OHI - Omega Healthcare Investors: Is The Dividend Sustainable?

2023-09-13 10:00:14 ET

Summary

- Omega Healthcare Investors, Inc. has seen its price rise over the last month while many REIT share prices have fallen over the same period.

- Part of this is due to the emerging signs of a recession, as historically healthcare has been a hedge during economic downturns.

- Omega Healthcare Investors combines an investment grade rating and a high yield which is not very common.

- Although they covered the dividend during last earnings, the payout ratio is above 90%, leaving no margin for error.

- Omega Healthcare Investors had 4 tenants on cash-basis including their largest tenant LaVie Care Centers.

Introduction

Omega Healthcare Investors, Inc. ( OHI ) is a popular stock amongst investors and for good reason. They offer a very high dividend yield over 8% considering the current macro environment. Bonds and CDs are offering investors a higher yield than most real estate investment trusts, or REITs, and OHI's yield beats them both. As rates have risen over the last few months so has OHI's price. They offer an appealing dividend of $0.67 a share that pays out on a quarterly basis.

But one thing I wonder is "Are investors chasing the yield or do they think the stock is a safe investment?" As a dividend investor, I typically have a further outlook on my stocks as I plan to hold them for the long term. But everyone is different and some may only want the yield for, say, 6-12 months. Or perhaps even less than that. The question is does OHI offer a safe dividend for the long term or could investors be walking into a yield-trap?

Business Model

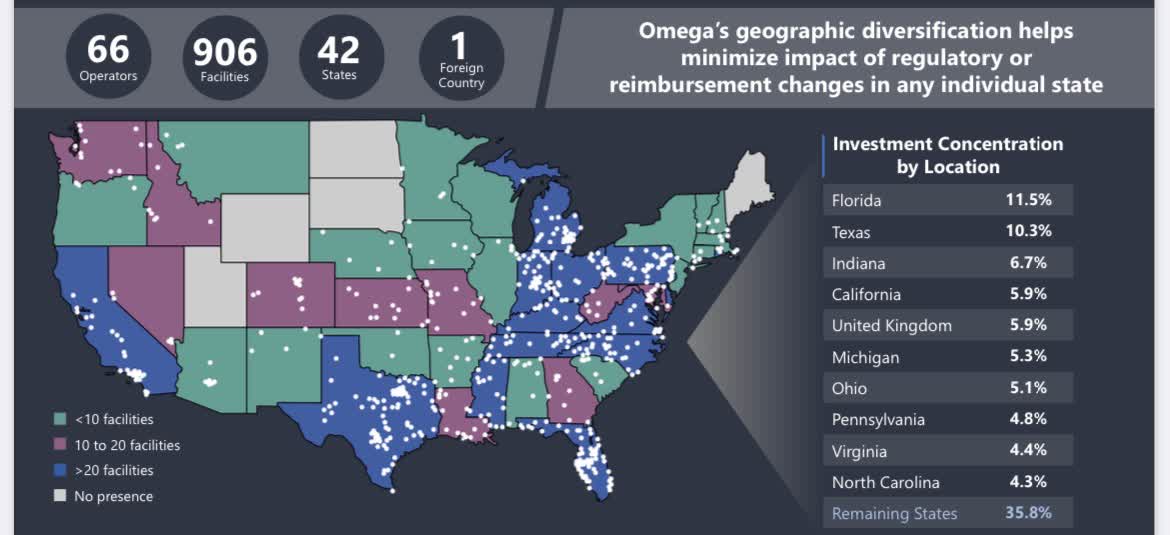

OHI is a REIT that invests in the healthcare industry with an emphasis on skilled-nursing and assisted living facilities. Its portfolio consists of a diverse group of healthcare companies, predominantly in the triple-net lease structure. They also have properties located in the United Kingdom. With a recession looking more likely, this could be one of the reason many investors have flocked into the stock, as healthcare is seen as a hedge during economic downturns.

{kind=link}

They have a higher concentration in Florida & Texas. The Southeast is a great geographical location for the company, as these are two of the fastest growing states in the U.S. Many states saw their population decline in 2020 & 2021, when COVID death rates were high. Another reason residents moved is the lower cost of living and lower/absent income taxes in most Southern states. It's safe to say people won't be moving back to their previous homes of record anytime soon.

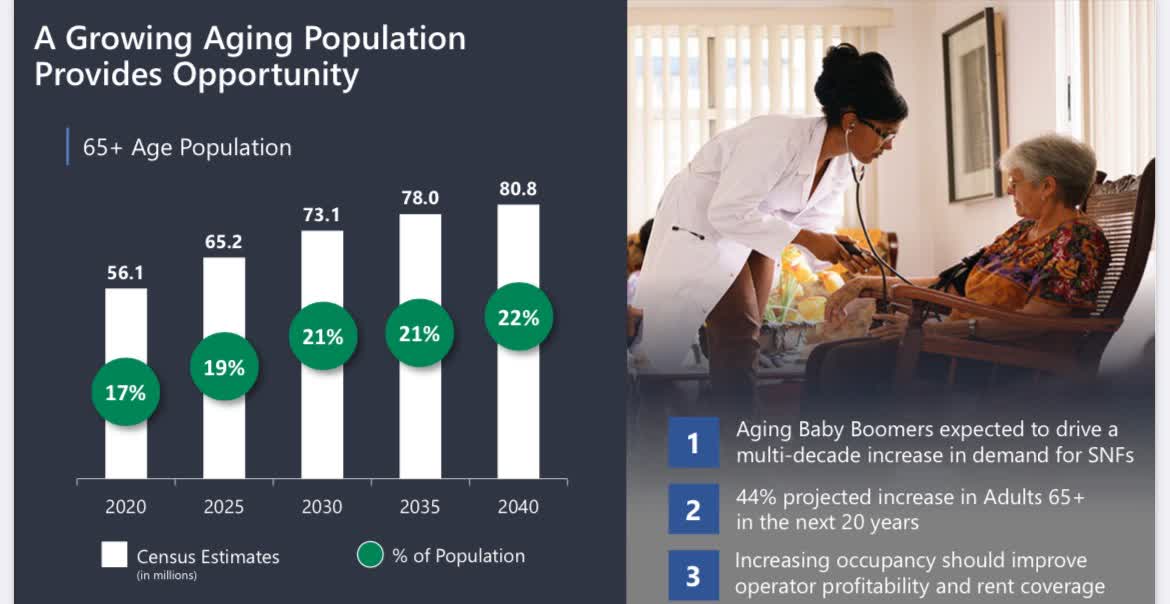

So OHI will continue to benefit from this as more people move South, making way for a growing aging population. Thus continuing to provide opportunity for the healthcare REIT. As seen below, aging baby boomers are expected to drive a multi-decade increase in demand for skilled nursing facilities, with a 44% increase projected in adults 65+ in the next 20 years. This is expected to improve profitability.

{kind=link}

People are living longer with chronic diseases due to continued innovation in medical therapies. With an aging population, the need for more skilled nursing facilities will most likely arise, thus creating more leasing opportunities for OHI and its peers. At the end of Q2 occupancy stood at 79.6%, up 6.7% from a year ago, but still below its historical average. OHI still may be feeling the effects of COVID as their occupancy rating was higher pre-pandemic at 83.4%. This may be due to the higher mortality rates among older people during the height of the pandemic.

A company's occupancy rating is a very important metric I feel many investors overlook when investing in REITs. I like to see somewhere upward of 95%, but the higher the better, obviously. As previously mentioned, the REIT has seen its occupancy rate move in the right direction since 2021.

Financials & Dividend Coverage

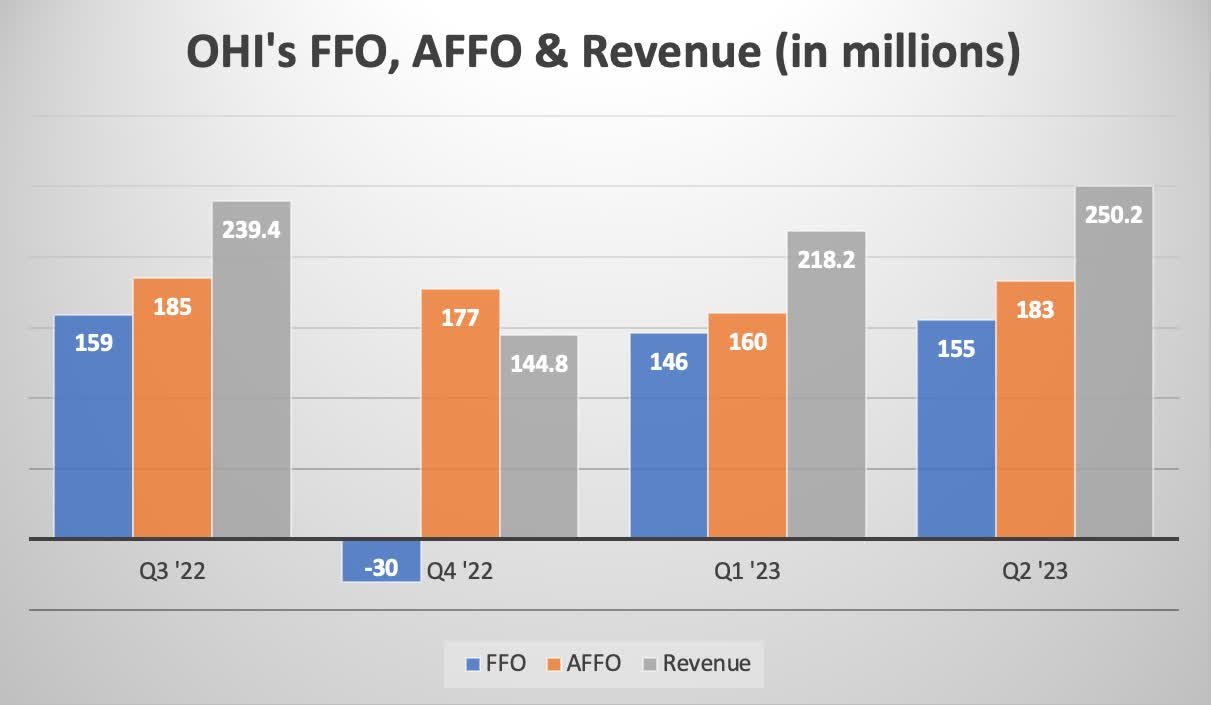

Below is a chart of OHI's financials for the last four quarters. With their occupancy slowly moving up, they should see some growth in the next few quarters. Although I like to see a nice ladder moving up and to the right (I call it the Stairway to Heaven), OHI has at least been able to cover its dividend of $0.67. They reported a loss of $30 million in funds from operations ("FFO") but were able to cover the dividend with reported AFFO of $177 million, or $0.73.

Also, OHI has not raised its dividend since 2019 but held steady when a lot of companies slashed their dividends. So, they do deserve some credit, especially with the headwinds the company has faced the last few years.

During that same period the company also saw their revenue drop to $144.8 million but it has since recovered. In comparison to 2022, the 1H of '23 has been relatively weak. Their CEO stated this came from incremental write-offs of straight-line accounts receivable and lease inducements as a result of placing 4 operators on a cash-basis for revenue recognition. One being their biggest tenant, LaVie Care Centers.

{kind=link}

During Q2 earnings OHI reported FFO of $0.63 and AFFO of $0.74. Revenue came in at $250.2 million, growing 14.6% from Q3 and by 4.5% from Q3 of '22. Management did say Q3 earnings may come in lower if incremental rents are received from those tenants placed on a cash-basis. OHI allowed their largest tenant LaVie to short pay rent by 66% in the third quarter. This should raise concerns with investors as this could potentially have a domino effect with other tenants within the portfolio. If your landlord didn't require your neighbor to pay their rent in full, why would you? Just food for thought.

I want to enjoy my dividends for a long time, and ways to ensure this are stable cashflows & a lower payout ratio. No dividend is guaranteed, but the more cash a stock has to cover it, the more likely they will pay a dividend long-term. This also means the company is retaining more cash flow to reinvest back into itself. REITs are required to pay out 90% by law, so it's not uncommon to see higher ones.

I consider OHI as at medium-to-high risk of a dividend cut. Their finances have been up and down, causing the payout ratio to increase over 90%, leaving minimal room for error. This is in comparison to its peers CareTrust REIT ( CTRE ) & Healthpeak Properties ( PEAK ) ,who both have lower payout ratios at 80% and 66% respectively. There are plenty of positive articles on this company and everyone has a different tolerance level or investment goal. But as a long-term investor, OHI is not my cup of tea. I understand it's very popular among income investors, but these next upcoming quarters will test the financial strength of the company even more.

Lease Expirations & Balance Sheet

Two things I do like about OHI besides the dividend yield are their balance sheet and well-laddered lease expirations. OHI does sport an investment grade rating of BBB- and offers a high-yield. Having both is not common for many companies. Furthermore, they have very minimal lease expirations throughout the next few years and no significant (expirations) until 2027. They also have a WALT of 9.3 years.

Moving onto the balance sheet. OHI recently paid $350 million in senior unsecured notes that were due August 1st and has no debt maturities due until 2024 with $400 million due in both 2024 and 2025. All of which is manageable for the company. 99% of their debt is fixed-rate with an adjusted EBITDA-to-debt ratio of 5.1x which decreased from 5.94x last quarter. I typically like to see 5 or less. But because of the business model of REITs it's not out of the norm to see above this. For example one of my absolute favorite REITs, Agree Realty ( ADC ), reported a net debt to EBITDA of 4.5x during its last quarter earnings.

Forecasted Growth & Tenant Risks

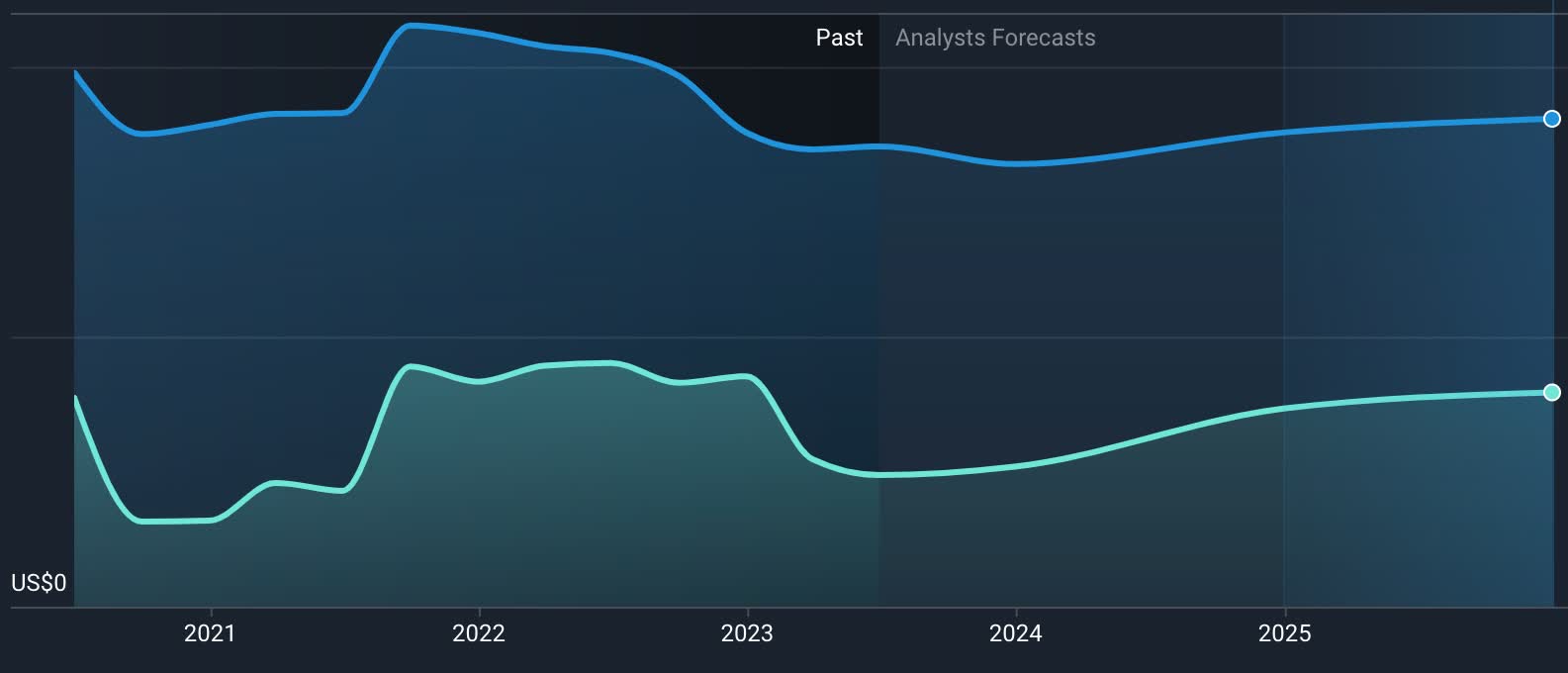

Revenue & earnings are expected to grow modestly over the next 2 years. Revenue is expected to grow 7% from the end of 2023 to 2024 and by less than 3% in 2025. During the same time, analysts are expecting earnings to post significant growth from '23 to '24 at 41.5% and lower in 2025 at 8%. But shareholders shouldn't be disappointed. Modest growth is still growth and better than no growth at all.

{kind=link}

I think OHI's biggest risk is their tenants. As mentioned earlier the company had 4 of their tenants on a cash-basis including their largest holding in their portfolio. During the second quarter, both LaVie and Maplewood short paid their rent. Because of this, OHI drew down on a $4.8 million security deposit to apply to any rental shortfalls next quarter. Additionally, both companies are in the process of restructuring their portfolio by releasing/selling certain underperforming facilities.

Investors should be aware of this and keep a close eye over the next few quarters, especially with rates to remain higher for longer and surging oil prices. This could push the economy into a recession, causing more tenants to default on their rents in the near-future. If so, this will cause a drop in revenue and cash flow, which may lead to a dividend cut in the near-term. Eventually leading to the REIT losing its investment grade rating, which would result in much higher interest expenses for a company who's having financial stress.

Valuation

I believe its yield is the reason OHI has seen its price increase as many investors are in search of high-yielding investments. With treasury rates at historical highs, many REITs have seen their prices drop during the same time. Both Realty Income ( O ) and Agree Realty are down over 5% while OHI is up over 3% in the last month. Because of this, the stock is trading close to its 52-week high of $33.16. I personally think the stock was a buy during the banking scare back in March of this year around $26. For me, the stock is a buy in that range as the REIT offers essentially no upside to its price target of $32.50.

{kind=link}

Conclusion

Because of its investment grade balance sheet and 8% yield, many investors have inflated the price of Omega Healthcare Investors, Inc. to near its 52-week high. There are some things to like about OHI. Stable healthcare industry, aging baby boomers, and solid balance sheet & lease expirations, but with their high payout ratio and constant tenant risks, investors should keep a close eye on OHI over these next few quarters. Especially with the promised higher for longer rates and surging oil prices. This could cause the economy to go into a recession and force more tenants into rent defaults. Because of this, I rate Omega Healthcare Investors, Inc. stock a hold.

For further details see:

Omega Healthcare Investors: Is The Dividend Sustainable?