ORI - Old Republic International: Strong Addition To A Dividend Portfolio

2023-06-21 09:48:02 ET

Summary

- Old Republic International Corporation is a strong dividend aristocrat with a near 4% yield, supported by robust cash flows generated through insurance and underwriting services.

- The company has a strong balance sheet, with $12 billion in cash and fixed-income securities, and a low debt of $1.5 billion, allowing for consistent dividend increases even through economic downturns.

- Despite some concerns about inconsistent revenue, ORI stock remains a solid investment opportunity due to its strong dividend history, share repurchase plans, and potential for growth in the global insurance market.

Investment Outline

Old Republic International Corporation ( ORI ) is certainly a strong contender as part of a diversified dividend portfolio. The company has a near 4% yield supported by strong cash flows which it generated through its insurance and underwriting services. ORI has established itself as a prominent company in the insurance industry. The industry is prone to the effects of lower interest rates, making their product less attractive and as a result often yields lower sales and a decrease in premiums which impacts the amount of capital the company has to invest into its portfolio. Betting on when interest rates are going down is a difficult game, but over the long term, ORI seems to have managed fine through most of these ups and downs.

ORI places most of its focus on the commercial side of insurance and lacks exposure to insurances for homeowners or automobiles. This focus on industries however has made the company deploy several techniques, like utilization of policy deductibles and policyholder dividend plans, which have helped it grow over the years.

ORI stock is a solid option for investors seeking a strong dividend aristocrat that has for many years continued to distribute a dividend. It hasn't stopped paying out a dividend for the last 80 years and increased the dividend for 42 years in a row. That should say something about the type of company we are covering here. Because of the decent growth prospects associated with the business and the strong payout history, I rate the company as a buy.

Recent Developments

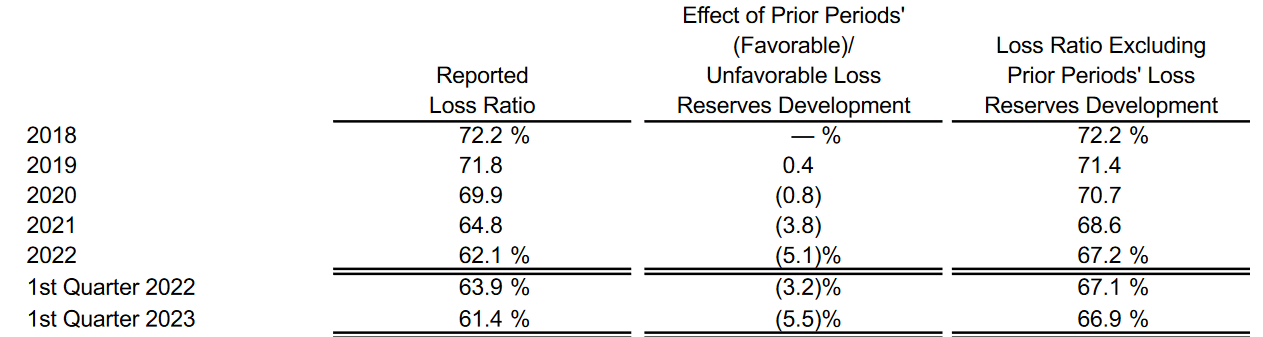

In the first quarter of 2023, ORI managed to complete its previously announced share buyback program. This entailed buying back shares for $450 million which was completed in April 2023. The quarter also showed ORI able to grow its general insurance segment at a decent 5.9% YoY, reaching nearly $1 billion in revenues for the quarter. This growth however resulted in a strong 35.6% increase in the pretax income for the segment. Where investors might be worried is the fact that the title insurance part went from $80.9 million in pretax income to $17.4 million. Looking historically though, the overall loss ratio for the business is decreasing, which is a great sign to see. Sitting at 61.4%, it has made strong steps forward from the 72.2% loss ratio back in 2018. Keeping up this trend further fuels a buy case and, as a result, I think the last quarter was a success for ORI.

{kind=link}

Where the investment case grows stronger with ORI is that the board of directors very recently announced that they are authorizing another buyback program with the same budget, $450 million. In Q1 of 2023, around $168 million in funds were used for repurchasing shares, so I find it likely that we'll see the new authorization completed within the next 12 months if the cash flows remain the same and the share price doesn't see a massive spike upwards. Within the next 12 months, that would mean about 6% of the outstanding shares would be repurchased. Combine that with the dividend yield nearing 4% and we have close to 10% in appreciation here for an investment, just solely from what the company themselves are doing. This really strengthens the buy case for the company, in my view.

Dividend History (Investor Presentation)

This new announcement is, in my opinion, heavily supported by the strong FCF the company is generating right now, although not the same as in 2021 perhaps when most companies in the sector were experiencing strong profits. ORI is still at a decent rate increasing FCF margins, and the last 12 months have meant $521 million in FCF.

Margins

Taking a look at the margins of ORI we can quickly note that they have a very strong gross margin of 68% in the last 12 months. This is a fair bit above the sector's average of 58%. With the insurance industry being very competitive , seeing strong margins like this is reassuring. ORI might not hold a substantial part of the market share , but they have proven to be able to grow whilst maintaining margins. That highlights the quality of the business quite well in my opinion. With ORI focusing on providing risk management to their clients, they have over the last 10 years achieved a book value CAGR of 11.5%. The company focuses on carefully selected major sectors in the USA that aren't at the same time exposed to a common business cycle, so essentially they keep a broad exposure to several industries like energy and commercials in order to create long-term stability. This approach lets ORI be more consistent with its growth and provides a safer investment for its shareholders. The company's title insurance business, for instance, has grown to become the third largest in the industry.

Margins (Seeking Alpha)

The company right now receives a B+ rating in terms of profitability and I think there is room for improvement. The bottom line has more upside potential from here, in my opinion. From the last report, it should be noted that ORI is experiencing a high renewal retention ratio in its General Insurance segment, which happens to be the largest segment in the business.

ORI has a hold by Wall St. Analyst ratings right now, but I think a more fair rating would be a buy considering the solid state of the business and margins. The benefit from the repurchase program is also an intriguing enough reason to assign a buy on the stock. The company is still trading under its average P/E of 11.9 over the last 10 years. That, together with a strong push by the management to repurchase shares and an unbeatable history of raising the dividend, holds the potential for plenty more upside to an investment here over the long term.

Balance Sheet

Supporting ORI right now with its dividend and repurchase endeavors is a balance sheet that lacks little. The cash the company is gathering has been steadily increasing over the last couple of quarters. With $12 billion in cash and fixed-income securities, it heavily outweighs the long-term debts in favor of assets. In fact, debts sit quite low at just $1.5 billion, which reflects the robust position the company is in financially. This has, over the years, aided the business in making sure they are able to raise the dividend even through downturns in the sector and also the broader economy.

With that said, the company's book value per share is currently at $21.91, which is not far below the current share price. This slight premium seems fair to me to pay if you want to get exposure to the market the company operates in and also capitalize from the dividends distributed. With upside potential for the share price as well, I think a fair earnings multiple would be somewhere around the long-term average of 11.9, further bolstering the investment thesis surrounding the company.

Valuation

ORI has a current P/E of 10.4 on a forward basis, which is below the long-term average of 11.9. If it is raised to the long-term multiple, the company would trade at $28 per share based on the 2023 EPS estimates of $2.42. I find it fair to suggest that ORI could see a further upswing in the share price, despite already being up over 17% in the last 12 months. Reaching $28 per share would mean a 15% upside potential from here.

ORI Gradings (Seeking Alpha)

Peer Comps

Kinsale Capital Group Inc. ( KNSL ) trades at a much richer premium than ORI right now, so they don't come out ahead. KNSL's margins might be better - in terms of net margin and levered FCF margins - but with a near 32x multiple to forward earnings, the upside potential seems very limited. Instead, there is a significantly higher risk of a drop in the share price to reflect a more realistic valuation, in line with the sector. In terms of the dividend opportunity, KNSL really underperforms with its 0.16% yield. Besides, you are paying a pretty hefty premium of 8x for the book value of the business. ORI has a P/B of 1.08, which in my view shifts the favor for ORI in terms of where to make an investment if you are looking for a solid dividend opportunity.

I want to also quickly make a comparison between ORI and Selective Insurance Group ( SIGI ). SIGI is a bit more focused on personal insurance coverages rather than solely on the commercial side. Margin wise, ORI has outdone SIGI in several parts. With SIGI having a gross margin of 21%, and ORI 68%, the winner is clear. But where SIGI has performed well is maintaining strong cash flows, which nets a levered FCF margin right now of near 16%. That has helped them maintain a decent dividend yield of around 1.2%. But it hasn't translated to buying back shares, rather the shares outstanding have been increasing instead.

Strong Dividend History

One of the main attractions of ORI right now is its very strong history of dividend payouts. They have, over the last 10 years, managed to raise the dividend and always maintained a strong yield to their investors. Comparing the company's yield to the 1.5% for the S&P 500, ORI is the clear leader here. Paired with its growth prospects, this means the stock could offer a better return over the long run as well. ORI also comes out ahead on this yield metric, when looking at peers in the same industry. Both First American Financial Corporation ( FAF ) and Selective Insurance Group have lower yields and higher valuations, which presents ORI as both the safer investment and the highest-yielding one right now.

Risks

Where there are some concerns is the revenue for the company which has been inconsistent on a YoY basis - peaking at over $9 billion in 2021 and steadily declining since. With the net premiums dropping by 19%, the company's ability to serve its shareholders and remain a solid business is a cause for concern. However, it does have a strong base of customers where some of the costs can be passed down.

But what does mitigate some of the concerns is that the net investment gains is growing at 29% YoY, reaching $137 million. With this level of growth, losses in other parts of the business are mitigated and shielded. Looking at the global insurance market, it remains quite robust and prices are expected to increase to reflect the growth the industry is experiencing. I am certain this growth will be visible in the coming quarterly reports, which will further support the case that ORI deserves a higher multiple.

Investor Takeaway

Old Republic International is a stable dividend aristocrat that, in my view, is a solid addition to any portfolio seeking a decent yield supported by growing cash flows. ORI ticks off all those boxes for me. The board of directors also quite recently announced a new share repurchase plan which, if all used, would decrease the outstanding shares by around 6%. For the long term, these moves are great to see and make me rate the ORI stock a buy.

For further details see:

Old Republic International: Strong Addition To A Dividend Portfolio