OMER - Omeros: Why It Is Worthwhile To Bet On Narsoplimab

2023-11-27 01:18:10 ET

Summary

- Omeros Corporation focuses on small-molecule and antibody drugs for common disorders and rare diseases.

- The company has prioritized the resubmission of its BLA for Narsoplimab for TA-TMA treatment and is advancing Phase-3 clinical trials for MASP-3 inhibitor OMS906.

- Narsoplimab holds promise for treating TA-TMA, COVID-19, and Lupus Nephritis but faces competition in the latter two conditions.

- OMER's valuation is low enough to justify a speculative "buy" rating, given its clear pathway for Narsoplimab's potential FDA approval.

Omeros Corporation ( OMER ) is a clinical-stage biopharmaceutical company based in Seattle, Washington. OMER focuses on various small-molecule and antibody drugs to meet medical needs for common disorders and rare diseases. In 2021, OMER sold its Omidria ophthalmic product franchise to Rayner Surgical for over $1 billion, a deal that continues to generate royalties. OMER has now pivoted and prioritized its BLA resubmission for Narsoplimab for TA-TMA treatment and advances Phase-3 clinical trials for MASP-3 inhibitor OMS906, targeting conditions like PNH and C3 glomerulopathy. From an investment perspective, this makes OMER an inherently speculative proposition. Yet, given the clear pathway to ultimate approval for Narsoplimab and exceptionally low valuation, I think there is a compelling "buy" argument for OMER at these levels. However, investors need to know this is still a highly speculative play.

Business Overview

Omeros is a clinical-stage biopharmaceutical company headquartered in Seattle, Washington. OMER was founded in 1994 and currently has over 200 employees. They pursue a diverse pipeline of small-molecule and antibody products to innovative target receptors and enzymes for various therapeutic indications. OMER's promising drugs aim to solve unmet medical needs for frequent disorders and orphan diseases.

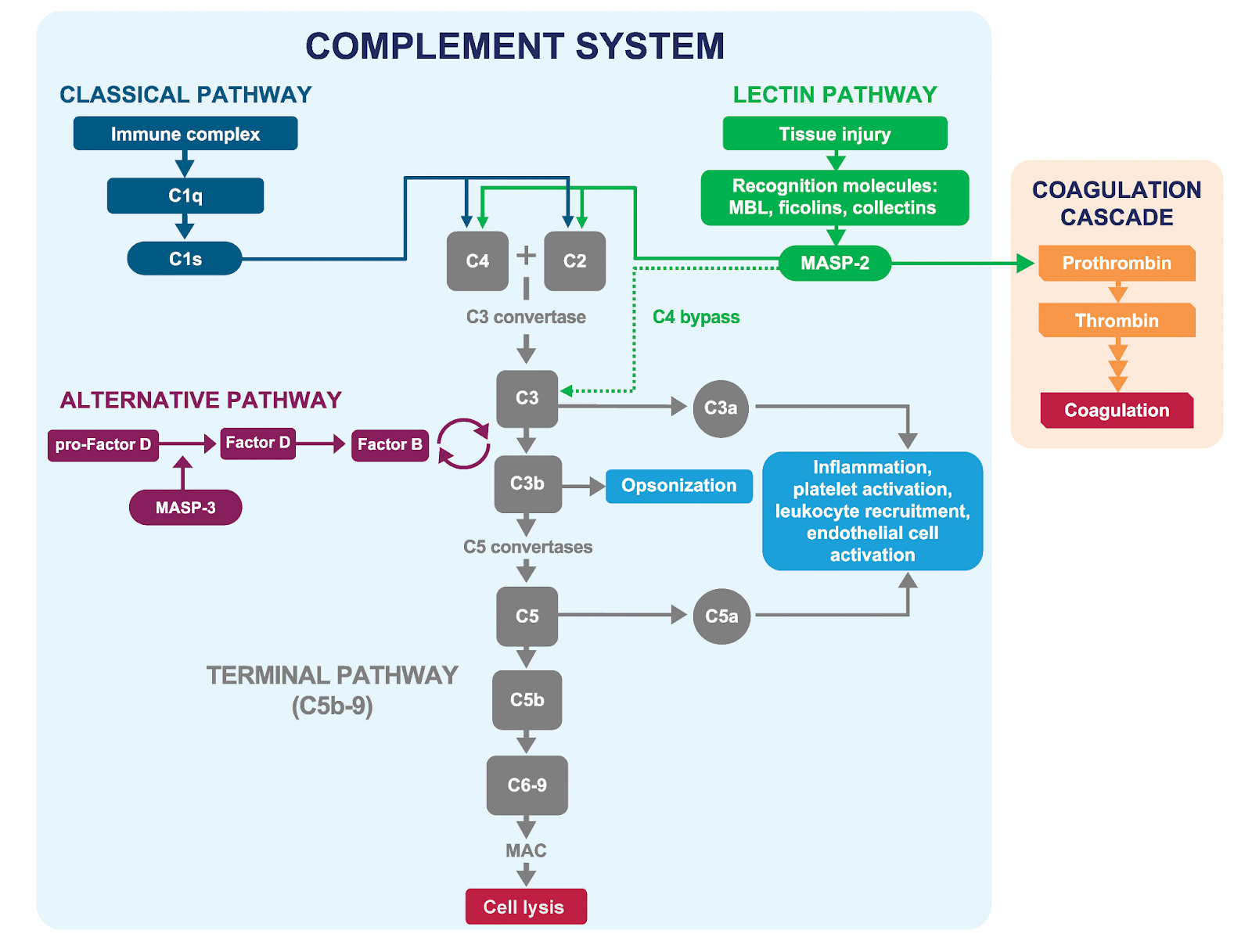

OMER's complement franchise provides several drugs. However, OMER's most prominent research in its pipeline is undoubtedly Narsoplimab, also known as MASP-2 or MS721. This drug is indicated for ImmunoChemistry Adaptive Bridging (iCAB), which targets the immune system as a monoclonal complement inhibitor. In particular, Narsoplimab is prescribed for Stem Cell Transplant-Associated TMA (TA_TMA), a severe complication characterized by the formation of blood clots that could lead to multiple organ dysfunction.

Why OMS721 (AKA Narsoplimab) Matters

OMS721 is Narsoplimab, and this particular drug holds promise for three potential conditions: 1) TA-TMA, 2) COVID-19, and 3) Lupus Nephritis. The way OMS721 works is similar for all three, though with slight differences. For TA-TMA, which is Stem-Cell Transplant-Associated TMA, the affliction is that some patients develop blood clots after stem-cell transplants. Such blood clots can cause organ damage, so OMS721 targets the MASP-2 protein, which reduces the activation of the lectin pathway. This is the main role of OMS721 because by doing this, Narsoplimab effectively reduces the formation of blood clots and protects patients from organ damage. This can potentially increase survivability rates, so it's a key treatment. OMS721 especially shines for treating TA-TMA because, as of today, Narsoplimab has become the only drug approved for this condition.

{kind=link}

However, unlike TA-TMA, Narsoplimab isn't the only viable treatment for critically ill COVID-19 patients or patients who developed SLE complications. These two conditions have many alternative therapies, so OMS721 would ostensibly face significant competition. Consequently, Narsoplimab's main market would be TA-TMA, particularly HSCT-TMA (Hematopoietic Stem Cell Transplant-Associated Thrombotic Microangiopathy). The drug is in Phase 3 of clinical trials , near registration for this indication. In May 2023 , OMER met with the FDA to discuss resubmitting the Biologics License Application ("BLA") for Narsoplimab indicated for TA-TMA. OMER will resubmit the application, including additional information supporting approval of Narsoplimab in this indication.

Naturally, OMS721 and its effects also help with COVID-19 or Lupus Nephritis. Here, the same dynamic is at play. By targeting the MASP-2 protein, the lectin pathway is inhibited. For COVID-19 patients, this is vital because it lowers excessive inflation and autoimmune effects, potentially improving survival chances in critically ill patients. Likewise, patients with Lupus Nephritis sometimes develop a condition known as systemic lupus erythematosus ((SLE)), which is an autoimmune complication. However, as with COVID-19 and TA-TMA, OMS721 targets the MASP-2 protein and reduces kidney inflammation, alleviating the complications stemming from SLE.

Narsoplimab is in Phase 2 to prevent complement-mediated inflammation produced by COVID-19 , Lupus nephritis & other renal diseases. For IgA nephropathy and Atypical hemolytic uremic syndrome, the medication is in Phase 3 . Small-molecule inhibitors of MASP-2, MASP-3, and MASP-2/-3 are orally available and form part of the lifecycle of Narsoplimab in the preclinical stage.

Regulatory Context and Product Pipeline Details

MASP-3 or OMS906 is a monoclonal antibody complement inhibitor for paroxysmal nocturnal hemoglobinuria ((PNH)) and a Wide Range of Other Alternative Pathway Disorders. The FDA has designed it as an orphan drug for treating PNH. This medication is in clinical trials at the end of Phase I. MASP-2, also called OMS1029 , is a long-acting second-generation antibody targeting mannan-binding lectin-associated serineprotease-2 (MASP-2), the effector enzyme of the lectin pathway of the complement system. The lectin pathway is one of the pathways through which the complement system is activated for the body's defense against pathogens. OMS1029 is in clinical trials, Phase 1.

Source: Omeros Complement Programs, April 2023.

Furthermore, OMER is developing several drugs for the treatment of addiction. OMS527 is a small-molecule phosphodiesterase 7 (PDE7) inhibitor indicated for Addictions, Compulsive Disorders and Movement Disorders. It reduces craving and relapse from abuse of drugs such as opioids, cocaine, nicotine, and alcohol and also reduces binge eating in animal models. Studies show that OMS527 does not depress the reward system or the ability to feel pleasure in normal activities, which are negative effects of current addiction therapies. This drug is in Phase 2 of the clinical trials. In the same line, OMS405 is a Small-molecule peroxisome proliferator-activated receptor gamma (PPAR?) agonist for the treatment of addictive disorders. It is in clinical trials, Phase II, with testing executed in collaboration with The New York State Psychiatric Institute. These studies showed that the PPAR? agonist significantly reduced heroin craving and overall anxiety.

In oncology, OMER offers GPR174, a small-molecule inhibitor for cancer that harnesses the body's immune system to fight cancer. This drug is initiating the preclinical stage. Also, in the preclinical trials is the Adoptive T cell therapies/CAR T, which are small-molecule inhibitors for preventing relapse associated with a lack of memory T cells, a significant shortcoming of many currently marketed immunotherapies.

Source: Omeros Complement Programs, April 2023.

Additionally, a notable prior development of OMER was Omidria, which includes intraocular lenses, ophthalmic viscoelastic devices, and dry eye treatments. In 2021, OMER sold the Omidria franchise to Rayner Surgical in a transaction valued at more than $1 billion. The deal included the payment of royalties of 50% of US net sales until January 1, 2025, or payment of a $200 million milestone. After that, OMER will receive royalties of 30% of US net sales for the life of Omidria's US patent estate. Outside of the US, OMER gets a 15% royalty rate on the net sales throughout the applicable patent state in each country.

Reducing Costs To Focus on Narsoplimab

In the last earnings call , OMER executives expressed that the company focuses on Narsoplimab in treating TAEarnings Call-TMA and advancing Phase-3 clinical trials for MASP-3 inhibitor OMS906 in PNH and C3 glomerulopathy. They stated that they are assembling all the information for Narsoplimab´s BLA to present to the FDA according to the guidance documents set forth by the FDA. Also, OMER is discontinuing its phase 3 Narsoplimab trial for immunoglobulin A ((IGA)) nephropathy treatment because the results were not better than those of the placebo. The data is being analyzed to understand the role of lectin pathway inhibition in kidney diseases. OMER stated that the funds earmarked for the commercialization in IgAN and continuation of the trial will be redirected to other later-stage programs. Furthermore, executives mentioned during the call that royalties for OMIDRIA were $10 million in Q3 2023.

Financial Analysis

In any case, I'd argue that the key value driver for the stock at this point is the potential of Narsoplimab (OMS721). As I've shown in my research, it's the best candidate among OMER's product pipeline to eventually become a reliable and considerable revenue contributor over the long run. This is not the case yet, as OMS721 is still pending approval. Moreover, OMS721 has three potential uses, of which the two main ones on phase 3 trials are for HSCT-TMA and IgAN. Still, the Narsoplimab trial for IgA nephropathy was discontinued due to unsatisfactory results, and OMER is strategically reallocating resources to optimize the development of its other promising drug.

Source: OMER's website.

This showcases the highly uncertain nature of OMER's research. Yet, Narsoplimab's orphan drug status designation is encouraging and likely the main silver lining, as it secures a market for the company. According to the Orphan Drug Act of 1983, the benefits include tax credits, market exclusivity for a potential seven years, and regulatory assistance in drug development. As such, this designation reduces Narsoplimab's risk profile from an investment perspective and makes it more attractive, assuming it's successfully developed and commercialized.

In that context, OMER must prepare the required research and documentation for its BLA. It's speculative to estimate how long this will take because this is where OMER has to do most of the R&D work. However, I gather it should take at least several months up to a year to prepare for its BLA resubmission. After this, the FDA usually takes 6 to 10 months to review the application and decide. At this point, assuming OMER gets approved, Narsoplimab would enter the market officially and should shortly become a revenue contributor. The timeline is uncertain, but if we add up these timetables, the ultimate approval could occur within 18 months to three years if no meaningful setbacks arise.

With that in mind, consider OMER's balance sheet and cash runway. In this sense, OMER´s net loss for the third quarter of 2023 was $37.8 million, and cash burn was $31.0 million. Annualized the cash burn, we get a yearly rate of $124.0 million. The company's current cash position of $310.3 million implies a cash runway of approximately 2.5 years. In theory, this should be enough time for OMER and its shareholders to determine Narsoplimab's actual likelihood of approval after its BLA resubmission.

Investment Thesis Risks

Hence, I think that at the current $115.7 million market cap valuation, it's a relatively attractive speculative buy. Naturally, investors must realize that there's a real possibility that OMER will fail to get Narsoplimab approved within the constraints of its current cash runway. Given that it already holds roughly $466.3 million in debt , I imagine financing options would quickly dwindle at that point for OMER. This worst-case scenario would lead to significant shareholder losses and potentially total capital loss.

Moreover, OMER still has commercialization challenges even if Narsoplimab gets approved within the next few years. These, coupled with winding down its current debt load, will likely mean that financing its production capabilities at that point can be tricky. Nevertheless, despite all these risks, I think OMER is so cheaply priced at this point that they're well compensated with the potential upside if OMER is successful in its endeavors.

OMER is at such a low valuation that it likely offers enough upside potential to compensate for its risks. (TradingView.)

Conclusion

Overall, OMER's value comes down to the likelihood and upside derived from Narsoplimab. Given enough time, there's a reasonable chance that OMER should be able to get it approved eventually. However, this is not without its risks, and the reality is that ultimate FDA approval remains highly uncertain. Yet, from an investment perspective, there's a compelling argument for OMER as a highly speculative "buy" at these levels. Its market cap is sufficiently cheap to offer high potential returns if OMER succeeds. But investors need to be aware that this type of investment shouldn't be the core of their portfolio but rather a smaller part dedicated to speculative, high-risk, high-reward opportunities.

For further details see:

Omeros: Why It Is Worthwhile To Bet On Narsoplimab