OMVJF - OMV: Reiterating The Buy Recommendation

2023-07-03 08:00:09 ET

Summary

- Q1 2023 numbers, announced on April 28, show the expected YoY deterioration due to lower oil and gas prices.

- Net debt was further reduced now to only 0.6bn euros, making the company practically debt-free.

- OMV is making good progress on its 2030 Strategy and the production decision for the Neptun Deep gas field is a very positive development.

- The rumoured sale of the Chemicals subsidiary Borealis to the Abu Dhabi National Oil Company is unlikely to happen - in my view.

- My forecast for 2023 earnings and dividend per share is around 9 euros for earnings and 3-4 euros for the dividend. The Buy rating is confirmed.

(Note: all amounts in the article, unless specifically marked, are in EUR. At the current exchange rate 1 EUR is around 1.09 USD.)

Investment Thesis

Since my first article on OMV ( OTCPK:OMVJF , OTCPK:OMVKY ), OMV: Double-Digit Dividend Yield And Better Financials Than Larger Peers , in April shares are down around 10% nominally (in Euro) and about flat considering the 11% dividend paid in May 2023.

It is time to reevaluate the Buy recommendation.

Notable developments since the previous article are that OMV published their Q1 2023 results, and its Romanian subsidiary OMV Petrov announced the final positive investment decision on the Black Sea Neptun gas field. Measured in boe the Neptun Deep gas field provides 20% of the current yearly production from oil and gas exploration, at around a third of the production cost.

Q1 2023 numbers, announced on April 28 , show the expected deterioration YoY due to lower energy prices. Still, I expect earnings per share for 2023 to be around 9 euros and the dividend per share (to be paid in 2024) to be between 3-4 euros. OMV had paid a dividend of 5.05 euros for 2022, consisting of a regular dividend of 2.8 euros and special dividend of 2.25 euros. At the current share price of 39 euros the P/E ratio would be only around 4.5, and the dividend yield around 8-10 percent.

The Buy rating from my previous article is therefore confirmed.

Q1 2023 financial results

As expected, the Q1 numbers were strong, but could not measure up to the first quarter in the previous year. OMV expected oil and gas prices as well as petrochemical margins to be lower in 2023 than during the exceptional year 2022, so this was no surprise.

Revenue decreased by 31% YoY to 10.964bn euros, mainly due to the decrease in natural gas prices. The operating result declined by 542mn to 2.08bn euros.

Cash flow from operating activities excluding net working capital effects decreased by 40% YoY to 2bn from 3.35bn. Net working capital effects generated a cash inflow of 684mn, compared to a cash outflow of -674mn in the previous year. Therefore the FCF increased by 12% YoY to 1.702bn.

Adjusted EPS was 3.13 euros versus 3.27 in the previous year. The adjustment here is mostly that the current cost of supply effect is eliminated from the accounting result, to make operational results comparable. Without adjustments EPS was 1.19 euros, versus 1.67 euros in Q1 2022 and 0.94 euros in Q4 2022.

The clean balance sheet became even cleaner

OMV has an exceptionally clean balance sheet and this has even improved over the last quarter. Net debt declined by 1.6bn to now 0.6bn.

OMV net debt and leverage ratio (Source: OMV)

The leverage ratio, defined as net debt including leases to capital employed, has continuously improved since 2020. At the end of Q1 2023 it was only 2%.

Dividend policy

This should assure that a significant dividend will be paid for 2023. OMV is not a growth stock and mostly interesting for income investors. Therefore dividend stability is very important.

OMV has established a progressive dividend policy, based on a regular dividend (2.8 euro per share for the fiscal year 2022) with an additional optional special dividend (2.35 per share for 2022). The goal is to increase the regular dividend every year or at least to maintain the level of the respective previous year. OMV aims to distribute ~20-30% of operating cash flow (including net working capital effects) as regular and special dividend. The special dividend is dependent on a leverage ratio below 30%. But as we have seen above the leverage ratio at the end of Q1 was only 2%.

OMV has an excellent dividend track record:

OMV dividend history (Source: OMV)

If OMV only keeps the regular dividend at least stable (the minimum per the dividend policy), the lower floor for the dividend yield (based on the current share price) is ~7%. That is not bad, but as I have said, I expect the company to do better and the dividend yield should be around 8-10%.

Neptun Deep gas field

OMV announced the final positive investment decision on the Black Sea Neptun Deep gas field. The Neptun Deep gas field is located in the Romanian Black Sea and it should become one of the largest gas exploration sites in Europe. OMV Petrom (OMV AG holds a 51.2% stake in the company) will be the operator and will develop the gas project in a 50/50 partnership with Romgaz. Requiring investments of 4bn (2bn from OMV Petrom mostly between 2024 and 2026), first gas is expected to be produced in 2027. The total estimated recoverable volume is 100bcm (around 700mn boe).

Production - at the peak - will be approximately 140 kboe/day, for almost 10 years. Unit production cost is estimated at to 3 USD/boe as an average over the life of the field.

As a comparison, in Q1 2023 OMV's total production was 376 kboe/day. The Neptun Deep field is almost 40% of that in total and 20% considering the 50/50 partnership with Romgaz. Production cost was USD 9.3/boe in Q1 2023, so significantly higher than the Neptun Deep field. I think it is fair to say that the Neptun Deep field is a big deal for OMV in a positive way.

Just a few days later OMV could announce that the Norwegian Ministry of Petroleum and Energy has approved its Plan for Development and Operation for the Berling gas and condensate discovery. The discovery was already made in 2018. First gas and condensate production should start in 2028 and the estimated gross recoverable resources are expected to be around a total of 45mn boe. OMV (Norge) AS is operator of the fields and has a 30% share. License partners are Equinor ASA (NYSE: EQNR ) and DNO ASA ( OTCPK:DTNOF , OTCPK:DTNOY ) with shares of 40% and 30%.

Both developments are much aligned with the OMV Strategy 2030 which plans for a temporary increase in natural gas supply as energy bridge/transition fuel.

ADNOC takeover of Borealis is unlikely - in my view

There have been rumours that ADNOC (Abu Dhabi National Oil Company) is interested in taking over Borealis, or at least increasing its 25% stake. 75% are currently owned by OMV. OMV had bought a majority in the Chemicals company not a long time ago from Mubadala Investment Company , a large state-owned Abu Dhabi investment vehicle. So in some ways this would a rollback of that transaction.

The interest of the state-owned company from Abu Dhabi is understandable, and Abu Dhabi is maybe feeling seller's remorse. Ironically the deal was criticized in 2020 by most analysts as being too expensive.

I have been doing a lot work in the United Arab Emirates over the last couple of years. To me it seems that everybody understands here that peak oil is close, and there is a rush to capitalise on the good times and diversify while this is still possible. Abu Dhabi cannot compete with Dubai on glitz and glamour, but it has most of the oil and gas resources - the national oil company is called Abu Dhabi National Oil Company for a reason.

ADNOC probably wants to secure access to future technologies in chemistry, like expertise in chemical recycling that enables a circular economy in which materials are reused in the best possible way. But the UAE company is probably also looking for takeover objects and manufacturing capacities in which the output of their huge petrochemical plants can be processed into higher-quality plastics.

Covestro ( OTCPK:CVVTF , OTCPK:COVTY ), the German chemicals company ADNOC is also interested in, and Borealis are quite similar in this regard.

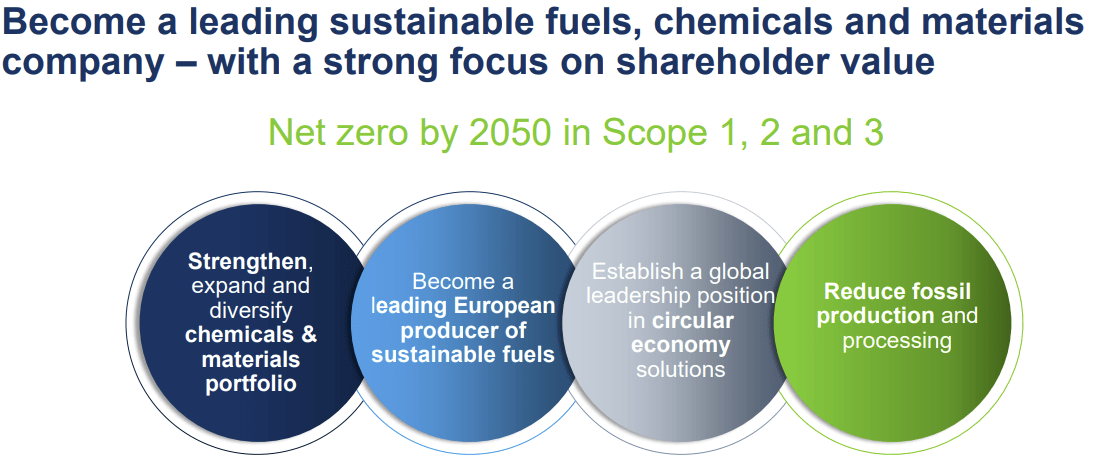

In my view it is unlikely that OMV will sell Borealis. ADNOC's supposed intent - to diversify into chemicals - is key to the Strategy 2030 which OMV has given itself just last year. A sale of Borealis would leave OMV in a strange place as the company would diminish its long-term vision for the transformation away from oil and gas to chemicals, materials, and recycling. Borealis plays a key role here and OMV would definitely have to completely rewrite its Capital Market Story .

OMV Capital Market Story (Source: OMV)

{kind=link}

(Note - fellow analyst Christian Liu has a different opinion here. Maybe you check out his article, OMV AG: There May Be The Chance To Make A Deal With ADNOC , to compare.)

Conclusion

OMV is an integrated oil and gas company with an ambitious transformation strategy away from oil and gas exploration towards sustainable fuels, chemicals, and materials.

The company has a strong focus on shareholder value and the sound balance sheet with very low debt should give ample financing capability for the transformation while maintaining high cash flows.

Together with the low valuation, this makes it a good pick for income investors.

For further details see:

OMV: Reiterating The Buy Recommendation