OLN - Olin Is Likely A Value Trap

2023-10-10 15:23:18 ET

Summary

- Olin Corp's shares have fallen due to the departure of its CEO and concerns about global growth.

- The company's earnings and revenue have declined, with volume and pricing pressures affecting its three business lines.

- Olin's business is heavily reliant on the Chinese construction market, which is facing major issues and could exacerbate supply conditions.

Shares of Olin Corp ( OLN ) have fallen over the past two months, given the departure of its CEO and ongoing global growth concerns. Shares are roughly flat to when I last wrote about the company in October 2022 , rating the stock a hold. While the stock is cheap, it faces some credibility challenges as well as macroeconomic headwinds. As such, I fear Olin may continue to be more of a “value trap” than “value opportunity.”

{kind=link}

In the company’s second quarter , Olin earned $1.13, which was down 59% from last year on revenue of $1.7 billion, down 35%. The company is facing both volume and pricing pressures, which are weighing on results. These pressures exist across its three business lines to different degrees. Winchester revenues fell 17% to $367 million sending EBITDA 43% lower to $71 million as commercial volume and prices fell while higher costs squeezed margins. This ammunition business tends to be the least economically cyclical, and conflicts in Ukraine and Israel could help support increased commercial sales in coming quarters, though this is not yet materializing.

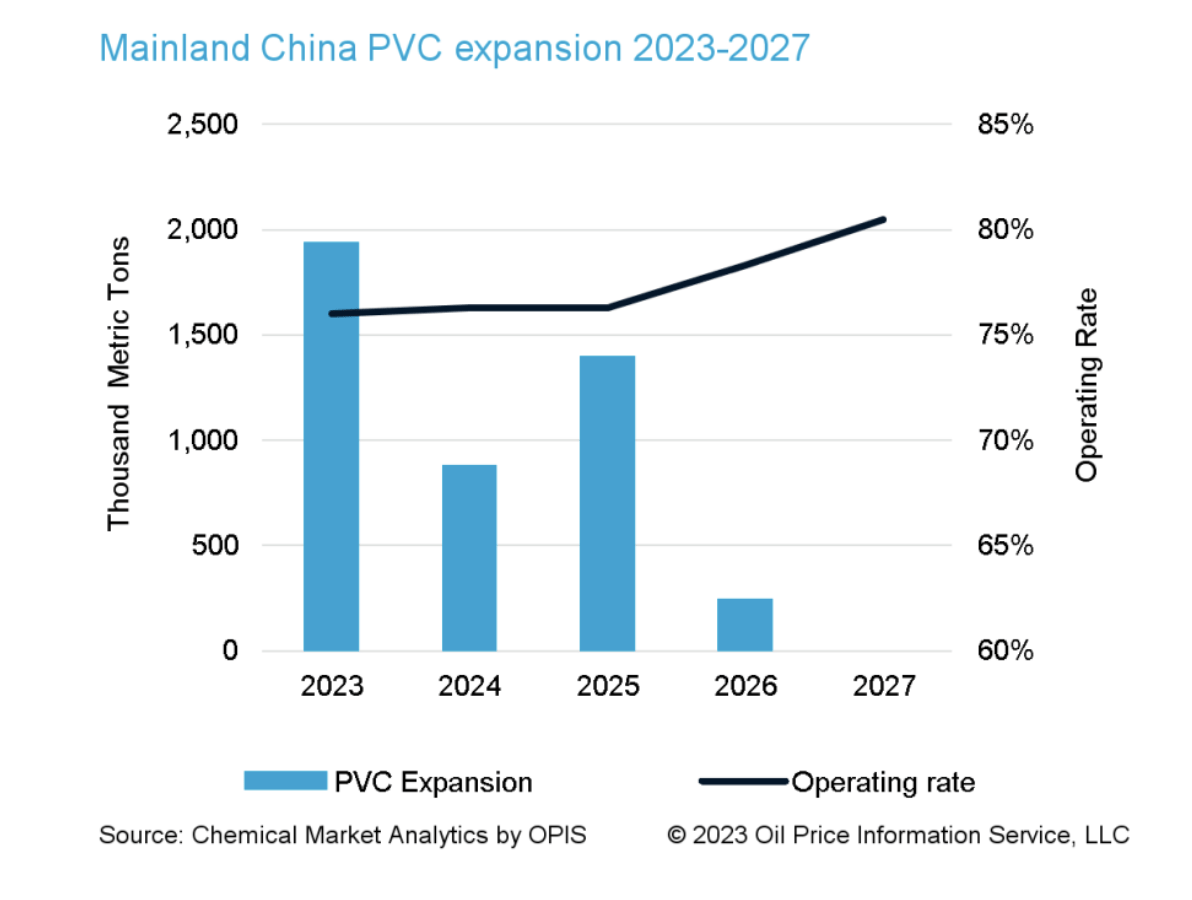

Its Chlor Alkali & Vinyls unit saw revenue drop 29% and EBITDA fall 37% to $293 million, exacerbated by operating issues at a plant. Epoxy EBITDA fell over 90% to $14 million as revenue plunged 57%. Management expects this unit’s EBITDA to turn negative by year-end, given supply pressures in the market. Products in these units provide chemical inputs to and adhesives for PVC piping, and 70% of PVC is used in construction.

Now, I have written in the past how construction activity in the US has been quite strong, which recently underlined my bullish thesis for Steel Dynamics ( STLD ). It is essential to note that while US construction activity is solid in my view, Olin’s PVC-oriented products serve a global market in which China is the leading consumer and faces major issues in its construction sector. Last year, China accounted for nearly half of global demand, and the US was just 10%. Olin’s business is much more geared towards activity in the Chinese real estate market, than our own.

S&P Global

That market remains especially troubled with multiple firms like Evergrande facing potential liquidation. I do not have a strong degree of conviction in either direction on Chinese construction activity, given the complexities, uncertainties, and opaqueness around actual activity levels and potential government actions. However, we do know that according to management the chemical market is weak amid over-supply in epoxy. Even if Chinese demand recovers, I fear over-supply conditions may persist.

This is because China has plans to increase supply of PVC as it builds out factories. Chinese demand will need to rise just to meet this incremental supply. If its construction market stagnates or worsens, these new facilities will just exacerbate the excess supply conditions the market faces today.

{kind=link}

Moreover, China’s exports had fallen last year , amid restrictions as lockdowns reduced its production, but have risen this year as these restrictions were loosened and domestic demand was soft. We have seen how this increased supply has reduced Olin’s profitability; if more supply from China comes online and has to be sold internationally, these pricing pressures can persist well into 2024. This is why, on balance, I view the macro environment as a headwind for Olin.

Now, cyclical companies always face ups and downs—that alone is not reason to buy or sell shares. The challenge facing Olin on top of this is credibility about how it manages and guides through the cycle. Last year, management said in a recession EBITDA would fall to no less than $1.5 billion, compared to the $636 million it generated in 2020, due to cost cuts, rationalization of operations, etc. I felt this ambitious target should be viewed with some skepticism given the EBITDA declines already occurring last year amid slowing global growth and higher energy prices. There is no doubt management has taken costs out, but one needs to actually see a recession to be sure exactly how much, and an $850 million improvement is a bold prediction.

Now, the company is guiding to “trough-level” $1.4 billion adjusted EBITDA. It is blaming this shortfall this on a $50-100 million operating issue and excess epoxy supply, plaguing the market. Of course, excess supply is often what occurs in a recession, so that rationale feels like a stretch, relative to a problem running a plant at anticipated utilization levels. However, it is also important to note that we are not actually in a recession, in China, the United States, or even Europe. In an actual recession, demand would like be even weaker than it is today—presumably creating some downside risk to $1.4 billion truly being trough level earnings. As you can see below, OLN is labeling trough full year EBITDA at a $350 million quarterly run-rate (consistent with the $351 million in Q2).

Olin

However, it will only achieve this because H1 EBITDA was $785 million. Its $1.4 billion calendar guidance assumes a $308 million quarterly run-rate (or $1.2 billion annualized) over the balance of the year. This is just adding to the uncertainty over what OLN’s true 12-month trough level of earnings power is, and unless the market returns strongly in Q1 2024, it will likely fall further below the $1.4 billion. This is why I believe management faces a credibility issue. And it is hard to disentangle that fact from the announced departure of its CEO.

In September , Olin announced its CEO, Scott Sutton, would be leaving the company under “mutual agreement” in H1 next year. This sent shares down as markets are often skeptical of the meaning behind such language. In particular, no successor has been named, which suggests this departure was not part of an existing succession plan, leaving us to wonder if there had been a falling out, or disagreement over strategy. Moreover, the fact an internal candidate was not immediately chosen could suggest the Board does not have complete confidence in the rest of the leadership team. That said, the departure, while seemingly not part of a plan, cannot be too confrontational as Sutton will be staying on until a successor is found next year, rather than leaving immediately.

Given management has under-delivered and over-promised on its recessionary earnings power, I understand why the board is looking for a change. For now though, investors are going to be concerned that either operational challenges plaguing production are proving more problematic to fix or that OLN will need to further revise down its trough-earnings power. At the least, when it finds a new CEO, I would not be surprised to see him/her adjust that pledge lower as new management often likes to give itself increased breathing room and lower expectations during their initial honeymoon period.

Essentially, Olin faces an over-supplied market in a challenging macroeconomic environment, the prospect of more supply from China, and dampened credibility over what its true earnings power is in a recession. These are all reasons to dislike the stock. The reason it is not an easy “sell” rating is that much of this is priced in, and even with the challenges, it still is generating solid cash flow, though less than hoped for.

Last year, I noted my view free cash flow would likely undershoot estimates and come in around $800 million. Instead, management is guiding to $700 million this year (including an unfavorable $50 million working capital). That implies $216 million of working capital improvement in H2, and $266 million of H2 free cash flow ex working capital. That means H2’s annualized underlying free cash flow pace is closer to $500 million.

With this free cash flow, OLN is returning capital to shareholders, though the pace will low. In Q2, it repurchased $187 million of stock, and the share count is down nearly 15% over the past year. It should be able to reduce its share count by another ~5% over the next year. Its balance sheet is also healthy, and while net debt to EBITDA has increased due to falling EBITDA, it remains low at 1.8x.

I expect conditions the company is currently seeing to persist at least for the next twelve months as it is unclear when/if the Chinese construction sector will rebound. With $500-$550 million in free cash, it has a free cash flow yield of ~8.75-9%. This level of free cash flow is consistent with $4-4.10 in earnings for an ~11.7x multiple.

For a company operating close to trough levels, these are not unreasonable levels and should limit downside. However, with meaningful management uncertainties, and exposure to China, I struggle to see a case for multiple expansion, which is why I expect shares to remain stuck in the $45-50 range. With stocks like Steel Dynamics (mentioned earlier) that also have low multiples but better fundamental stories, I see better investment opportunities than OLN and expect shares to stay flat over the next year.

For further details see:

Olin Is Likely A Value Trap