ZEUS - Olympic Steel: Headwinds Ahead But This Stock Is A Winner

2023-12-23 00:12:40 ET

Summary

- A "Hold" rating is recommended for Olympic Steel, Inc.

- ZEUS stock has outperformed competitors and the market in the long term.

- ZEUS's balance sheet remains resilient, with a strong financial position and a very low risk of bankruptcy.

- This stock represents a valid solution to expose to bright long term prospects of steel market.

A "Hold" rating for Olympic Steel, Inc.

This analysis believes that the "Hold" recommendation rating for Olympic Steel, Inc. (ZEUS) is currently the most appropriate.

The company is a Highland Hills, Ohio-based manufacturer, distributor, and warehouse of metal products in the United States and abroad. This steel operator's stock is referred to as "ZEUS" or "Olympic Steel" in this analysis.

In the Long Term, ZEUS Outperforms its Competitors and the Market

The performance of ZEUS's U.S.-listed shares over the past five years compared to the overall U.S. stock market and the steel operator's industry shows that this stock has performed in a way that long-term shareholders can be pleased with. ZEUS's share price is up 325.80%, significantly outperforming the SPDR® S&P 500 ETF Trust (SPY), +97.27%, and the Materials Select Sector SPDR® Fund ETF (XLB), +75.91%. SPDR® S&P 500 ETF Trust ( SPY ) is the benchmark index for the entire U.S. stock market, while Materials Select Sector SPDR® Fund ETF is the benchmark index for the industry of ZEUS.

{kind=link}

This analysis considers the past 5 years to be sufficient time beyond a reliable stress test to base forecasts on possible future developments as this time range includes as many downsides as upsides in the share price of ZEUS. In particular, this range includes the financial fallout with the supply chain and business disruptions triggered by the COVID-19 virus-induced pandemic, as well as the impact of the conflict in Ukraine with the procurement of raw materials and fuels becoming more expensive for a while.

Long-Term Growth Catalysts for Olympic Steel's Markets

Some recessionary headwinds in 2024 could result in a decline in the share price and potentially create an opportunity to increase ownership as this company appears to be well aligned with the steel market growth. Despite a gloomy short-term situation, retail investors should continue to hold shares of Olympic Steel, as the very strong long-term outlook for the steel market will trigger a rapid recovery in the share price after recessionary headwinds in 2024.

ZEUS serves many metal-consuming industries with very strong long-term growth catalysts in global markets. ZEUS sells most of its products in North American markets, but the globalization and interconnection of markets undoubtedly mean that increased demand from abroad will inevitably have a positive impact on ZEUS as well, as its steel products can benefit from more robust pricing conditions. After all, one of the goals of technological development is the globalization of society and the economy.

Commenting on the sales results for the third quarter of 2023 , Chief Executive Officer Richard T. Marabito attributes the growth opportunities of the ZEUS business to the long-term outlook for the US steel market in a favorable pricing environment.

He said: "We remain optimistic about the long-term outlook for the U.S. steel market and our business. As we finish another solid year, we are seeing a rebound in pricing."

The Asia-Pacific region, with its rapid industrialization and economic development as well as the electrification of all economic activities and transportation worldwide, as well as increased government spending on the expansion of clean energy supply infrastructure, will provide an amazing boost to the global steel market in the next decade.

The size of the global steel market, which analysts at Future Market Insights (fmi) estimate at $1.82 trillion in 2022, will be nearly $3 trillion in terms of sales in 2033, driven by significant growth in global demand for steel products. This growth in global demand for steel products is described as "significant" as global steel sales will show a higher growth rate of 4.4% per annum until 2033, compared to a slower annual growth rate of 1% over the past five years, including 2022.

The main drivers for consuming more steel products will be global strategic goals such as tripling renewable energy and doubling energy efficiency by 2030, as recently outlined in the Cop28 Global Stocktake endorsement at the United Nations Climate Change Conference in Dubai.

US President Joe Biden's administration aims to make at least 50% of all new vehicles sold in the US electric vehicles (EVs) by the end of 2030 and to build and strengthen the nationwide infrastructure with 500,000 chargers to make EVs available to a growing number of US citizens. The automotive industry is heavily dependent on steel as it uses the industrial metal for the fabrication of various components of the EV such as chassis, body frames and engine parts.

A growth catalyst for the steel market will come from the Chinese government's strategy to help the domestic economy recover from three years of strict measures against the COVID-19 virus. To keep the iron ore and base metals markets active, a series of measures to boost domestic industrial infrastructure will drive strong demand for steel products. This growth strategy is in line with the rapid industrialization and economic development of China, the world's second-largest economy and probably still the world's largest steel consumer, as the country accounted for a relevant share of Asia-Pacific demand in 2021.

The Last Few Years Have Been a Reliable Stress Test for ZEUS' Solid Financial Position

Olympic Steel, Inc.'s balance sheet has weathered a difficult past five years and remains resilient should the near-term future presents again some in challenges.

As of September 30, 2023, Olympic Steel had $14.5 million in cash and short-term securities, compared to total debt of $234 million. Following its acquisition in early October 2023 of value-added manufacturing services provider Central Tube & Bar , which serves original equipment manufacturers (OEMs) and other operators throughout the Mid-South, all debt is contained in a revolving credit facility.

The company also says it has $359 million to withdraw, which it considers sufficient to fund growth through additional acquisitions and initiatives that will increase the capacity and efficiency of operations.

Based on trends over the last 12 months, the debt doesn't appear to be particularly expensive. Despite the Fed's 11 interest rate hikes since March 2022 to combat elevated inflation, ZEUS's debt results in annual interest expense of approximately $4 million to $4.5 million. Against this expenditure, Olympic Steel was able to generate a twelve-month operating income of $20.9 million . The operating income is already five times higher than interest expense (investors believe the interest coverage ratio should be at least 1.5 times higher) and with the incorporation of CTB's high-margin "tubular and pipe" products business, the solvency of ZEUS is now better positioned to continue this trend in the future.

Plus, overall, ZEUS's balance sheet is robust from a solvency perspective, as demonstrated by its Altman Z-Score of 4.25 (scroll down to the "Risk" section on this page of Seeking Alpha ), meaning ZEUS is in safe areas. This suggests that the company's risk of bankruptcy within a few years is zero.

Trends in ZEUS Business Profitability and Growth Opportunities

In the first 9 months of 2023, the " Tubular and Pipe Products " segment of ZEUS produced an operating income of $29.1 million (approximately 36.2% of ZEUS's total operating income of $80.3 million over the same period), which was up 0.6% year over year. The "Tubular and Pipe Products" segment of ZEUS had net sales of $281.5 million (approximately 17% of ZEUS's total net sales of $1,668.8 million over the same period) which were instead down 17% year over year due to high-interest rates/increased inflation impacting the steel market. Thus, ZEUS' operating margin for the Tubular and Pipe Products segment was 10.3% of segment net sales compared to ZEUS' total operating profit margin of 4.8% of the company's total net sales.

If CTB's trailing twelve-month revenues were already in ZEUS's portfolio, they would have contributed approximately $40 million to the Tubular and Pipe Products segment of ZEUS's net sales, thus yielding more than 10.3% of ZEUS' segment's operating income margin in 9M of 2023 based on CTB's historical financial performance, as ZEUS indicates .

Fast Growing Indian Economy/Globalization of Markets Will Improve Market Price Dynamics for ZEUS Pipe and Tube Products Segment

The ZEUS Pipe and Tube Products segment is now in a stronger position to participate in the positive knock-on effects that the upturn in the fast-growing petrochemical plant construction market in India is expected to have on the expansion of the global steel pipe and tube market in the next several years.

Analysts at Grand View Research estimate that the global steel pipe & tubes market size will grow by more than 3.7% over the next seven years, from approximately $185.47 billion in 2022 to approximately $240 billion in 2030.

Growth Catalysts also from the US Petrochemical Industry

However, tailwinds for ZEUS pipe and tube products segment are expected to come from the domestic petrochemical market especially, other than from the strong growth in the Indian market through globalization and industry interconnection.

In response to OPEC's action against the Cop28 Global Stocktake's desire to usher in an era of zero dependence on fossil fuels, and in response to Russian retaliation for US and NATO support for the Kyiv government in the war in Ukraine against Russian forces, the US economy will increase investments in domestic energy infrastructure to supply more barrels of oil and offset the restrictive policies of OPEC and Russia in the coming years. This is intended to prevent Russia's supply shortage from exerting excessive upward pressure on the price of barrels, which would add to the drag on economic activity due to the recession expected in 2024.

As major oil producers such as Exxon Mobil Corporation ( XOM ) and Chevron Corporation ( CVX ) increase their production in line with the US government's strategy, they will need to do so using ad hoc technologies, so the ZEUS segment will benefit from this need for more steel pipes & tubes for transportation and other operational purposes driven by increasing investment in oil production by U.S. industry.

ZEUS' other two segments have performed as follows over the past 9 months through Q3 2023 and will benefit from highlighted growth catalysts:

Growth Catalysts for ZEUS's Carbon Flat Products Segment

The Carbon Flat Products segment sold 651,758 tons of products (up 5.2% YoY) at $1,444 per ton (down 17.6% YoY) and generated operating income of $30.6 million (up 12.5% YoY) from net sales of $941 million (down 13.4% YoY). The segment operating income was 38% of ZEUS's total operating income of $80.3 million over the same period. The segment's net sales were 56.4% of ZEUS's total net sales of $1,668.8 million over the same period. The Carbon Flat Products segment's operating income margin was 3.3% of the segment's net sales (up 80 basis points YoY) compared to ZEUS' total operating profit margin of 4.8% of the company's total net sales.

Experts at Verified Market Research see significant growth in the global carbon flat steel market during 2023-2030 at a CAGR of 3.17% from $437 billion in 2022 to $562 billion in 2028, with the construction and automotive industries and increasing industrialization worldwide being the main drivers.

Due to its low maintenance and construction costs as well as its flexibility and high strength properties, customers' awareness of the advantages of using more and more flat carbon steel is growing, according to the report by the experts mentioned.

Also, this analysis believes that: home-building is a major consumer of these products, and given the strong outlook for the US home-building industry, the merger will provide a tailwind to the ZEUS segment. Housing construction in the US is expected to be on a strong growth trajectory. Higher borrowing costs, which are reaching historic levels due to the Fed's hawkish stance, are causing consumers to postpone mortgage-based or mortgage-refinanced home purchases, leading to two problems: Shrinking inventory of homes for sale and high selling prices. To replenish inventory, make selling prices more affordable and also stimulate the entire real estate sector, house builders are encouraged to construct new houses. This will be good for the demand for ZEUS products.

Growth Catalysts for ZEUS's Specialty Metals Flat Products Segment

The Specialty Metals Flat Products segment sold 89,163 tons of products (down 19.7% YoY) at $5,006 per ton (down 9.6% YoY) and generated operating income of $20.6 million (down 76% YoY) from net sales of $446.3 million (down 27.4% YoY). The segment's operating income was 25.7% of ZEUS's total operating income of $80.3 million over the same period. The segment's net sales were 26.7% of ZEUS's total net sales of $1,668.8 million over the same period. The Specialty Metals Flat Products segment's operating income margin was 4.62% of the segment's net sales (down 931 basis points YoY) compared to ZEUS' total operating profit margin of 4.8% of the company's total net sales.

Olympic Steel associates the decrease in sales volumes from this segment with an overall decline in the market demand for stainless steel. Sales volumes for flat specialty metal products are still below pre-pandemic levels of 111,389 tonnes in 2019 as they still face the headwinds of a sharp downturn in the global market from 2019. It must be said that these headwinds are impacting ZEUS's revenues, but most likely other operators as well. Net sales of ZEUS' Specialty Metals Flat Products segment are expected to return to an upward trend as the global market continues to recover to pre-pandemic levels.

However, the future promises improvement.

The specialty steel market size is estimated to grow from $223.45 billion in 2022 to $271 billion in 2030, rising at a CAGR of more than 2.45%, as indicated by a report from Verified Market Research.

The automotive, aerospace, and railway industries will drive the growth of the industry. Concerning the automotive and infrastructure sectors including transport, growth catalysts have already been described above.

The aerospace and defense industry has robust growth prospects as well: Geopolitical disputes and existing conflicts between countries increase the sense of uncertainty in Western countries and even in the United States. In response, governments are increasing their spending on armaments and various bulwarks against external (including cybernetic) attacks. ZEUS segment will benefit from the growth engine of continued global weapons proliferation around the world, but especially in the United States, as the country is home to the world's largest manufacturers of space technologies and weapons. The sharp increase in US military budgets in recent years and near-record sales of US weapons provide forecasters with a good indication of the current trend.

The Looming Recession Will Delay Sales Strong Recovery to Pre-Pandemic Levels After 2024, but Will Drive Shares to More Attractive Entry Points

This analysis assumes ZEUS sales will improve in 2024, albeit more moderately, while these economists expect the economy to be gripped by a recession next year: Michael Pearce , Chief US Economist at Oxford Economics, Chryssa Halley , Chief Financial Officer of the US Federal National Mortgage Association (Fannie Mae), and David Rosenberg , Economist at Rosenberg Research. Also, former US Treasury Secretary Larry Summers predicted that the next economic cycle would be a recession as early as 2024, and Luke Tilley , Chief Economist at Wilmington Trust, says that the US economy is not recovering but weakening, which will soon be clear to everyone, implicitly indicating an economic recession.

The view of these economists is also confirmed by the inverted yield curve for the 10-yield to 3-month US Treasuries' spread (3.88% for 10-year Treasury notes versus 5.407% for 3-month Treasury notes at the time of this writing). If the yield on shorter bonds which usually carry less risk to compensate for relative to riskier/longer bonds, instead exceeds the yield on longer bonds, it is because bondholders experience the outlook as more uncertain than before. Therefore, they prefer either to shorten the time their money stays in the hands of borrowers or to purchase money market instruments.

The Federal Reserve has been sending recession signals since March 2022 when it began its fight against elevated core inflation by raising the federal funds rate. The higher borrowing costs combined with the elevated inflation weigh on consumption and investment, which are the pillars of the economy. The Federal Reserve's key interest range rate is currently 5.25% to 5.5% , but rate cuts are likely to occur starting in 2024, lowering the range by 75 basis points by the end of next year. This does not mean that the threat of recession is over, but rather that a "Higher for Longer" stance is considered appropriate so that core inflation will return within the 2% target. But core inflation remains well off target as it currently stands at 4% . For the Fed to win the battle, both consumption and investment will need to show further signs of damage, with very clear trends for a decline in consumption and a slowdown in business transactions for investment emerging in the third quarter of 2023.

Consumption Is Showing Signs of Recession

When it comes to negative trends in consumption (it accounts for nearly 70% of U.S. gross domestic product), these well-known U.S. retailers are sending a very telling message as their sales and same-store sales have generally declined and they have lowered their forecasts for future sales in the face of gloomier demand.

Best Buy Co., Inc. ( BBY ), a specialty retailer of technology products such as computers and cell phone products in the United States and Canada, reported revenue that came in $140 million short of expectations in the third quarter of fiscal 2024 (ended October 28, 2023). Revenue dropped 7.8% year-over-year to $9.8 billion.

Burlington Stores, Inc. ( BURL ) - the fashion-focused branded clothing retailer known as off-price stores in the U.S. issued a gloomy outlook for Q4- 2023 (ending January 30, 2024): Management expects total revenue to go up 5% to 7% to $2.88 billion to $2.93 billion in Q4 FY 2023, disappointing the consensus, as the consensus instead forecasts $3.03 billion (a significantly higher increase of 10.6% from Q4 FY 2022).

DICK'S Sporting Goods ( DKS ) - a specialty retailer primarily focused on sporting goods in the United States - reported that same-store sales move up 1.7% for the three-month period ended October 28, 2023, which was below growth of 6.5% for the same period in 2022.

Kohl's Corporation ( KSS ) - a department store that offers branded apparel, footwear, accessories, beauty, and home products through its stores and websites in the United States -- posted an 11.2% sales decline in the Q3 of the FY 2023 (ended Oct. 28, 2023), to $3.8 billion. KSS has less confidence in near-term demand as its inventory of $4.2 billion shrank 13% year-on-year in Q3 FY 2023.

Nordstrom, Inc. ( JWN ) - fashion retailer of apparel, footwear, beauty, accessories, and home goods for all ages, females and males - had a 6.5% year-over-year loss in revenue to $3.32 billion in its Q3 FY 2023 (ended October 28, 2023) short expectations by $100 million. For JWN's full fiscal 2023 outlook, revenue is foreseen to decline 4% to 6% from $15.53 billion in fiscal 2022 to a range of $14.6 billion to $14.91 billion, while consensus is for $14.75 billion.

Lowe's Companies, Inc. ( LOW ) - a home improvement retailer in the United States - posted a 12.8% decline in sales to $20.47 billion in the Q3 FY 2023 that ended November 3, 2023, which was $390 million below expectations. The company reported a 7.4% drop in comparable sales, driven by a drop in consumer discretionary spending. The full-year 2023 outlook includes that comparable sales are foreseen to be 5% lower year-over-year, compared to the previous forecast of -2% to -4%.

Investments Activities Are Showing Signs of Recession

In terms of negative investment trends, Morgan Stanley's ( MS ) Q3 2023 IPO and M&A data is very informative as IPO proceeds have cooled significantly and M&A has also been lower year-on-year.

When going public on the US market, it is also important to note that the number and value of deals are still well below 2021 levels. The bleaker outlook for future demand is discouraging companies from raising investment capital through IPOs, which is reflected in the poor statistics for IPOs in the US market .

Unemployment Will Increase

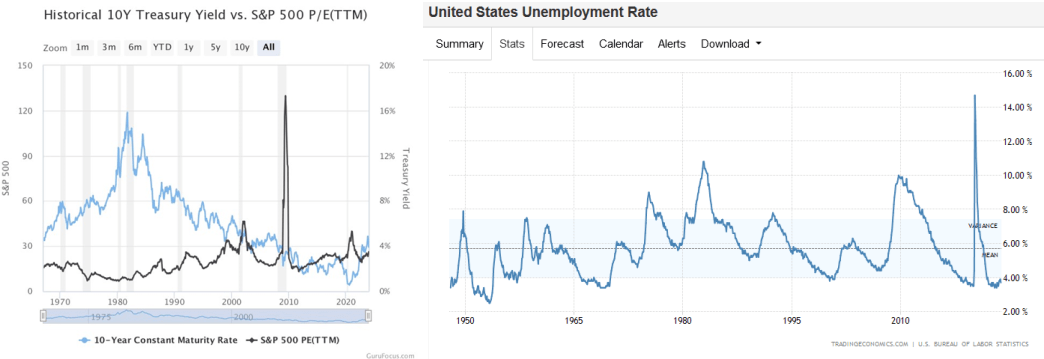

As soon as these negative trends in consumption and investment are accompanied by an increase in unemployment, it is a recession in the true sense of the word (according to the books about economics), contradicting those who still stubbornly support the thesis of soft landing today, which has so far led to unjustified overvaluation in the stock market. Analysts who, despite all the problems, see a soft landing as the next scenario for the economy simply ignore the past: When comparing Guru Focus's "Historical 10Y Treasury Yield vs. S&P 500 P/E ((TTM))" chart with Trading Economics' "United States Unemployment Rate" chart, it appears that each of the eight recessions of the last 60 years is associated with a significant increase in the unemployment rate as the latter was well above the historical average of around 5.7%.

Source: GuruFocus for the chart on the left side, while the source of the chart on the right side is Trading Economics

{kind=link}

Additionally, when the following chart of the US Fed Interest Rate is included in the analysis, it shows that the Fed's aggressive rate hikes anticipated a recession in each of the last eight cases. Therefore, the latest rate hike must be followed by another recession as the Fed has taken an aggressively hawkish stance since March 2022, similar to the action implemented to weather the 2007-2008 financial crisis, to combat what has been the worst inflation in 40 years.

Source: Trading Economics

The rate is currently 3.7%, but there are signs that the number of unemployed will rise. As reported in this Seeking Alpha article , recent readings from Challenger, Gray and Christmas, Inc., the Automatic Data Processing, Inc., and the U.S. Bureau of Labor Statistics report on nonfarm pay growth in November indicated that working conditions are worsening.

Collective bargaining to adjust employees' wages and working conditions to the increased cost of living will inevitably become a burden for companies. To protect their profit margins, which are under pressure from reduced US household spending capability, companies will be forced to cut the number of workers in the coming months, starting with the most precarious and temporary jobs. During the industrial action by US employees of major automobile companies against their respective employers, former US President Donald Trump said that many workers would lose their jobs anyway. Perhaps the shift to more expensive production of electric vehicles compared to cheaper operations in China or emerging markets will be used as an excuse to lay off workers in the automotive industry, and others will be used as "reasons" to justify employer decisions in other sectors of the economy. What is certain is that when profits are at risk, the most outspoken shareholders will be at the forefront, demanding draconian decisions to defend margins. A reorganization of the workforce will inevitably be part of corporate strategies to defend the profitability of their operations, weakened by the impact of lower consumption and now also by the slowdown in the growth of prices for goods and services. The scenario will not be so different from the one described, since labor costs make up the largest part of companies' total operating costs. Despite headwinds from weaker spending trends and concerns that the Fed's rate hikes may have a larger-than-expected impact, analysts at Bank of America Corporation ( BAC ) early last month expected profits to continue to rise next year anyway. Reducing excess capacity is seen by analysts as a countermeasure with which companies want to achieve the goal of a leaner cost structure and support margins. Tech companies began laying off workers last year, but other sectors of the economy will follow suit.

Andrew Challenger, a labor expert and senior vice president of Challenger, Gray & Christmas, Inc., said two weeks ago that they "expect to continue to see layoffs going into the New Year".

Additionally, one of the most interesting aftereffects of the recession was the significant decline in the P/E ratio of the S&P 500 (see the chart above showing "Historical 10-Year Treasury Yield vs. S&P 500 P/E Ratio ((TTM)). If this decline occurs from current levels in the US stock market, which is overvalued due to bullish sentiment among tech stocks on AI hype and its disruptive benefits for all companies in various sectors, the knock-on effect on US-listed stocks could be such that will be remembered for a long time.

There is a Risk of a Lower Market Valuation in 2024, but not for the Dividend

The negative cycle will create headwinds in the financial markets. Under this influence, ZEUS shares could trade below current levels and fall enough with a 24-month beta of 1.42x (scroll down to the "Risk" section on this page of Seeking Alpha ), potentially creating attractive entry points sometime in 2024 to add to the holding and thus be better positioned to participate in the company's long-term growth prospects in the steel market.

For now, investors may want to maintain their holding in ZEUS, as a solid financial position will help this company continue to pay dividends.

In fact, dividends have continued to grow over the past year at a growth rate of 60.34% (versus the industry average of 4.21%), despite the recent decline in net sales across all segments due the aftermath of the pandemic and the combination of monetary tightening together with rising inflation, which weigh heavily on the steel market.

On December 15, Olympic Steel paid a quarterly dividend of $0.125/share, in line with the previous one, which at the time of writing is leading to a (forward) dividend yield of 0.76%, compared to the S&P 500's dividend yield of 1.46% .

Going forward, the balance sheet will provide the company with financial stability, which is not a small feat, as the near future still presents some challenges, which this analysis links to an impending significant slowdown in the US economic cycle, as some economists and the US Treasury inverted the yield curve and other economic trends are pointing to.

However, as some industry forecasts show, the recession is unlikely to have a real impact on demand for Olympic Steel's steel products while with regard to prices these are likely to hold up quite well thanks to the various growth catalysts already mentioned in this analysis.

Despite the high probability of a recession in 2024, Fitch Ratings has a neutral industry outlook and expects steel demand to continue to grow in most regions, indicating an increase in global consumption of 20 million to 30 million metric tonnes compared to 2023. Demand growth will be moderate in the US for ZEUS steel products, but it will still be growth compared to 2023.

The rating agency predicts that the profitability of steel operators in the US will improve: They will seek to meet more of the demand that would otherwise be met through imports, with a supply of higher value-added products that better meet market demands for electrification and greener technologies. And then prices should remain above historical averages and therefore consistent with the ZEUS CEO's vision for prices to remain robust.

While the company's profitability is unlikely to pay the price for the economic recession expected in 2024, fears of headwinds in financial markets will also impact ZEUS stock. Therefore, this situation offers investors an opportunity to increase their stake in ZEUS, which has everything it needs to continue outperforming the industry and market in the long term, driven by various industry growth drivers. Until then, however, the rating for this stock is "Hold."

The Stock Valuation

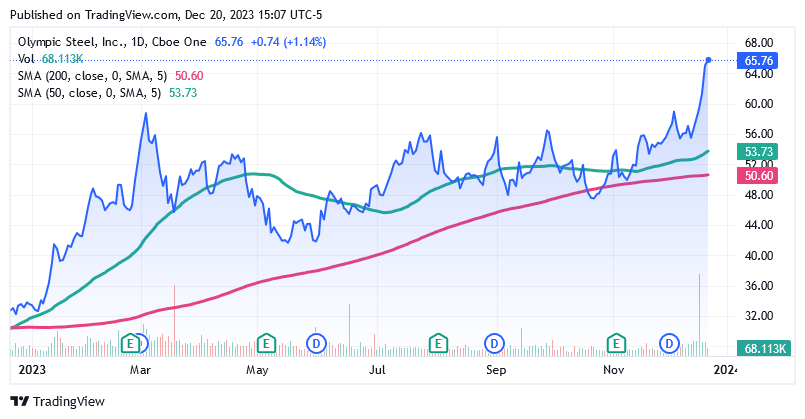

Shares of Olympic Steel, Inc. were trading at $65.76 per unit giving it a market cap of $723.84 million as of this writing (December 20,2023). Shares were trading significantly above the 200-day simple moving average ((SMA)) of $50.60 and significantly above the 50-SMA of $53.73.

{kind=link}

The levels now do not look the most attractive when comparing the current share price levels with its recent trends and also in light of the following comparison: the shares are also now significantly above the $49.11 midpoint of the 52-week range of $31.62 to $66.60.

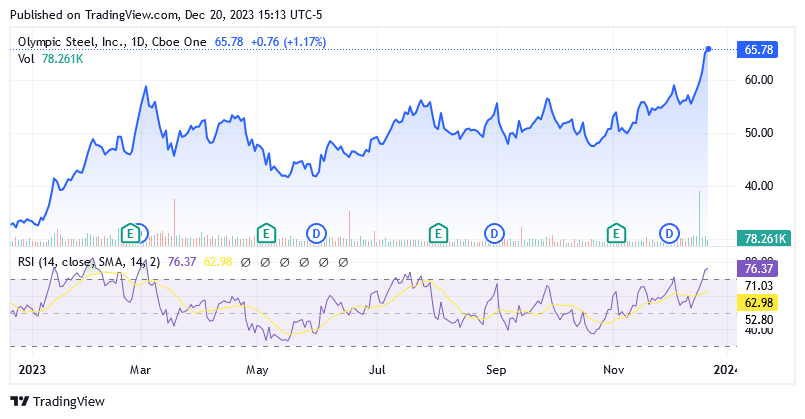

The 14-day relative strength indicator of 76.37 says shares are close to overbought levels and that the good scope to the downside along with the 24-month beta of 1.42x means there is a risk of a significant pullback from these levels should recessionary headwinds begin to blow on US-listed shares.

{kind=link}

Furthermore, this market valuation of ZEUS shares does not appear attractive based on the EV/EBITDA ((TTM)) ratio of 9.36x, which is higher than the industry average of 9.30, nor is it based on a comparison with Aswath Damodaran's valuation.

Aswath Damodaran is a professor of corporate finance and equity valuation at New York University's Stern School of Business. Aswath Damodaran points out that companies operating in the iron and steel industry should have an EV/EBITDA of not more than 4.24x to be considered fairly valued. This analysis therefore suggests taking advantage of the looming headwinds of recession and trying to buy shares of ZEUS not now but when they will show more attractive valuations.

Let's look at ZEUS's valuation compared to its most direct competitors, which according to Seeking Alpha are the following: Haynes International, Inc. (HAYN), Ramaco Resources, Inc. (METC), Schnitzer Steel Industries, Inc. (RDUS), SunCoke Energy, Inc. ( SXC ) and Algoma Steel Group Inc. (ASTL).

Based on EV/EBITDA ((TTM)), which is considered by investors to be a very suitable measure of profitability for capital-intensive industries, including steel, Olympic Steel is not the most attractive stock at the moment, but looking ahead to 2024, there will be some great opportunity with a lower share price, thus supporting the "Hold" rating thesis for the time being.

Haynes International, Inc.'s EV/EBITDA ((TTM)) is 10.59x; Ramaco Resources, Inc. ratio is 7.35x, Schnitzer Steel Industries, Inc. ratio is 11.73x, SunCoke Energy, Inc. ratio is 4.93x and Algoma Steel Group Inc. ratio is 5.52.

Conclusion

Olympic Steel, Inc. is a good solution to participate in the long-term growth prospects of the steel market, which are promising. Driven by the positive upward long-term trend in the steel commodity market, this company's shares are demonstrably outperforming the industry and the overall stock market. But recently, the aftermath of the pandemic crisis and the tight monetary policy to combat inflation have not allowed ZEUS to develop sales very well. Due to the bullish sentiment driven by tech stocks and the Fed's interest rate break in mid-December 2023, the current market valuation may not reflect fair value relative to the company's ability to generate revenue. This ability is influenced by macroeconomic factors and not business factors, which is also important to emphasize. ZEUS revenue is expected to improve in 2024, driven by moderate growth in demand for steel products and robust pricing conditions, as discussed in this article. This scenario bodes well for the value of ZEUS. Here's the opportunity: With a looming recession, investors may want to capitalize on the strong possibility of more attractive entry points to increase their exposure to the steel industry's growth prospects through ZEUS. For the time being: Investors should continue to hold this stock for now and benefit from a dividend that seems safe given the financial stability of ZEUS' balance sheet and a strong future for the company's steel products sales beyond the recession.

For further details see:

Olympic Steel: Headwinds Ahead, But This Stock Is A Winner