ONCT - Oncternal Therapeutics: Making Progress And Still In Buy Territory

Summary

- As ONCT's MCL Phase 2 study continues to mature, the data also continues to improve. In fact, the data now looks outstanding.

- Thus, I believe that the chances of success in the newly initiated Phase 3 trial are good and hence I rate the stock as a buy at today's stock prices.

- Nonetheless, I haven't upsized my speculative sized position because I worry that the company may be forced to engage in a dilutive financing over the next 18 months.

This article is the fourth in my ongoing coverage of Oncternal Therapeutics ( ONCT ). For readers new to the company, I suggest you read the earlier articles ( 1 , 2 , 3 ) for more in depth background on the company and its candidate therapeutic programs. Today I'll give a brief overview of the company and then consider its lead program in mantle cell lymphoma (MCL) as it has progressed since the beginning of my coverage. I'll also review the company's cash position and mention the major risk inherent in investing in small cap biotechs.

Company

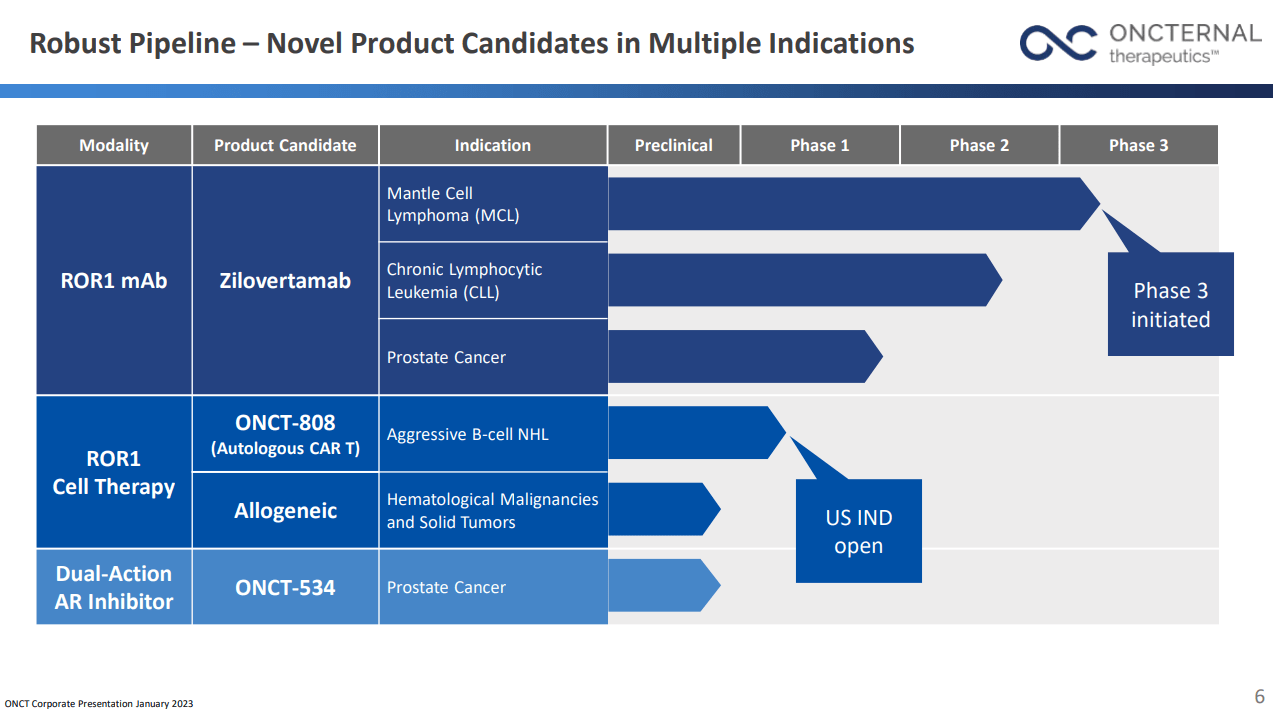

ONCT is a small biotech company based in San Diego which is focused on developing treatments for rare cancers with relatively limited existing therapy options. The January 2023 corporate presentation includes this updated slide with its pipeline.

{kind=link}

Corporate Presentation

As can be seen from the slide, the most advanced asset in ONCT's portfolio is zilovertamab which is a monoclonal antibody targeting ROR1 (receptor tyrosine kinase-like orphan receptor 1).

Note that in the heady days of biotech investing (circa 2020), two private companies in this same space were bought by major pharmaceuticals at premium prices. See my first article for all the details, but just to summarize (and noting that the two companies were working with antibody drug conjugates, not monoclonal antibodies):

- On November 5, 2020, Merck ( MRK ) announced that it was buying VelosBio for $2.75B . VelosBio is a privately held clinical-stage biopharmaceutical company committed to developing first-in-class cancer therapies targeting receptor tyrosine kinase-like orphan receptor 1 (ROR1).

- On December 10, 2020, Boehringer Ingelheim bought NBE-Therapeutics for 1.18B euros . "We look forward to progressing NBE-002, our lead program and best-in-class anti ROR1 ADC, and to continuing the fight against cancer alongside Boehringer Ingelheim with its strong clinical development capabilities."

Moreover, ROR1 is expressed on many solid and liquid tumors, such that there are many more cancers in which to explore the use of ONCT's ROR1 treatments.

{kind=link}

Corporate Presentation

In any case, zilovertamab has advanced to Phase 3 trials in MCL which is now the main focus of the company as it tries to preserve cash. However the rest of the pipeline has potential value as well, with the following summary slide doing a good job of highlighting this.

{kind=link}

Corporate Presentation

Before discussing the most recent company data in MCL, I think it's worthwhile to quickly review the disease, both in terms of patient impact and economic cost.

Mantle Cell Lymphoma

The lymphoma research foundation summarizes the disease as follows:

Mantle Cell lymphoma (MCL) is an aggressive, rare form of non-Hodgkin lymphoma (NHL) that arises from cells originating in the “mantle zone.” The mantle zone is the outer ring of small lymphocytes surrounding the center of a lymphatic nodule. MCL accounts for roughly six percent of all NHL cases in the United States.

The Cleveland Clinic has this to say about its aggressiveness and prognosis (my emphasis):

This is a serious illness because it can spread very quickly to become an advanced form of cancer. Mantle cell lymphoma is not a curable lymphoma . In most cases, treatment can put the condition into remission.

Unfortunately, cancer in remission isn’t the same as cancer that’s been cured. Mantle cell lymphoma can come back (relapse) after being in remission for months or years.

Over time, the cycle of remission and relapse revolves more quickly until treatment can no longer put the disease into remission. With newer targeted treatments, remission periods for mantle cell lymphoma have significantly increased.

[...]

In general, people with mantle cell lymphoma live two to nine years after diagnosis . Survival rates vary depending on whether the condition is indolent (slow growing) or aggressive. Studies show people at high risk for relapse live about two years after diagnosis and people at low risk are alive five years after diagnosis.

A 2022 study gives the following information regarding the prevalence and distribution of MCL (my emphasis):

MCL comprises about 7 percent of adult non-Hodgkin lymphomas in the United States and Europe with an incidence of approximately 4 to 8 cases per million persons per year [ 3-8 ]. Incidence increases with age and appears to be increasing overall in the United States [ 9 ]. Approximately three-quarters of patients are male, and White individuals are affected almost twice as frequently as Black individuals. Median age at diagnosis is 68 years .

Using 6 cases per million and a US population of 332M people gives about 2,000 new cases a year in the US and another 4,500 in Europe.

Finally, this NIH study from 2018 provides a look at the economic burden of MCL. Here is the abstract, with my emphasis, but for those looking to get into the weeds, the full article is quite detailed.

In view of recent therapeutic advances in mantle cell lymphoma (MCL), the aim of this retrospective cohort analysis was to assess treatment patterns, adverse events [AEs], resource utilization, and health care costs in patients with MCL in a US-based commercial claims database. A total of 783 patients with MCL (median age=65 years) were selected. Among patients receiving systemic therapy (n=457), the most common treatment regimens were bendamustine / rituximab [BR] (41.1%), rituximab / cyclophosphamide / doxorubicin / vincristine (RCHOP) (26.7%), rituximab monotherapy (20.4%), and ibrutinib monotherapy (14.2%). Mean monthly costs during treatments with BR, RCHOP, rituximab, and ibrutinib were $12,958, $24,719, $13,153, and $21,690, respectively. Mean monthly cost during follow-up was $13,650 among patients with ?6 AEs versus $5,131 among those without AEs. The costs of MCL varied considerably by treatment regimen and care setting. The overall economic burden of managing patients with MCL can be substantially affected by costs associated with managing AEs occurring during treatment.

Updated MCL Study Results

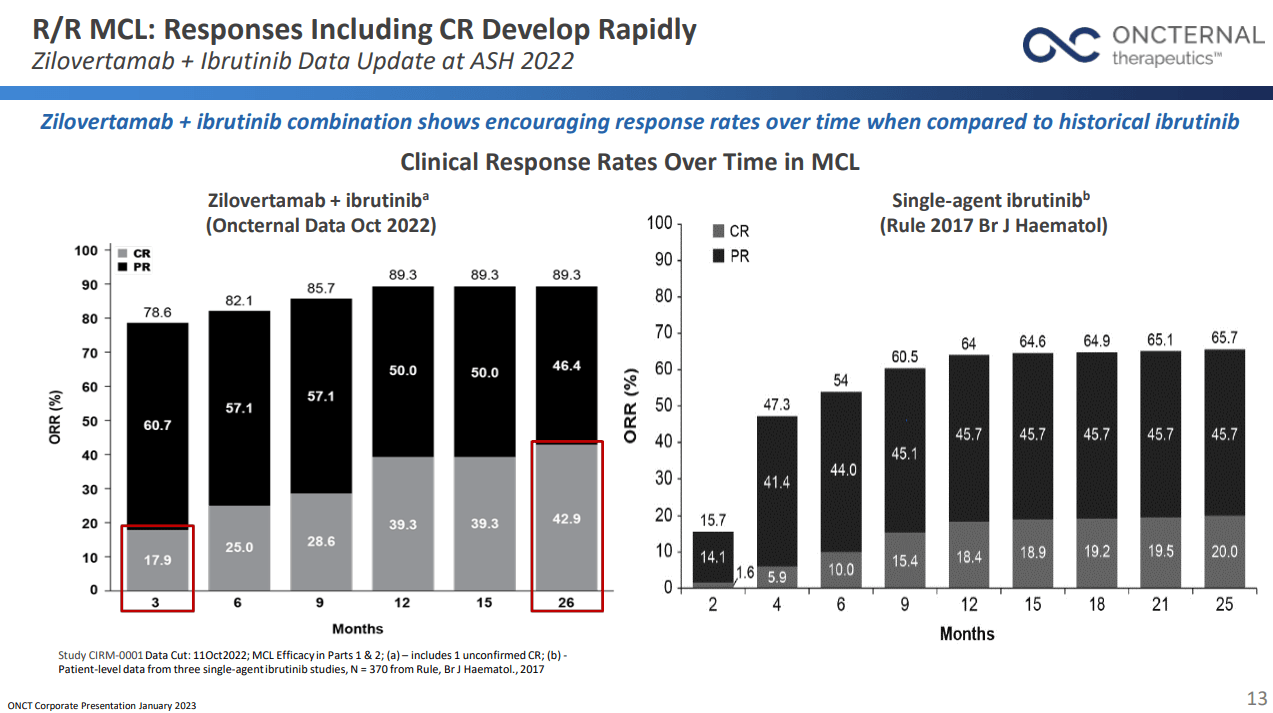

As ONCT's phase 2 MCL study continued to advance, the results also continued to improve. Here are two slides giving data through October of 2022.

The first one shows what percentage of patients experience partial and complete responses as a function of time on treatment. The slide also includes comparative historical data from patients taking only ibrutinib. The combo therapy shows impressive advantages, e.g. at 6 months 10% of patients on ibrutinib experienced complete responses and 44% showed partial responses. But when treated with a combination of zilovertamab and ibrutinib, the comparable numbers improve to 28.6% complete responses and 57.1% partial responses. This is very exciting.

{kind=link}

Corporate Presentation

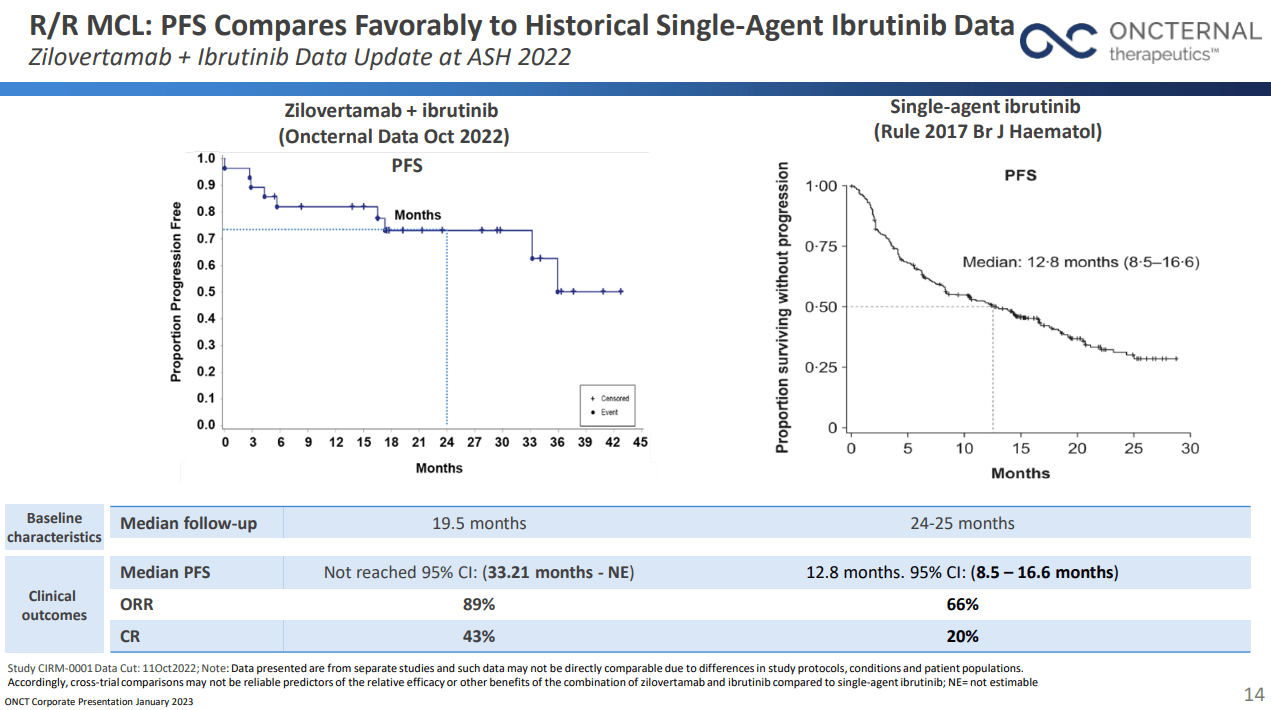

The second slide shows the proportion of progression free patients versus time (again comparing the combo to historical ibrutinib data). The objective response and complete response data mirrors that seen above. But it's also noteworthy that the median time to PFS hasn't been reached in the combo trial (with a median follow up time of 19.5 months) while it was only 12.8 months with ibrutinib monotherapy.

{kind=link}

Corporate Presentation

To see why I believe the data has been getting better as the study matures, consider the same slide when the data only went through April of 2022. All three measures are better with data through October versus through April.

Corporate Presentation June 2022

Phase 3 Study

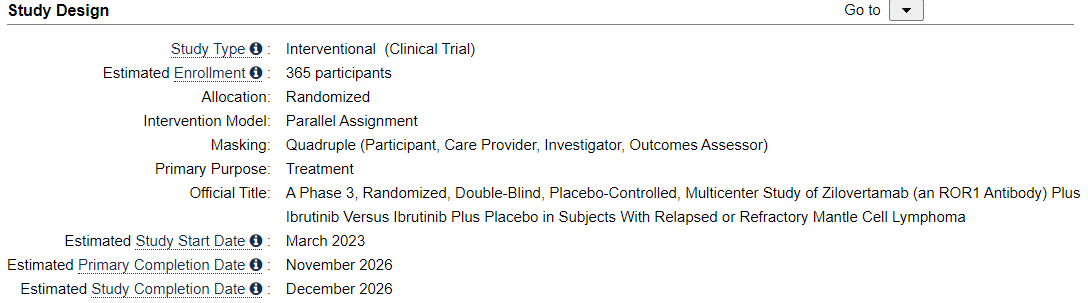

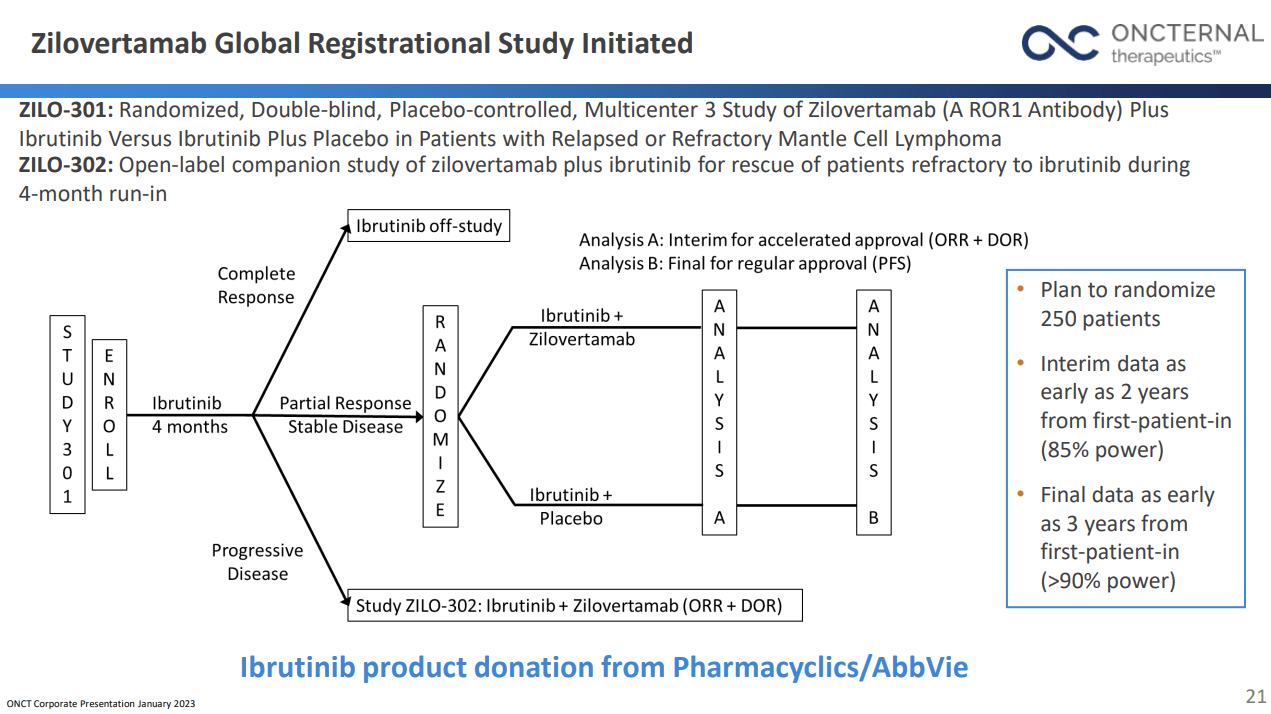

Based on this and other positive MCL data, ONCT applied for and received clearance to begin a Phase 3 study in MCL. Here is a link to the clinical trials site with all of the particulars, with the high level design being as follows:

{kind=link}

clinicaltrials.gov

As can be seen, the trial won't end before Q4 of 2026, but the company hopes to have some interim data available after 2 years (say Q2 of 2025). Here is a slide showing the trial design, note however that it shows 250 patients vs. the 365 listed at the clinical trials site. I have sent a question to ONCT to clarify if the 365 includes ZILO-301 + ZILO 302 while the 250 number is only for ZILO-301 and I will leave a comment to this article if I get a clarification.

{kind=link}

Corporate Presentation

Cash on Hand

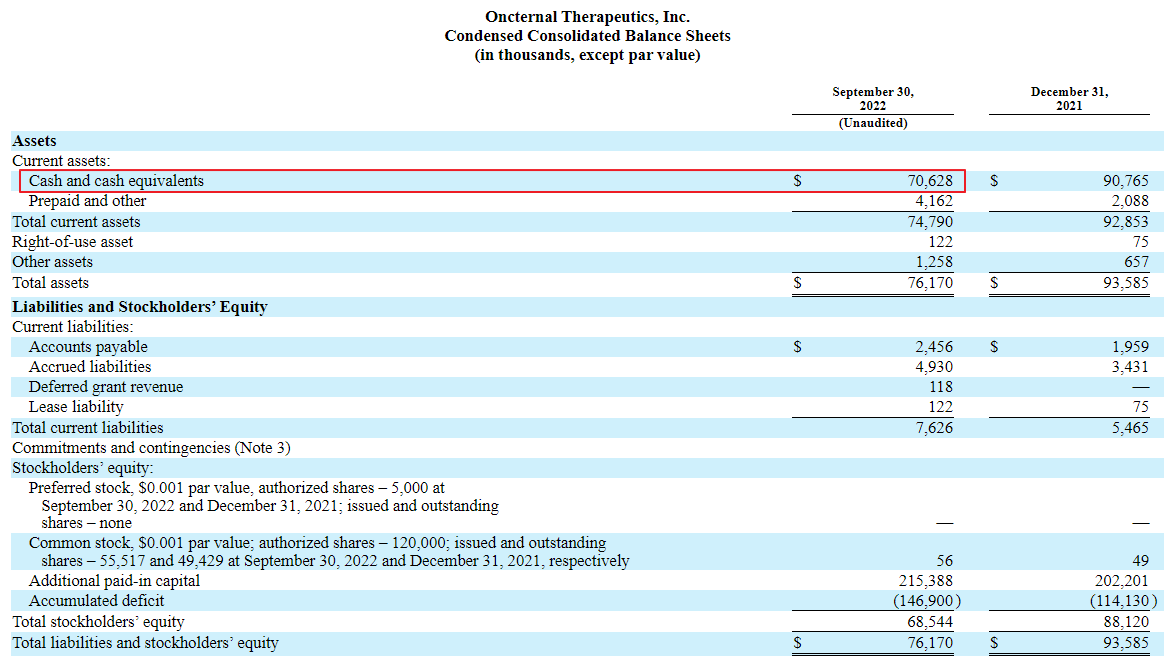

ONCT has about $70M in cash on hand which means the stock essentially trades for cash on hand (and thus its enterprise value is slightly negative). However, the $70M probably isn't enough to see it through the full Phase 3 MCL trials. This means there will likely be more financings, though I'm hoping that maybe they can partner some or all of their assets to avoid this. In any case, running short of cash is the biggest worry / risk with the company in my opinion.

{kind=link}

3Q 10Q

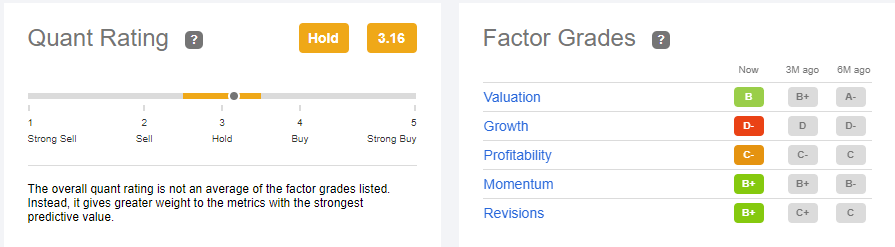

Quant Rating and Factor Grades

I'm not sure how relevant these ratings are to small cap development stage biotechs, but I still like to check them. Here we see that valuation looks decent while growth is obviously poor (and will stay that way until they either matriculate a product to commercial sales or enter some type of partnership).

{kind=link}

Seeking Alpha

Options

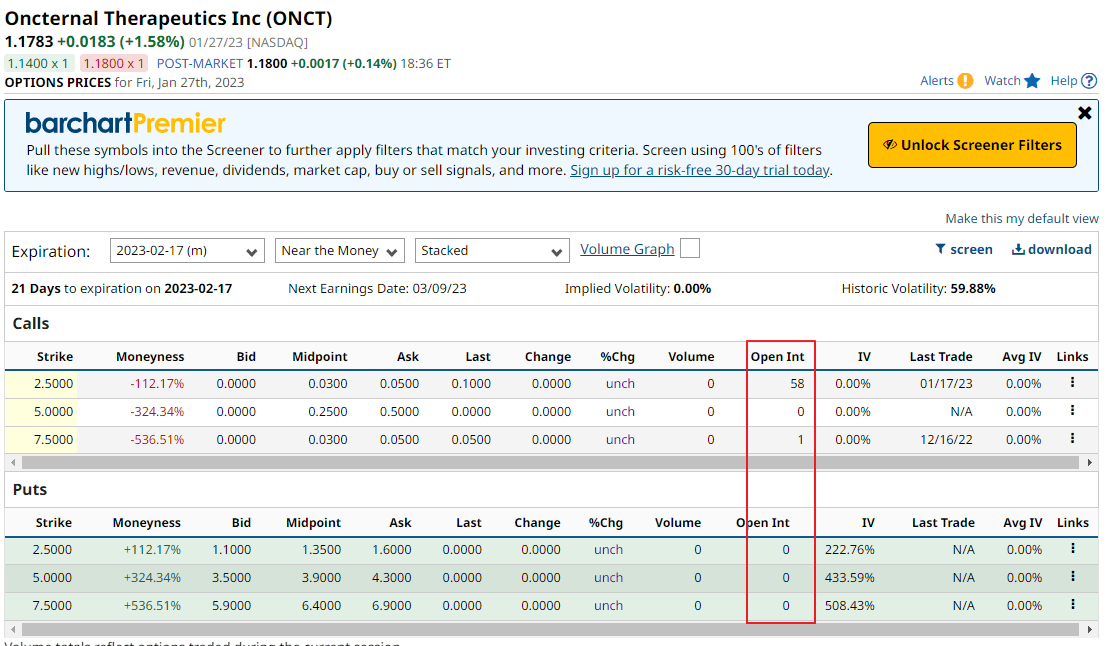

ONCT trades options, but currently they are very illiquid, see open interest column. However, should the market heat up, these may begin to trade with some volume.

{kind=link}

barchart.com

Risks

I believe that biggest risk with ONCT is that it doesn't have enough money to complete its Phase 3 trial in MCL. And despite having good data in earlier studies, raising additional cash in today's biotech market is difficult. Thus there is a real risk that any financing they achieve will be dilutive and thereby depress the stock price further.

Summary

I believe that ONCT's clinical results in MCL are outstanding and that the chances are good that the Phase 3 trial will be successful. However I haven't added to my original speculative sized position because I worry there will be a dilutive financing sometime in the next 18 months. However, for anyone not currently in the stock, I continue to rate it a "Buy" for an initial entry.

For further details see:

Oncternal Therapeutics: Making Progress And Still In Buy Territory