VNQ - Omega Healthcare Has Problems: Is It Time To Sell?

Summary

- Omega Healthcare Investors, Inc. has a near-10% dividend yield and a BBB- credit rating.

- But Omega Healthcare Investors is facing growing problems that could put the dividend and credit rating of the company at risk.

- We would avoid Omega Healthcare Investors, Inc. stock and invest in other REITs instead.

Omega Healthcare Investors, Inc. ( OHI ) is a very popular real estate investment trust ("REIT") because it is one of the highest-yielding investment-grade-rated companies.

It pays a near 10% dividend yield and it has a BBB- rated balance sheet.

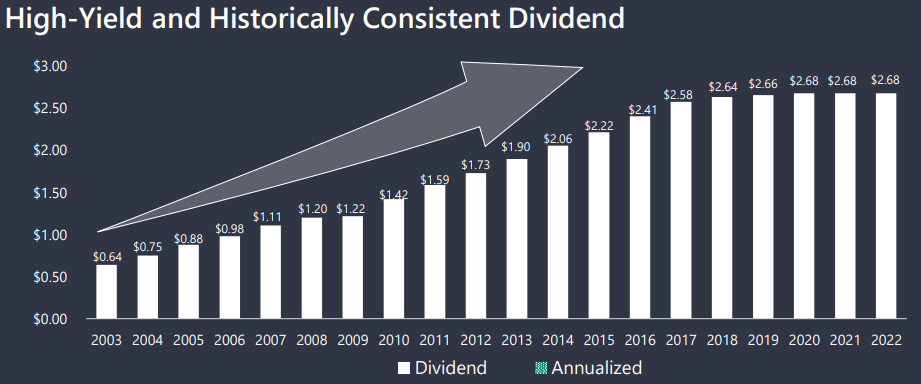

Moreover, OHI has also grown its dividend for 20 years in a row, which would suggest that its dividend is safe:

{kind=link}

But is it a good buying opportunity today?

I don't think so, and here's the simple reason why:

Over the past year, OHI has massively outperformed the rest of the REIT sector ( VNQ ), and that's despite facing more challenges than your average REIT.

We think that the chart should be the other way around.

OHI should have underperformed , not outperformed. But since it didn't, it has now become overpriced relative to most other REITs.

OHI is a skilled nursing REIT, and this is one of the most challenged real estate sectors right now.

Omega Healthcare Investors

The pandemic and the high labor cost inflation has made it very difficult for the operators of these properties to turn a profit.

Already before the crisis, the rent coverage ratios were very low because these are higher cap rate / higher risk properties, but now rent coverage ratios are even lower, leaving no margin of safety.

The EBITDAR coverage is just above 1x on average, which means that many are below 1x, which means that they cannot afford to pay rent:

Omega Healthcare Investors

Therefore, the risk of lease defaults and missing rents is now particularly high.

In the third quarter of last year, Omega Healthcare Investors, Inc. already had some difficulties, as it failed to collect rents from 12% of its tenants.

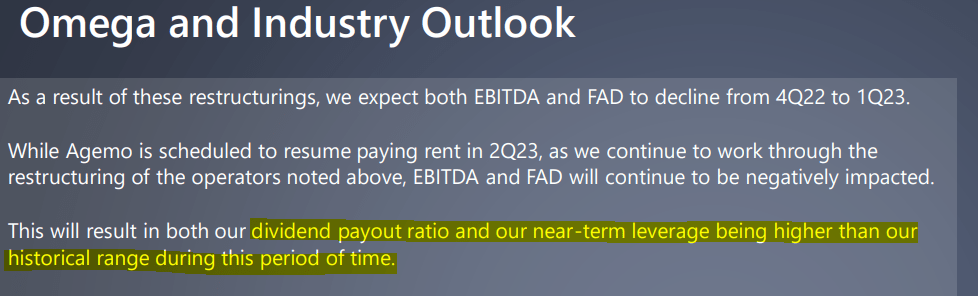

And just now, the company issued a warning that it is facing more problems related to its operators' ability to pay rent and mortgage obligations on time. As a result, its cash flow will be lower in Q1 than in Q4.

Their most recent investor presentation also says that the impact "will result in both our dividend payout ratio and our near-term leverage being higher than our historical range during this period of time."

{kind=link}

And the issues don't stop there.

Already before facing these issues, OHI's dividend payout ratio was too high at 92%. Now, it could exceed 100% in the near-term, putting the financial health of the company at risk.

I fear that this could cause credit rating agencies to downgrade OHI to junk. Omega Healthcare Investors, Inc. currently has a BBB- rating, which is lowest investment grade rating.

If it was downgraded, it would cause its interest expense to rise, only making the risk of a dividend cut even larger.

Now consider the following scenario

OHI isn't able to collect rents because many of its tenants are losing money. To resolve issues, it grants some rent cuts, which then increase its leverage, leading to a downgrade to junk, higher interest expense, and a dividend cut. This would then also hurt their market sentiment, potentially preventing them from trading at a premium to NAV, which would also hurt their external growth prospects for a long time to come.

That scenario is not improbable, and it would lead to significant capital losses in the near-term, especially since OHI massively outperformed the rest of the REIT sector in 2022.

I think that Omega Healthcare Investors, Inc. management should have already cut the dividend just to be safe, preserve some liquidity and protect its investment grade rating, but the management is reluctant to do so because it does not want to ruin its dividend track record:

Omega Healthcare Investors, Inc. is doubling down, hoping that it will be able to resolve issues, and return to growth, saving its dividend as well as its investment grade rating.

If it manages to do so, the returns could be significant, but is the potential reward worth the risk?

I say no.

If OHI was heavily discounted, perhaps it could be worth the risk.

But as we noted earlier, OHI actually outperformed other REITs in 2022, even as it should have been the opposite in my opinion.

It delivered a positive return even as most other REITs dropped by 30% and, as surprising as it may sound: most other REITs actually did a lot better than Omega Healthcare Investors, Inc. from a fundamental perspective. They grew cash flows and aren't facing the same challenges.

Now there are many other REITs that are offered at historically low valuations relative to OHI and so I just don't see the point of investing in OHI in light of its troubles.

If you are investing in OHI for its high yield, you should note that there are safer higher yielding options in today's market. A good example would be Global Medical REIT ( GMRE ), which specializes in medical office buildings (5x rent coverage), and yet, it yields 8%.

For further details see:

Omega Healthcare Has Problems: Is It Time To Sell?