OFLX - Omega Flex: Boring Stock Facing Temporary Headwinds But Valuation Still High

2023-08-23 05:27:53 ET

Summary

- Omega Flex has seen a significant reduction in volumes due to deteriorating demand for new construction projects.

- The company remains highly profitable as margins are high.

- Demand is expected to remain weak, but headwinds are likely temporary as they are directly linked to the current macroeconomic landscape.

- OFLX enjoys a strong, debt-free balance sheet.

- The recent decline in the share price represents a good opportunity for long-term conservative investors, but I strongly advise averaging down as the P/E ratio is still high at 35.63.

Investment thesis

Omega Flex ( OFLX ) has managed to increase its sales over the years thanks to the launch of new products, but recent quarters showed a significant reduction in volumes caused, among other reasons, by a decrease in residential construction projects. Added to the supply chain issues and inflationary pressures suffered in recent quarters, this volume decline has caused a further deterioration in profit margins due to unabsorbed labor, but still, the company remains highly profitable as its profit margins are very high.

With demand not expected to pick up soon due to high interest rates and even a potential recession, the share price has fallen by 56%, but despite this, the P/E ratio is still high at 35.63 (compared to a sector median of 19.74). This can be explained by several reasons. The company enjoys a debt-free balance sheet, and insider ownership is very high, which provides a certain sense of security to investors as the management are active shareholders. Also, the company is highly profitable as profit margins are very high, and the industry in which it operates is essential and (arguably) simple . For these reasons, I believe that the recent share price could represent a good opportunity for very conservative long-term dividend investors, but averaging down is currently, in my opinion, the only way to invest in Omega Flex with reasonably reduced short and medium-term volatility risks.

A brief overview of the company

Omega Flex is a leading manufacturer of flexible metal hose (or corrugated tubing) used to carry gases and liquids within their particular applications, including fuel gases within residential and commercial buildings, gasoline and diesel gasoline for automotive and marina refueling or back-up generation, medical gases and pure gases for the medical and pharmaceutical industries, and industrial applications. The company also sells its proprietary fittings and a wide range of accessories.

Omega Flex was incorporated in 1975 as a subsidiary of a Japanese manufacturer, and its market cap currently stands at $820 million. Despite its large market cap, insiders own a whopping 38.16% of the company's shares outstanding, which means the management is the main beneficiary of the good share performance.

Omega Flex logo (Omegaflexcorp.com)

{kind=link}

The company is very profitable as its margins are very high while capital expenditures are very low, but its valuation is very high as it has managed to grow over the years without using debt by launching products on the market and expanding its customer base as the company currently serves slightly over 10,000 customers, and although its operations are characterized for their great stability, the share price has dropped significantly in the last few quarters due to a noticeable weakening in demand, especially regarding home construction projects.

Currently, shares are trading at $81.36, which represents a 56.45% decline from all-time highs of $186.80 on February 1, 2021. Despite this, the company currently trades at a trailing-twelve months' P/E ratio of 35.63 as profit margins remain very high and risks are very low thanks to a strong balance sheet. For this reason, it is important to invest with caution, because although it might seem that investors are pessimistic due to such a significant share price decline, they rather seem to be cautious due to the high valuation of the company coupled with a current complex macroeconomic context, so shares could continue declining in price if prospects don't improve soon.

Revenues are weakening due to declining volumes

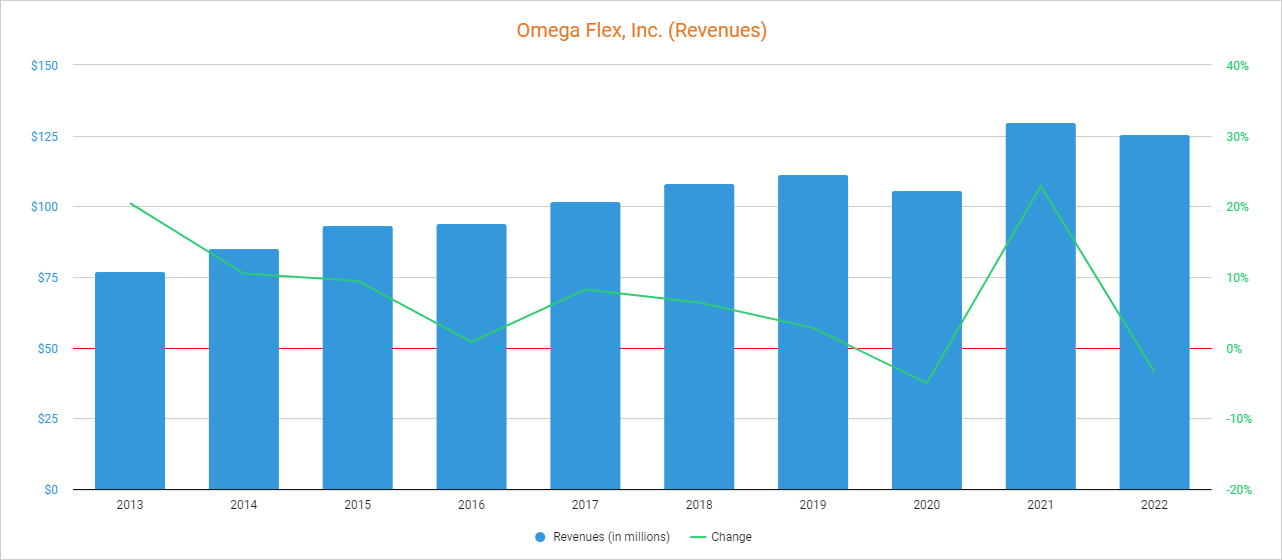

The company has managed to increase its sales over the years as it has released new products in order to expand to new markets. In 2013, it launched AutoSnap, which is a flexible gas piping product and, in 2018, it launched MediTrac, a corrugated medical tubing product. Although the coronavirus pandemic caused a 5% decline in revenues in 2020, they recovered in 2021 as they increased by 22.89%, and stabilized at a high level in 2022 as they declined by 3.48% (but were still 12.66% higher than those revenues of 2019).

Omega Flex revenues (Seeking Alpha)

{kind=link}

Nevertheless, revenues declined by 4.17% year over year during the first quarter of 2023, and by 18.62% (also year over year) during the second quarter strongly impacted by a significant decline in housing starts. Furthermore, current high interest rates suggest that demand should not return to those levels of 2021 and 2022 in the short-to-medium term, so sales are expected to remain relatively weak for a while. Even so, this weakening in demand is, in my opinion, of a temporary nature as it is caused by headwinds directly linked to the current macroeconomic landscape.

But even with the recent decline in sales, the P/S ratio has dropped significantly to 6.944, which means the company currently reports trailing twelve months' revenues of $0.14 for each dollar held in shares by investors. Still, this ratio still doesn't reflect the full impact as trailing twelve months' sales still reflect strong quarters prior to the last one.

Despite being such a high ratio compared to what investors are used to when looking at other companies in the industrial sector, this ratio is 1.15% lower than the average of the past 10 years and represents a 60.66% decline from the recent spike of 17.65 reached at the beginning of 2021, which means investors have been reducing the value they place on the company's sales as growth prospects have been diminished due to the current economic situation while profit margins have been affected not only by supply chain issues and inflationary pressures but also by unabsorbed labor derived from the declining volumes.

The company is highly profitable despite recent margin contraction

Historically, the company's operations have remained very profitable over the years, but margins have recently started to decline due to inflationary pressures, supply chain issues, and declining volumes as the trailing twelve months' gross profit margin currently stands at 61.58%, and the EBITDA margin at 25.53%.

As for 2023, profit margins have continued to deteriorate due to declining volumes as the company reported a gross profit margin of 61.16% during the second quarter, and an EBITDA margin of 22.39%, both below current trailing twelve months' margins but partially offset by pricing actions. Despite this decline, the company reported cash from operations of $8.0 million, but inventories declined by $0.4 million and accounts receivable by $3.1 million while accounts payable declined by just $0.2 million, and the company reported a net income of $4.6 million. In this regard, the company's trailing twelve months' cash from operations currently stands at $23.83 million, which was boosted by some inventory usage in the fourth quarter of 2022, but cash generation should eventually decline, as inventories are very limited, for as long as margins and sales remain weak.

Nevertheless, the company's cash from operations can be used almost exclusively for dividend payments as the company's balance sheet is debt-free and capital expenditures are very low at ~$1 million per year, which makes Omega Flex a very safe investment in my opinion. It is due to a strong balance sheet that the valuation is high despite recent operational weakening.

A very strong balance sheet dramatically reduces the investment risk

Since the company has no debt, it has no interest expenses to cover at the end of each period, and the balance sheet is very strong as cash and equivalents currently stand at $39.88 million while inventories are still at relatively high levels compared to the past at $17.38 million. Still, these inventories are significantly lower than the inventories of $21.8 million reached during the third quarter of 2022, which means that cash from operations should be lower in the foreseeable future until demand and margins stabilize at healthier levels.

In this sense, a strong balance sheet with no debt makes it possible for Omega Flex to be seen as a company whose dividends are subject to a very low risk of being cut or cancelled, which makes it a good investment, in my opinion, for very conservative investors. And I say very conservative because the dividend yield is low and, despite potential special dividends a regular dividend with the potential to grow significantly over the years due to high margins that should allow future raises potential short-term (regular), dividend returns are limited due not only to this low dividend yield, but also due to the conservative nature of the management. However, investors can expect more special dividends during years of strong operational performance.

The dividend is safe as the cash payout ratio is relatively low

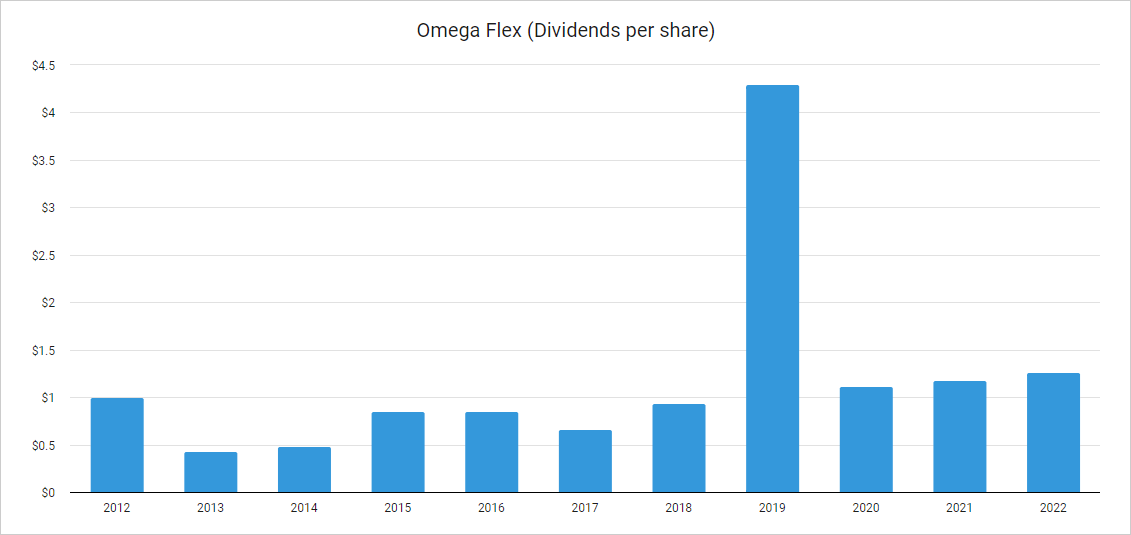

Until 2016, the company paid special dividends at the end of each year based on operational performance, but in 2017 it introduced a regular quarterly dividend of $0.22. Since then, the company has increased the quarterly dividend to $0.33, which represents a 50% increase from 2017 to 2023, but also paid a special $3.50 dividend in 2019, which would represent a 4.30% return at current share prices. The latest regular dividend increase was announced in June 2023 when the company announced a raise of 3.1%, which reflects the conservative nature of management as they seem to prefer to preserve cash as long as current headwinds continue to impact the company.

Omega Flex (Dividends per share) (Seeking Alpha)

{kind=link}

Despite these dividend increases and the recent drop in the share price, the dividend yield currently stands at a modest 1.63%, which is still 49.54% higher than the average of 1.09% during the past 5 years (excluding the special dividend of 2019).

In my opinion, said low dividend yield can be explained by the fact that the dividend is seen as a very safe one as the company has high profit margins and no interest expenses to cover, which allows a relatively low cash payout ratio. In the following table, I present the cash payout ratio (the percentage of cash from operations allocated for regular dividend payments) that the company has reported in recent years, excluding the 2019 special dividend.

| Year |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| 2021 |

| 2022 |

| Cash from operations (in millions) |

| $18.0 |

| $21.1 |

| $16.0 |

| $19.3 |

| $25.1 |

| $15.2 |

| Dividends paid (in millions) |

| $4.4 |

| $9.8 |

| $10.7 |

| $11.3 |

| $11.9 |

| $12.7 |

| Cash payout ratio |

| 24% |

| 46% |

| 67% |

| 59% |

| 47% |

| 84% |

As one can see, the company has historically allocated a relatively low percentage of cash from operations for the dividend payment, but the decline in cash from operations in 2022 has put some pressure on the dividend as the cash payout ratio increased to 84% due to lower cash from operations and higher dividends paid. Despite this, the recent cash from operations improvement to $23.83 million ((TTM)) should push the cash payout ratio to levels similar to those of 2020, and the company has high cash and equivalents, in case of a potential recession, to cover the dividend as long as current and potential headwinds continue to impact the company's operations, so I consider the current dividend to be safe.

Risks worth mentioning

Although the company has, in my opinion, a very low-risk profile thanks to high profit margins, a debt-free balance sheet, and a relatively low cash payout ratio, there are certain risks that I would like to highlight, especially for the short and medium term.

- Over 90% of the company's revenues take place within the United States and Canada, and almost the whole of the rest in the United Kingdom and France. In this sense, the company's geographical diversification is very low, and a significant housing downturn in North America could have a material impact on the demand for the company's products.

- If inflationary pressures continue to impact the company's operations, profit margins could continue to decline.

- Profit margins could continue declining if demand continues to fall as declining volumes could cause more unabsorbed labor.

- Due to the current complex macroeconomic landscape, both the company's operations and its share price are facing a period of high volatility, so the share price could continue to decline. This is why I strongly recommend adding small positions in order to average down if the share price keeps declining.

- The company may not pay special dividends for a significant period of time if operations remain weak as the management will likely prefer to preserve cash for as long as current and potential headwinds impact the company's operations.

Conclusion

Omega Flex is one of those companies suitable for the most conservative investors as it has a clean balance sheet and highly stable and profitable operations. To grow, the company does not require acquisitions or heavy investments, but it instead launches a new product every few years and introduces it to the market in subsequent years. But despite the historical stability of its operations, recent pricing actions have not been sufficient to contain the current margin contraction caused by supply chain issues and inflationary pressures as now volumes are declining due to weaker demand, which is having a significant impact on the company's ability to generate cash through its operations.

Despite this, I believe that the recent share price decline represents a good opportunity to start gradually adding shares to any conservative dividend portfolio and averaging down if the price continues to fall as the company is facing a complex macroeconomic landscape marked by high volatility and valuation is still high as the P/E ratio is at 35.63 (vs. a sector median ratio of 19.74). Taking advantage of the recent share price decline (and further potential declines) should allow for a higher dividend yield on cost in the long term. In this regard, Omega Flex is, in my opinion, what many investors would call a boring stock that should deliver modest (but safe) regular dividends with modest raises in the long term, and some special dividends along the way.

For further details see:

Omega Flex: Boring Stock Facing Temporary Headwinds, But Valuation Still High