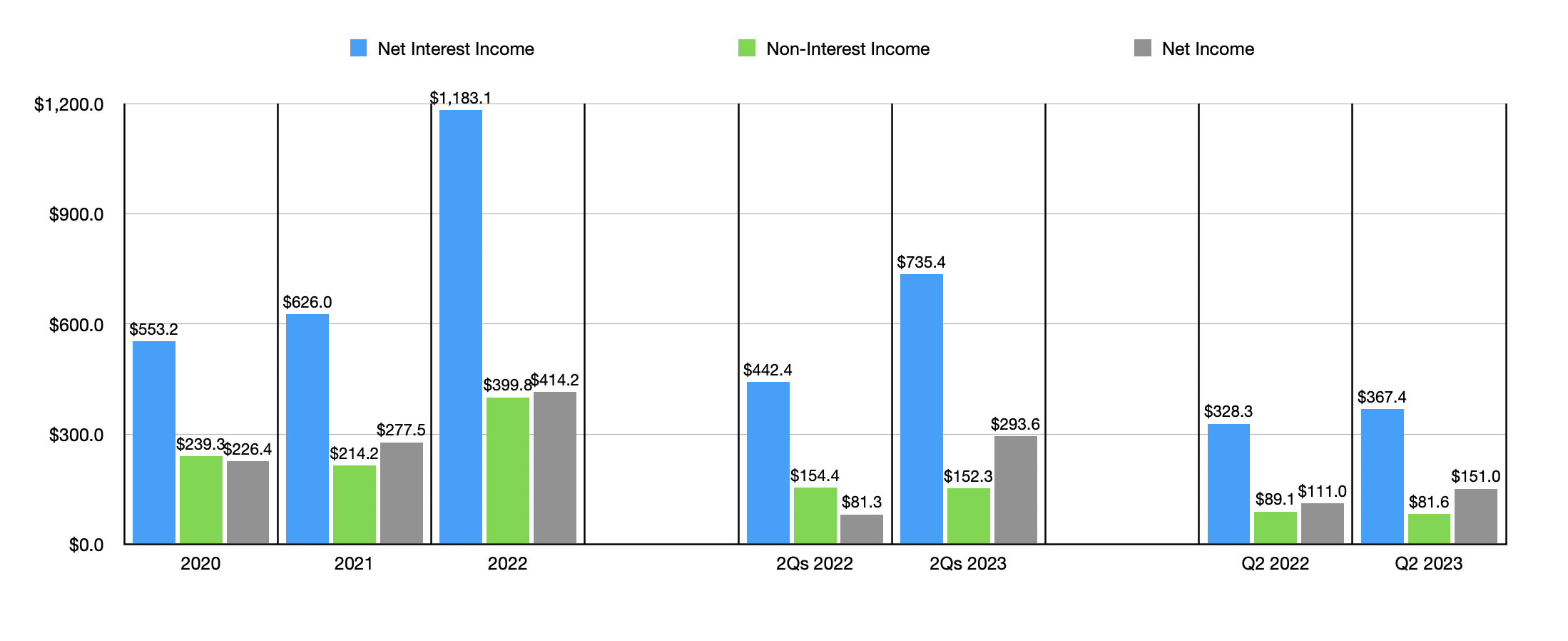

The overall growth of the company’s assets has allowed it to grow both its top and bottom lines in recent years. Net interest income more than doubled from $553.2 million in 2020 to $1.18 billion in 2022. Non-interest income almost doubled from $239.3 million to $399.8 million, while net income jumped from $226.4 million to $414.2 million. This year has been problematic for many banks, with a narrowing of the net interest margin and a decline in assets coalescing to create a condition where financial performance has worsened. But that has not been the case when it comes to Old National Bancorp. Non-interest income has dipped slightly in the first half of this year compared to the same time last year. But both net interest income and net profits have increased materially.

{kind=link}

This increase was driven by two primary factors. First, the value of average earning assets of the bank grew from $36.27 billion last year to $42.52 billion this year. And the second relates to the firm's net interest margin. This is the net interest that it can capture on its average earning assets. This increased from 3.13% in the first half of 2022 to 3.65% the same time this year. While this may not sound like much, when applied to the average earning assets of the bank at the end of the most recent quarter, we get extra revenue and profits of $221.1 million from the increase in the net interest margin alone. Higher spreads on the loans that the bank has given out have been a big driver of this improvement. Interest associated with loans has grown from 3.86% to 5.59%.

{kind=link}

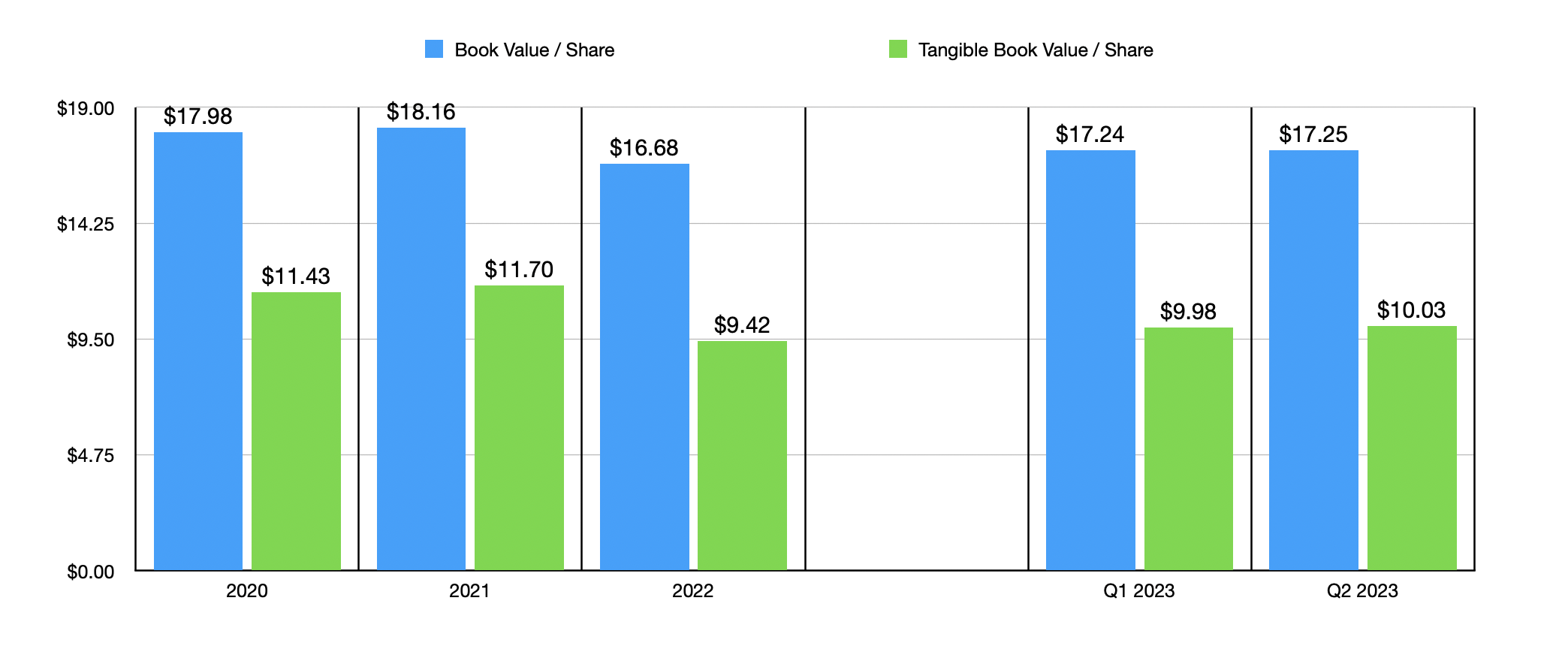

While this year does look to be setting up to be a great time for Old National Bancorp and its shareholders, when it comes to valuing the company, I would prefer to be more conservative and rely on the results achieved in 2022. After all, I don't believe that we are going to be dealing with high interest rates a year from now and, if I am correct, we should see the net interest that the company generates pull back to some extent. Relying on the figures from 2022, I found that the company is trading at a price to earnings multiple of 10.1. This is slightly lower than the average of 10.4 that I have seen elsewhere. It is trading at a discount to its book value. The price to book ratio for the company is only 0.82, while the price to tangible book value ratio stands at 1.41. None of these are the best that I have seen. But they are also not the worst.

Takeaway

Whether you love Old National Bancorp or hate it, one thing that's undeniable is that management has done a great job of growing the company's physical footprint. The value of assets on the company’s books has grown markedly in recent years and I believe that this trend could very well continue for the foreseeable future. Relative to the industry average, shares are only marginally cheap. But I do like to see it trading at a discount to book value while simultaneously growing its top and bottom lines. Given these factors, I've decided to rate the business a soft "buy" at this time.

For further details see:

Old National Bancorp: A Quality Bank Investors Should Take A Close Look At