UA - On Holding: Clouds And Circularity

2023-04-03 16:23:09 ET

Summary

- On is revolutionizing running — makes you feel like you're running on clouds.

- On is building a culture — igniting the power of the Human Spirit through movement.

- On is creating circular systems — Cyclon could produce near-100% Gross Margin and generate software-like Revenue for On.

- The company possesses strong technology, brand, and cost advantages moats.

- Shares seemed to be trading at fair value — but keep an eye out for cash flow.

Bought my first pair of On running shoes a few weeks ago... I love them.

The next thing I know, I'm researching everything about the company and contemplating buying another pair. Cloudmonster perhaps?

Here's a deep dive into On Holding ( ONON ). Enjoy!

Investment Thesis

While the sporting goods industry declined as a whole, On's business continued to "take off".

Despite the outperformance, excess inventory, waning consumer sentiment, and negative cash flow are still major concerns for On.

However, On has strong technology, brand, and cost advantages moats to help the company weather an economic storm and capture market share.

Despite phenomenal growth numbers in FY2022, On still has a long growth runway ahead. Launching new products, expanding geographically, and introducing circular systems represent some of the growth opportunities for On.

Given its growth potential and superior profitability, shares seemed to be trading at fair value — but keep an eye out for its cash flow.

History

On was founded in the Swiss Alps in 2010 with the goal of revolutionizing running.

Retired athlete Olivier Bernhard — a three-time world duathlon champion and multiple Ironman winner — wanted to create a running shoe that would give him the perfect running sensation.

I always felt there was room not for another running shoe but for a different running feel. I had no clue how to build or manufacture a running shoe, but I had this vision or dream that stuck with me [where] I really wanted to bring that different feel to life in a running shoe.

(Olivier Bernhard — Behind the Brand With On Running's Olivier Bernhard )

Bernhard developed the first On shoe prototype by gluing pieces of a garden hose to a running shoe which creates a spring-like mechanism for a softer landing and better take-off. Bernhard took it for a test run, and that's when he felt something unusual — he felt like he was floating above the ground like he was running on clouds.

{kind=link}

Excited by his new invention, Bernhard shared his idea and prototype with Nike ( NKE ). Back then, Bernhard was sponsored by Nike, so naturally, Nike was the first place to go since the company has all the resources needed to make his dream into reality.

His idea was rejected outright as the shoe prototype was "hideous".

Determined to get his idea off the ground, Bernhard worked with a Swiss engineer and developed more prototypes of what could be the next big thing in sports footwear.

Bernhard then pitched his idea to his friends David Allemann and Caspar Coppetti. Unlike Bernhard, they were amateur runners. However, they had excellent business acumen given their experiences in the corporate world.

Soon after, the trio shook hands, and On was formally established in January 2010. Their goal was to create the most high-performance running shoes ever, guided by two overarching features: cushioned landings and powerful take-offs.

The three of them wasted no time refining their prototypes and finalizing the design and technological components of the shoe. A couple of months later in March 2010, On's revamped prototypes won the ISPO BrandNew Award — one of the most prestigious prizes for sports innovation, selected from over 300 sports startups worldwide.

In 2012, On launched its first shoe ever, the Cloudracer. The shoe was featured in the Wall Street Journal's list of revolutionary running shoes .

On Holding: Cloudracer

With increased publicity and chatter about this new running company, On started to gain traction in a few markets. The three founders quickly realized that they needed to expand the team to scale and professionalize the business.

In 2013, two new executives joined the team: Martin Hoffmann as CFO and Marc Maurer as COO. The five (equal) partners worked collaboratively with the three founders focusing on innovation and product development while Martin and Marc devotes their time to operational and administrative matters.

A year later, On launched the On Cloud, which won the company its second ISPO award, the ISPO Gold Award for Best Performance Footwear 2015/2016 .

On Holding: On Cloud

In the following years, On launched more and more models (which I'll briefly discuss later in the next section), packed with upgraded technology. On has always been laser-focused on running shoes, but that changed in 2016 when the company decided to introduce its own performance running gear, which made its expansion to sports apparel official.

While the company specializes in running, it pursuing a greater mission:

Mission : Ignite the power of the Human Spirit through movement.

Even though On has its successes as an emerging sports tech startup, few believed in the long-term prospect of the company as the industry has always been dominated by big players like Nike and Adidas ( ADDYY ) — since its inception, On had only three funding rounds from three separate investors.

In its pre-seed round, investor-entrepreneur Philippe Bubb wrote the first check to On and became its chairman from 2013 to 2018.

In its Series A round, Stripes was the sole investor. The New York-based private equity firm advised On with team building, international expansion, and growing its DTC business.

The first two funding rounds had little to no publicity for the brand. But it all changed when 20-time Grand Slam winner, tennis legend Roger Federer became an investor in the company. In 2019, he invested an undisclosed amount in the company, which not only validates the product and management team behind On, but also provided the brand exposure On needed to be a global sports brand.

Two years later, On went public in 2021, raising $746 million. It is now one of the fastest-growing sports brands out there with more than $1 billion in sales achieved in just 13 years.

Value Proposition

In a nutshell, On offers innovative, high-performance premium footwear, apparel, and accessories for running, outdoor, and all-day activities.

At the very core of On is its premium footwear. The company specializes in running shoes but has since expanded into other categories such as tennis, hiking, and lifestyle sneakers. The price of each pair of On shoes ranges from $129.99 to $269.99.

Below are the different categories of footwear which On offers:

{kind=link}

According to the company's website, here are the different models in each category. Note that some models are more versatile than others, and thus, fall into multiple categories:

| Category |

| Model |

| Road Running |

|

| Trail Running |

|

| Competition |

|

| Tennis |

|

| Indoor/Training |

|

| Hiking |

|

| All-Day Wear |

|

Perhaps, one of the reasons why customers buy On shoes is because it looks futuristic and unique , especially because of their cloud soles. Another reason would be its high-quality construction , which feels durable, comfortable, and expensive. In addition, advanced technology built into each shoe could be the main determining factor in customers purchasing an On shoe.

For me, it's all three. But I would put more weight on the technological aspects of the shoe. Here's why.

Just a week ago, I took my new Cloudswift for a run and wow, I really do feel like I'm running on clouds. You see, I've not run for many months so I expect some pain/soreness in my soles, ankles, and knees. To my surprise, my run felt painless and comfortable, which allows me to focus more on my pace and breathing. I've had joint pain issues with other shoe brands but not On running shoes which is why I think On has a technological advantage among peers (and also why I plan to get another pair).

{kind=link}

Cushioned landings and powerful take-offs. These are the basic concepts that make On running shoes effortless to run on. Digging deeper, here are the different technologies that make it seem like you're running on clouds:

- CloudTec : This is the technology behind the little cloud-like pods that run the whole length of the sole. It serves as the cushioning system that delivers soft landings and powerful take-offs. It reacts and adapts to your running style, compressing horizontally and vertically based on your movements. CloudTec forms the foundation of every On shoe.

- Speedboard : CloudTec works in unison with Speedboard, which is a responsive, semi-stiff board that connects the cloud-like pods to the upper of each shoe. The primary role of the Speedboard is to increase the runner's speed by converting the kinetic energy of each landing into a more explosive take-off. The material, shape, thickness, and curve of the Speedboard also adapt to the runner's unique movement and foot shape, providing optimal comfort and speed.

- Helion : The CloudTec sole in all On shoes is made of Helion, which is On's proprietary superfoam that is lightweight, flexible, and responsive. It allows for smoother, effortless runs.

- Missiongrip : Some of On shoes are specially designed for offroad running and these shoes are equipped with Missiongrip, which is a rubber compound that gives enhanced grip and traction on rough terrain.

{kind=link}

Besides shoes, On sells apparel and accessories as well but I won't go into detail as they do not make up a large portion of the company's revenue.

Market Opportunity

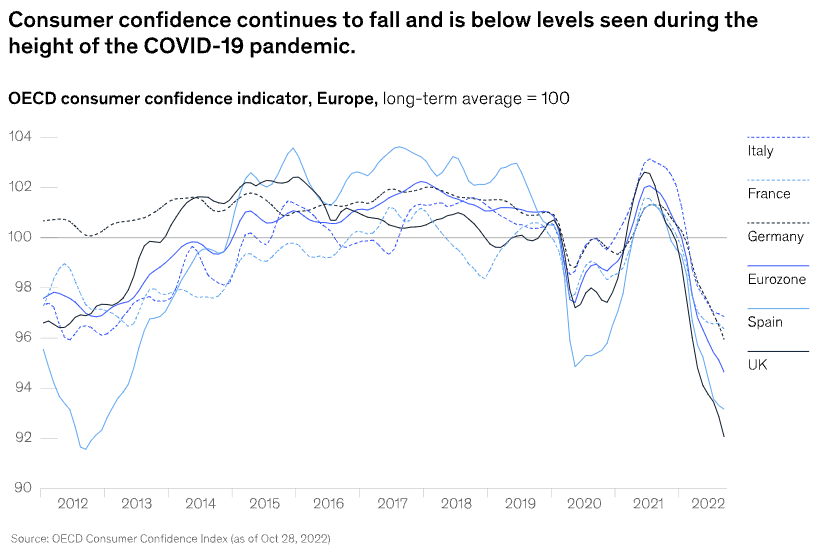

The last few years have been nothing but a roller coaster ride for the sporting goods industry. First, COVID-19 hit global markets in 2020, which forced many companies to shut down operations for a while. It caused major strains in the global supply chains in the better part of 2020 and 2021.

Then there's the Russia-Ukraine war, which caused massive inflation in raw materials and energy costs, prompting companies to raise prices. To make matters worst, the blistering hot economy and labor markets forced the Fed to hike interest rates at a record-breaking pace, causing companies all over the world to rethink their capital allocation strategies. In addition to a looming global recession, consumer confidence showed signs of increasing pessimism.

{kind=link}

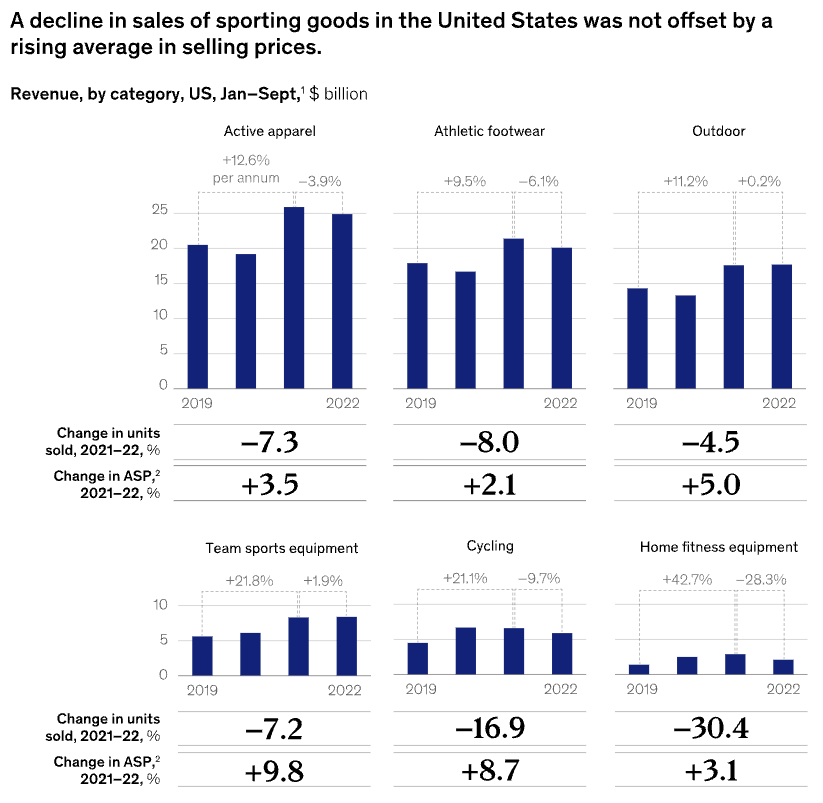

While many industries saw major declines in operations, sporting goods seemed to be one of those resilient sectors of the economy. As you can see below, each category in the US sporting goods industry has outperformed pre-pandemic levels as increasing awareness of health, fitness, and sports buoyed consumer spending.

{kind=link}

On a cautious note, Sales declined YoY in 2022. For instance, Active Apparel and Athletic Footwear (categories where On operates) saw sales drop by 3.9% and 6.1%, respectively — companies in these categories were able to raise average selling prices, but were not enough to offset declines in units sold.

Although the COVID-19 situation has materially improved since the early days of the pandemic, companies placed large orders in 2022 to build up inventory in anticipation of high demand and to avoid the supply chain challenges of 2021. Heading into 2023, companies thus have higher inventory levels but given declining consumer discretionary spending, they need to do more than just raise prices to boost productivity.

While the industry as a whole saw YoY declines, On was able to gain market share, outpacing the growth of the industry. In other words, as the rest of the industry struggles against a challenging macroeconomic backdrop, On continues to grow at a rapid pace. Still, the main concern would be if On can unload excess inventory amidst falling consumer demand. We'll discuss this further later in the financials sections.

Nevertheless, the running industry, in particular, is booming. Running brands are currently seeing sales increases of up to 60% to 70% . Newcomers are joining the running revolution — a survey found that one in six of respondents has only started running in the past two years. The number of respondents that had taken part in a running race in 2021 has dropped to just 58%. This was the lowest figure in the history of the survey, which has historically been as high as 80%, showing an influx of beginner runners in recent years.

Most runners also own more than one pair of running shoes. According to the survey, runners in Germany own six pairs of running shoes on average, having spent an average of 377 euros a year on running shoes.

With the rush of new runners, the opportunity lies in building brand loyalty among consumers, thus attracting repeat buyers.

The running gear market alone is quite massive, as quantified by several market research agencies:

- Market Research Future — $62 billion by 2030

- IMARC Group — $56 billion by 2027

This is just the running gear market alone — as a sporting goods brand, On has tons of optionality in terms of expanding into other categories such as basketball, soccer, yoga, athleisure, weightlifting, and so on. These markets open significant opportunities for On to grow further, expanding beyond its identity as a running-specific brand.

The biggest challenge for On would be growing brand awareness and loyalty in an industry dominated by giants like Nike and Adidas, as well as intensified competition from smaller brands such as Allbirds ( BIRD ) and Hoka ( DECK ). In addition, offering unique value propositions, whether through advanced technologies or eye-catching designs, is equally important for long-term success.

Business Model

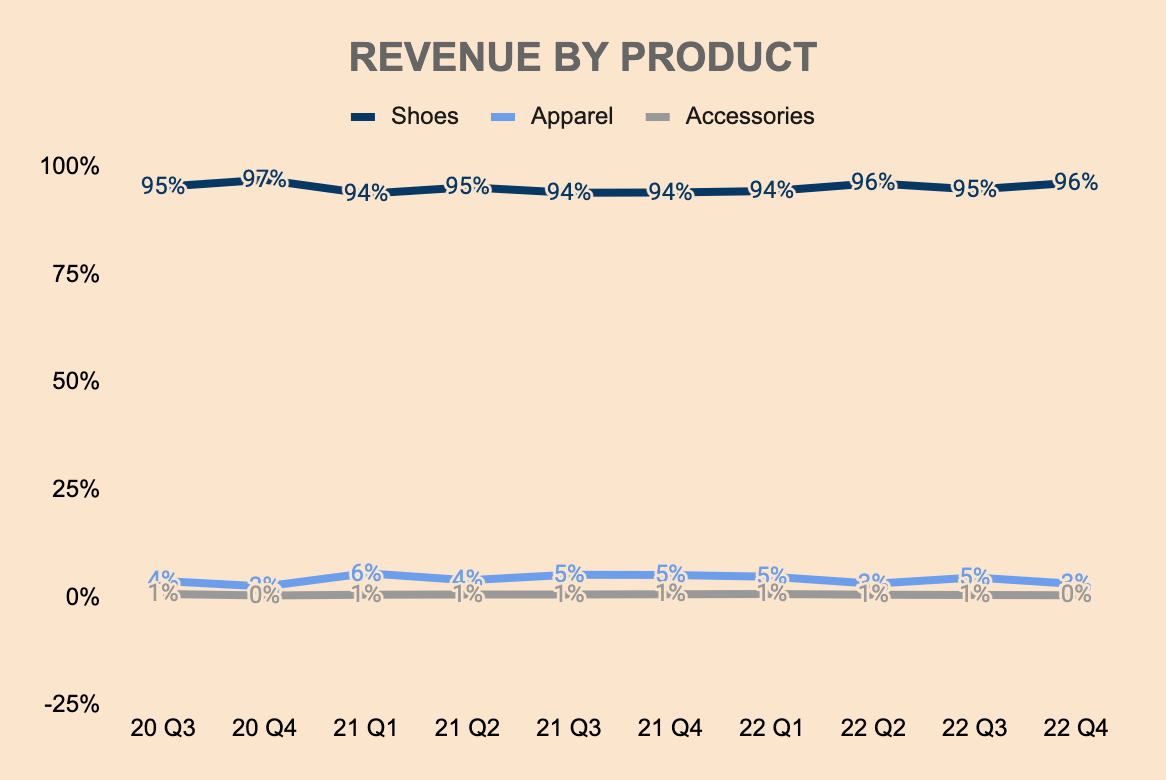

On operates a rather simple business model, primarily generating Revenue from selling three types of premium performance products: shoes, apparel, and accessories.

The graph below shows Revenue by Product as a % of total Revenue. As of Q4, shoes make up the bulk of total Revenue, at 96%, while its apparel and accessories segment make up much smaller portions of the business, at 3% and less than 1%, respectively.

ONON Investor Relations and Author's Analysis

{kind=link}

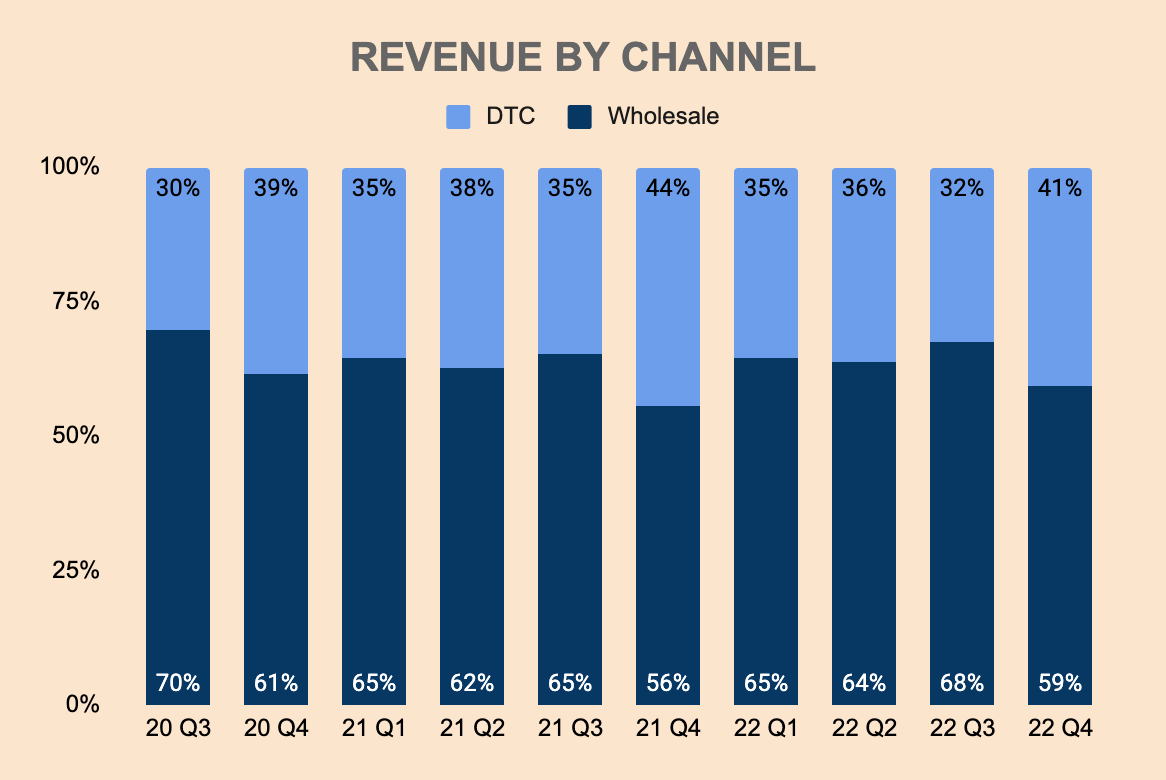

The company generates Revenue through two channels, namely DTC and Wholesale. DTC Revenue comprises sales that occur directly through On's website and retail stores. Wholesale Revenue consists of sales to wholesale customers such as international distributors and large retailers like REI, Nordstrom ( JWN ), and Foot Locker (FL).

As of Q4, DTC makes up 41% of the business while Wholesale accounts for 59% of total Revenue.

ONON Investor Relations and Author's Analysis

{kind=link}

Growth

Note: unless otherwise stated, all of On's financial figures are denominated in Swiss Francs (CHF).

Let's dive into On's financials, starting with its growth metrics.

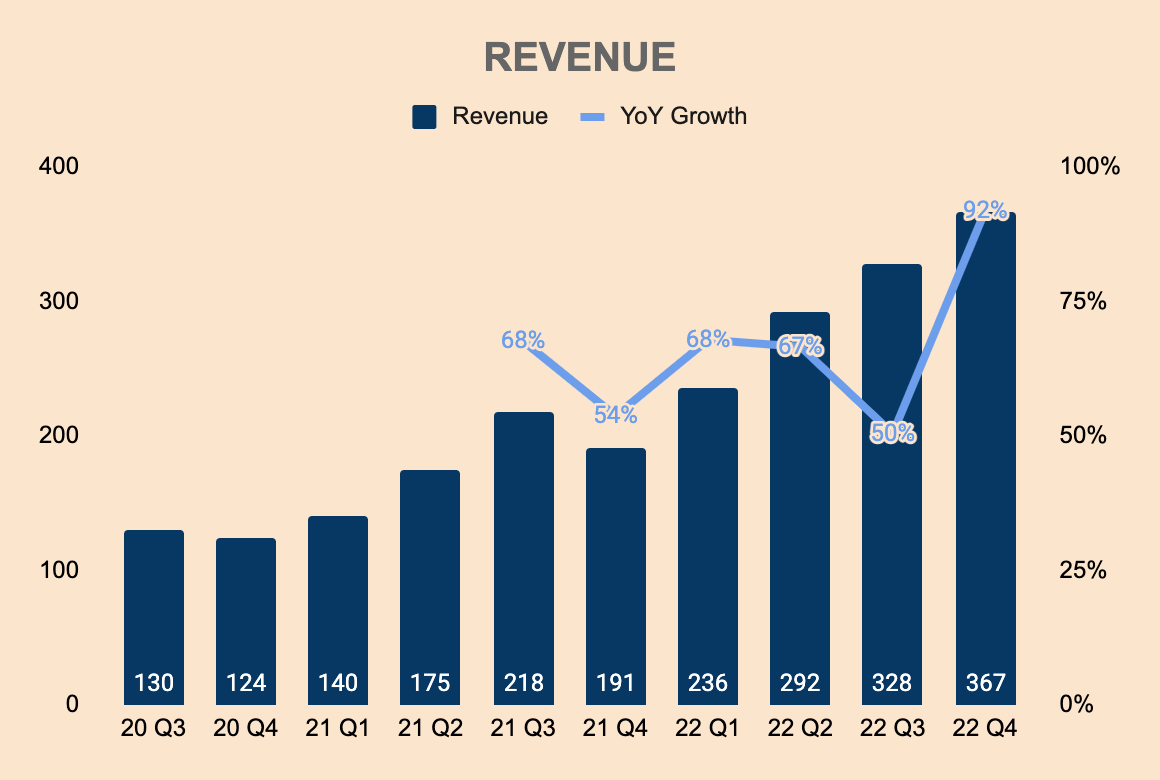

2022 Revenue was CHF 1.2 billion, which was a 69% increase from 2021. In Q4, Revenue was CHF 367 million, a 92% YoY increase and a major beat on analyst estimates. As you can see below, Revenue accelerated in Q4 driven by strong demand during the holiday season across regions and channels. The normalization of inventory levels was also a key contributor to growth:

91.9% Q4 net sales growth year-over-year is the result of the strength of the brand that we have built in 2022 combined with the good product availability following a further normalization of product supply in our warehouse operations.

In Q4 2021, we were unable to fulfill all the demand due to supply shortages and low inventory levels as a result of the factory closures in Vietnam during the third and fourth quarter of ‘21.

(CFO and Co-CEO Martin Hoffman — ONON 2022 Q4 Earnings Call )

ONON Investor Relations and Author's Analysis

{kind=link}

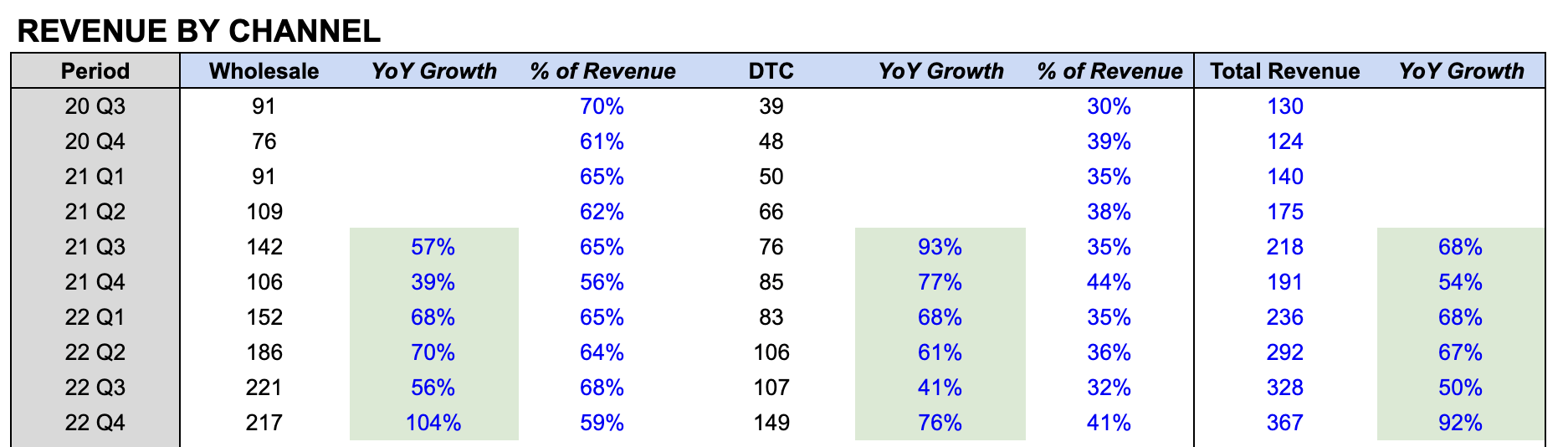

Looking at the different channels, its Wholesale channel was the star of the show, more than doubling, to CHF 217 million in Q4. This was due to continued growth within existing wholesale customer stores as well as the launch of new wholesale partnerships. On ended the year with 9,200 wholesale stores, compared to 8,000 doors in 2021.

Wholesale Revenue as a % of Revenue increased to 59% in Q4, compared to 56% a year ago. The reasons for this expansion were the strong recovery in wholesale stores following lockdowns and shopping restrictions in Q4 of 2021, as well as the normalization of operations in its US East Coast warehouse.

ONON Investor Relations and Author's Analysis

{kind=link}

In Q4, DTC Revenue was CHF 149 million, a 76% increase YoY, driven by increased website traffic. On's e-commerce platform saw 39.7 million visits in Q4, an increase of 44% from 27.5 million visits in the same period last year. Moreover, DTC Revenue benefited from the opening of additional retail stores globally.

DTC Revenue makes up 41% of Revenue in Q4. In my view, this figure could increase to more than half of the business as the company expands its company-owned retail stores, and more people gain awareness of the brand.

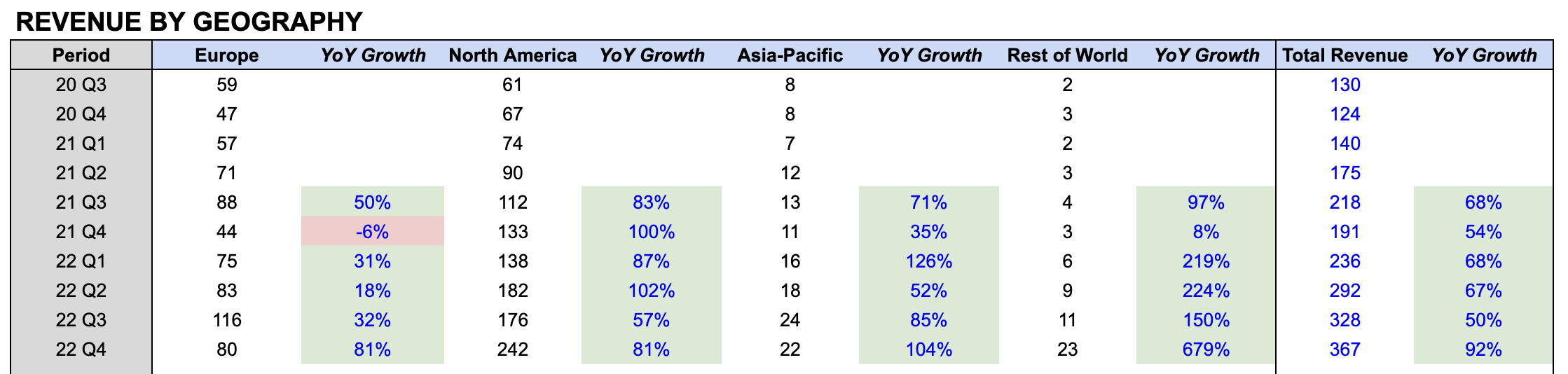

In terms of geography, Revenue growth was robust across all regions.

As previously mentioned, the supply chain problems and COVID-19 restrictions experienced in 2021 Q4 had negatively impacted key markets outside of the US, which is why Revenue growth for that quarter was lackluster in those regions. However, as the supply chain stabilizes and pandemic restrictions eased, these markets returned to growth mode in Q4 of 2022, as seen by the 81%, 104%, and 679% growth in Europe, Asia-Pacific, and Rest of World markets, respectively. The growth spurt in Rest of World segment is due to the successful entry into new markets in Latin America and continued growth in UAE and Israel.

The US also has its fair share of supply chain problems. In Q3 of 2022, there was a temporary slowdown caused by warehouse disruption, but growth accelerated in Q4 as operations improve. In Q4, North America sales were CHF 242 million, an 81% increase from last year.

ONON Investor Relations and Author's Analysis

{kind=link}

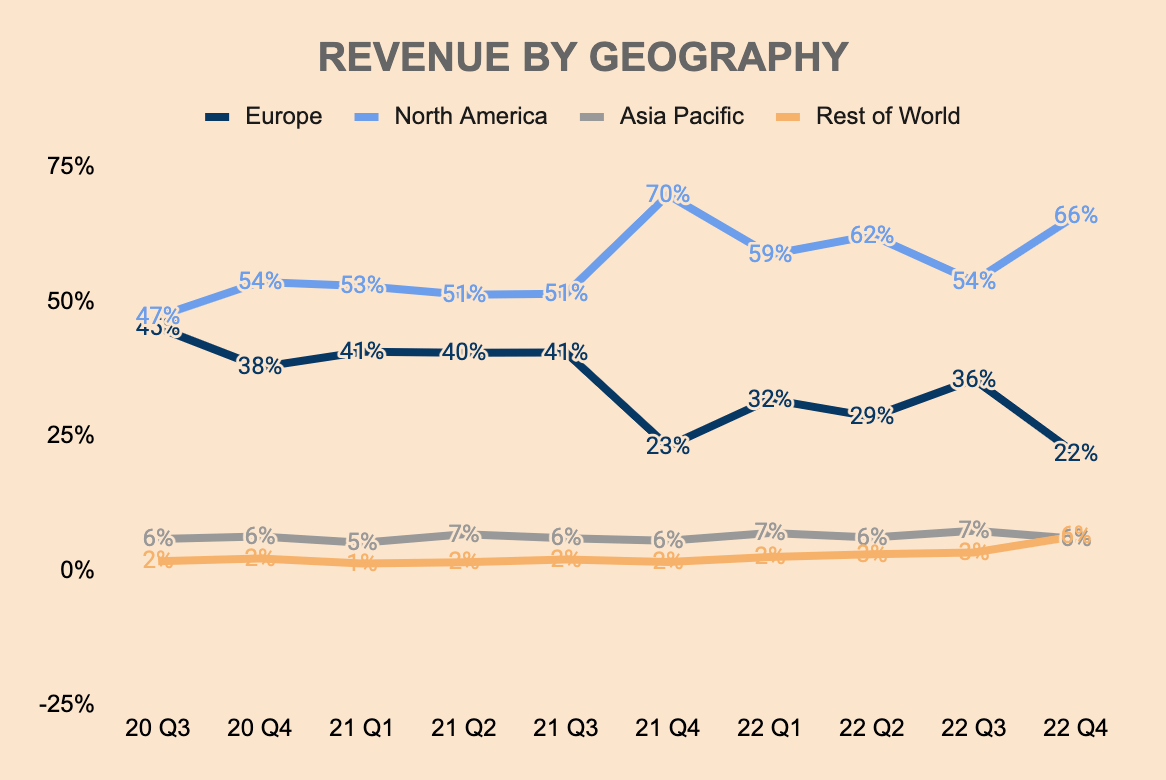

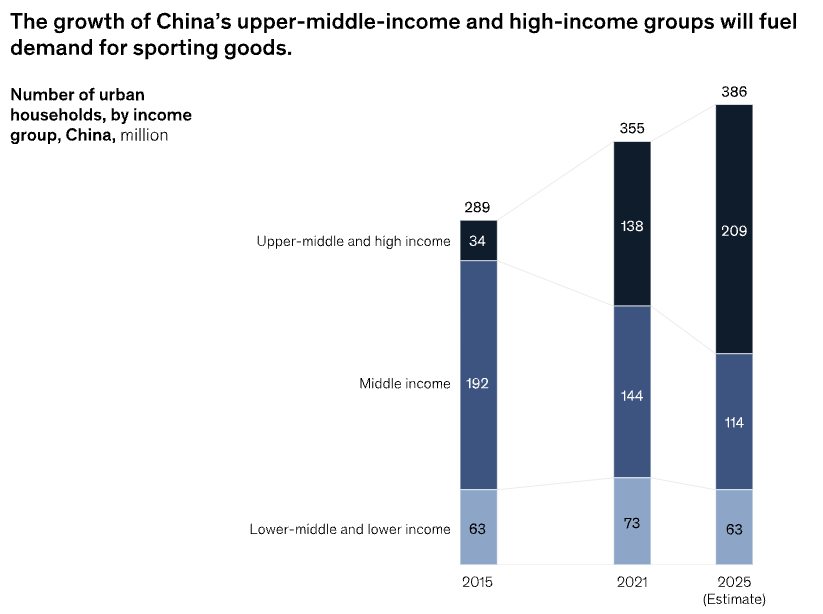

As a % of Revenue, Europe and North America make up the bulk of total Revenue, at 22% and 66%, respectively. Although Asia-Pacific only makes up 6% of the business, there's substantial growth potential in this region, especially in China.

ONON Investor Relations and Author's Analysis

{kind=link}

It seems that On is really focusing on its growth expansion plans in China. According to its annual report , On opened three retail stores in 2022, bringing the total number of company-owned retail stores to 18. Of these 18 stores, 13 operate within China. Perhaps, management sees a massive opportunity in the Chinese market, as the growth of the country's upper-middle and high-income groups is expected to significantly increase demand for premium sporting goods like On. In other words, On is skating to where the puck is going to be. That said, expect Asia-Pacific to make up a larger portion of the business in the years to come.

{kind=link}

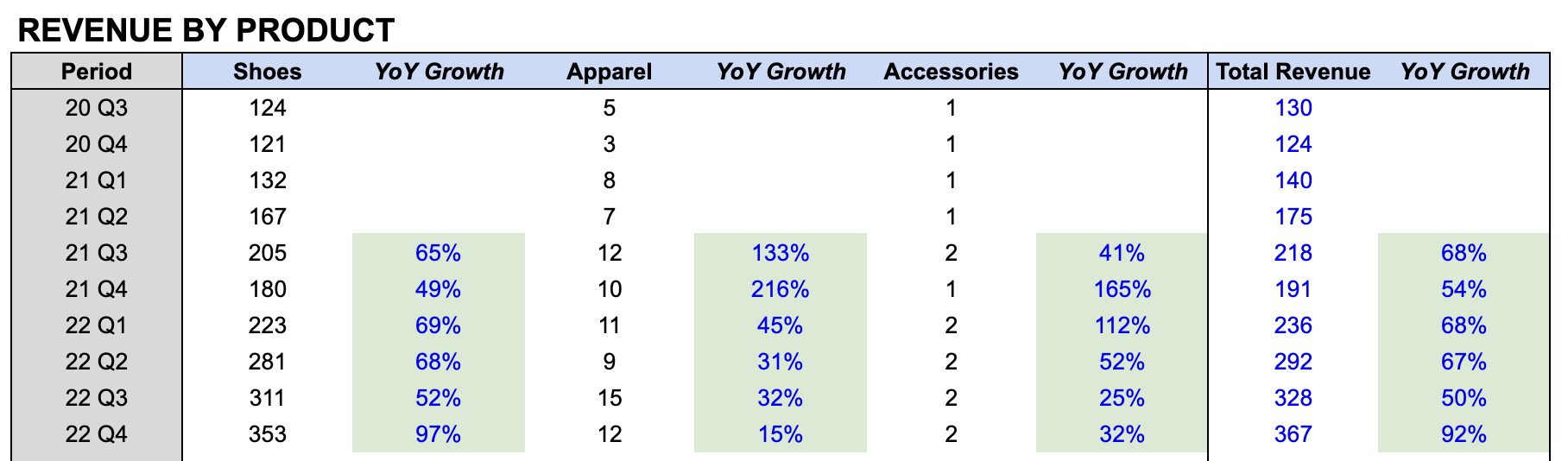

Switching over to product type, Shoes saw the largest growth in Q4, reaching CHF 353 million in Revenue, which was a YoY increase of 97%. Growth in this category was driven by updates to existing models and the launch of new products in 2022 such as the Cloud 5, Cloudmonster, Cloudrunner, Cloudgo, and Cloudrift.

We continue to gain market share in the running community especially with the Cloudmonster, the Cloudrunner and the CloudGo. While at the same time, the Cloudnova is winning more and more younger fans. In Q4, we launched the new CloudX, another key franchise that strongly resonates with the fitness community. And that continues to win market shares in gyms around the world. The CloudX is also our most sold product in China.

(CFO and Co-CEO Martin Hoffman — ONON 2022 Q4 Earnings Call )

ONON Investor Relations and Author's Analysis

{kind=link}

Apparel Revenue grew by 15% YoY, to CHF 12 million. This was primarily driven by increased own retail stores and shop-in-shop environments. Revenue for the category decelerated though, due to fewer new products launched in Q4, as compared to the same period in the previous year.

All in all, On showed explosive growth despite a challenging macroeconomic environment. Elevated brand awareness and continued retail expansion were the drivers of growth. On still has massive growth opportunities ahead as it continues to relentlessly introduce new technologies, expand to other categories, and build its global presence. As the numbers suggest, On has a powerful brand that resonates well with consumers, a key differentiating factor and long-term asset that will be crucial for On's journey towards profitable growth.

Profitability

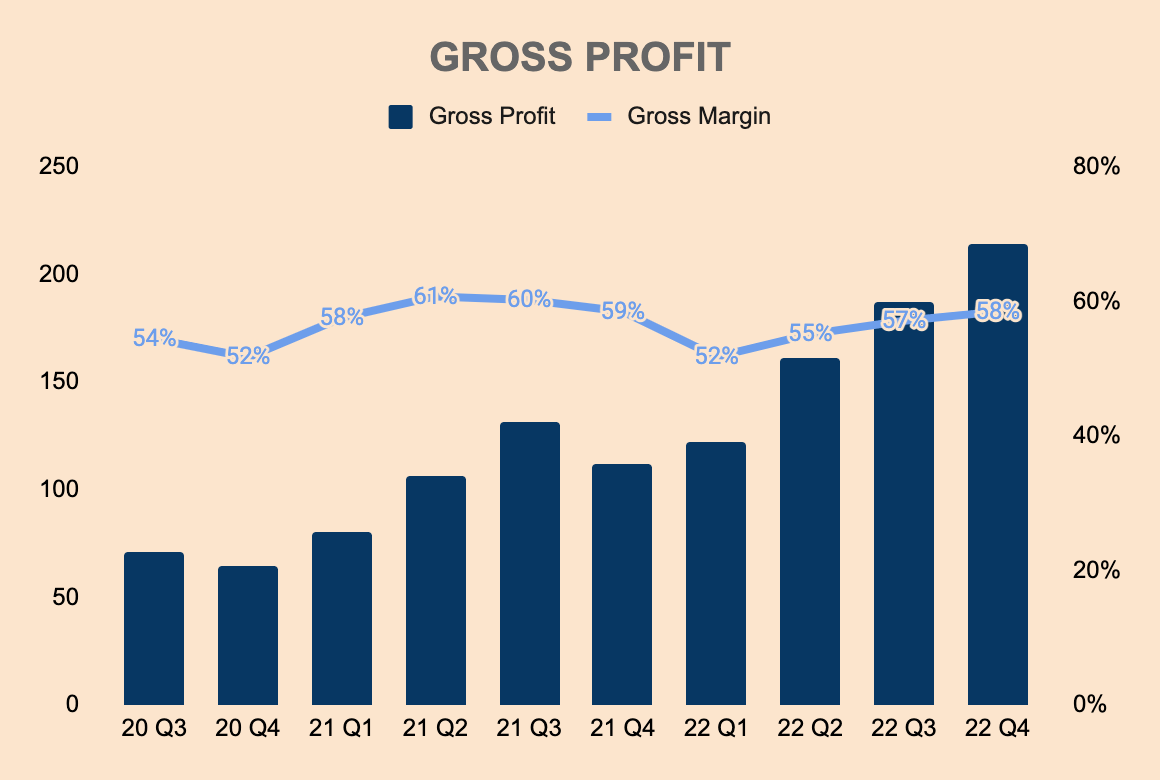

Turning to the profitability of the company, On produced CHF 685 million in FY2022. This represents an industry-leading Gross Margin of 56%, compared to peers such as Nike, Adidas, and Under Armour ( UA ), which have Gross Margins of 44%, 48%, and 42%, respectively. Such a superior Gross Margin profile means higher earnings potential for On.

ONON Investor Relations and Author's Analysis

{kind=link}

As shown above, Q4 Gross Margin was 58%, a slight decrease from last year's 59%. Gross Margin decreased due to several factors, including 1) higher air freight expenses to expedite order fulfillment; 2) currency exchange pressures, and; 3) the outperformance of the Wholesale segment, which typically has lower margins than the DTC side of the business.

Nevertheless, as macroeconomic conditions improve, and as the DTC segment expands, On's Gross Margin should increase further. Through economies of scale, I see a clear path for Gross Margin to reach the low-60s.

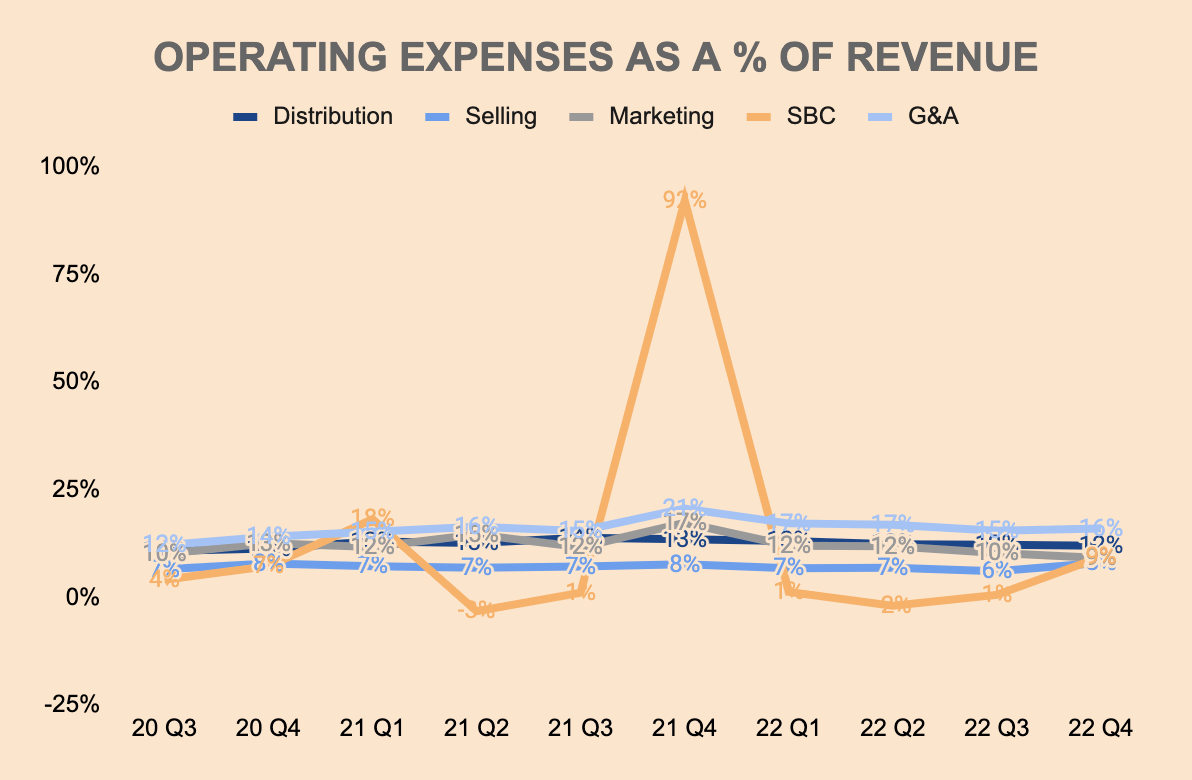

Moving down the income statement, we can see how the different components of Operating Expenses have trended as a % of Revenue. The clear outlier is Share-Based Compensation, which spiked in Q4 2021 following the company's IPO in that quarter. 2021 Q4 SBC was CHF 176 million but has gone down significantly ever since. As of 2022 Q4, SBC was only CHF 34 million, and the decrease was due to lower grant valuations as a result of lower share prices.

ONON Investor Relations and Author's Analysis

{kind=link}

As for the other components of Operating Expenses, as a % of Revenue, they have all slightly improved YoY as the company achieves operating leverage.

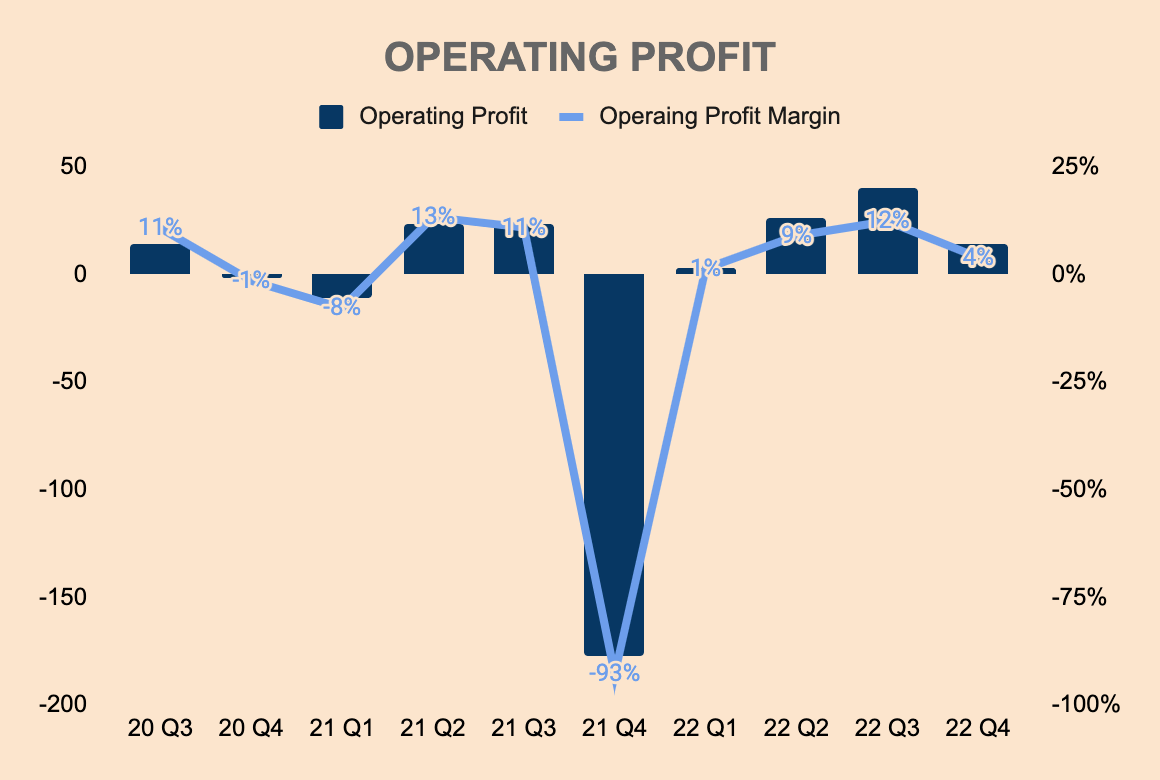

Operating Profit for FY2022 was CHF 85 million, which is a 7% Operating Margin. You can see that Q4 Operating Margin took a dip from Q3's 12% Operating Margin. This was primarily due to higher SBC and Selling expenses in Q4, as compared to Q3.

ONON Investor Relations and Author's Analysis

{kind=link}

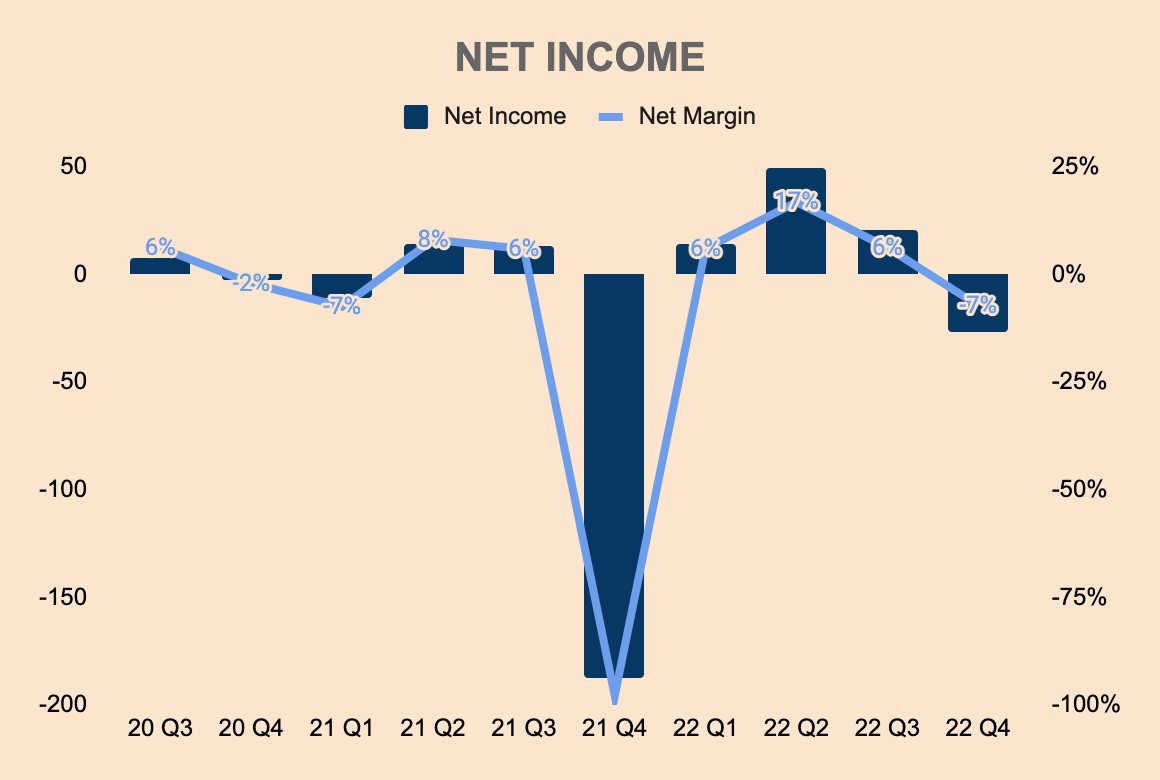

Looking at the company's bottom line, FY2022 Net Margin came in at 5%, a major improvement from FY2021's Net Margin of (24%). Do notice that Q4 Net Margin dipped into negative territory. This was due to currency exchange pressures from fluctuations in the CHF/USD exchange rate. As global conditions improve and currency exchanges stabilize, On should return to profitability.

ONON Investor Relations and Author's Analysis

{kind=link}

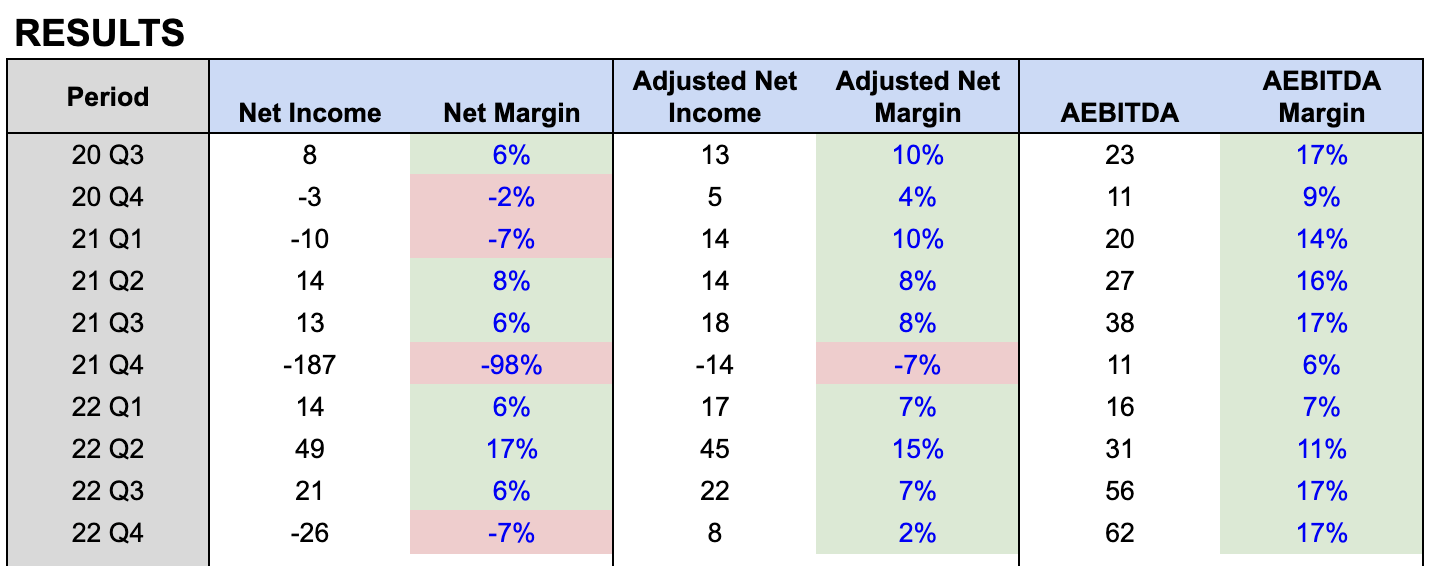

For reference, here's what On's Net Income, Adjusted Net Income, and Adjusted EBITDA looked like over the last few quarters. AEBITDA excludes depreciation, foreign currency exchange, and SBC expenses.

ONON Investor Relations and Author's Analysis

{kind=link}

To summarize, On is showing strong and improving profitability despite growing at such a rapid clip. It's quite rare to see a high-growth small-cap company achieve profitability in this market environment.

On has strong earnings potential and has demonstrated operating leverage within its business model. The real competitive advantage comes from its superior margin profile, which should reward shareholders in the long run if it can maintain pricing power amidst a sea of competition and deteriorating consumer sentiment.

Financial Health

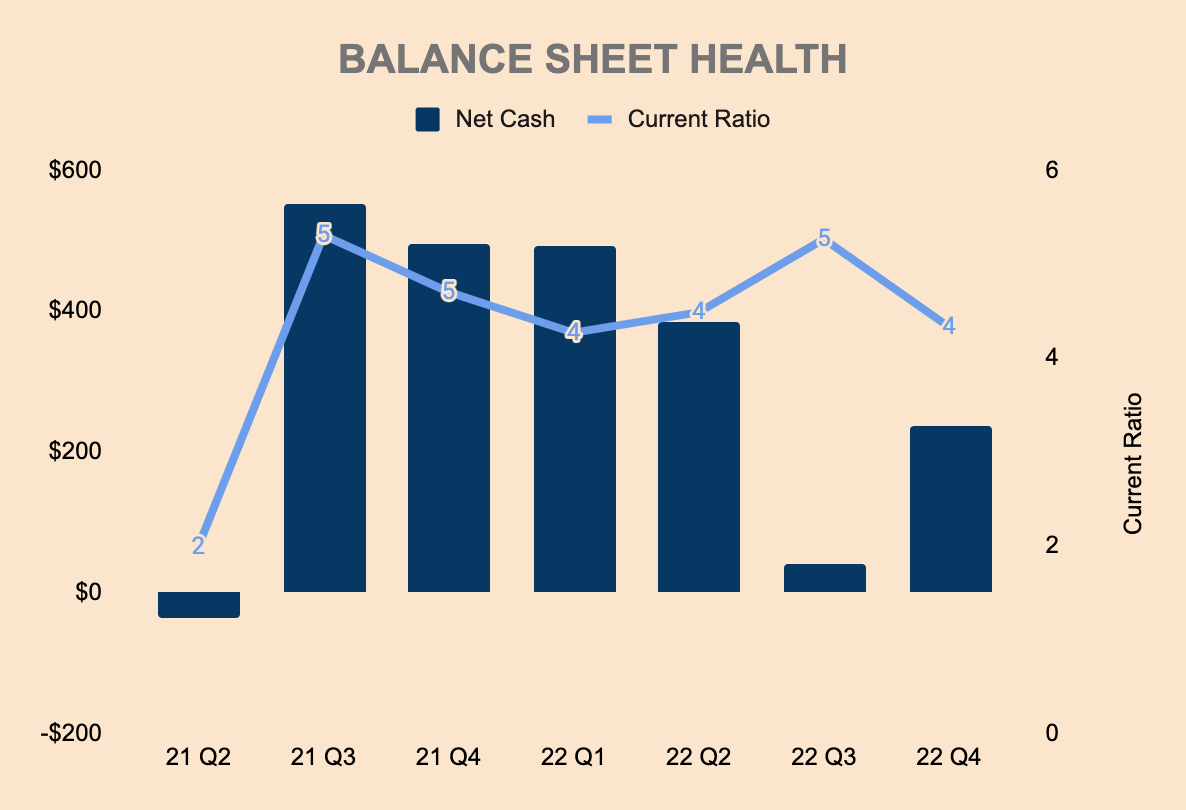

At first glance, On seemed to have a strong balance sheet. The company holds CHF 397 million of Cash and Short-term Investments with CHF 160 million of Total Debt. That leads to CHF 237 million of Net Cash available. Current Ratio is also at about 4x, which is quite liquid.

ONON Investor Relations and Author's Analysis

{kind=link}

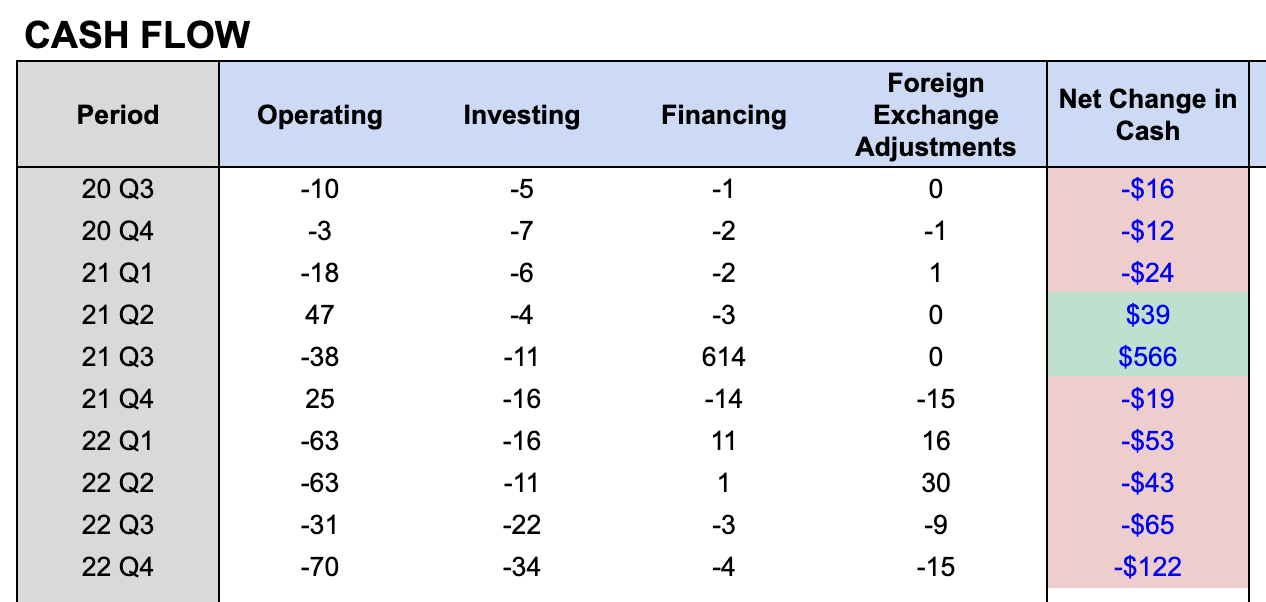

However, the company doesn't seem to be managing working capital efficiently. In FY2022, On's Cash Flow from Operating Activities was CHF (227) million, a plunge from CHF 17 million in the previous year. This was due to Net Working Capital increasing 145% YoY to CHF 459 million, largely driven by an increase in Inventory levels in anticipation of strong demand in 2023.

In addition, On is also reinvesting in the business for expansion. Cash Flow from Investing was CHF (83) million in FY2022. As a result, the Net Change in Cash was CHF (282) million in FY2022. If On maintained this level of cash burn, it would wipe out its Net Cash position entirely, which could force the company to raise capital elsewhere, diluting shareholders in the process.

ONON Investor Relations and Author's Analysis

{kind=link}

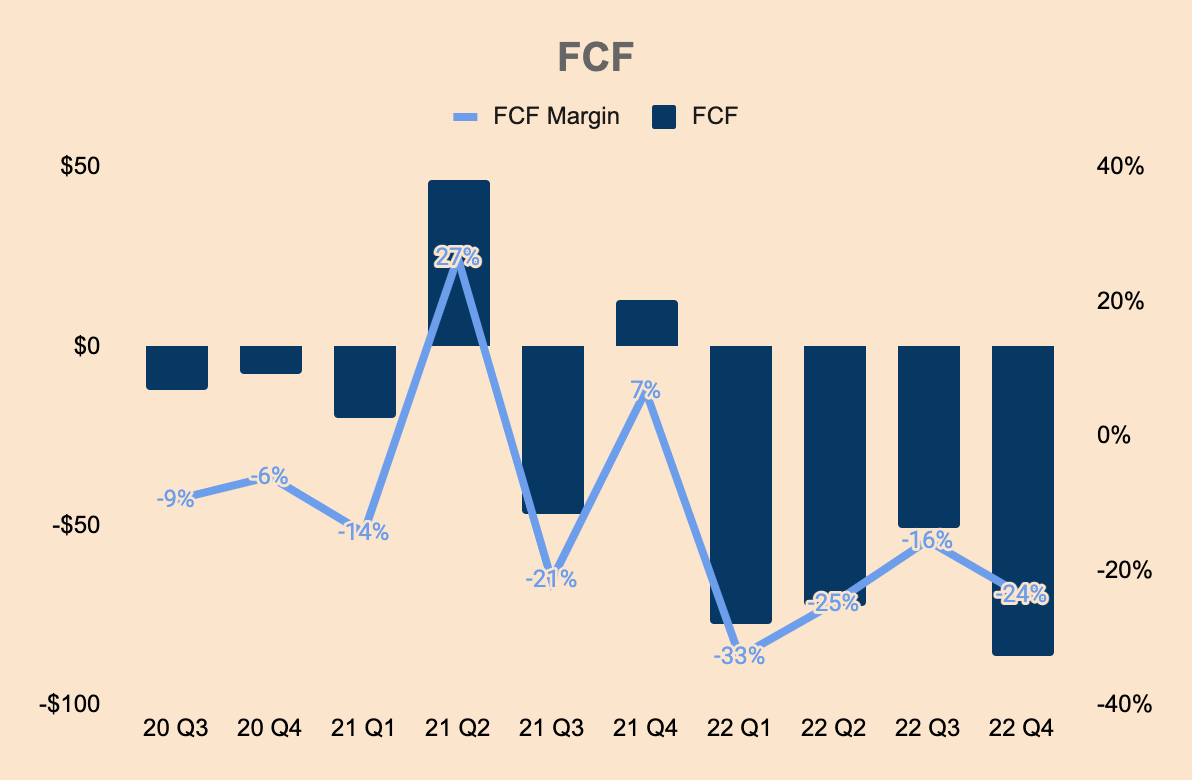

As you can see, On is burning lots of cash. FY2022 Free Cash Flow was CHF (287) million. Excess inventory and worsening consumer sentiment are not a great combo for On — management needs to manage working capital more carefully. On doesn't want to offload its inventory at steep discounts, which could damage its brand reputation as a premium footwear company.

ONON Investor Relations and Author's Analysis

{kind=link}

To add fuel to the fire, not all of On's cash in hand may be readily available — some of it could actually vanish into thin air. As we've seen in recent weeks with banks like Silicon Valley Bank and Credit Suisse, it is possible that one or more of On's smaller, weaker bank partners collapse, which would add more pressure on On's balance sheet.

As at December 31, 2022 and 2021, 90.4% and 94.9%, respectively, of our cash and cash equivalents were held at banks that are deemed systemically important financial institutions, with remaining balances in banks with an investment grade rating.

(On Holding — FY2022 Annual Report )

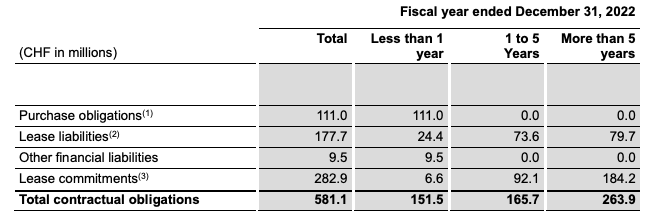

In my view, On's balance sheet may be at risk here. The company also has CHF 152 million of contractual obligations in the next year. If On built too large of an inventory and if sales didn't turn out as robust as management expected, On may be forced to raise additional capital, which would dilute shareholders.

On Holding FY2022 Annual Report

{kind=link}

Outlook

In terms of outlook, management provided the following guidance:

Management expects Q1 Revenue of CHF 380 million, a 61% increase YoY . This reflects strong ongoing momentum across all regions, channels, and product types, supported by a much-improved supply chain and inventory position.

Management projects FY2023 Revenue of CHF 1.7 billion, a 39% increase YoY . This includes 300 basis points of currency exchange headwinds, which means a currency-neutral growth rate of 42%. This figure is also ~30% higher than what management expected back on September 21 before the IPO, showing strong demand for On's products as well as relentless execution by the On team. Management also added further details on their full-year guidance:

As a result of the strong first quarter momentum, and the comparably heavy supply disruptions that we had faced primarily in the first half of 2022, we anticipate a higher growth rate of high 40s in half year on 2023 was a slow to mid-30s in the back half of the year. Based on the current momentum and pre-orders for the fall-winter season, we see an opportunity to achieve even higher growth rates in the second half, but we remain prudent in the life of the many risks in the current macroeconomic environment.

(CFO and Co-CEO Martin Hoffman — ONON 2022 Q4 Earnings Call )

In other words, growth is expected to slow down following a strong FY2022, but management is also being conservative with their guidance. Rest assured, On has beaten analyst estimates (by a wide margin) in all quarters as a public company, so there's a good chance that On continues to outperform both internal and analyst expectations.

{kind=link}

Management also added that they'll be keeping inventory relatively flat for the year, which should help the company turn cash flow positive.

Despite the strong growth of net sales this year, we do not expect a meaningful further increase of our absolute inventory positions throughout the year. Depending on phasing, we may see modestly higher or lower inventory levels in the quarters, but over the course of the full year this will allow us to choose our net working capital balance relative to net sales and to improve our cash flow.

(CFO and Co-CEO Martin Hoffman — ONON 2022 Q4 Earnings Call )

On expects FY2023 Gross Margin of 58.5% , an improvement from 56.0% in FY2022. Management expects Gross Margin to resume its path toward the company's long-term target of 60% as supply chains and shipping rates stabilize. On intends to use these cost savings to increase Marketing Expenses in 2023, to around 12% to 12.5% of Revenue.

Finally, management expects an FY2023 AEBITDA Margin of 15% as the company gains operating leverage from the continued maturity in key markets and higher efficiencies across key processes.

All things considered, the initial guidance provided by management was shockingly good, which is why the stock reacted so positively following its recent earnings release. Given On's history of outperformance and the growth of its brand, I won't be surprised if the year turned out to be even better than expected.

Competitive Moats

Based on my research and analysis, I identified three competitive moats for On: Technology, Brand, and Cost Advantages.

Technology

As mentioned in the first few sections, On focuses on developing the most technologically-enabled running shoe out there with core components such as CloudTec, Speedboard, and Helion. Through cushioned landings and powerful take-offs, its shoes make the runner feel like they're running on clouds. They definitely do, as I've experienced it firsthand.

There's no denying that technology is one of On's competitive advantages, as seen by its ISPO Awards over the years:

- On Prototype — ISPO BrandNew Award 2010.

- Cloud — ISPO Gold Award 2015 for Best Performance Running Shoe.

- Cloudflash — Product of the Year of ISPO Award 2017 in the Performance segment.

- Cloudultra — ISPO Award Winner 2021 in the Running & Fitness segment.

- Cloudneo (Cyclon) — Product of the Year of ISPO Award 2021 in the Running & Fitness segment.

- Cloudmonster — ISPO Award Winner 2022 in Shoes.

- On Zero Jacket — ISPO Award Winner 2022 in Clothing.

Not only is On innovative in the design of the shoe but also in the production side.

The company focuses on two key production areas:

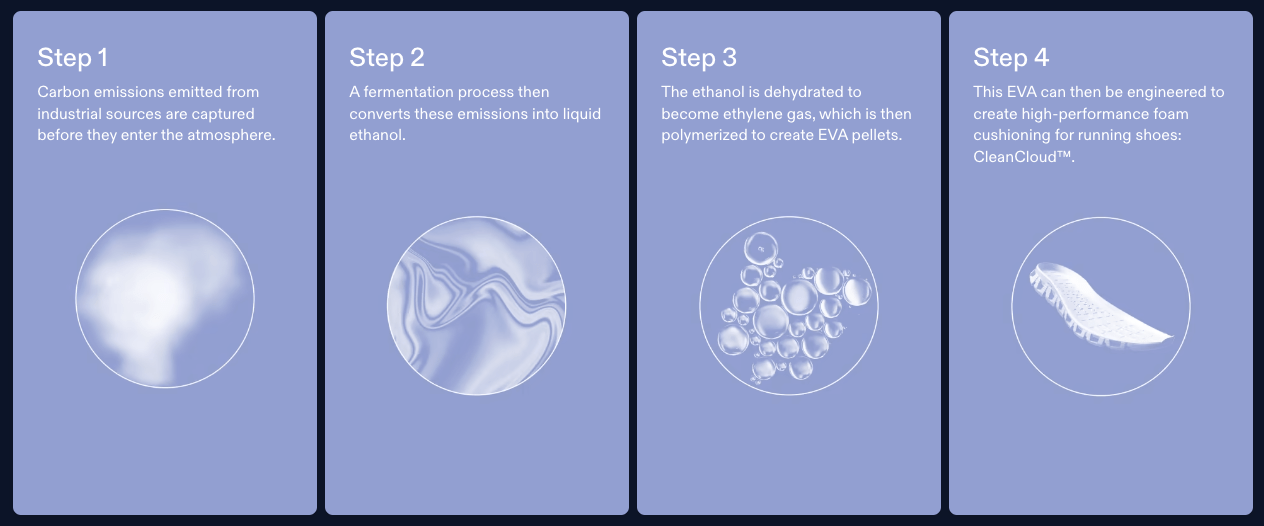

- Using alternative materials : On uses sustainable materials such as recycled polyesters, organic cotton, and vegan leather. The company is pursuing advanced recycled sources, carbon emissions-based materials, and bio-based materials when constructing its products. Most recently, On partnered with LanzaTech, Borealis, and Technip Energies to capture carbon emissions to create CleanCloud — a high-performance EVA foam for outsoles. Cloudprime will be the first-ever shoe made from carbon emissions, engineered by On's proprietary CleanCloud technology.

On Holding: CleanCloud Process

{kind=link}

- Creating circular systems : On aims to create a circular value chain where products are designed and manufactured to be used and reused. To fulfill this mission, On launched the Cyclon subscription model whereby customers pay a monthly fee of $29.99/month for a pair of running shoes. After 6 months when the shoe is pretty beaten up, customers can request for a new pair through the Cyclon program. The old, worn-out shoes are then sent back to On where they will be 100% recycled. Cloudneo is the first shoe under the Cyclon program and it is made entirely from sustainably sourced polyamide, more than 50% of which is made from bio-based castor bean oils.

{kind=link}

Technology is in On's DNA — in design and production — and it is a key differentiating factor that sets it apart from competitors.

Brand

Technology and innovation are why On has millions of fans rooting for the brand — wearing On shoes means supporting technology development for next-generation running. At the same time, On has established a running culture that has influenced many to join the running revolution, even those that have not previously incorporated running into their lifestyles (including me).

Their shoes also feel different, premium, and techy. Even though competitors like Hoka and Saucony price their shoes similarly to On shoes, they don't look and feel as premium and modern as On. This is why On shoes have been spreading like wildfire — the unmatched quality, performance, and brand story On offers are why athletes, influencers, and everyday explorers are recommending On shoes.

On's brand power is displayed in its explosive growth — while the sporting goods industry declined as a whole, On's business continued to "take off". But On is also careful enough not to hurt its brand positioning by opening as many stores as possible. Management doesn't want On to become a mass brand — they want On to maintain its premium appeal, only for hardcore runners and athletes.

With the focus on our premium position, we continue to manage the channel carefully and closed over 200 doors, that we considered as less additive to the positioning of the brand. The strengths of our premium products rooted in innovation, design and sustainability is even more directly reflected in the demand we have seen in our DTC business, resulting in 76.4% growth in Q4 versus the prior year period. While assets in the market were discounting, we have achieved our strong growth with a very high share of full price sales .

(CFO and Co-CEO Martin Hoffman — ONON 2022 Q4 Earnings Call )

On's focus on sustainability is also winning more customers as people become more environmentally conscious. Along with its sustainable production methods, On has introduced new business models that promote going green. The Cyclon subscription model is one such example. Another would be the recent launch of Onward , which enables customers to trade in and shop pre-owned On shoes as the company pushed beyond first-hand gear. Such initiatives further reinforce On's brand moat.

Cost Advantages

On is able to grow rapidly through its wholesale partnerships with major retailers that are complementary to On's brand. Even though these partnerships result in lower margins compared to its DTC business, it's a capital-light and fast way for On to attract new customers and enter new markets.

As On gains brand awareness, On intends to grow its DTC channel — both digital and physical — to create a more premium and intimate customer experience. It is important to note that On is incredibly selective with their retail presence, opening stores only in premium shopping locations in major cities such as New York City, London, and Beijing, where its customer demographics reside.

While competitors try to open as many stores in as many locations as possible, On focuses on high-value markets which are aligned with its premium brand positioning. As such, On can maintain its pricing power, and thus, achieve higher productivity in terms of sales per store.

These are, perhaps, reasons why On has superior Gross Margins compared to peers. Considering the fact that On is still in its early stages of growth, On could potentially improve profitability as operations in key markets mature.

The rollout of the Cyclon program could further boost margins as the Cost of Goods Sold drops to near-zero given that shoes under the program are 100% recycled.

As profitability improves, On will gain even more edge over competitors, allowing management to invest the profits elsewhere (expansion, R&D, buybacks, etc.).

Valuation

On 15 September 2021, ONON stock opened for trading at $35.40, which was way higher than the company's IPO price of $24. Back then, greed and euphoria still existed in the markets, causing the stock to rally further before the growth stock crash of November 2021. ONON stock found a base between $16 to $25 for the better part of 2022, before blowing past the $25 resistance following its blowout Q4 earnings.

As of this writing, ONON trades at $31 a share, valuing the company close to $10 billion.

On a historical basis, ONON is trading at a much reasonable valuation multiple today, at 7.3x EV to LTM Revenue, which is considerably lower than its peak of 20x in November 2021.

Now, let's take a look at ONON's relative valuation compared to peers.

At a quick glance, ONON seems to be overvalued compared to other brands. However, its premium valuation is well justified given its higher growth rates.

For example, ONON is trading at an EV/Sales (NTM) multiple of 5.1x compared to NKE's 3.6x, but ONON is expected to grow nearly 5 times faster than NKE in the next two years.

ONON is also reasonably valued compared to the premium athletic apparel brand Lululemon ( LULU ). ONON has the same EV/Sales (NTM) multiple as LULU, despite having more than twice the expected growth rate compared to LULU.

| ONON |

| NKE |

| CROX |

| LULU |

| ADDYY |

| UA |

| BIRD |

| EV/Sales (NTM) |

| 5.1x |

| 3.6x |

| 2.6x |

| 5.0x |

| 1.7x |

| 0.8x |

| 0.5x |

| EV/EBITDA (NTM) |

| 33.7x |

| 25.1x |

| 9.4x |

| 19.2x |

| 38.3x |

| 9.2x |

| - |

| P/E (LTM) |

| 157.3x |

| 35.3 |

| 14.5 |

| 54.5x |

| 130.8x |

| 21.8x |

| - |

| P/E (NTM) |

| 54.8x |

| 31.8x |

| 11.3 |

| 31.6x |

| 69.5x |

| 13.7x |

| - |

| FY2023 Growth Estimate |

| 42.3% |

| 9.0% |

| 12.3% |

| 14.7% |

| (7.2)% |

| 3.2% |

| (12.5)% |

| FY2024 Growth Estimate |

| 31.7% |

| 6.9% |

| 10.4% |

| 12.8% |

| 13.9% |

| 4.4% |

| 9.4% |

On the other side, it's not fair to compare ONON's valuation with underperforming peers, namely ADDYY, UA, and BIRD. These companies either have significantly lower growth rates or are expected to decline in the next year.

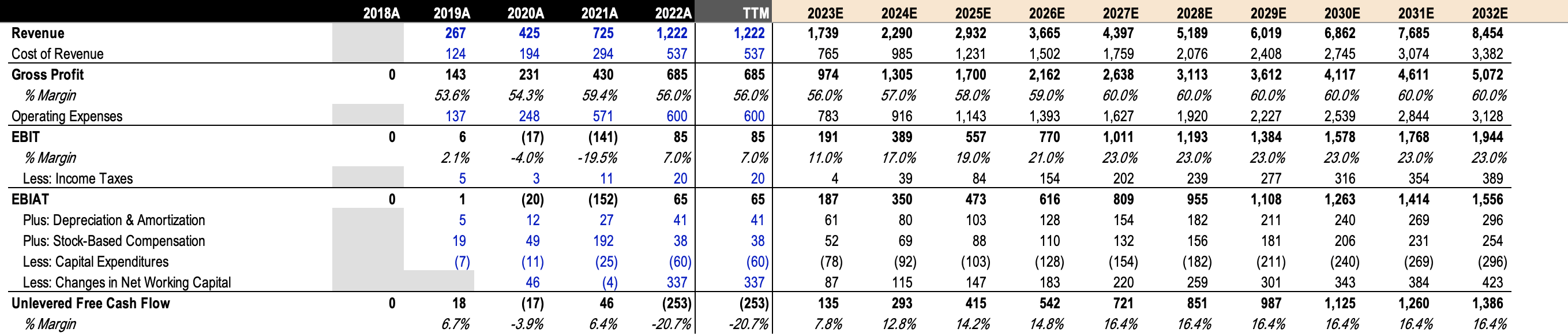

I also did a 10-Year DCF model on ONON. Here are my key assumptions:

- Revenue YoY Growth : follow analyst estimates for the first three years then decrease to 10% by 2032.

- Gross Margin : reaches the company's long-term target of 60%.

- Operating Margin : reaches 23% by 2027, slightly better than LULU's 21%

- FCF Margin : reaches 16.4% by 2027 and kept constant for the remaining years.

ONON Investor Relations and Author's Analysis

{kind=link}

Here's what the projections look like. Keep in mind that they are still in Swiss Francs.

ONON Investor Relations and Author's Analysis

{kind=link}

Based on a 12% discount rate and a 3% perpetual growth rate, we arrive at an intrinsic value of CHF 29.05 per share. Converting to USD (CHF/USD = 1.09 as of this writing), we get a price of $31.66 per share, which is slightly higher than the current price of $31.03.

ONON Investor Relations and Author's Analysis

{kind=link}

All in all, despite the recent pop in the stock, I believe ONON is still fairly valued given its growth potential, superior profitability metrics, and durable competitive moats.

With that said, I'll be a buyer of ONON during dips as I prefer a large margin of safety in my investments.

It is also reassuring to know that insiders own a considerable amount of stock in the company — directors and executives have total economic ownership of about 29.5%.

On Holding Annual Report 2022

Catalysts

- Product Launches : New products, sports categories, or even business models, will be positive developments for On shareholders. It's what drives growth and excitement in the company. Fortunately, innovation is On's specialty, and the company has a bunch of product launches lined up:

if you think about Q4 last year, half of all the growth came from our all new running products. And now on top of that, the Cloudsurfer that Marc just mentioned. These are early, early days of growing blockbuster franchises. And so, you can just anticipate how much runway this will give us.

And then apart from that, we're also launching new iterations of our existing running blockbusters, which means of course for us that we're also going to innovate on them. So blockbusters that come all new in ‘23 and ‘24 you're going to see the Cloudboom Echo 3, which has been at the seat now of pro athletes winning races. And you're also going to see a lot of run apparel that is going to come along. And then you can bet that ‘24 for the Olympic Games, we're going to be ready with full range, and from very accessible running products to the absolute pinnacle running products to go into the banner year for performance running.

(Executive Co-Chairman and Co-Founder David Allemann — ONON 2022 Q4 Earnings Call )

- Tapping Influencers : Management did mention that they'll be increasing marketing spend in FY2023. One way in which On can boost brand awareness is through additional celebrity endorsements. Signing new athletes such as Olympic Champion triathlete Kristian Blummenfelt and women's number one ranked tennis player, Iga ?wi?tek will play major roles in promoting the On brand. I expect On to sign more athletes throughout 2023 and beyond — a megastar name could be a major catalyst for the stock.

- Subscription Model : The launch of its circular system, Cyclon — whereby customers subscribe to get their shoes recycled every 6 months — could be a game changer. Although still far in the future, On could also enter the connected fitness industry, offering fitness equipment such as treadmills along with guided workout programs. Not only could it expand On's margin profile, but it also introduces a more stable, software-like revenue stream for On. Perhaps the markets could give ONON a higher valuation multiple if the subscription business becomes a major part of On's business model.

Risks

- Competition : The sporting goods industry is highly competitive. There're giants like Nike and Adidas. There're running-specific brands such as Hoka and Asics. There're premium sports performance brands like Lululemon and Nobull. The competition is fierce — On needs to at least maintain its reputation as a brand that excels in sports technology and innovation. If not, its brand may deteriorate and growth will not be as robust as many initially expected. As a consequence, the stock could flutter like UA or BIRD.

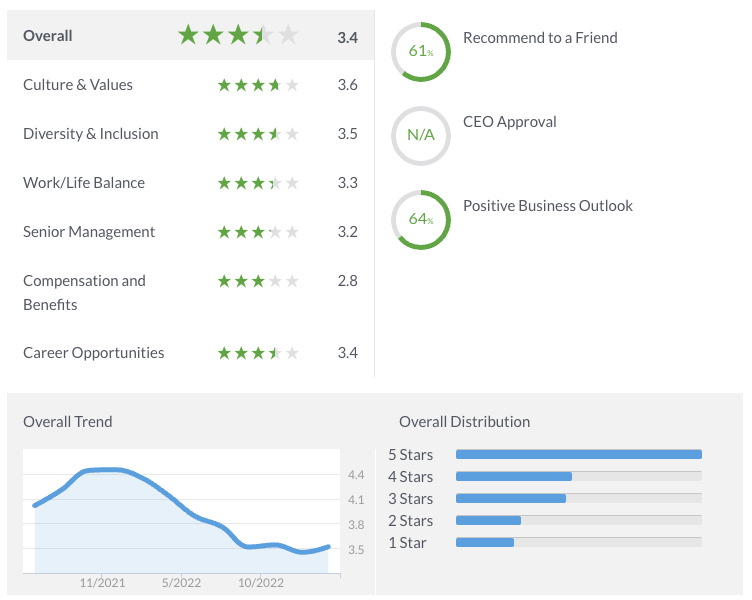

- Management : One thing that caught my attention during my research is that On's glassdoor rating has been on a downward trajectory ever since November 2021. The overall rating dropped from 4.4 stars to just 3.4 stars today. It's never good to see poor employee reviews from a company. After all, people are the ones that dictate the success of the company, and ultimately, shareholder returns.

{kind=link}

- Manufacturing Concentration : According to its annual report, in 2022, 95% of On's footwear products and 60% of its apparel and accessories products were produced in Vietnam. Furthermore, 5 out of its 22 suppliers produced approximately 70% of its products in 2022. If operations were in Vietnam or its top 5 suppliers are disrupted, On's operating results could take a major hit.

The Bottom Line

In conclusion, On is taking the premium performance sportswear industry by storm. Its growth numbers are nothing short of spectacular, supported by its technology, brand, and cost advantages moats.

The company still has a long growth runway ahead with tons of optionality to expand its business — new products, markets, and business models. I'm particularly interested in its award-winning Cyclon subscription model, which could revolutionize the way products are manufactured and used. Through its circular system, Cyclon could produce software-like margins and sales for On.

Q4 earnings were a big surprise and the upbeat guidance was welcome news for shareholders. Despite the post-earning pop, shares still seemed to be fairly valued. On the other hand, cash flow is still negative and its balance sheet is running thin — investors should manage risk appropriately.

That said, thank you for reading my On deep dive. If you enjoyed the article, please let me know in the comment section below.

For further details see:

On Holding: Clouds And Circularity