PEAK - Omega Healthcare Looks Extremely Attractive As The Dividend Yield Approaches 10%

Summary

- Omega Healthcare is going into 2023 with a dividend yield that is approaching 10%.

- I have been a shareholder for just over 5 years and while OHI has declined -7.31% from my average price, my overall investment has appreciated 40.81% due to dividends.

- OHI trades at a discount to its peer group, and I believe that if a dividend cut was going to occur, it would have happened already.

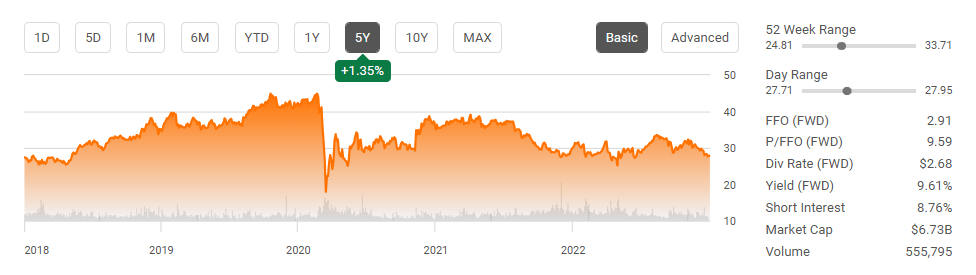

Omega Healthcare Investors ( OHI ) has again fallen under the $30 level, and its dividend yield is quickly approaching 10%. This has been a battleground REIT as Skilled Nursing and Assisted Living Facilities were drastically impacted during the pandemic. Since the Covid crash in 2020, many have speculated that OHI would need to reduce its dividend due to operational difficulties and some of its operators not being able to fulfill their rent obligations. OHI has paid 11 consecutive dividends since the Pandemic started without reducing its payment to shareholders. Management has faced unprecedented adversity and demonstrated that no matter what obstacles OHI is faced with, it can adapt and navigate any business cycle. The U.S. population continues to age, and there is a revolving door of clients for Skilled Nursing and Senior Housing Facilities. OHI is a triple net equity REIT that specializes in these facilities, providing an interesting investment as its operators have a long-term customer base and a never-ending demand for services. I have been a shareholder for just over 5-years and the power of compounding has served me well even though shares are currently below my average price per share prior to the dividend income I have reinvested. I am planning on adding more OHI as shares look very attractive to me under the $30 level.

{kind=link}

My investment in OHI and how reinvesting the dividends have made this a positive investment while shares are trading under my cost basis

At the end of 2017, I purchased my first block of shares when OHI traded at $31.57. At the beginning of 2018, OHI dipped below $30, and I added to my position when shares reached $27.38, bringing my average price per share to $29.95. Since I have been a shareholder, shares of OHI have exceeded $40 leading up to the Pandemic, and shares have traded under the $30 level. I have always said that when it comes to high-yielding REITs, I don't mind price fluctuations if the dividend stays intact, and shares don't retrace too far under my average price per share. Today shares of OHI trade at $27.76, which is -7.31% (-$2.19) from my average price per share. Reinvesting the dividends has made this a net positive investment, generating an increased amount of dividend income each quarter. I am going to outline how my investment has worked out to illustrate how dividends can play an important factor in an overall investment.

To date, I have collected 21 dividends from OHI, which is equivalent to 56.32% of my original invested capital. I had collected my 1st dividend before dollar cost averaging, so my 1st dividend is significantly smaller than the rest. I haven't added shares of OHI to this account since early 2018. After the 2nd dividend was paid, the quarterly dividend paid by my shares of OHI increased by 48.78% over the next 19 dividend payments. I didn't add a single dollar for almost 5 years, and over 19 dividends, my quarterly dividend payment has grown significantly.

If you were to look at this investment and deduct the dividend income from my original cost basis, the average price per share I paid out of pocket has declined from $29.95 to $13.08 on the original shares. While shares of OHI have retraced under my original price per share by -7.31%, my actual investment has appreciated by 40.81% due to my share base growing by 51.91%. Over the course of the last 19 dividends, my quarterly dividend income has increased by 2.57%. Shares of OHI may have retraced under my original purchase prices, but my actual investment has appreciated, and the amount of dividend income generated each quarter continues to increase. OHI has been a winner despite shares having a lower share price than I would like. I plan on reinvesting each dividend that is paid, and I look forward to my next dividend from OHI in February.

{kind=link}

Omega Healthcare's declining finish to 2022 could be due to tax loss harvesting or investors changing their investment thesis, but management hasn't given investors a reason to be worried

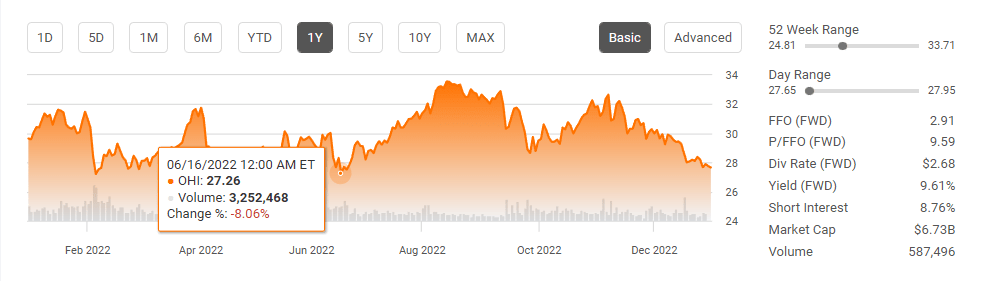

Shares of OHI have declined -6.71% over the past year, and despite falling from $32.66 on 11/7/22, they are well off their 2022 established lows of $24.81 in May. There hasn't been any significant news since Q3 earnings coming from management. The only negative news I have seen is that Bank of America ( BAC ) analyst Joshua Dennerlein has downgraded OHI from buy to neutral. The declining share price could be attributed to many factors, including investors selling due to tax loss harvesting, or with the markets down double digits in 2022, they could feel that their capital would be better invested elsewhere.

{kind=link}

Regardless of what OHI's share price does, I believe it's a buy. Over the years, OHI's share price has fluctuated, and the ups and downs are something I have built into my investment thesis. If I was looking for upside appreciation, I would look at Alphabet (GOOG) ( GOOGL ) or Apple ( AAPL ) rather than OHI, as these are cash cows that have the potential to appreciate when the market turns significantly. OHI plays an important role in the healthcare space as they have 916 properties where 63 operators manage 91,643 beds. As a triple net lease company, 97% of OHI's revenues are tied to master leases, with 95% of its revenue tied to fixed-rate escalators at an average of 2.3%.

{kind=link}

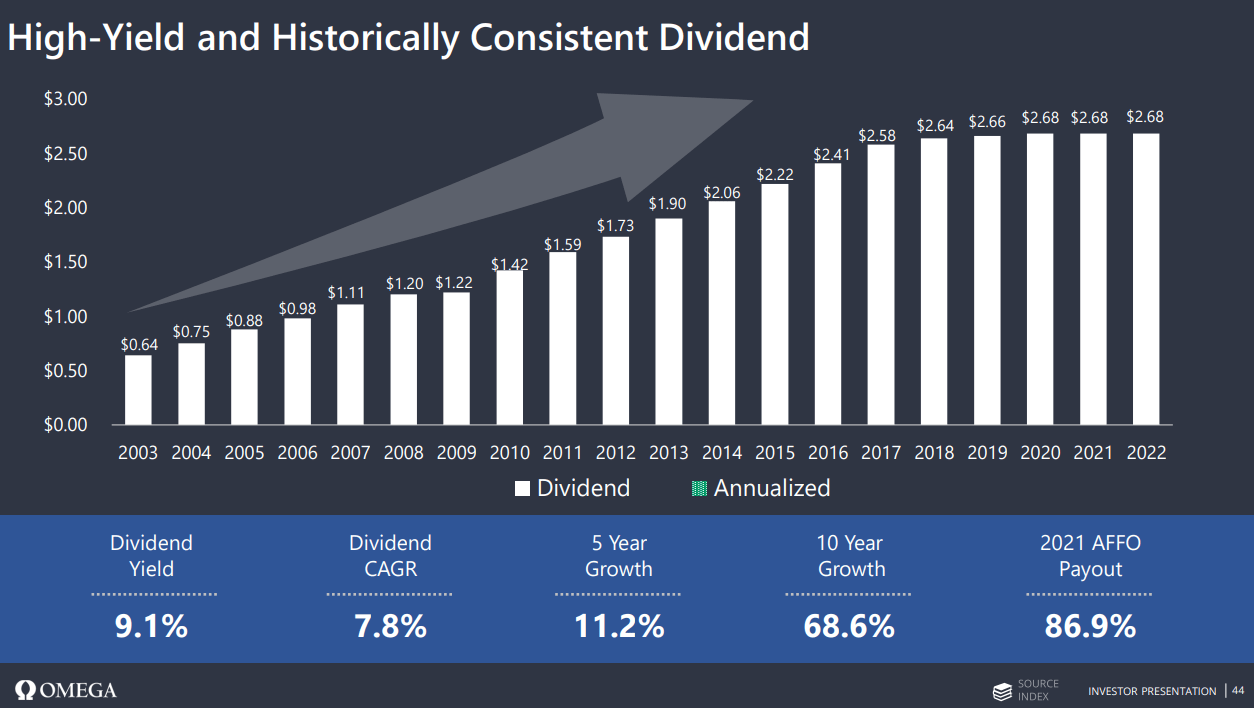

Reading through the Q3 report once again, I am not finding reasons to abandon OHI, especially since I have ridden out cycles like this previously. OHI delivered stronger than expected earnings in Q3 generating $0.76 of Adjusted FFO while the consensus estimate was $0.74, and its revenue came in at $239.4 million while the consensus estimate was $215.9 million. OHI's funds available for distribution came in at $173 million, and OHI declared another $0.67 quarterly dividend, keeping its annual payout of $2.68 intact. OHI was also active as it completed $28 million in real estate acquisitions and funded $19 million in capital renovation and construction projects. OHI also took most of the proceeds from selling 4 facilities for $51 million and investing $40 million in a new loan that will generate 12% for them. On the Q3 conference call , Taylor Pickett (OHI CEO) discussed that working with some of their struggling operators, such as Agemo, through the portfolio restructurings will have minimal to no impact on its asset values or long-term cash flows. Since the pandemic, OHI has sold $1.6 billion of assets allowing them to exit underperforming facilities, and deployed this capital toward asset purchases, construction, loans, and leverage-neutral stock buybacks, strengthening its operations and protecting the long-term value proposition for shareholders.

OHI looks undervalued compared to its peers and is an income-producing opportunity in the healthcare RIET space

I have tracked OHI against its peer group in its price to Funds From Operations (FFO), EBITDA to Total Debt, and Dividend Yield for some time. OHI still looks attractive to me from these metrics. I will be using the following companies to compare OHI against:

- Sabra Health Care ( SBRA )

- National Health Investors ( NHI )

- Medical Properties Trust ( MPW )

- Physicians Realty Trust ( DOC )

- Healthcare Realty Trust ( HR )

- Healthpeak Properties ( PEAK )

- Global Medical REIT ( GMRE )

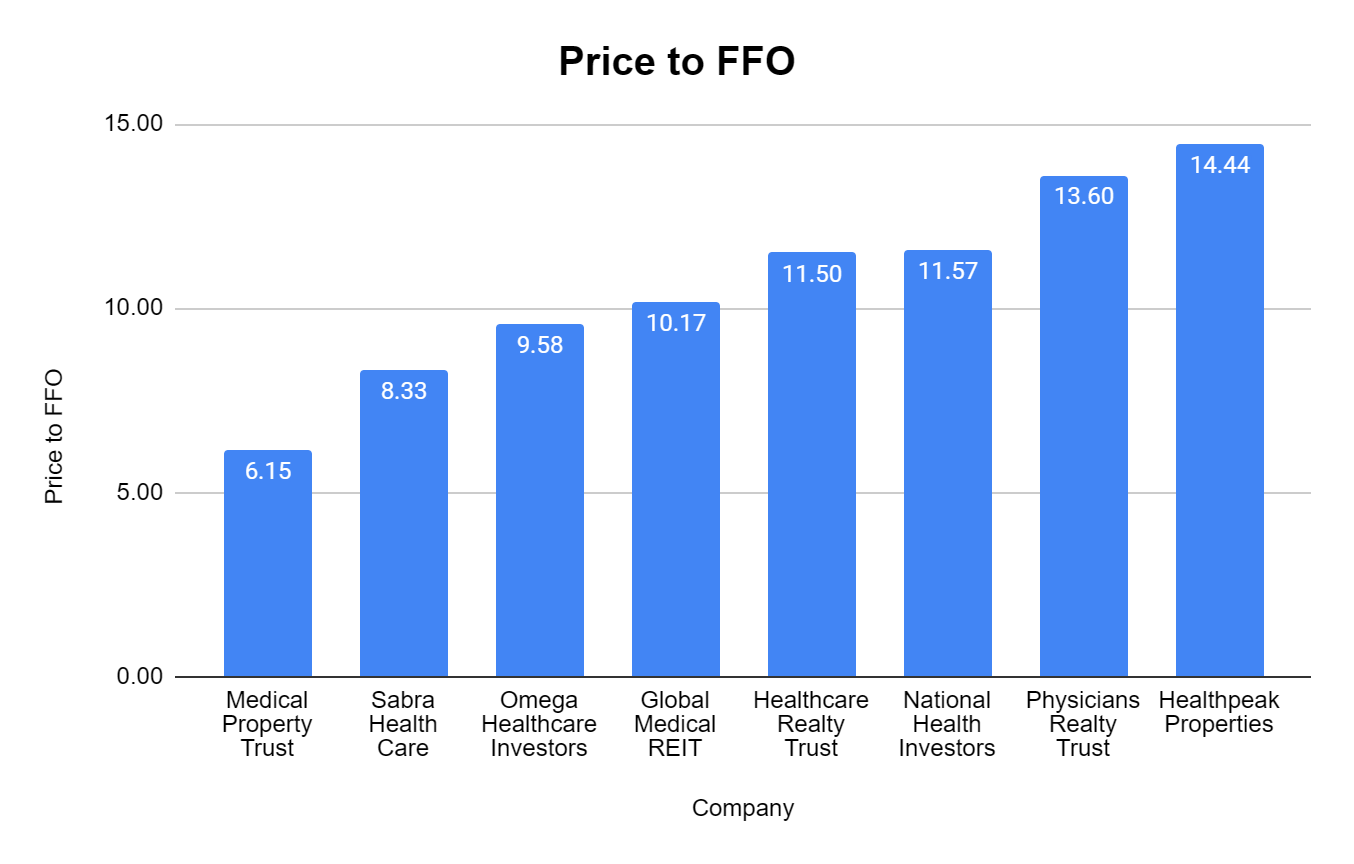

OHI is currently trading at a multiple of 9.58x its funds from operations ((FFO)) compared to a peer group average of 10.67x. When it comes to REITs, the price-to-FFO metric is my favorite comparison tool because I like to see what price I am paying for a REIT FFO. Since all dividends are paid from FFO, I want to make sure I am not overpaying for a REITs ability to produce FFO. OHI is trading at a significant discount to its peers.

{kind=link}

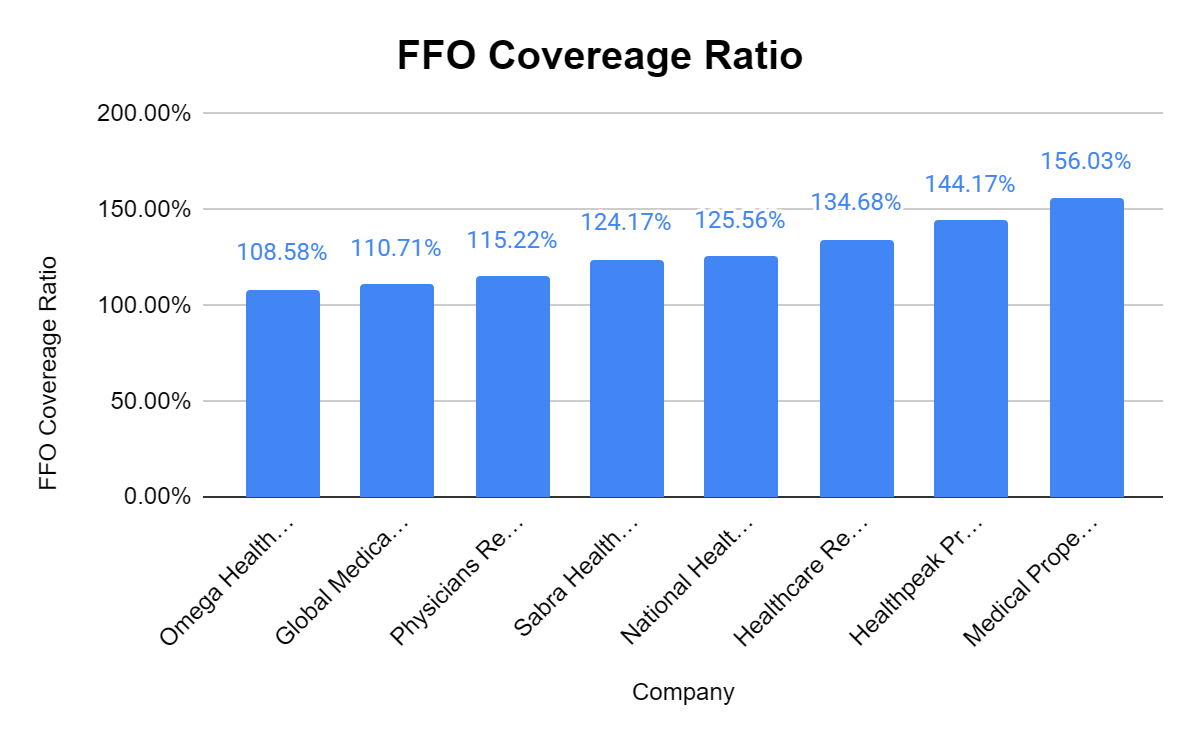

OHI hasn't dipped below a 1:1 coverage ratio for its dividend. While OHI trades at a discount to its FFO, it provides a 108.58% coverage ratio for its dividend. This is also expected to improve in the future, per the conference call.

{kind=link}

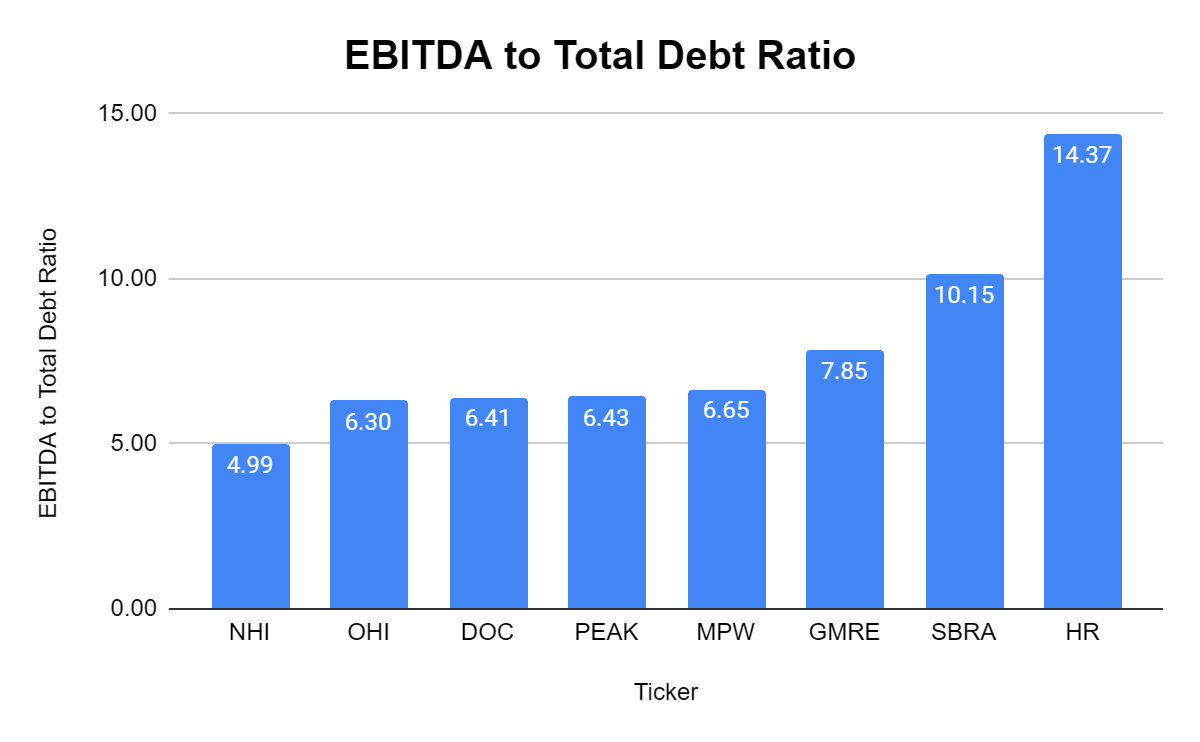

Looking at the EBITDA to Total Debt ratio, OHI looks to be in excellent condition. OHI trades at a 6.3x multiple of EBITDA to total debt, which indicates that OHI can eliminate all its debt with 6.3 years of its EBITDA. The peer group average is 7.9 years, and OHI has the 2nd lowest multiple.

{kind=link}

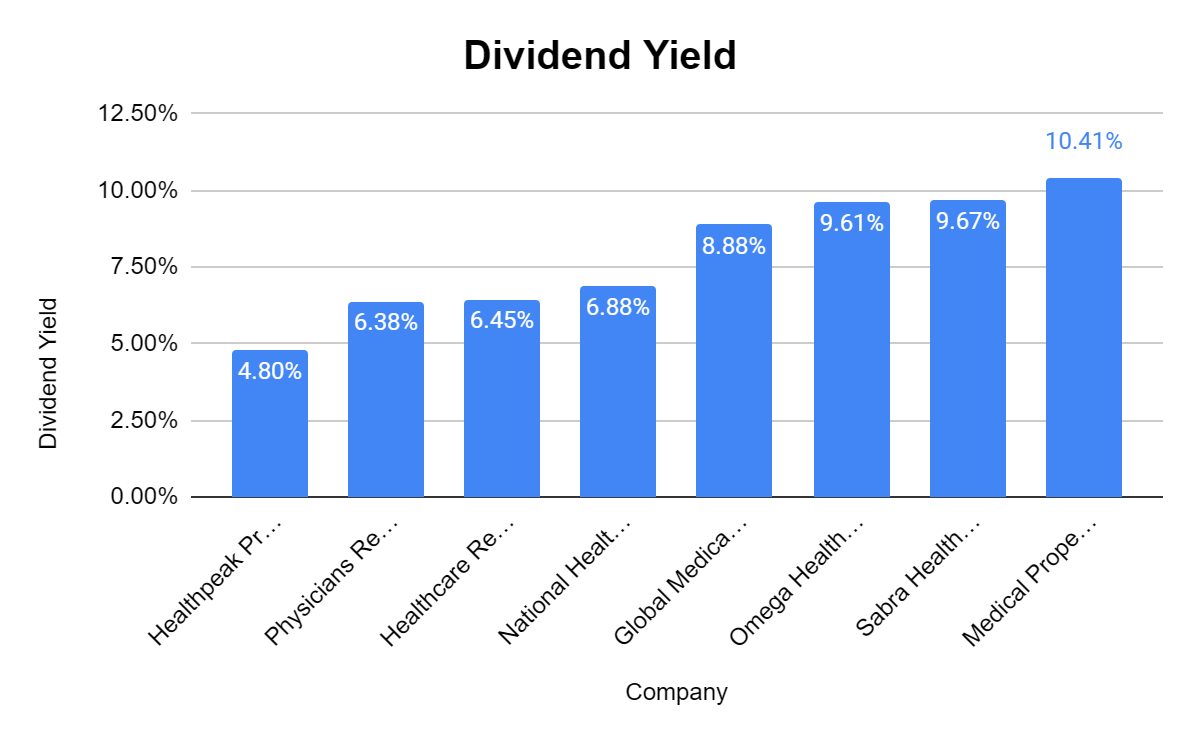

REITs are ultimately income investments for me, so the dividend yield and FFO payout ratio are important. OHI has a dividend yield of 9.61%, which is significantly above the peer group average of 7.9%. This also exceeds the risk free yield environment that short term treasuries and CDs are providing for investors.

{kind=link}

Conclusion

I am long OHI, and I feel that shares are trading at low valuations going into 2023. OHI has been a great investment for me, and even though shares are below my entry point, my investment has grown 40.81%, and I have generated 56.32% of my initial investment through dividends over the past 5-years. I plan on adding to my position in OHI under the $30 level and believe this is a strong long-term buy for income investors. In my opinion, if OHI needed to reduce the dividend, it would have occurred already, and since 11 dividends have been paid since the pandemic started, it should remain intact. As the yield approaches 10%, this can be a lucrative investment over time without modest share appreciation occurring if you're reinvesting the dividends. I am looking at OHI as a pure income play, and if shares appreciate, it's an added bonus.

For further details see:

Omega Healthcare Looks Extremely Attractive As The Dividend Yield Approaches 10%