STMEF - ON Semiconductor: Buy Now If You Believe In Management's Goals For 2027

2023-08-14 06:00:01 ET

Summary

- ON Semiconductor has seen a significant increase in its fundamentals and stock price over the past three years, with revenue being up ~60% and the stock price being up 300+%.

- The company currently seems expensive when compared with major competitors.

- Nevertheless in a Discounted Cash Flow Analysis both the Bear and Bull Case suggest that the company might be undervalued at current prices.

ON Semiconductor Corp. ( ON ) has rallied 300+% over the last three years, but their fundamentals have also increased significantly over the same time span.

Considering both, the question arises if the company is currently still offering additional upside, which in turn could justify an investment in ON Semiconductor.

SWOT Analysis

To get a quick introduction into the company and potential aspects that impact ON's business, I conducted a small SWOT Analysis. The main component of this article will however focus on the companies valuation and future potential.

Strengths:

- Diverse Product Portfolio : Among the many products offered by ON Semiconductor are solutions for power and signal control, logic, discrete computing, and bespoke applications. Reduced reliance on a particular product or market sector results from this diversification.

- Global Presence : The business efficiently serves a global clientele thanks to its global operations, logistics, and design centers.

- Strategic Acquisitions : In order to improve its technological capabilities and broaden its market presence, ON Semiconductor has acquired businesses and technologies over the years.

- Experienced Management : A seasoned management team with extensive industry knowledge oversees the company's growth and strategic direction.

- Robust R&D : By investing in R&D, the business makes sure it stays on the cutting edge of innovation and technical breakthroughs in the semiconductor sector.

Weaknesses:

- Cyclicality: The semiconductor market is in general pretty cyclical , this could negatively impact ON's future business as future demand might decline.

- Competitive Market : The intense competition in ON's market might put pressure on profit margins and market share.

- Supply Chain Vulnerabilities : Due to a number of causes, including geopolitical conflicts and global health crises, the semiconductor sector could experience supply chain interruptions.

Opportunities:

- Growing Demand for AI : The demand for semiconductors is expected to surge in response to the development of artificial intelligence ((AI)), creating a sizable potential opportunity.

- Automotive Advancements : Advanced semiconductors are required by the rising demand for electric cars (EVs) and autonomous driving technologies, creating a potential market for ON Semiconductor.

- Technological Partnerships : Collaborations can provide ON Semiconductor access to cutting-edge technology and a competitive edge. These partnerships could be with established tech giants or new startups.

- Expansion in Emerging Markets : As these regions quickly industrialize and digitize, growth in countries like India, Southeast Asia, and Africa presents a substantial potential.

Threats:

- Trade Tensions : Trade conflicts and geopolitical difficulties, particularly those involving the United States and other major economies, can affect a company's operations and profitability.

- Rapid Technological Change : The semiconductor business moves swiftly, therefore if goods aren't updated often, they can quickly become outdated.

- Environmental Concerns : The manufacturing of semiconductors can have an influence on the environment, which may lead to tighter laws in the future.

- Competition : Major firms with enormous resources and the ability to apply significant competitive pressure include Intel ( INTC ), Texas Instruments ( TXN ) and Qualcomm ( QCOM ).

- Global Economic Instability : During economic downturns or recessions, the demand for semiconductors can be significantly decreased, which can have an impact on sales and profitability.

A Look Into ON's Future

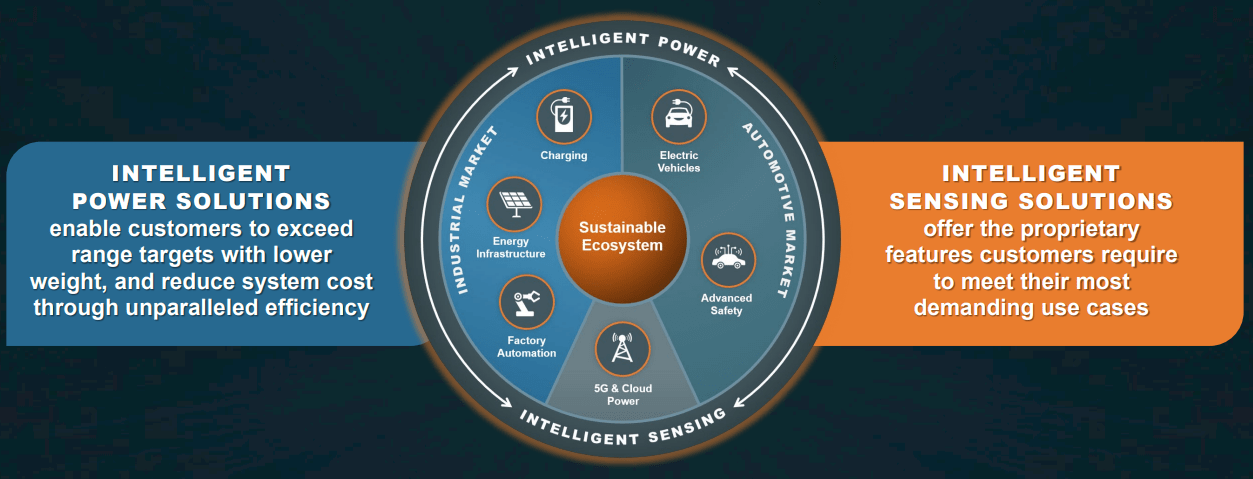

ON's management is dividing its business in the two different segments Intelligent Power Solutions and Intelligent Sensing Solutions. The following graphic nicely illustrates their different business segments:

{kind=link}

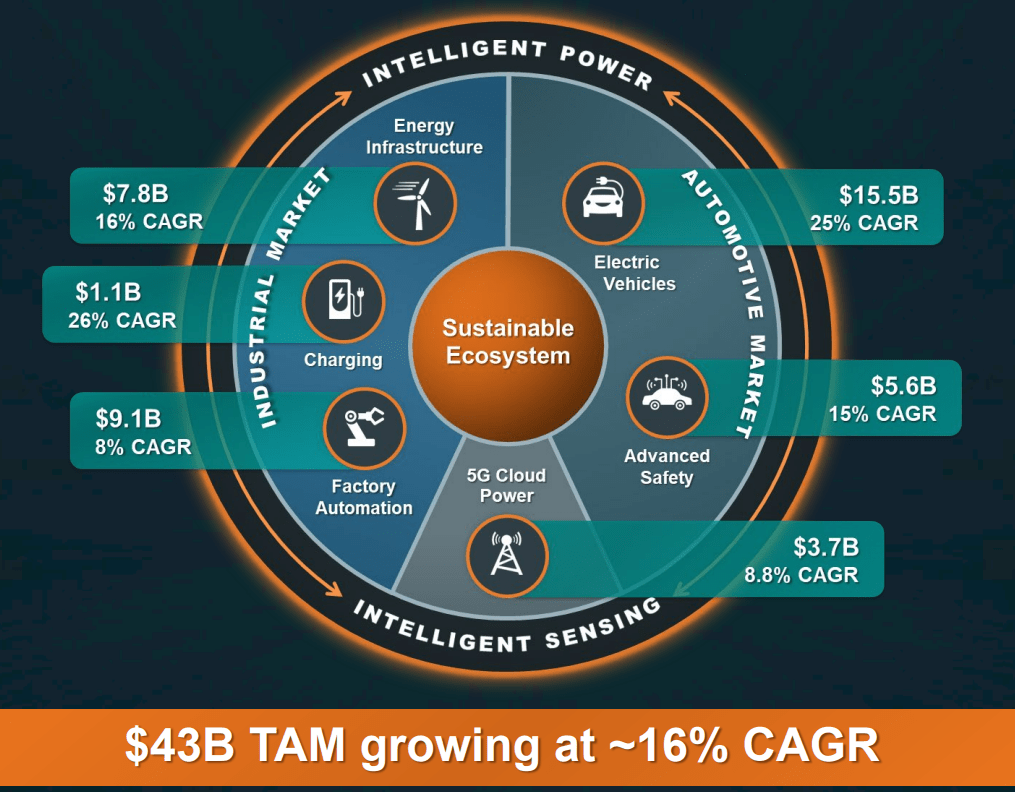

Based on current market projections ON is internally projecting that most of these segments will have a CAGR above 15% until 2027, which underlines the strength of ON's business.

{kind=link}

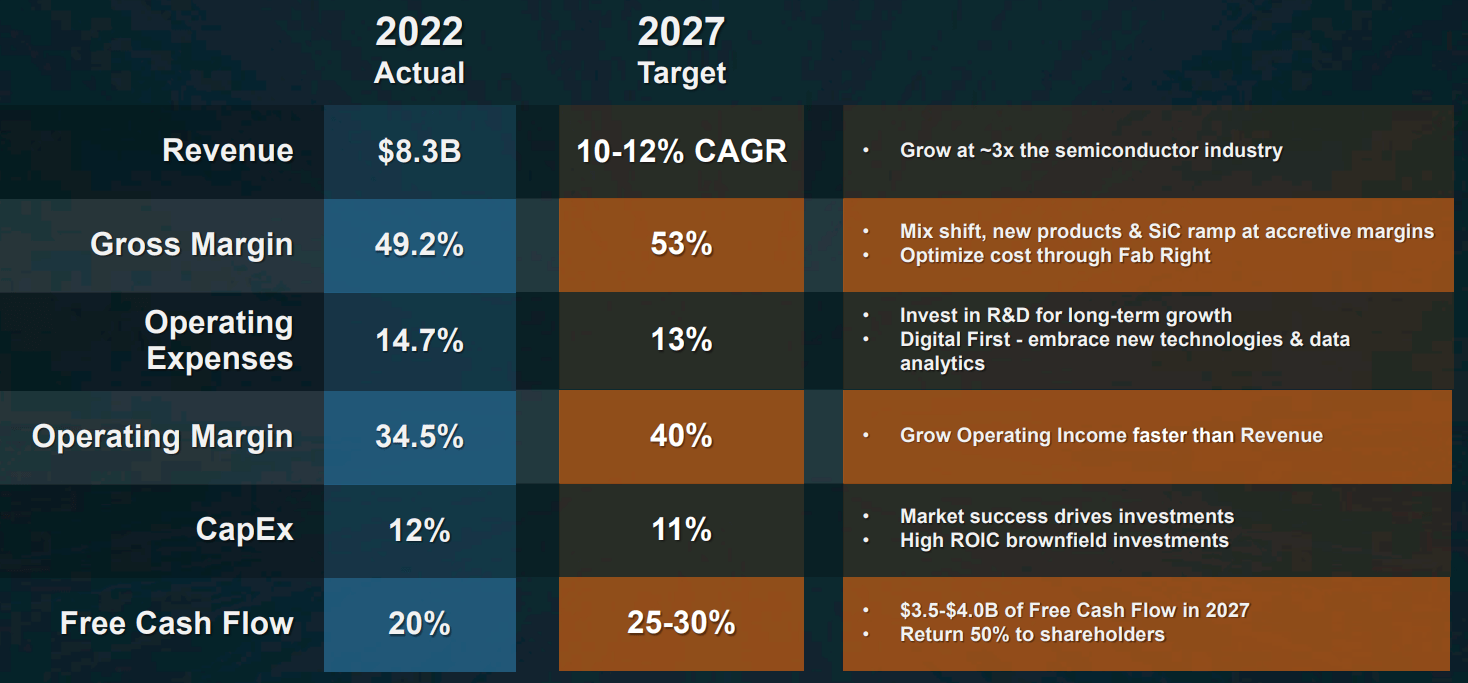

Based in these assumptions ON is setting ambitious goals for itself. They plan to increase their Gross Margin from 49% to 53% through three different measures:

- Mix / New Products: They plan to shift the focus towards Auto & Industrial and to introduce new differentiated products which achieve margins above average.

- Silicon Carbide ((SIC)): With more scale, margins will increase in this segment and initial startup costs are going to be absorbed.

- Fab Right: Optimizing the manufacturing network and maximize the utilization.

With their current product mix, they anticipate a revenue CAGR of 10 to 12% till 2027. Their goals are nicely summarized here:

{kind=link}

Valuation

Both the regular PE Ratio of 21.6 and the forward PE Ratio of 18 from ON seem cheap when considering the 10 year average PE Ratio of 27.

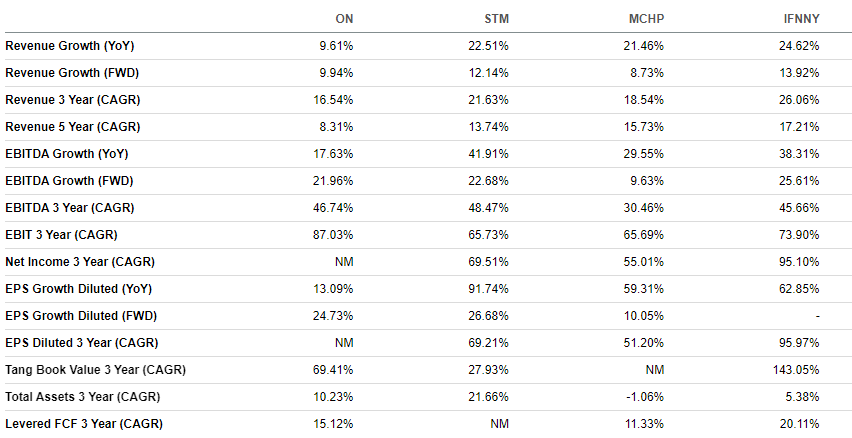

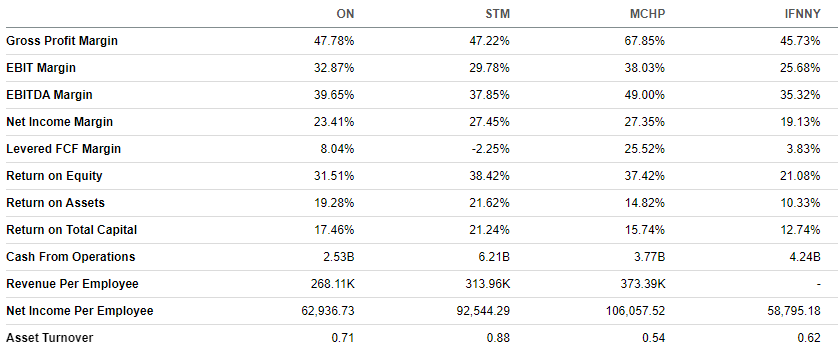

When however comparing ON's PE to the major competitors STMicroelectronics N.V. ( STM ), Microchip Technology Incorporated (MCHP) and Infineon ( IFNNY ) the company looks expensive.

As can be seen above, this discrepancy in valuation seemed to start in April 2023, as from there on ON is trading at higher PEs compared to its peer group.

When we zoom out further, we can see that in the last 4 years ON was rather trading at the middle or the low end of the four compared companies, which in turn confirms the current mismatch.

This seems weird when we take a look at the growth and profitability metrics of the four and compare them to each other:

Growth Metrics of ON, STM, MCHP and IFNNY (seekingalpha.com) Profitability Metrics of ON, STM, MCHP and IFNNY (seekingalpha.com)

{kind=link}

{kind=link}

In (almost) all metrics ON is in the middle or on the low end, which in turn means that the company doesn't earn a valuation premium over its competitors.

From this insight we can draw two different conclusions:

- ON is overvalued

- It's peers are undervalued

As this comparison only includes data from the past and a lot of uncertain aspects like valuations of other companies, I conducted two Discounted Cash Flow Analyses to evaluate the company independent from other companies

Discounted Cash Flow Analysis

To create a reliable analysis, I divided the Discounter Cash Flow Analysis ((DCF)) in two different parts:

- Bear-Case: The company "only" achieves the low ends of management's goals for 2027 and most of the margins stay flat even though the management laid emphasis on a margin expansion.

- Bull-Case: ON manages to achieve the high end of management's goals for 2027 and is successfully expanding the margins.

The blue cells are the assumptions I took, to evaluate the company.

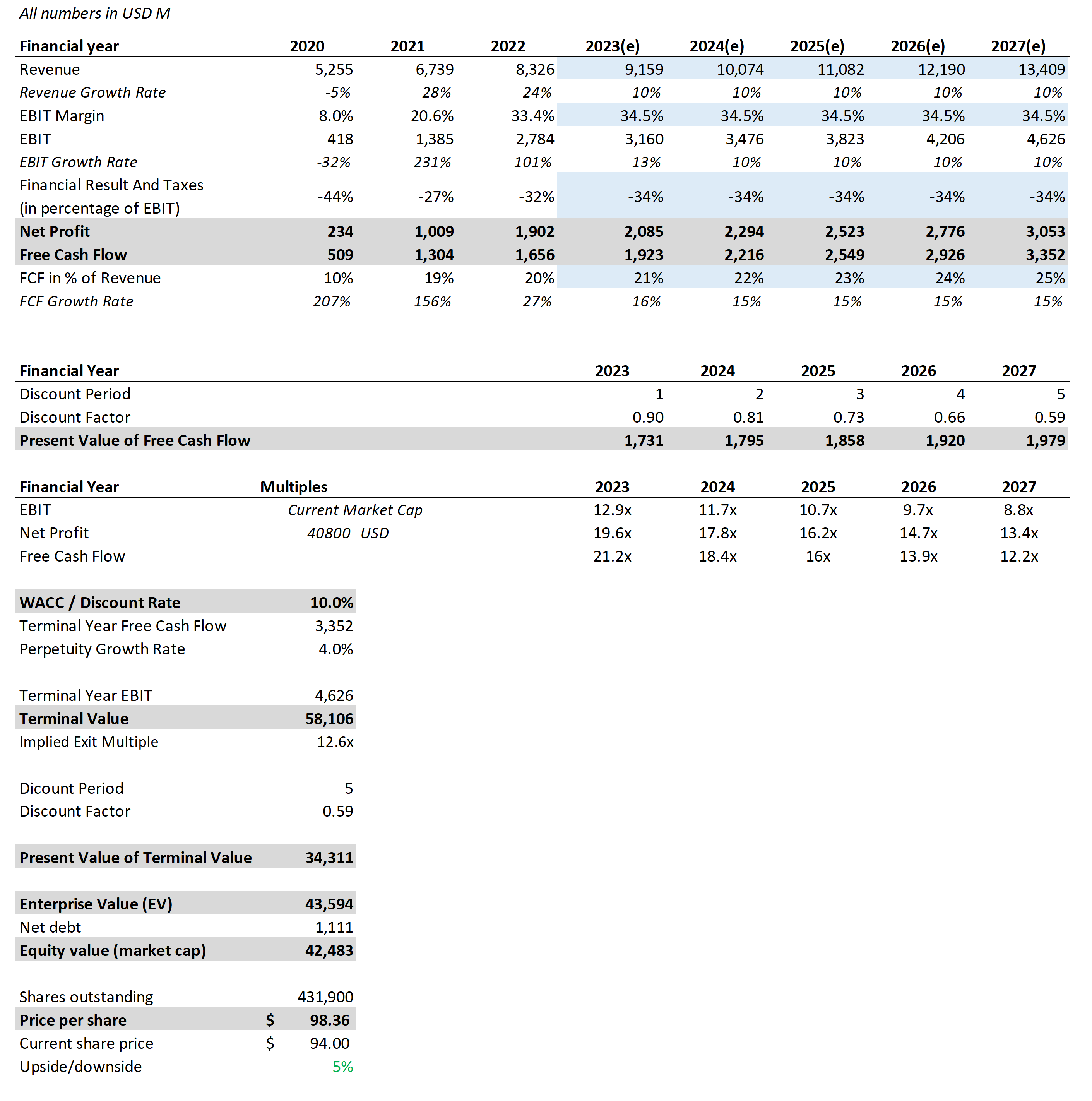

Bear-Case

- Revenue: I predicted a conservative revenue growth rate of 10% till 2027. This is, like mentioned above, the low end of management's guidance for 2027. This seems also pretty much in line with historical growth rates:

Growth Prediction for ON (own prediction)

{kind=link}

- EBIT Margin: For the EBIT margin, I assumed that the current EBIT margin of 34.5% stays flat for the next 5 years.

- Financial Result And Taxes: I averaged the values of the last three years and therefore used -34% to calculate the Net Profit for the years 2023 to 2027.

- Free Cash Flow: The management guided a Revenue to FCF metric for 2027 in the range of 25 to 30%. To address for the YoY improvement, I predicted this ratio as follows:

FCF Prediction for ON (own prediction)

{kind=link}

- WACC: I used the current WACC of ON, which currently sits at around 10%.

- Perpetuity Growth Rate: The perpetuity growth rate assumed for the analysis is 4.0%. This seems conservative, in my opinion, for a semiconductor stock.

DCF ON Bear-Case (seekingalpha.com; investor.onsemi.com)

{kind=link}

For our Bear-Case, we arrive at a price target of ~$98, indicating the company is slightly undervalued by around 5%.

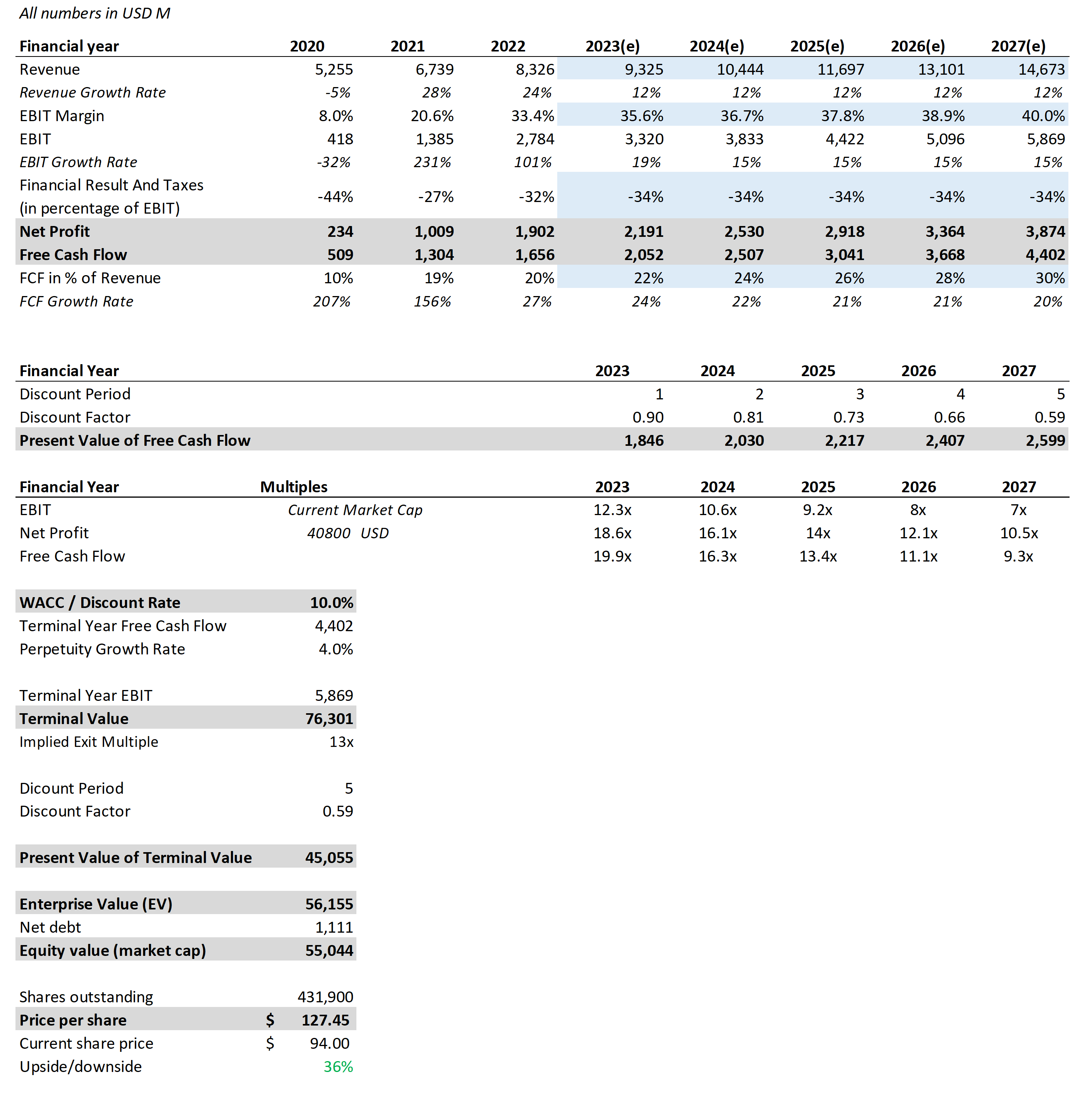

Bull-Case

- Revenue: For the Bull-Case, I used the 12% p.a. revenue growth, anticipated by ON's management.

- EBIT Margin: ON is planning to expand its EBIT margin to 40% over the next 5 years. To once again adjust for the YoY growth, I anticipated the margins to be as follows:

EBIT Margin Prediction for ON (own prediction)

{kind=link}

- Financial Result And Taxes: I again used the -34% to calculate the Net Profit for the years 2023 to 2027.

- Free Cash Flow: I now took the high end of management's goal for 2027, which translates into the following Revenue to FCF metrics:

FCF Prediction for ON (own prediction)

{kind=link}

- WACC: Here I also used 10%.

- Perpetuity Growth Rate: For the perpetuity growth rate I again assumed 4.0%.

DCF ON Bull-Case (seekingalpha.com; investor.onsemi.com)

{kind=link}

The Bull-Case DCF gives us a price target of ~$127, which could indicate that the stock is currently undervalued by 35%.

Risks to the DCF

Both scenarios somewhat anticipate, that the management is able to pull off - at least some - of the goals it set itself. If one or more of the above mentioned threats or weaknesses come into play, the fundamentals and therefore the reliability of our DCFs could decrease significantly.

Conclusion

The past three years have shown outstanding performance and fundamentals for ON Semiconductor Corp, with a gain of more than 300%.

Despite having lower growth and profitability indicators, ON seems to be trading at a premium when we compare its valuation to that of its competitors.

When looking at the DCF calculations we however get an opposing picture: the bull-case shows a potential undervaluation of up to 35%, while the bear-case predicts just a small undervaluation of roughly 5%.

I believe that the goals set by ON's management are well achievable, which in turn means that our DCF assumptions are realistic. Therefore I currently rate the company as a 'Buy' with a price target of $115.

Whether ON's competitors - namely STMicroelectronics N.V., Microchip Technology Incorporated and Infineon - are therefore even more undervalued, like suggested by the peer comparison, is a topic for other articles. If you don't want to miss these, please consider following me, to get notified whenever I upload a new article.

For further details see:

ON Semiconductor: Buy Now If You Believe In Management's Goals For 2027