SBRA - Omega Healthcare Investors: The Yield Exceeds 9.5% Q1 Dividend Has Been Paid Debt Looks Ok

2023-03-14 09:00:00 ET

Summary

- The high-yielding dividend from OHI appears to be safe as management addressed concerns around a dividend cut on the conference call.

- As rates rise and debt becomes more expensive, OHI doesn't have the same issues as others as more than 98% of their debt is fixed.

- I believe OHI will ride out the storm, and there is a long-term opportunity here while collecting a dividend that is more than double the yield of T-bills.

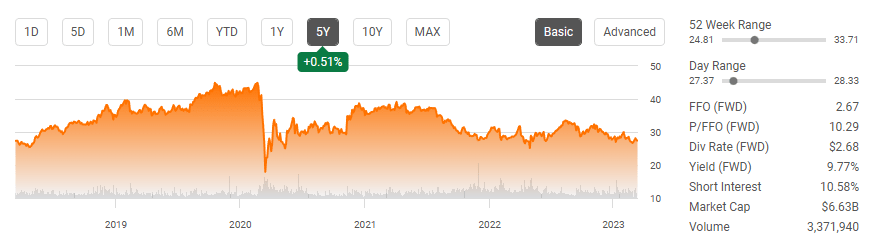

Here we go again, Jerome Powell was hawkish, and rates are going up. Sentiments about a soft landing and cuts on the horizon have been hindered after his testimony on the hill. With interest rates rising, sectors of the economy have been hit harder than others, especially companies with non-fixed debt. Real Estate Investment Trusts (REITs) have lost considerable value during the rising rate environment. The Vanguard Real Estate ETF ( VNQ ) has declined -22.67% over the previous year. REITs are also not as attractive for yield as they once were, as the 2-year T-bill yields 4.59%. One of my old faithfulls, Omega Healthcare Investors ( OHI ), is still dishing out a yield that is more than double the 2-year and has declined -4.42% in the past year and appreciated by 0.51% over the past 5-years. Over the past 5-years OHI has delivered $13.34 in dividend income which is 48.86% of its share price on 3/12/18 of $27.30. I believe my capital is safe in OHI, and no matter what has been thrown at them, the dividends keep coming.

{kind=link}

OHI doesn't have the debt issue that some are concerned about

When looking at REITs, it's important to see if their debt is structured with fixed or variable rates. I dislike variable-rate loans because while they may have a fixed duration upfront, the interest rate can change over time after the fixed duration period expires if market conditions change. I look for REITs with the majority of their debt tied to fixed rates because a fixed interest rate is a rate that will not change for the entire term of a loan. This is much easier from a budgeting and capital perspective, as unexpected surprises are eliminated from the debt market.

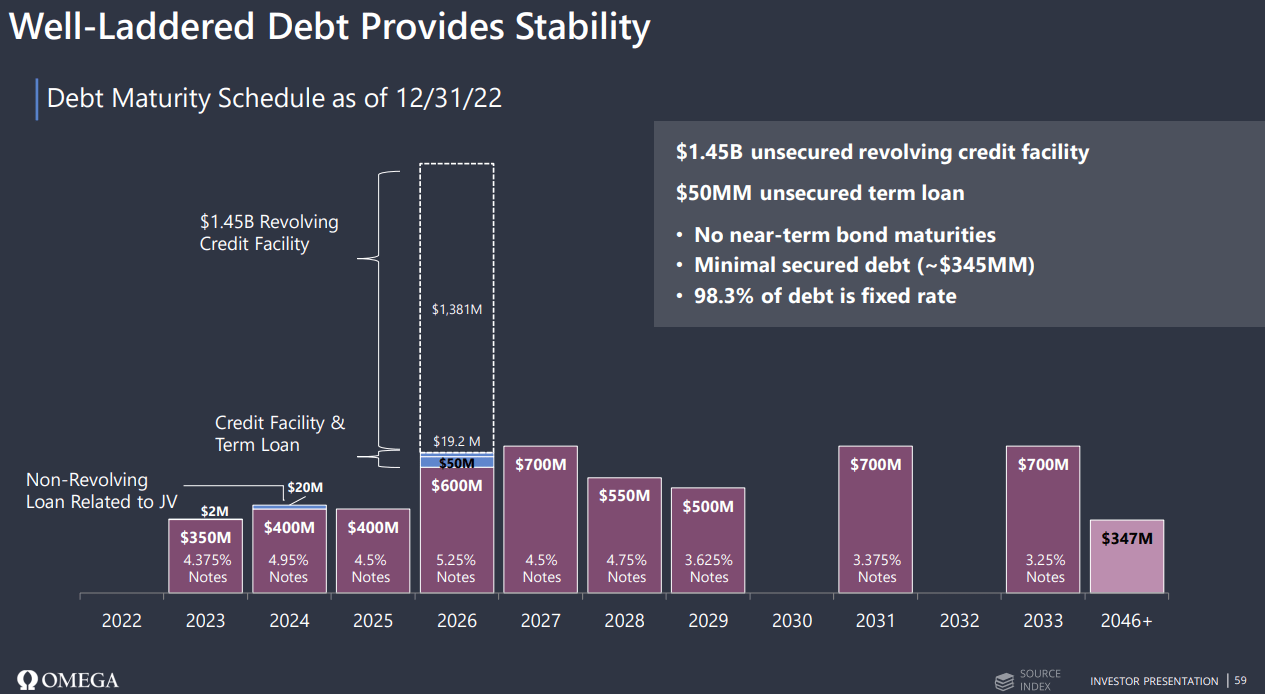

According to Bankrate , traditional banks charge 5.5% -7%+ on a business loan, and SBA loans are pegged between 10-13.5%. The Federal Reserve Bank of Kansas City indicated that in Q3 of 2022, the average interest rate for all small business term loans in the third quarter of 2022 was 5.39% for fixed-rate loans and 6.25% for variable-rate loans. As interest rates increase, the cost of borrowing becomes more expensive. OHI has 98.3% of their debt tied to fixed rates. OHI's debt is fixed at rates between 3.25% and 5.25%. There is also a $1.45 billion unsecured revolving credit facility with $1.38 billion of untapped availability throughout its debt ladder. This is a line of credit where OHI can access the funds whenever needed. This would typically only be used for operating purposes if OHI was experiencing sharp fluctuations in its cash flows and some unexpected large expenses. Having a laddered debt schedule is normal, and the cost of doing business. Even Apple ( AAPL ) has $99 billion in long-term debt and $111 billion in total debt.

{kind=link}

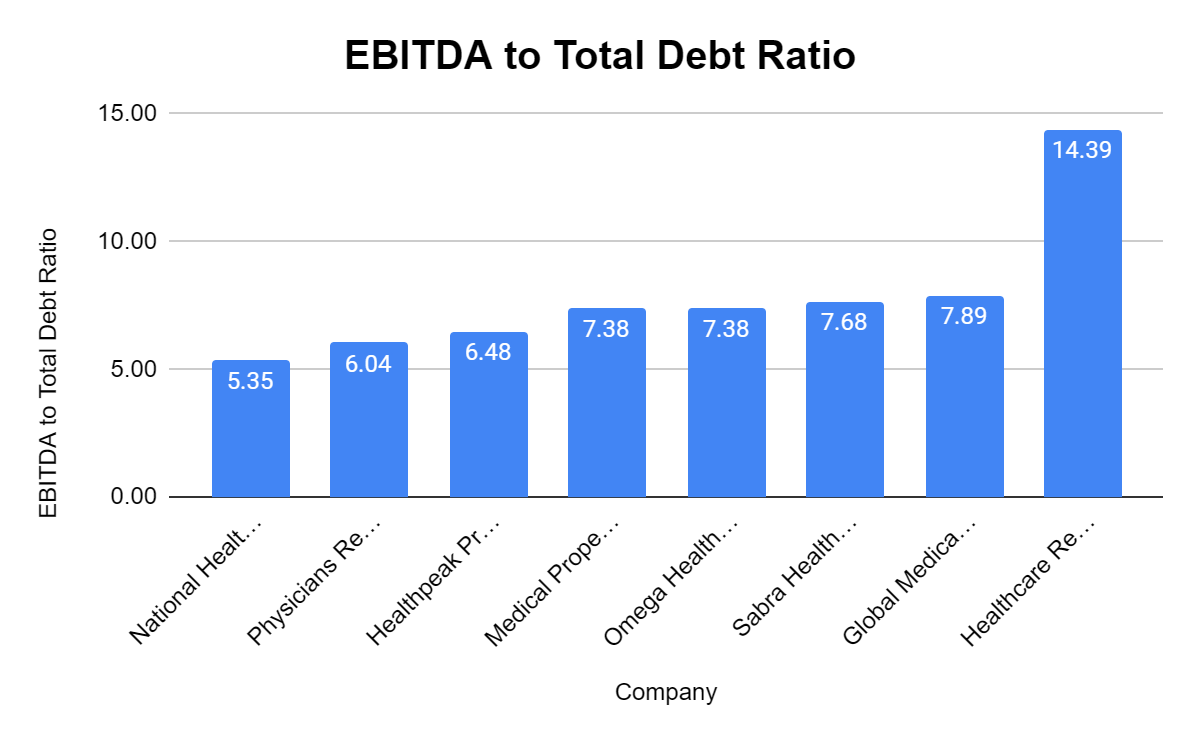

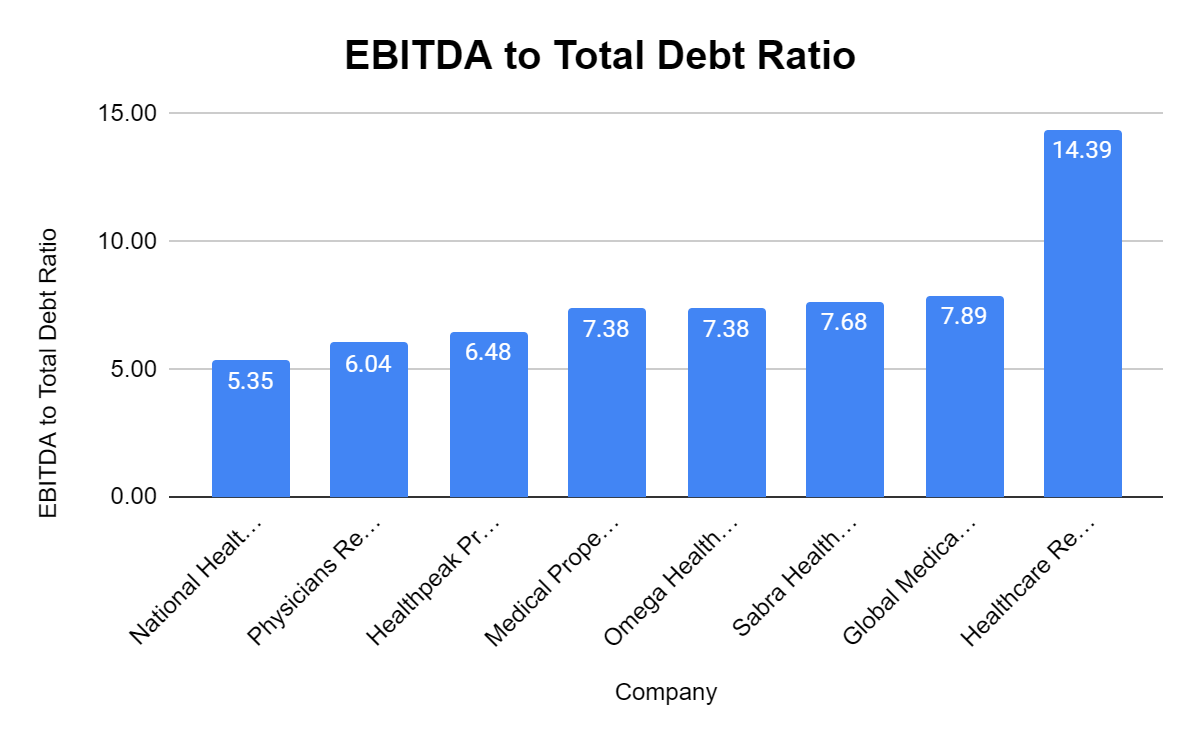

Based on OHI and its peers, OHI's EBITDA to total debt ratio looks acceptable. I look at this because banks may look at these ratios when applying for loans. Also, this metric can be used by credit rating agencies to assess a company's probability of defaulting on issued debt, as companies with high ratios may have difficulty servicing the debt. OHI has an EBITDA to total debt ratio of 7.38x compared to its peer group average of 7.82x. I am not that concerned by this as OHI is generating enough EBITDA to make me feel comfortable. The peer group I used is:

- Sabra Health Care ( SBRA )

- National Health Investors ( NHI )

- Medical Properties Trust ( MPW )

- Physicians Realty Trust ( DOC )

- Healthcare Realty Trust ( HR )

- Healthpeak Properties ( PEAK )

- Global Medical REIT ( GMRE )

{kind=link}

The dividends keep rolling in and that's why I am invested in OHI

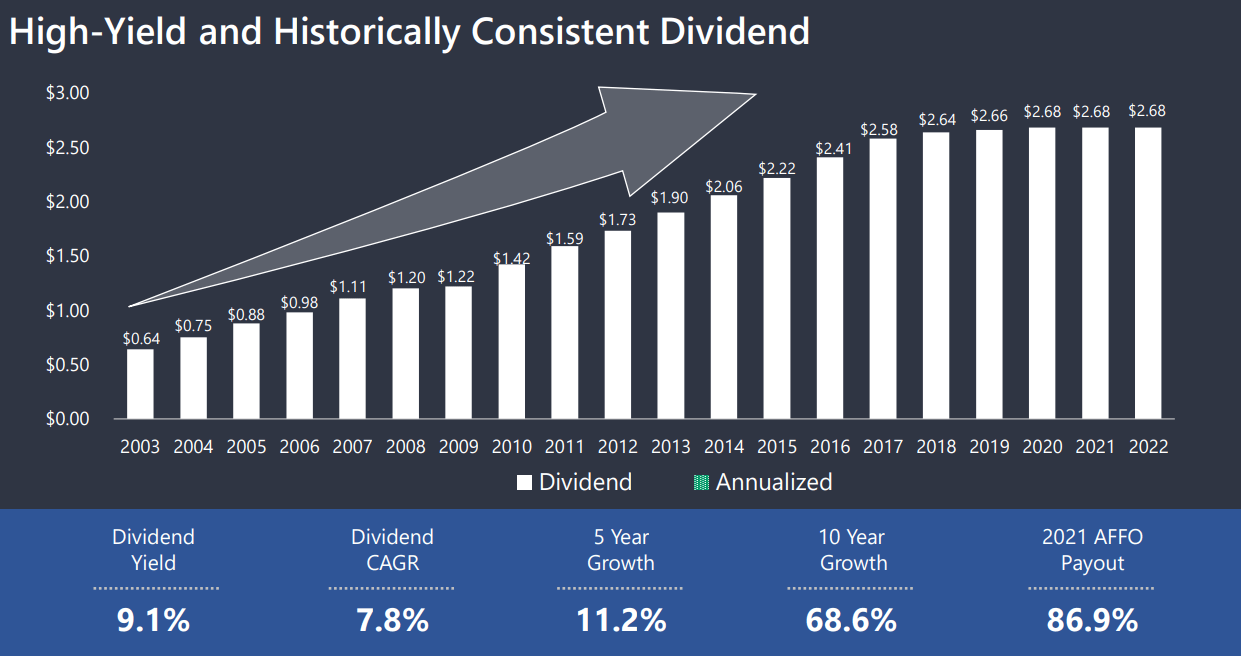

I have been invested in OHI since the end of 2017 and have reinvested each and every dividend. On the Q4 conference call , Taylor Pickett (OHI CEO) wasted no time discussing the dividend and specifically indicated that OHI will return to a run rate that exceeds the dividend in 2023 as the current restructurings are resolved. OHI just paid their quarterly dividend on 2/15/23, and their upcoming ex-dividend date should be coming at the end of April. There has been no public indication of OHI reducing or slashing the dividend, and the rising rates shouldn't impact the dividend as OHI's debt is fixed. This is a dividend that has been paid since 2003, and history has indicated that the dividend is reliable regardless of what the outside commentary is.

{kind=link}

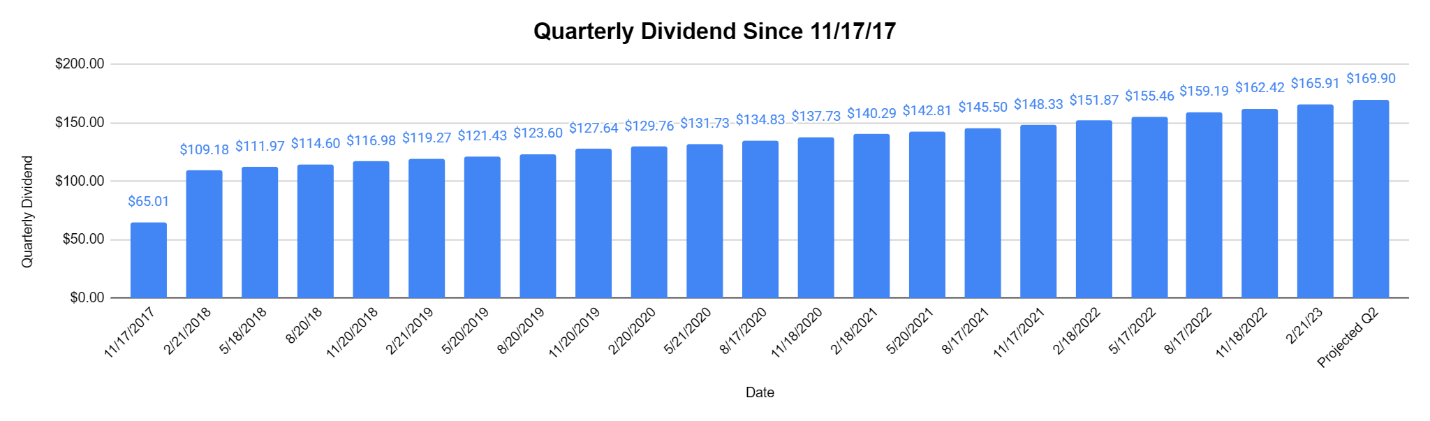

I just received my Q1 dividends from OHI, and here is an update on what this has done to my original investment in one of my accounts I hold OHI in. I decided to disclose this information to illustrate the power of dividends. In the first account, I purchased 163 shares of OHI. I purchased 100 shares in the fall of 2017, then another 63 shares in January 2018. My average out-of-pocket price per share is $29.91 on a $4,890 investment prior to incorporating dividends. I have now received 22 dividends from OHI since my initial investment. I have collected $2,915.50 in dividend income, which is 59.80% of my initial investment. My initial share count has increased by 90.58 shares and added an additional $242.77 of projected dividend income to my base.

My quarterly dividend income from my 2 nd dividend over the previous 20 quarters has grown by $56.73, or 51.96%. My Q2 2023 dividend is projected to be $169.90, which would purchase an additional 6.19 shares at OHI's current prices. As long as the dividend isn't impacted, I will continue adding shares each quarter and growing the compounding effect in OHI. Eventually, I will have generated 100% of my original investment in dividends, and doubled my initial share base without adding an additional dollar.

{kind=link}

OHI still looks interesting compared to its peers

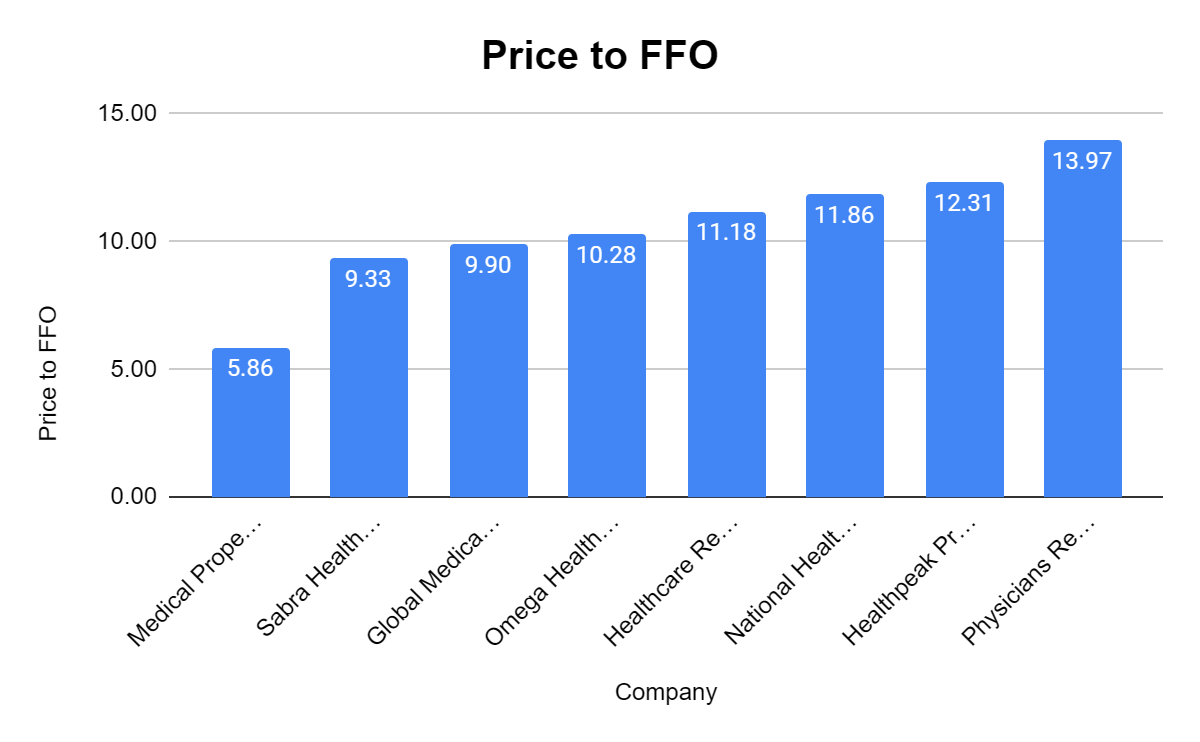

OHI is currently trading at a multiple of 10.28x its funds from operations ((FFO)) compared to a peer group average of 10.59x. When it comes to REITs, the price-to-FFO metric is my favorite comparison tool because I like to see what price I am paying for a REIT FFO. Since all dividends are paid from FFO, I want to make sure I am not overpaying for a REIT's ability to produce FFO. OHI is trading at a discount to its peers.

{kind=link}

As I went over earlier, OHI is trading at a 7.38x EBITDA to total debt multiple, which is below the 7.82x peer group average. This makes me feel comfortable that they won't have issues servicing and repaying their debt obligations.

{kind=link}

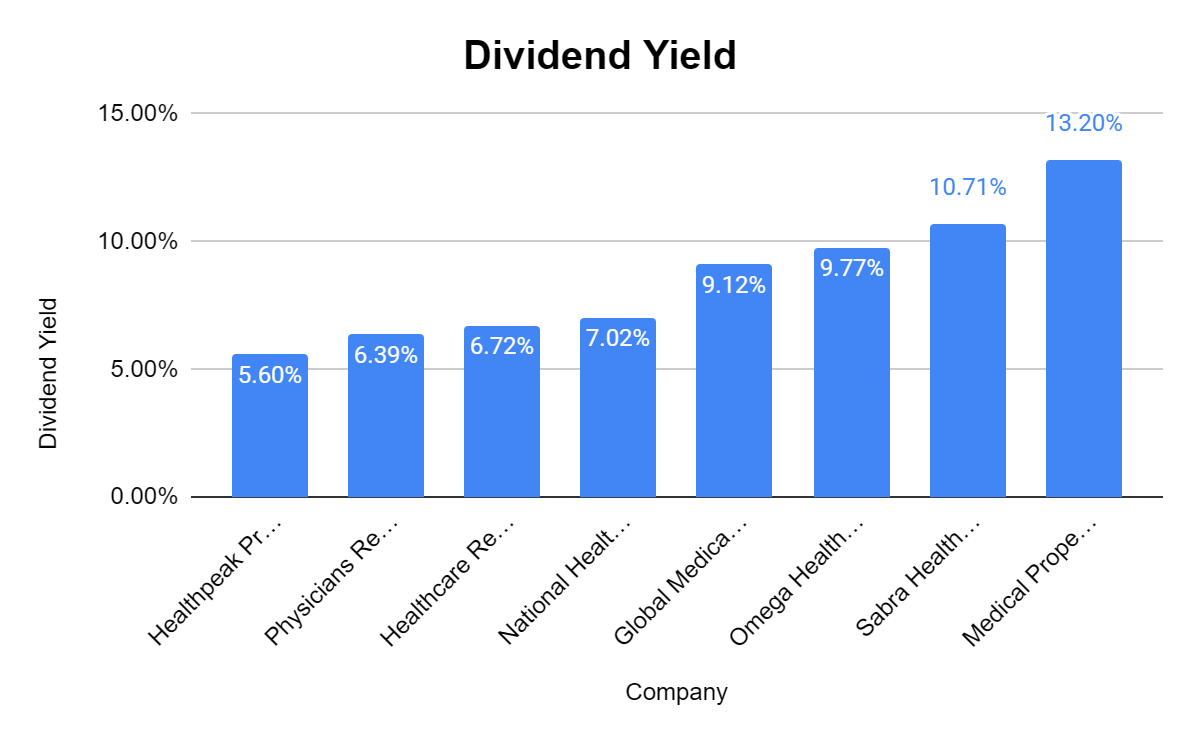

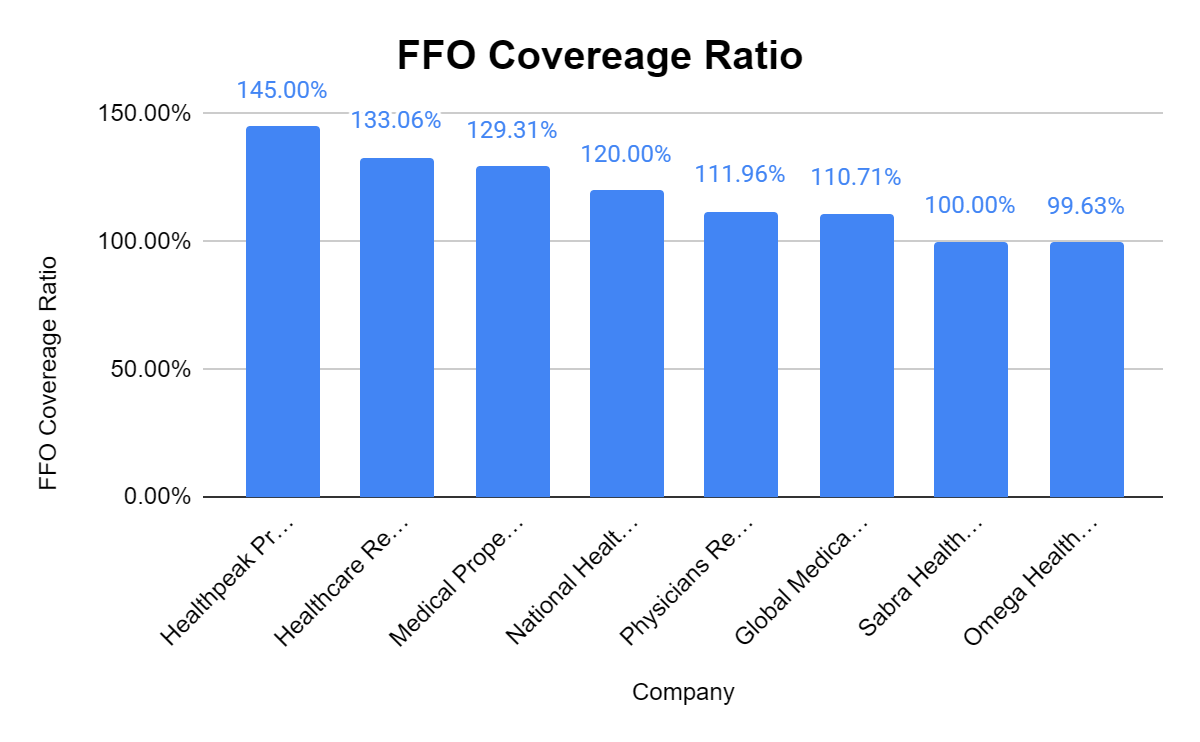

OHI is on the higher end of dividend yields at 9.77%. The peer group average is 8.57%. With the 2-year over 4.5%, I need to generate above 6% to take on equity risk, and in many cases, I would like to see more than 7%. This is why I like REITs, MLPs, and BDCs. The only aspect I don't like is that the FFO coverage ratio is lower than 100%. On the conference call, Mr. Pickett briefly touched on operator restructurings and indicated that OHI is projecting that the FAD in Q1 2023 will be less than $0.67, but OHI will return to a run rate that exceeds the dividend in 2023 as the current restructurings are resolved. While this isn't optimal, as long as OHI returns to a coverage ratio that exceeds 100%, I won't make a big deal about it and will take their word at face value.

{kind=link}

{kind=link}

Conclusion

I am still long on OHI and feel that the dividend is secure. OHI doesn't have a debt problem, and its debt isn't impacted by rising rates, as more than 98% is fixed. It's been a long road for OHI, but they have faced adversity head-on and maintained their dividend while dealing with countless hardships over the years. We still need to see how the restructuring unfolds, but management has delivered during these unprecedented times, and I will continue to reinvest the dividends while waiting for a rebound in the share price.

For further details see:

Omega Healthcare Investors: The Yield Exceeds 9.5%, Q1 Dividend Has Been Paid, Debt Looks Ok