OLN - Olin Corporation: Downtrending Metrics Do Not Inspire Confidence

2023-12-19 00:11:43 ET

Summary

- Olin Corporation is a global manufacturer of chemicals and ammunition products, with a leading position in the industry.

- The company's recent quarters have seen declining metrics, including lower volumes and pricing, higher costs, and reduced profit.

- Olin expects its 2023 Q4 results to decline significantly and faces challenging global conditions, leading to inflating valuations.

- I believe there are better places for your capital than this stock and recommend a Sell rating over the near term.

Olin Corporation ( OLN ) is a global manufacturer of chemicals and ammunition products. Being a leader in some of the segments it operates in, the company flies largely under the radar. As an investment, this business (as we will see further) is largely cyclical. Fluctuations in demand and pricing impact its earnings, and we are seeing it play out right now. But its leading position in the industry and the areas it serves have intrigued me, and while it does not interest me as an investment right now, it is on my radar.

Business Model

I primarily see two main lines of businesses operating under the Olin Corporation

-

Chemicals Segment:

- Olin's chemicals business involves the production of chlor alkali products, vinyl, epoxy, and other specialty chemicals (Key products include chlorine, caustic soda, hydrochloric acid, sodium hypochlorite, epoxy resins, etc.).

- The chemicals produced by Olin have applications in various industries, including agriculture, food processing, pharma, textiles, and electronics.

- Its scale, integration, and raw material positions make it one of the low-cost producers in the chlor alkali and epoxy industry.

-

Ammunition Segment:

- Olin is a major producer of ammunition products for commercial, military, and law enforcement markets (The Winchester brand, owned by Olin, is well-known for its firearms, ammunition, and related products)

- Olin believes that it is a leading U.S. supplier of small-caliber commercial ammunition

Declining metrics from recent quarters

The company saw its best year in terms of revenue and profitability in 2022. But recent quarters have seen this normalizing and moving towards the five-year average.

The balance sheet saw declining cash, high inventory, and total equity remaining flat over a multi-year period.

In its latest quarterly report, the company has explained the headwinds it is facing in its business. It saw lower operating results across all of its business segments. In the chlor alkali products and vinyl segments, the company saw lower volumes and pricing, higher costs, and reduced profit from lost sales associated with operating issues. The story was no different in the Epoxy line of products, and the factors that caused lower pricing were due to record exports out of Asia into the European and North American markets. This pattern is repeated in the Winchester segment.

The company also saw restructuring charges to reconfigure its global Epoxy asset footprint. The restructuring was to optimize its most productive and cost-effective assets to the tune of $80M. Interest expense was also higher by $30M due to higher average interest rates. All in all, the last few quarters have not been conducive to the growth of the company. But do we see this improving in the near future? This is what we know from their outlook.

- Expects 2023 Q4 results to decline significantly from the previous quarter

- For the Chlor Alkali Products and Vinyls division, the company sees challenging global conditions and expects reduced market participation

- Epoxy business to be plagued again by European and North American demand weakness exacerbated by elevated Asian exports

- Expects continuing restructuring charges through 2026 (less material)

Scenario-based valuation

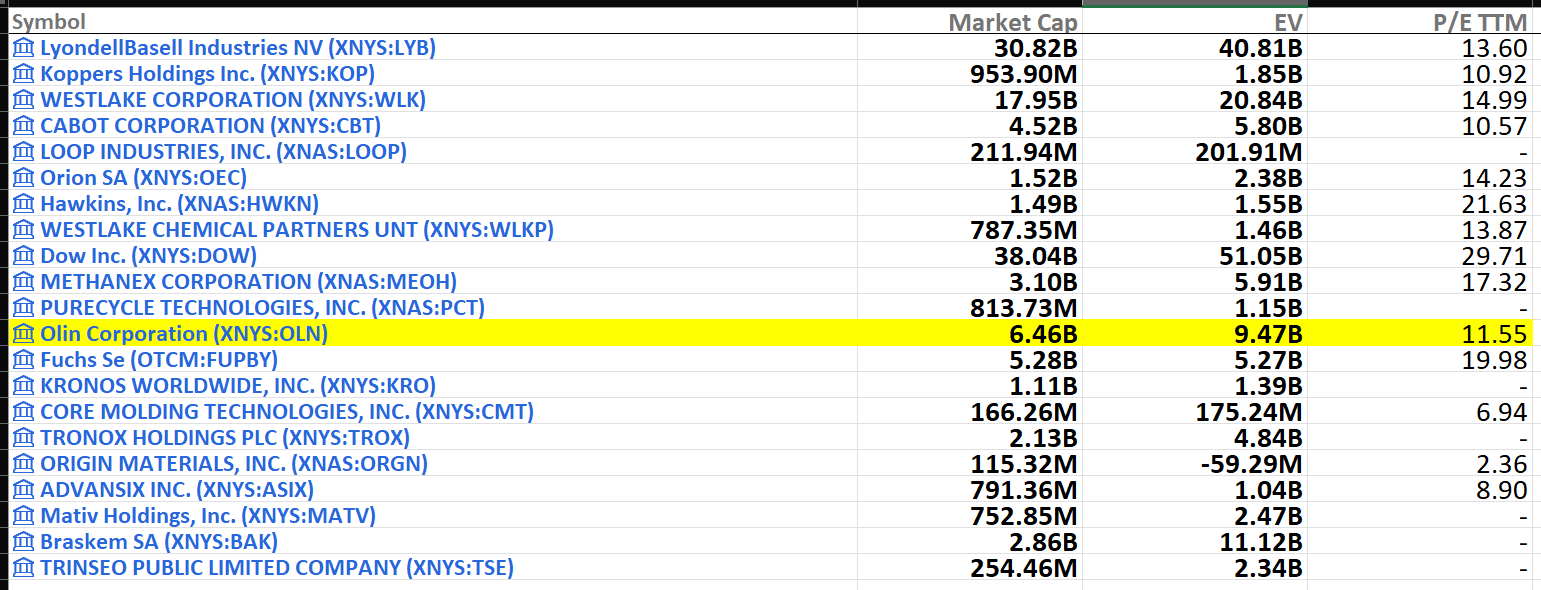

In light of challenging conditions and uncertainty in its outlook, I believe we need to value this company under a range of scenarios. Currently, it trades at a PE multiple of 11.5x. The decline in the EPS resulted in the multiple expanding significantly. But this is still below the sector median of 18x. It also compares favorably against its industry peers.

{kind=link}

But this won't be sufficient. An uncertain future and challenging macro mean the forward multiples need to be evaluated and possible situations should be factored in.

{kind=link}

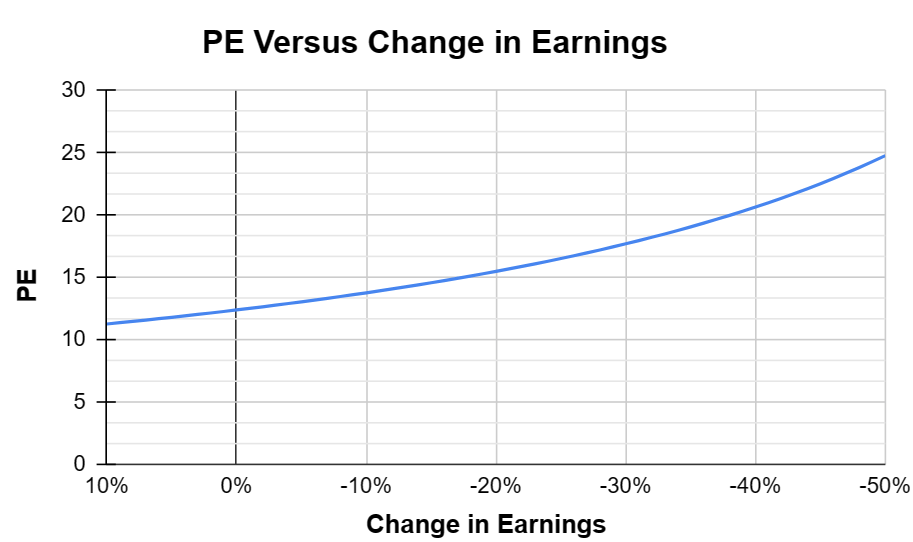

In the last few quarters, we have seen net income drop by more than 60%, and from the chart, we see that the multiples continue to expand rapidly for any further downward change in earnings. This could mean that the stock may see a reset in its price for the valuation to be in line with the sector median. The next few quarters may be tricky indeed to continue holding the stock. This is also confirmed by insider activity.

{kind=link}

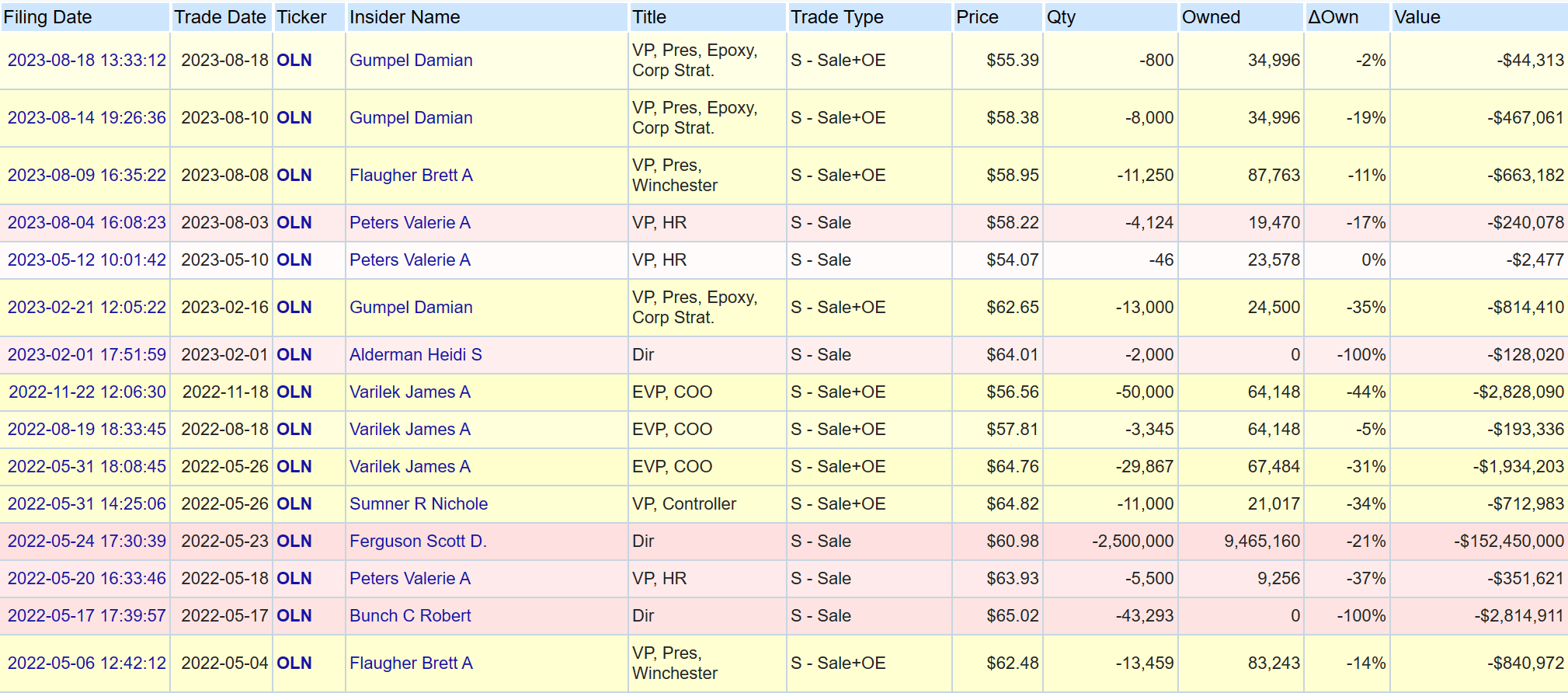

When you look at insider trades, we only see sells, which could be a good indication that we may have seen peak performance of the company in this cycle as the executives are taking some of their chips off the table.

A Positive note

Management initiated a stock buyback program at an aggregate price of up to $2B and we are already starting to see some of the effects of this.

The net effect of the decrease in share count may end up arresting some of the decline in the EPS. But it could get tricky again if the environment gets worse. As of September 30, 2023, $1.11B remained authorized to be repurchased under the program. The program could be suspended if the management decides to conserve cash against a difficult environment.

Final Call

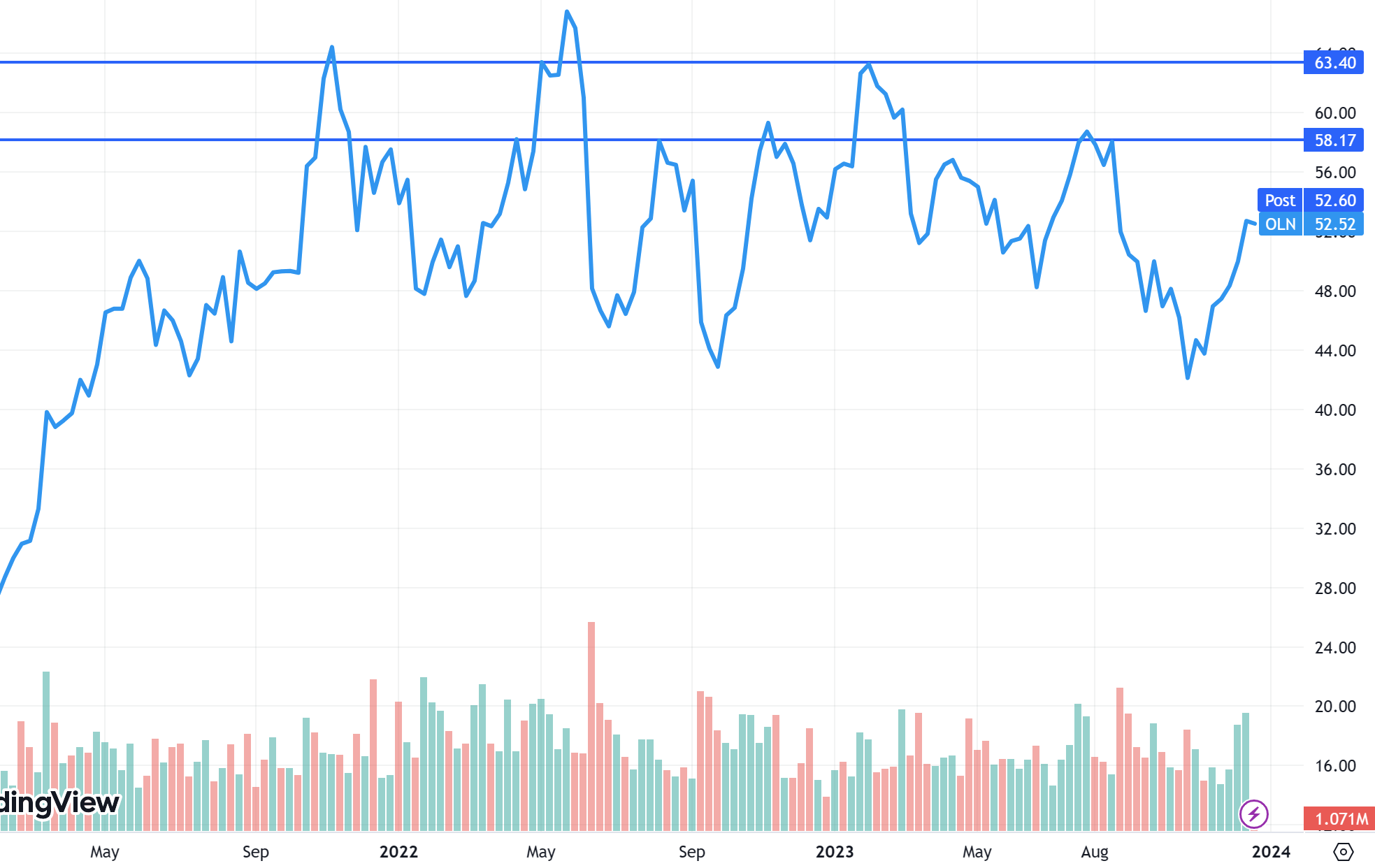

I am rating this as a Sell. I believe the stock price could see further correction and the near-term future is not conducive to an investment in this company. The stock has been in a tight consolidation for more than 2 years and faces significant resistance around $60. It could get tough for the stock to break this resistance unless there is a big positive outlook for the company, and as we saw from its recent quarter, this is not possible in the near future. At present, I believe that there are better places for your capital than this stock.

{kind=link}

For further details see:

Olin Corporation: Downtrending Metrics Do Not Inspire Confidence