WING - Olo: Large Industry Strong Tailwinds And Value Proposition

2023-12-12 12:30:05 ET

Summary

- I recommended a buy due to its potential for continued growth, attractive valuation, and Olo Pay's growth potential.

- OLO is a software solutions provider to the F&B industry, connecting restaurants to technology and channel partners.

- OLO is well-positioned to benefit from the secular trend of digital sales penetration in restaurants and offers a strong value proposition to its users.

Investment overview

My recommendation for Olo Inc. ( OLO ) is a buy rating, as I believe it can continue to grow at the current low-20% rate given the strong secular tailwind, value proposition, and Olo Pay growth potential. The current valuation is also attractive, as it is near the lowest OLO has ever traded at. As OLO proves to the market that churn is not an issue and growth momentum can continue, I see a possibility for valuation to tick upwards (I did not model this for conservative sake).

Business overview

OLO is a vertical software solutions provider to the F&B industry, particularly restaurants. In essence, OLO is a two-sided network connecting restaurants to various technology and channel partners, including 3P digital ordering platforms like DoorDash. This enables restaurants to facilitate their digital strategy (e.g., online food delivery, digital kiosks, analytics, etc.). The complexity increases exponentially for restaurants that have multiple units (franchise model); as such, they look to OLO for a solution. OLO is a fast-growing company that has compounded its revenue at a 46% CAGR since 2018 to LTM3Q23, scaling revenue from $31.8 million to $215.1 million. Notably, the growth was not fueled by M&A or debt; OLO has had a clean balance sheet (net cash) over the past few years. As of 3Q23, OLO had a net cash position of ~$360 million.

Strong secular tailwind

I believe OLO is well positioned to benefit from the longer-term secular trend of digital sales penetration in restaurants, with COVID having been a key catalyst. To give a basic background, digital orders refer to orders that are executed through a digital platform. For instance, a customer who orders food via the DoorDash app is placing a digital order. The same applies to a customer ordering from a digital kiosk in the store. These orders will flow from these consumer-facing digital fronts to the OLO platform, to the restaurant point-of-sale system, and then to the back-of-house to fulfill the orders as per normal. I believe digital ordering adoption accelerated during COVID, and this massive shift in consumer behavior is here to stay. Taking online food delivery services as a gauge for digital order penetration, digital orders are expected to grow to high teens in the coming decade. This far outpaces restaurant industry growth as a whole, which has typically grown at 0.5% over the past few decades.

{kind=link}

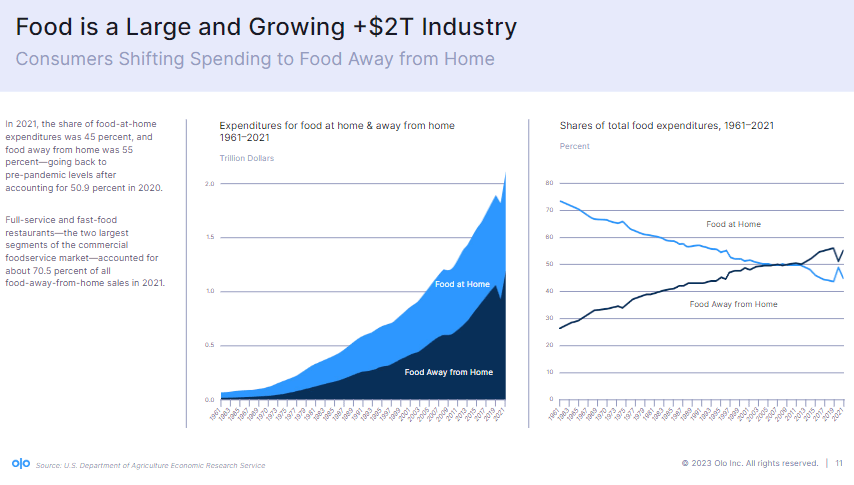

Moreover, there is another tailwind that is driving the entire industry and benefits OLO. More consumers are shifting their consumption habits away from home. This should continue to drive positive growth in the restaurant industry, which, coupled with increasing digital adoption, will increase the total addressable market for OLO.

{kind=link}

Strong value proposition to entire value chain

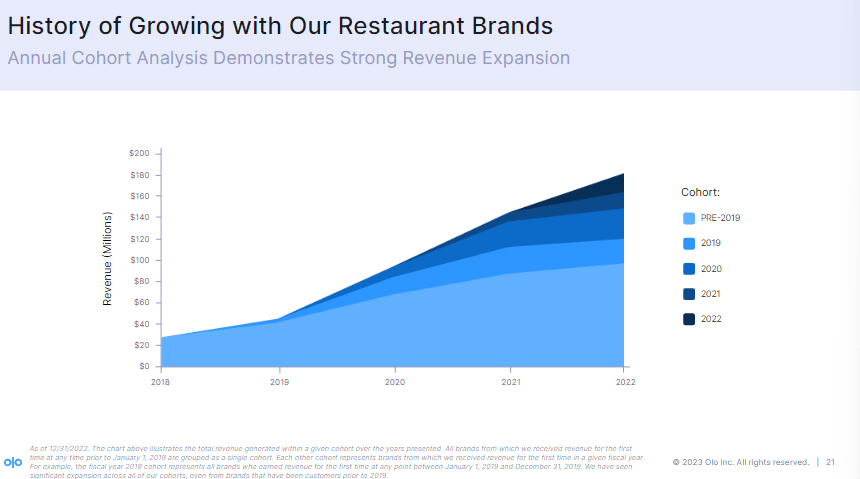

OLO offers a very strong proposition to its users across the entire value chain. Customers are able to order food digitally from their favorite restaurants, either via the restaurant’s website or 3P food delivery platforms. For restaurants, OLO enables them to tap into the growing digital preference of consumers and also improve their order execution metrics, such as order accuracy and time to completion, as the OLO platform facilitates all the data flow behind the scenes. All of these lead to a more positive customer experience, which drives recurring orders. At a deeper level, restaurants would also have a better understanding of their customers (order frequency, taste preferences, location data, etc.). All of these enable more efficient customer targeting, which translates to better unit/store economics. I think it is evident in OLO’s annual cohort analysis that it is making huge improvements to restaurants that are using its platform.

{kind=link}

As such, I believe OLO is a platform that is here to stay. In 3Q23, the stock reacted very negatively to the news that Wingstop ( WING ) will be leaving OLO platform once its contract expires at the end of 1Q24. This is big news as it is the 2 nd time WING lost a big customer (1 st was Subway ), which suggests that:

- WING can continue its digital strategy without OLO. Which means OLO might not be as mission-critical or sticky as it seems.

- Large enterprise restaurants can create their own platform, which increases the risk of further churn.

Although further churn among larger enterprises is a concern, my view is that the OLO value proposition remains very attractive. Remember that WING is a business that is growing at a rapid rate with sufficient financial capacity and resources to build its own technology platform. Also, digital strategy is a core part of WING’s business strategy. Hence, I think it makes sense for them to build their own technology platform for long-term benefit. However, this logic does not apply to all the restaurants. The fact that the OLO net retention rate accelerated to 119% (from 115% in 2Q23 and 107% in 3Q22) is a strong indication that churn is not a major issue. Moreover, as OLO continues to roll out more product modules (and successfully upsell them), I think it will make it more sticky and harder to rip out. As such, I don’t see this development as something that has structurally impaired my view of OLO's competitive advantage.

Olo Pay gaining traction

One underappreciated aspect of OLO is its payment module, Olo Pay. I believe this will become a large revenue driver in the medium term. From $49 million in gross payment value [GPV] in 2Q22, OLO has managed to drive it up to $347 million in 3Q23, implying a GMV penetration of 5.5%. This clearly indicates the strong underlying demand, and management highlighted that it is on track to exceed $1 billion GPV in FY23. This implies a 4Q23 GPV of at least $280 million, or ~2.8x the 4Q22 level. Chances are that OLO will outperform this $280 million given the festive season (more food away from home occasions). Management decision to increase its Olo Pay outlook to $25 million from the low $20s in 2023 was a strong sign, I believe, that the adoption of Olo Pay continues to outperform expectations. I expect adoption to continue increasing, as only 15% of industry-wide transactions are digital, implying a potential more than 6x addressable market once OLO rolls out its card-present functionality in 2H24.

“the $23 billion of GMV that we quoted last year being processed over the platform and you assume that, call it, 15% of transactions industry wide are digital, that means as card-present comes to market, we actually have a, call it, 6x opportunity”

Valuation

May Investing Ideas

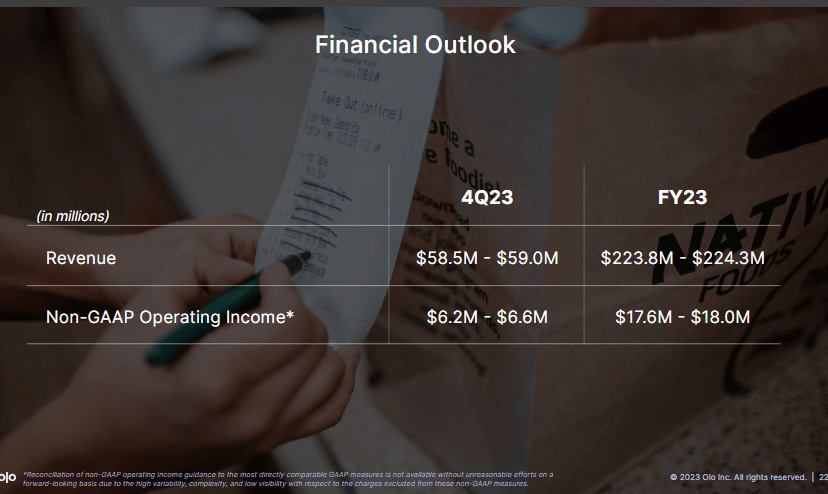

With my view on the industry, OLO value proposition, and OLO pay growth potential, I think OLO can easily sustain its current growth momentum of low-20%. I am basing my FY24 and FY25 21% growth rate against management’s FY23 revenue guidance. For valuation, I am using OLO's current forward revenue multiple of 2.25x in my model, which translates to a target price of $6.68 (17% upside). I note that my valuation assumption is to reflect the negative sentiment around the stock today, given the churn of WING on OLO’s platform. It will take some time for the market to realize that the OLO value proposition remains sound and that churn is not an issue (remember, the net retention rate is 119%). From a margin of safety perspective, 2.25x forward revenue is near the lowest OLO has ever traded. Even at this multiple, the upside is attractive.

{kind=link}

Risk

The churn of WING could signal a deeper issue than I expected. If WING is able to recreate a technology stack with a lower cost of capital that works perfectly fine, It could be a blueprint for other restaurants to eventually follow. This is a long-term risk that OLO needs to address by continuously rolling out more product modules (making itself more sticky). So long as OLO doesn’t give the restaurants a reason to leave, I think it will be fine.

Conclusion

In conclusion, I give a buy rating for OLO. I believe its strong position in the growing digital sales penetration within the restaurant industry, coupled with a robust value proposition and the potential of Olo Pay, should support its current growth momentum of low-20%. Importantly, the current valuation, near its historic low, presents an attractive entry point, especially considering the potential upside as market sentiment aligns with the company's true value proposition.

For further details see:

Olo: Large Industry, Strong Tailwinds And Value Proposition