NONOF - One Dangerous Dividend Aristocrat To Ignore And 2 Potentially Set To Soar

2023-04-18 07:15:00 ET

Summary

- A mild recession could be starting in July, and the stock market could be in for a nasty 17% to 33% correction before the new bull market begins.

- Dividend aristocrats are the bluest of blue chips and usually outperform the market by significant amounts in recessionary bear markets.

- But not if you overpay for them by 60%, as with this world-beater drug maker that's expected to grow earnings 100% in the next four years.

- This AA-rated drug maker is pricing in the next three year's worth of growth, and the last time it was this overvalued, it was almost cut in half within a year.

- In contrast, here is the most undervalued aristocrat on Wall Street, 60% undervalued, trading at 6.9X cash-adjusted earnings, and it could deliver 112% returns within three years. This high-yield dividend king is 37% historically undervalued, the best defensive aristocrat bargain, and could soar 70% within three years.

This article was published on Dividend Kings on Monday, April 17th.

---------------------------------------------------------------------------------------

A lot of investors are worried about recession right now, and for good reason.

{kind=link}

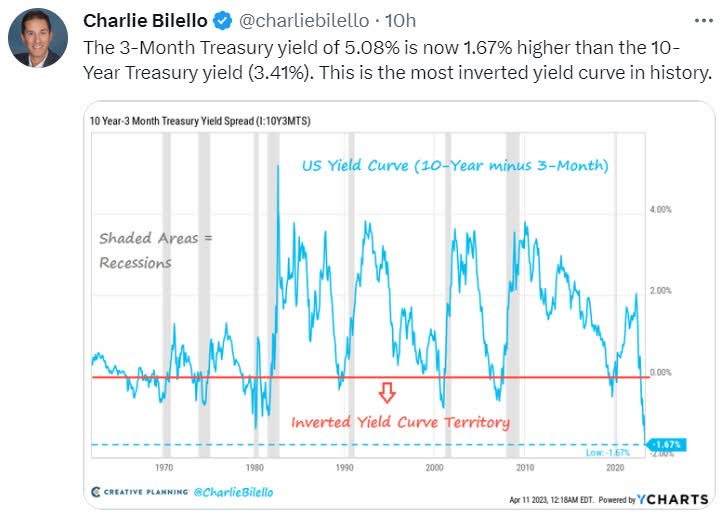

The yield curve, the best recession forecasting tool in history according to studies from the NY, Chicago, Dallas, and San Francisco Feds, is the most inverted in history.

{kind=link}

The bond market thinks a recession could begin as early as July and that the Fed will soon be cutting rates to stimulate the economy.

The Fed says it won't cut this year because inflation is proving stickier than expected.

{kind=link}

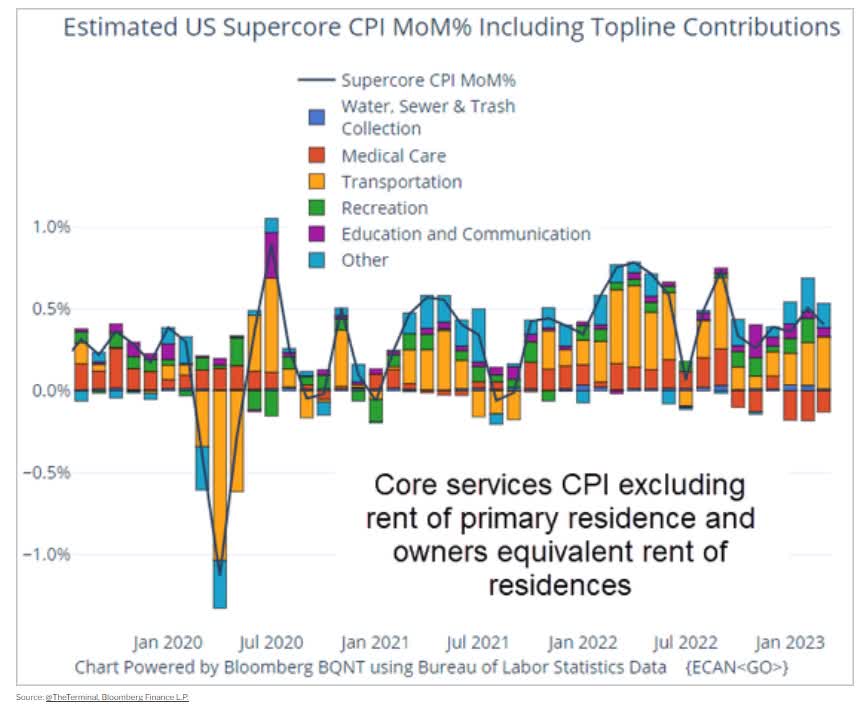

For example, the annualized month-over-month super core inflation, services ex-housing, has been around 5.5% since January 2021 and is still 5.5%.

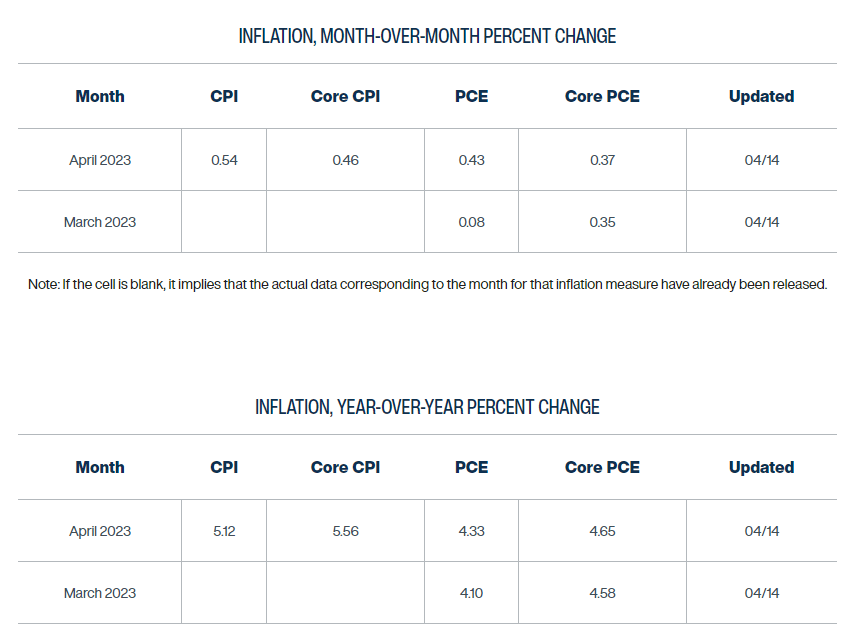

Core CPI is 5.6%, and core PCE (personal Consumption Expenditures Price Index, the official inflation metric) is 4.6%.

{kind=link}

The Cleveland Fed's real-time inflation model expects next month's CPI to go up to 5.1% with month-over-month +0.54% (6.8% annualized).

Core CPI is expected to rise to 5.7% YOY and +0.46% month-over-month (5.7% annualized).

Meanwhile, core PCE is expected to rise to 4.7% YOY and 4.5% annualizing the month-over-month change.

In other words, inflation isn't close to beaten and the Fed knows it can't start cutting yet.

{kind=link}

Even Paul Volker, the legendary slayer of the 1970s stagflation, pivoted too early.

Back in 1980, he slashed the Fed fund rate from 20% to 10% and inflation soared from 0.1% month-over-month to 1% (12.7% annualized) in a matter of months.

The Fed ended up going from 20% to 10% and then back to 20%, but not until it pivoted a 2nd time, for a single meeting.

What does the economic data say?

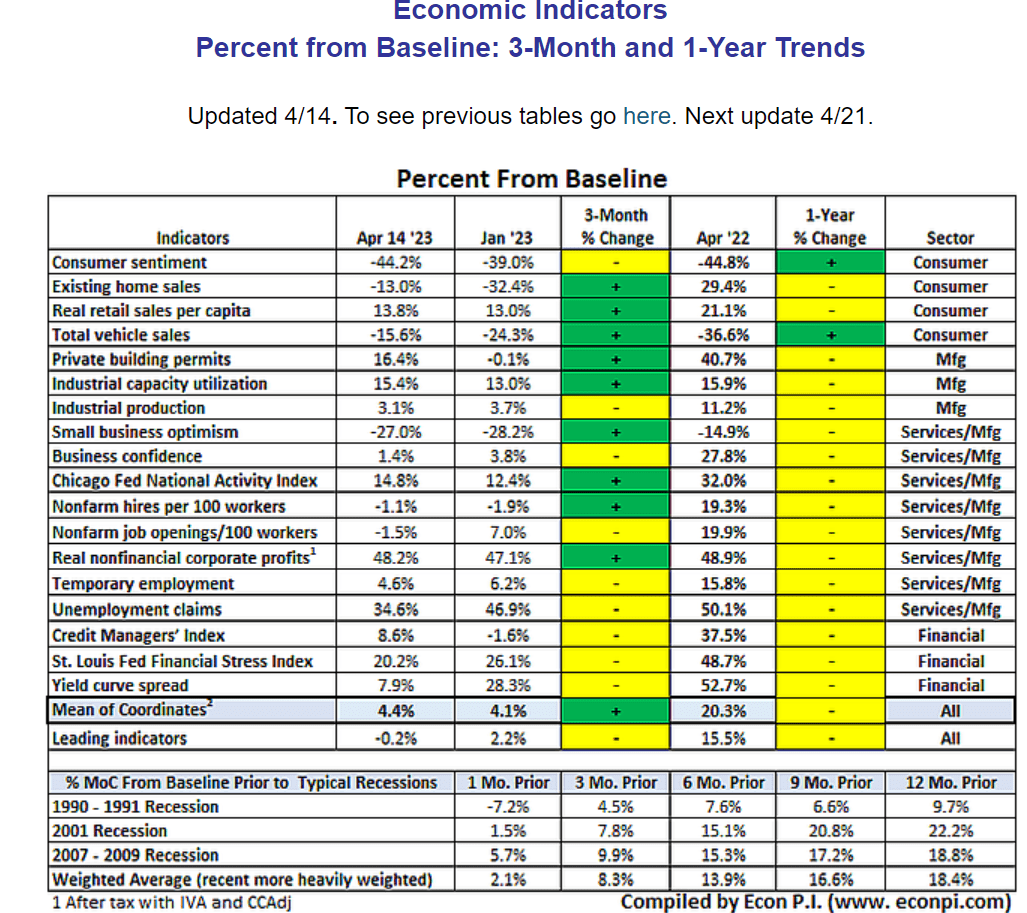

Economic Data Confirms Recession Could Be 3 Months Away

{kind=link}

For the first time in 3 years, the average of 9 leading indicators is below historical base-line and weakening month-over-month at an accelerating pace.

That tells us that the bond market is likely correct and a mild recession is likely months away, potentially beginning in July.

How Bad Could The Recession Be?

For context, 2001's recession was the mildest in history, with a 0.4% GDP contraction that year.

In 2020, including the 8% single-quarter contraction (30% annualized) caused by lockdowns, the economy contracted 2.8%.

During the Great Recession, it contracted by 4.6% over two years.

Since WWII the average recession is a 1.4% GDP contraction.

{kind=link}

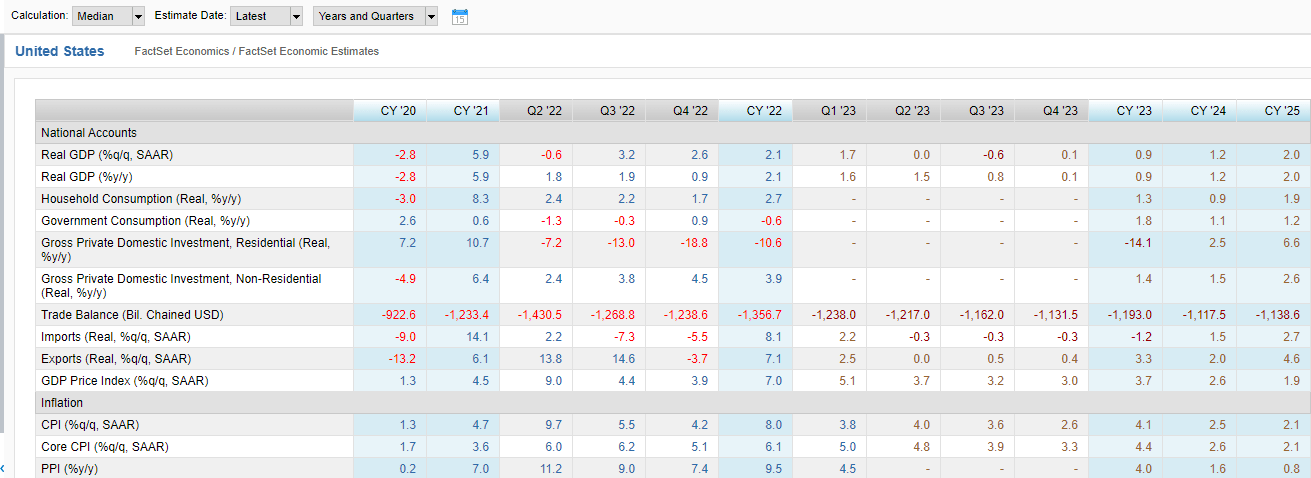

The FactSet median economist consensus is for no official recession, just flat growth in Q2 and then a 0.6% contraction in Q3.

- it was -0.5% in Q3 last week.

Economists expect modest 0.9% growth in 2023 and then growth accelerating to 1.2% in 2024 and returning to normal 2% in 2025.

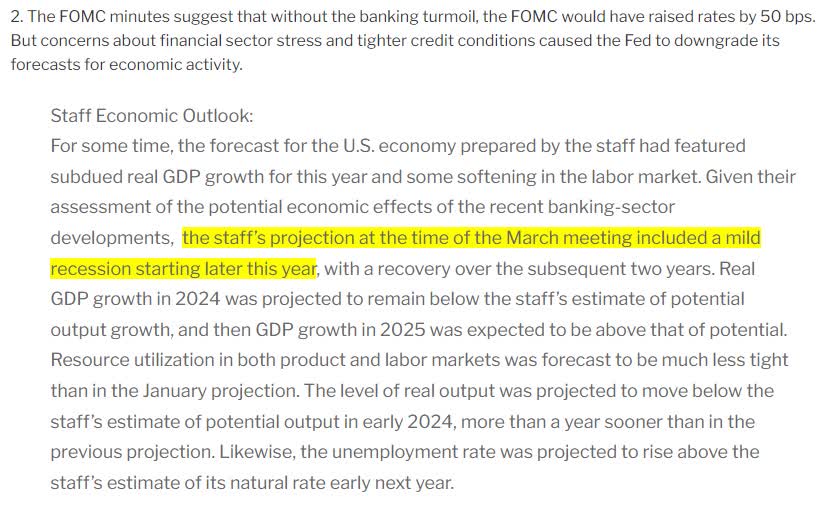

Mind you, the Fed officially now expects a mild recession courtesy of the banking crisis, which is expected to cause credit to contract for small businesses.

{kind=link}

{kind=link}

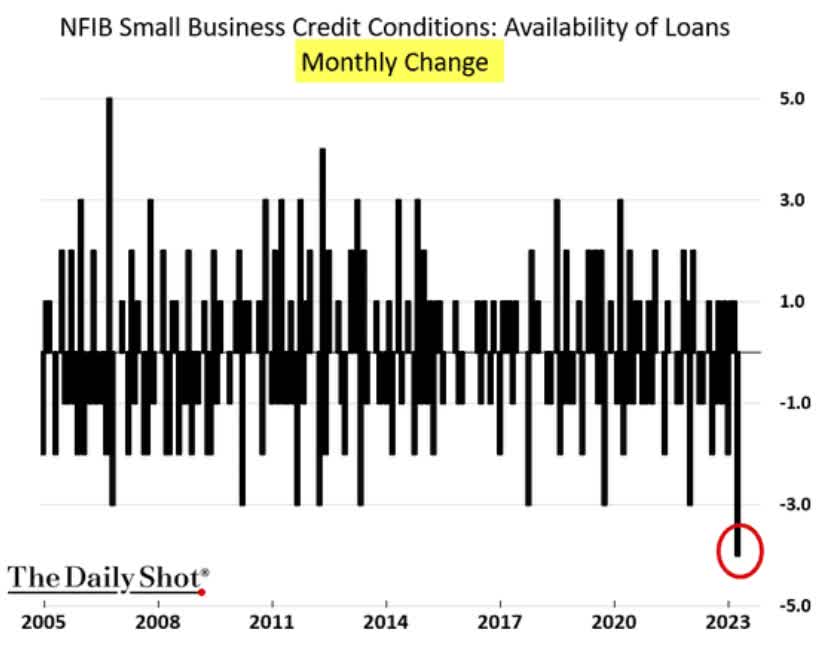

Small businesses have seen loan availability contract at the fastest monthly pace since data tracking began, worse than the Pandemic and Great Recession.

And small businesses employ 50% of Americans.

What Could This Mean For The Stock Market?

Morgan Stanley's base-case forecast is for the S&P 500 (SP500) to bottom at 3,000 to 3,300 around September.

- corresponding to peak earnings pessimism

- and the debt ceiling showdown.

In Q4 the earnings recession began, and the cycle is playing out exactly as it normally does according to SoFi's chief macro strategist.

First the bear market, then the earnings recession, and finally the economic recession.

The earnings recession is currently expected to run into Q1 and Q2. However, that doesn't really price in a recession.

- energy, financials, industrials, and consumer discretionary are the only sectors expected to post positive growth in Q1 and Q2

- these are cyclical sectors.

In a recession, they would all have negative earnings growth, and that's why SoFi expects the earnings recession to last through Q4 2023.

The historical trough P/E range for nonfinancial crises and recessionary bear markets is 13 to 15X forward earnings.

S&P Bear Market Bottom Scenarios (Upper End Of Historical Trough PE Range)

| Earnings Decline |

| S&P Trough Earnings |

| Historical Trough PE 15 |

| Decline From Current Level |

| Peak Decline From Record Highs |

| 0% |

| 228 |

| 3413 |

| 17.5% |

| -29.2% |

| 5% |

| 216 |

| 3243 |

| 21.6% |

| -32.7% |

| 10% |

| 205 |

| 3072 |

| 25.8% |

| -36.3% |

| 13% (average since WWII) |

| 198 |

| 2970 |

| 28.2% |

| -38.4% |

| 15% |

| 193 |

| 2901 |

| 29.9% |

| -39.8% |

| 20% |

| 182 |

| 2731 |

| 34.0% |

| -43.3% |

(Source: Dividend Kings S&P Valuation Tool, Bloomberg.)

This is what is historically likely at the upper end of the P/E range.

Even if high inflation and cost-cutting help corporate America avoid an earnings contraction in 2023, stocks would still be expected (historically speaking) to fall 17.5%.

S&P Bear Market Bottom Scenarios (Historical Midrange 14 Trough P/E)

| Earnings Decline |

| S&P Trough Earnings |

| Historical Trough P/E 15 |

| Decline From Current Level |

| Peak Decline From Record Highs |

| 0% (Consensus, mild recession) |

| 228 |

| 3186 |

| 23.0% |

| -33.9% |

| 5% (Consensus, mild recession) |

| 216 |

| 3027 |

| 26.9% |

| -37.2% |

| 10% |

| 205 |

| 2867 |

| 30.7% |

| -40.5% |

| 13% (Average Since WWII) |

| 198 |

| 2772 |

| 33.0% |

| -42.5% |

| 15% |

| 193 |

| 2708 |

| 34.6% |

| -43.8% |

| 20% |

| 182 |

| 2549 |

| 38.4% |

| -47.1% |

(Source: Dividend Kings S&P Valuation Tool, Bloomberg.)

- Morgan Stanley 3,150 base-case bottom

- SoFi: 3,250 base-case bottom

- Goldman Sachs: 3,250 base-case bottom.

A 27% decline from here would represent a historically average recessionary bear market bottom.

Naturally, every bear market feels like an apocalypse, and the doomsday prophets will be out in force telling you all the reasons why stocks are going to fall 50% more and it's going to be the "worst stock market crash in history."

{kind=link}

But the non-cranks warning about a correction ahead aren't wrong; that's what the majority of the data is pointing to.

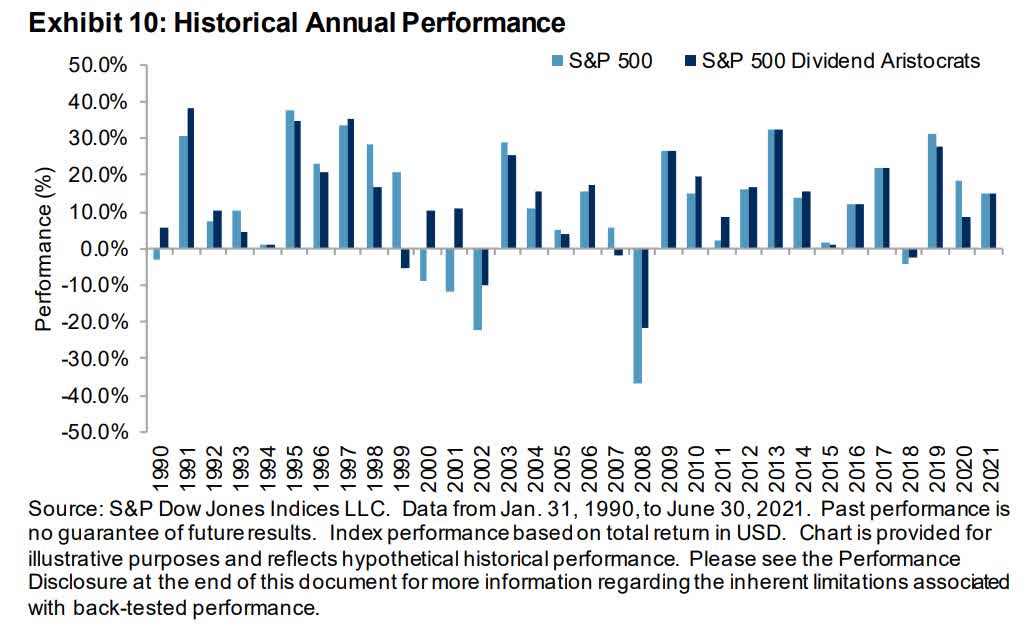

Dividend Aristocrats Are A Great Way To Ride Out The Likely Coming Storm

{kind=link}

The dividend aristocrats are S&P companies with 25+ year dividend growth streaks, the bluest of dividend blue-chips.

- dividend champions are any company with a 25+ year streak.

They historically outperform the market by 1% to 2% annually, not by beating the S&P during bull markets but by falling a lot less in bear markets.

But just because a company is an aristocrat or dividend champion doesn't mean it's a safe harbor to ride out the coming recession.

Let's take a look at two aristocrats that could be in for a dive in the coming storm and two great alternatives.

Not All Aristocrats Are Safe To Buy Before A Recession

You shouldn't expect good returns if you pay an absurd premium for even God's own company.

Some defensive aristocrats like Brown-Forman Corporation ( BF.B ) and The Clorox Company ( CLX ) are trading at 33 to 36 times forward earnings. But believe it or not, those aren't the most overvalued aristocrats.

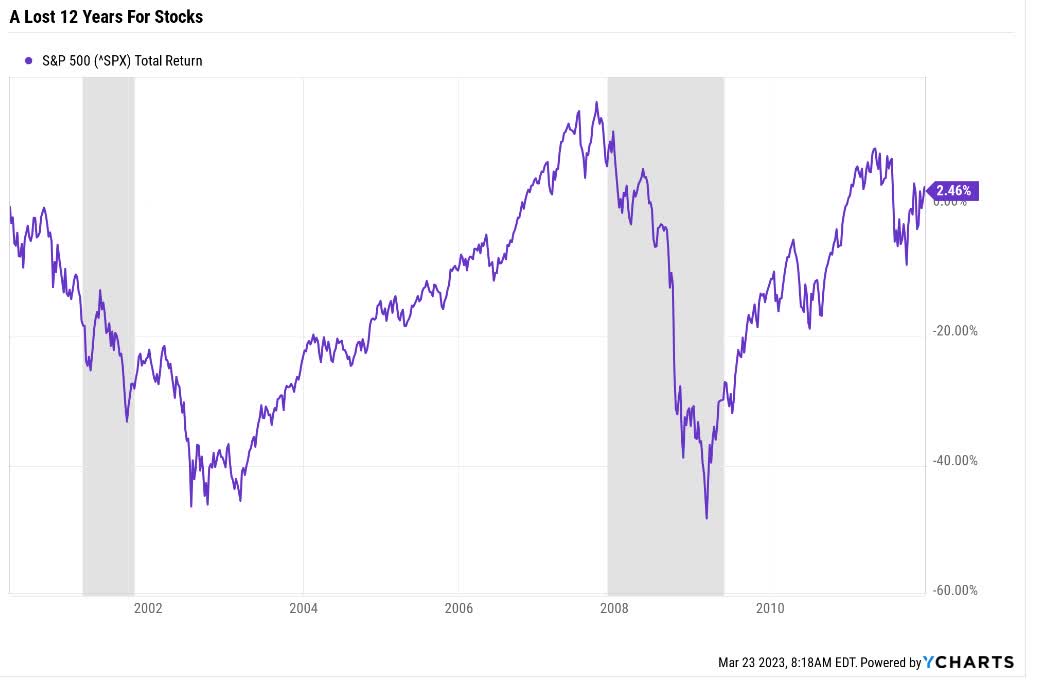

For context, the S&P was 50% historically overvalued in March 2000, the peak of the tech bubble.

And then this happened.

{kind=link}

Dividend Kings uses 50% historically overvalued as its cutoff for "potential sell/trim" prices for this reason.

I've never seen a blue chip that became 50% overvalued that didn't eventually crash.

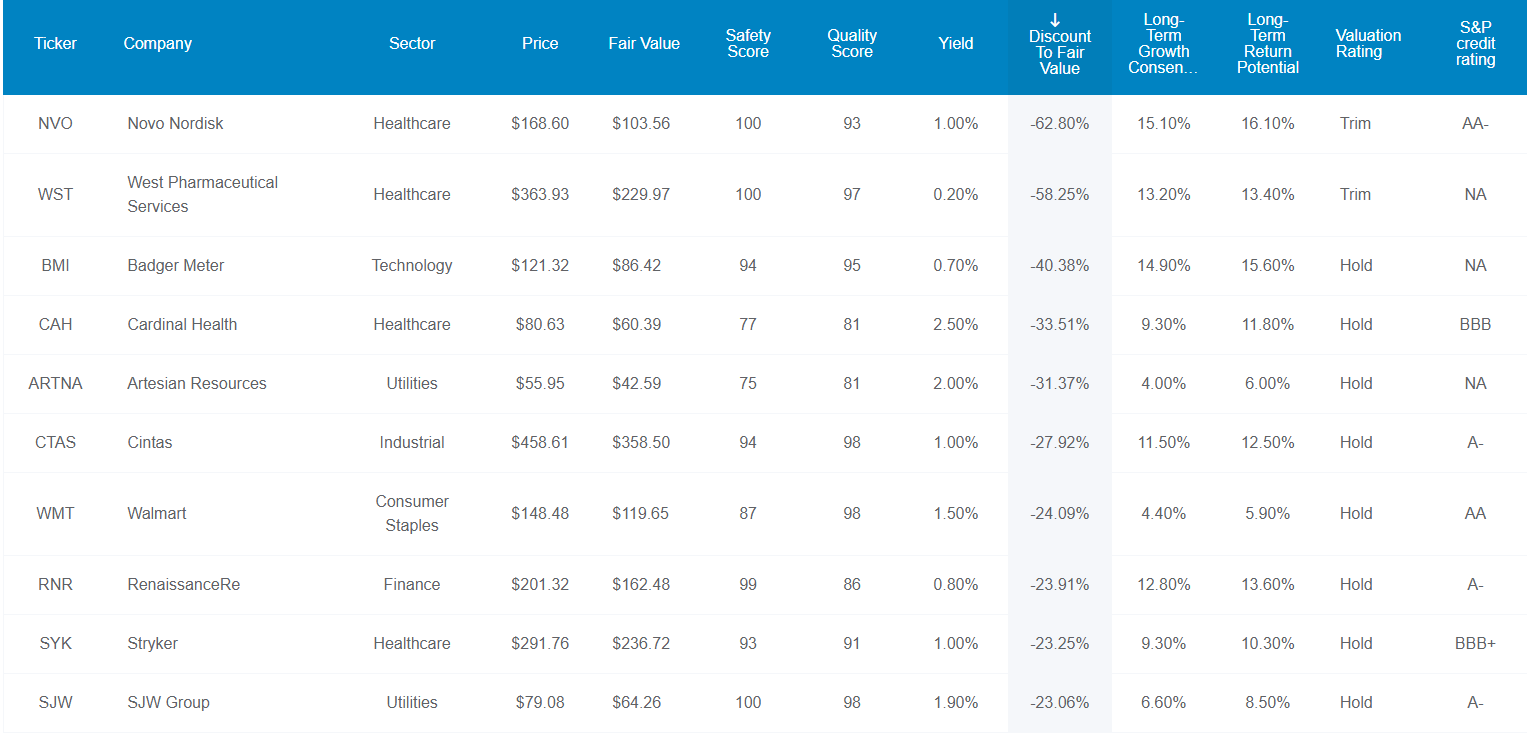

The Most Overvalued Dividend Aristocrats

Dividend Kings Zen Research Terminal

{kind=link}

Today, we'll look at the two most overvalued aristocrats and two solid alternatives.

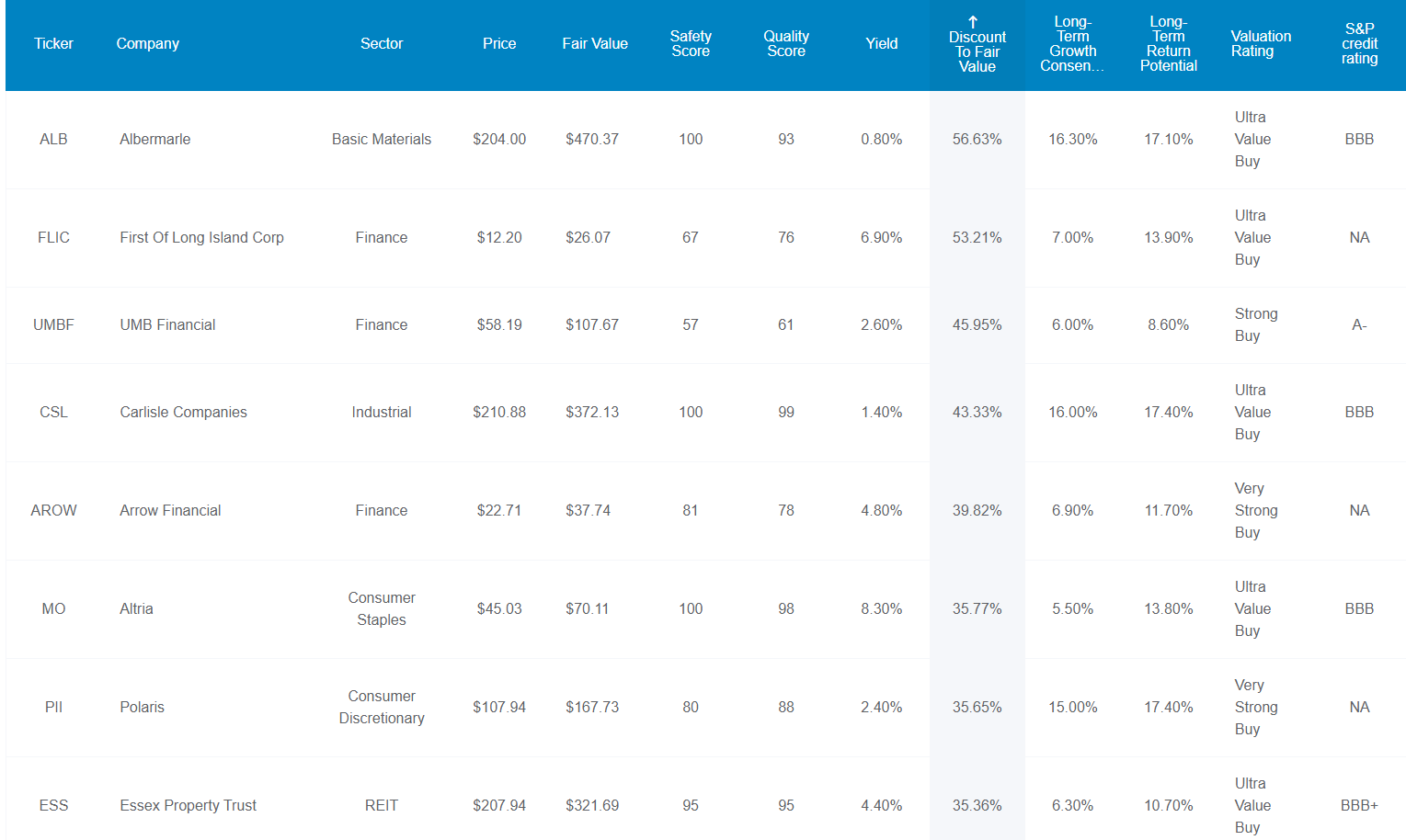

The Most Undervalued Dividend Aristocrats

Dividend Kings Zen Research Terminal

{kind=link}

2 Dividend Aristocrats To Sell And 2 To Buy

Let's start with the most overvalued dividend aristocrat of all.

Novo Nordisk A/S ( NVO ): The Most Overvalued Aristocrat On Wall Street

Further Reading

Why It's In A Bubble

The investment thesis behind NVO is brilliant and easy to understand.

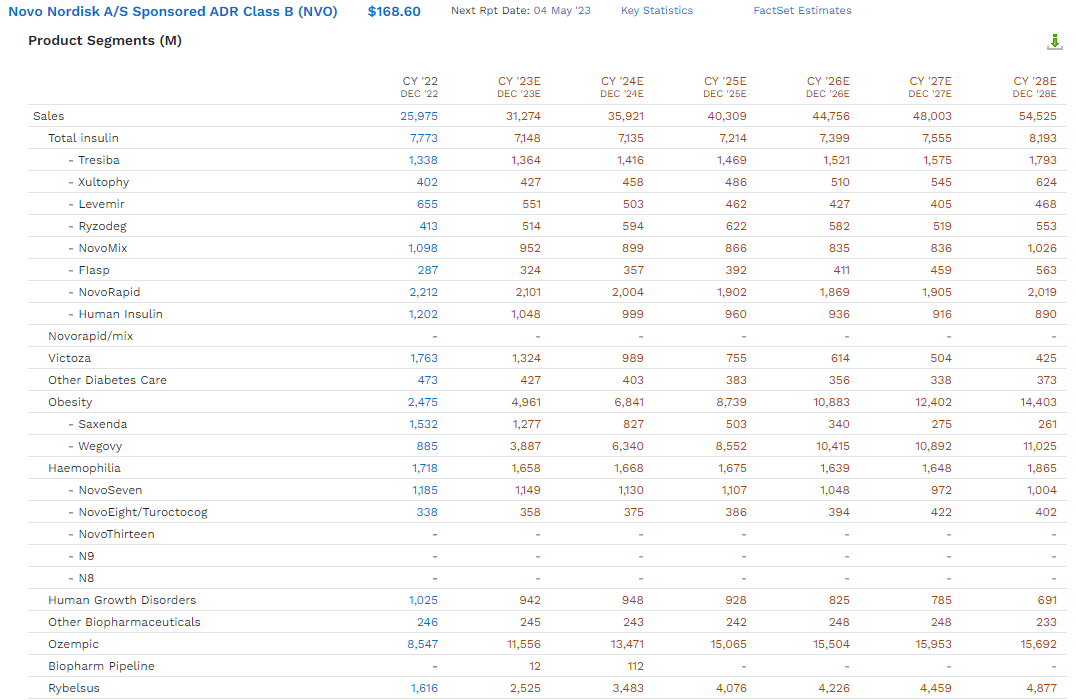

As a pioneer in diabetes care, Novo has been in the business for over 85 years and claims 30% of the $50 billion-plus diabetes treatment market and roughly half of the $20 billion insulin market. The prevalence of diabetes is expected to soar in the coming decades due to an increasingly overweight and aging population, and we expect Novo to maintain its wide moat as it continues to dominate in diabetes and obesity therapy innovation." - Morningstar.

NVO is the world leader in diabetes treatments. While insulin has long been off-patent, NVO has been pioneering new, far superior insulin forms.

While insulin accounts for 30% of Novo's top line, Novo's GLP-1 franchise is now more than 50% of sales and growing, as injectable GLP-1 analog Ozempic (patent 2032) looks best-in-class over Lilly's Trulicity and oral Rybelsus (patent 2032) expands reach into the oral diabetes treatment market. Outside of diabetes and obesity, Novo's more profitable biopharmaceutical arm (roughly 10% of sales) includes NovoSeven and Norditropin but also newer hemophilia and growth hormone products at the launch or late-stage pipeline phase." - Morningstar.

But Wall Street is so in love with NVO right now because of its obesity drugs, Saxnda, Wegovy, and Ozempic.

{kind=link}

In 2022, these three drugs combined for $11 billion in sales, about 50% of the company's revenue and nearly twice that of insulin sales.

By 2028, obesity drugs are expected to generate about $30 billion in sales, more than doubling revenue for NVO.

That's expected to result in about 16% earnings growth, or four times faster than the industry norm.

In other words, in a world where obesity and diabetes are going to be two of the largest health problems for the foreseeable future, NVO is the industry leader.

Summary Facts

- DK quality rating: 93% very low risk 13/13 Ultra SWAN (sleep-well-at-night) global aristocrat

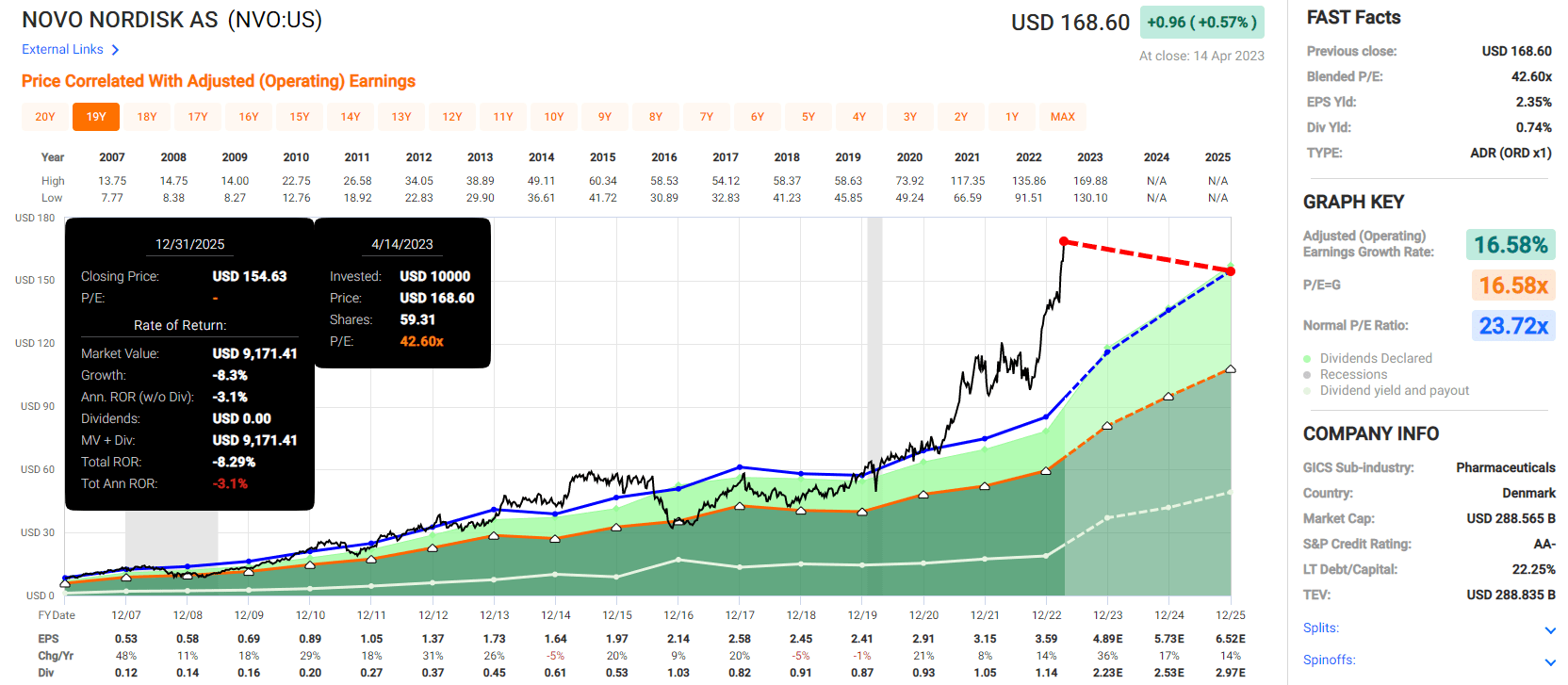

- Fair value: $105.87

- Current price: $168.60

- Historical discount: -59%

- DK rating: Potential Sell/Trim

- Yield: 1.0%

- Long-term growth consensus: 16.1%

- Long-term total return potential: 17.1%.

{kind=link}

NVO growing at 16% to 17% is historically worth about 24X earnings, not 43.

NVO is priced as if nothing could go wrong, and something will invariably go wrong.

Analysts expect 82% earnings growth in the next three years. But NVO has priced in the next three years' worth of growth already. In fact, even if it grows exactly as expected, a return to historical market-determined fair value would result in slightly negative returns over the next three years.

What Kind Of Bear Markets NVO Is Capable Of If You Overpay By This Much

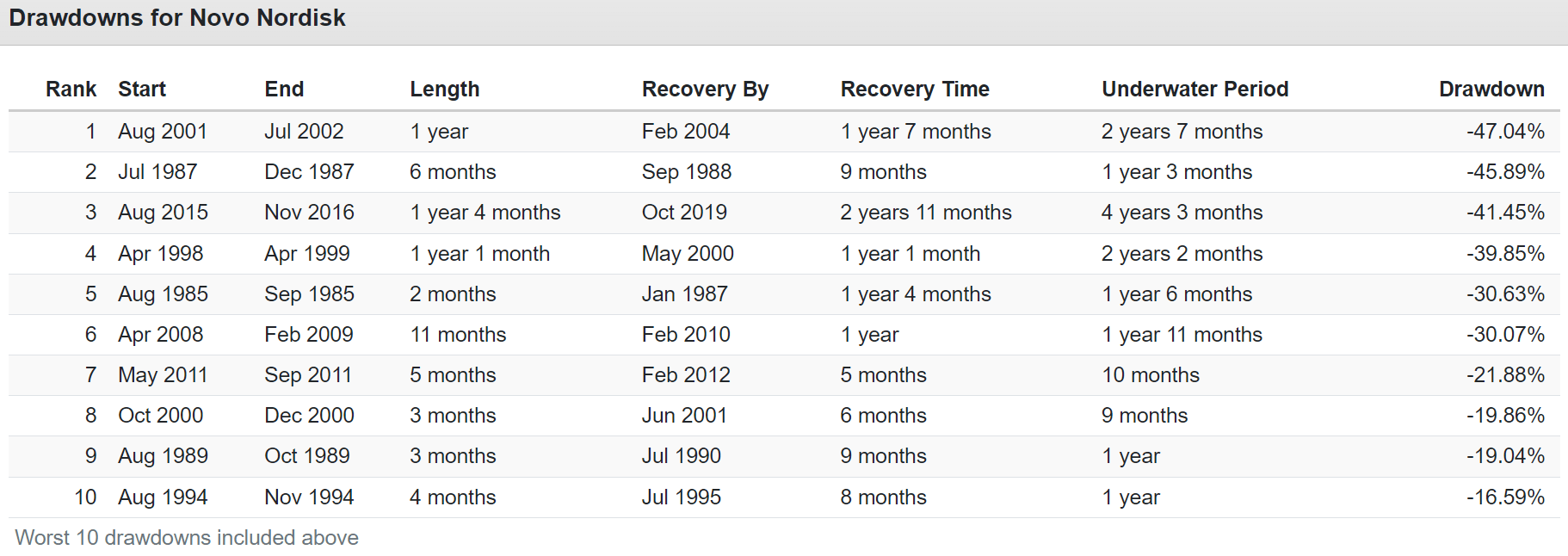

{kind=link}

The last time NVO was this overvalued, during the tech bubble, it spent the next year falling 47%.

Ok, so NVO is the most dangerous (due to valuation) aristocrat to sell today, but what about the best ones to buy ahead of this recession?

2 Great Aristocrat Bargains To Buy Today

First, let's consider the most undervalued aristocrat.

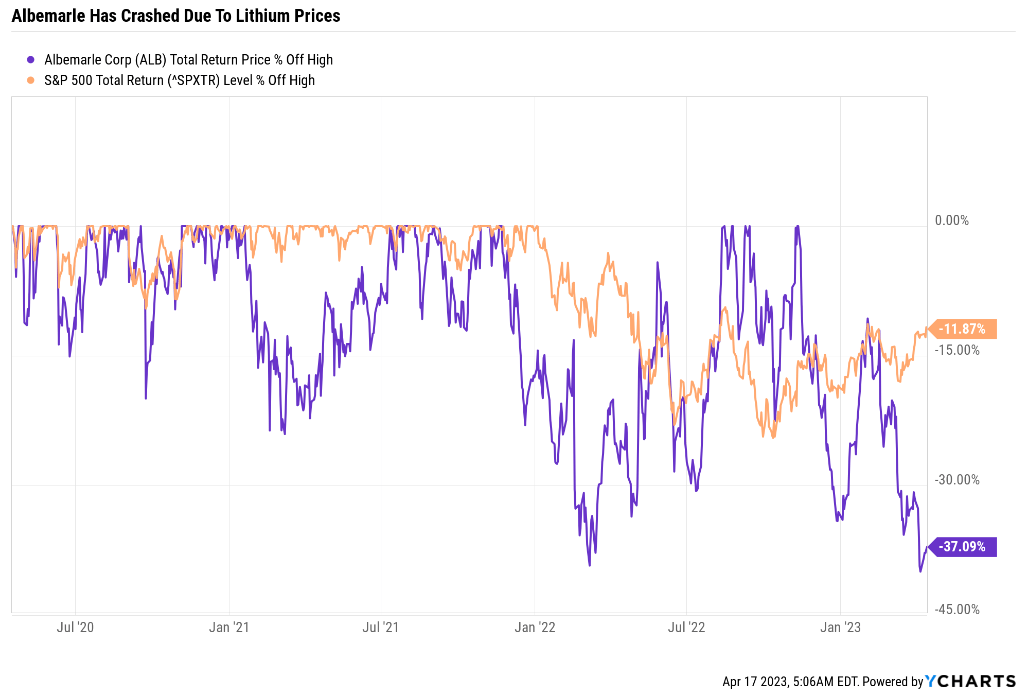

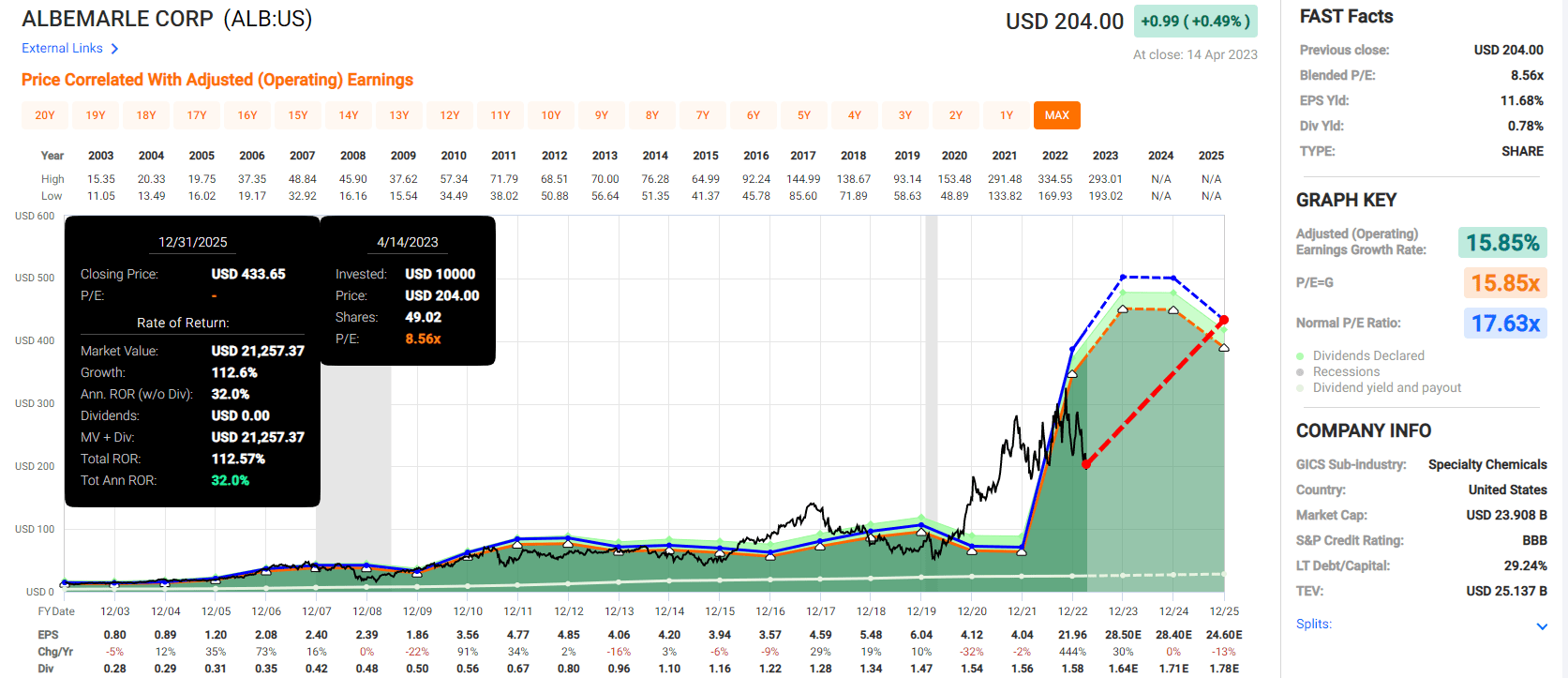

Albemarle Corporation ( ALB ): The Most Undervalued Aristocrat On Wall Street

Further Reading

Why It's In A Bear Market

{kind=link}

Albemarle Corporation is the world's low-cost lithium leader.

ALB benefited from lithium prices soaring to $70,000 per ton as car makers worldwide raced to lock up lithium supplies for the electric vehicle ("EV") transition.

By 2025, lithium prices are expected to normalize at just over $27,000, which is still more than double 2020 levels.

Management thinks lithium prices will average well over $20,000 per ton over the long term, 2X the pre-pandemic level.

ALB's growth thesis is only partially based on higher lithium prices in the future. The key growth driver is lithium demand, specifically from EV adoption.

Europe is talking about requiring 100% EVs by 2035, and the EPA is potentially going to impose new regulations requiring 66% EVs by 2032.

The chances that these regulations actually go into effect is small, given the logistical challenges involved with such rapid EV ramp-ups.

But the point is that demand for lithium is expected to soar in the coming decades as the race for "white gold" heats up.

For example, in 2022, global EV sales were up 64%; by 2030, global lithium demand is expected to soar 400% to 3.7 million tons per year.

ALB has a solid plan to deliver 20% to 30% volume growth over the next five years.

Summary Facts

- DK quality rating: 93% very low risk 13/13 Ultra SWAN (sleep-well-at-night) aristocrat

- Fair value: $413.25

- Current price: $204.00

- Historical discount: 51%

- DK rating: potential Ultra Value Buffett-style table-pounding "fat pitch" buy

- Yield: 0.8%

- Long-term growth consensus: 16.3%

- Long-term total return potential: 17.1%.

{kind=link}

ALB is expected to have negative growth in 2024 and 2025, but it's trading at an anti-bubble valuation of 8.7X trough earnings and 6.9X cash-adjusted earnings.

That's why it could potentially more double in the next three years, delivering Buffett-like 32% annual returns.

Albemarle Corporation 's Best Bear Market Recovery Rallies Since 1994

| Time Frame (Years) |

| Annual Returns |

| Total Returns |

| 1 |

| 178% |

| 178% |

| 3 |

| 68% |

| 378% |

| 5 |

| 31% |

| 280% |

| 7 |

| 31% |

| 561% |

| 10 |

| 22% |

| 655% |

| 15 |

| 19% |

| 1268% |

(Source: Portfolio Visualizer Premium.)

Want to earn Buffett-like returns for 15 years? Then buying this fast-growing anti-bubble aristocrat after a 40% crash is a potentially great way to do it.

Altria Group, Inc. ( MO ): The Most Undervalued Defensive Aristocrat On Wall Street

Now let's consider a defensive (recession-resistant, historically low volatility) aristocrat that could be just what the doctor ordered ahead of a recession.

Further Reading

Why It's In A Bear Market

{kind=link}

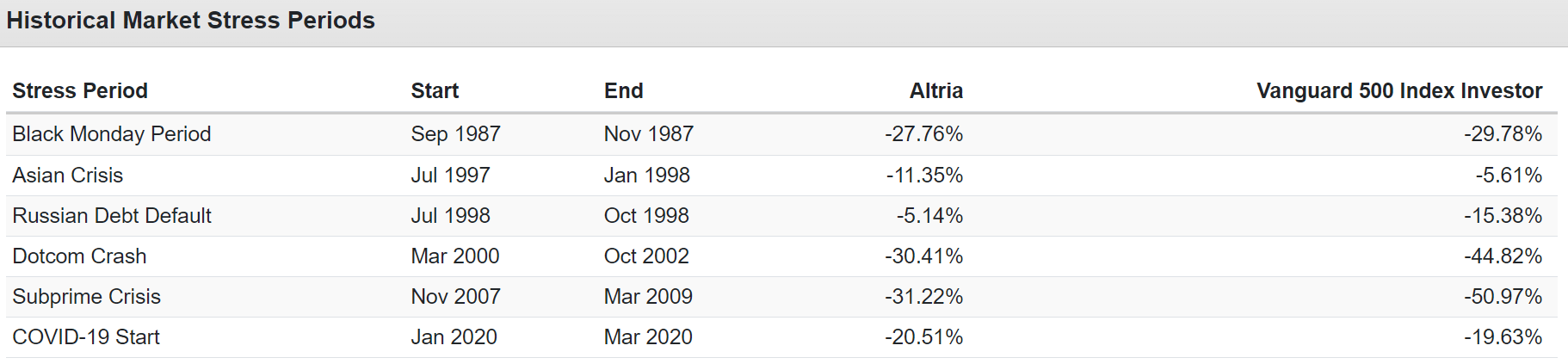

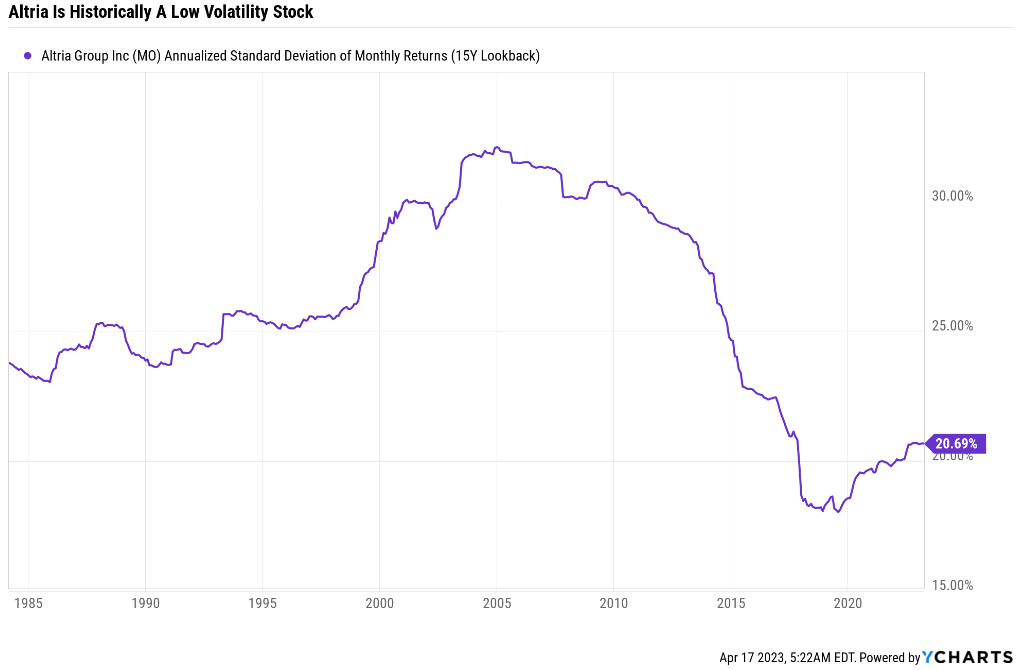

MO isn't always defensive in a market decline but is historically a low-volatility stock.

{kind=link}

For context, the average standalone company has 28% annual volatility and the average aristocrat 25%.

{kind=link}

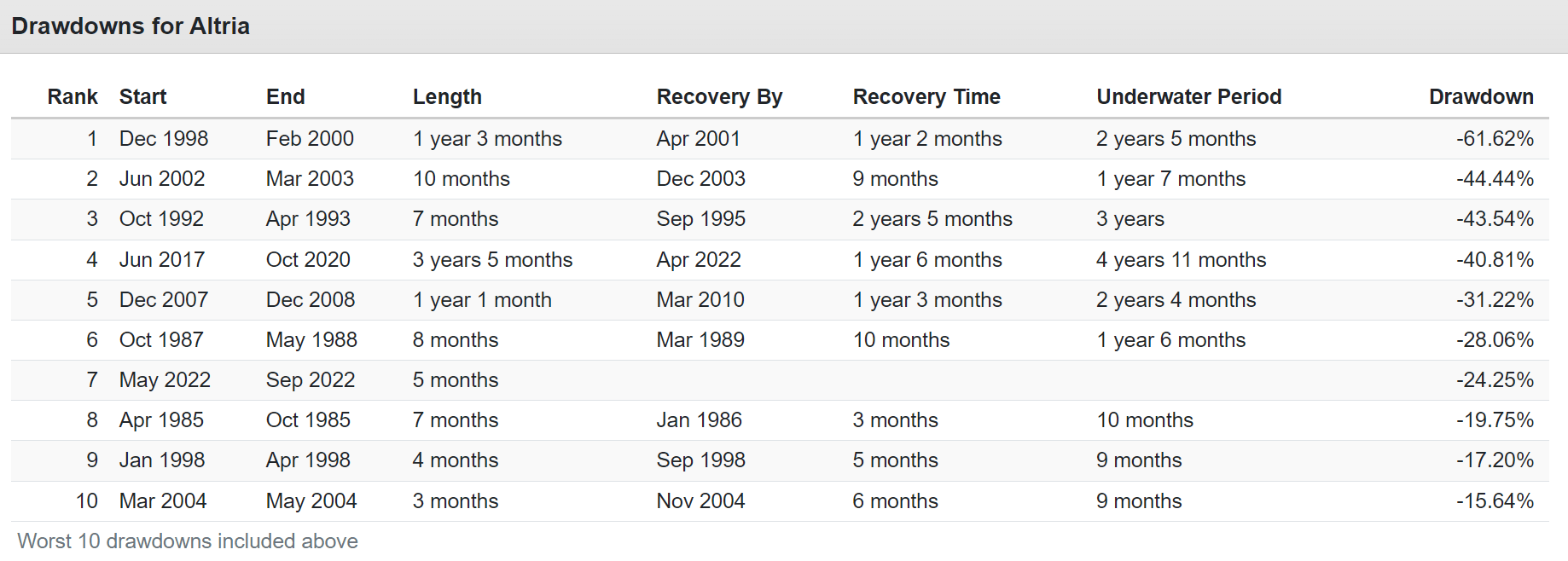

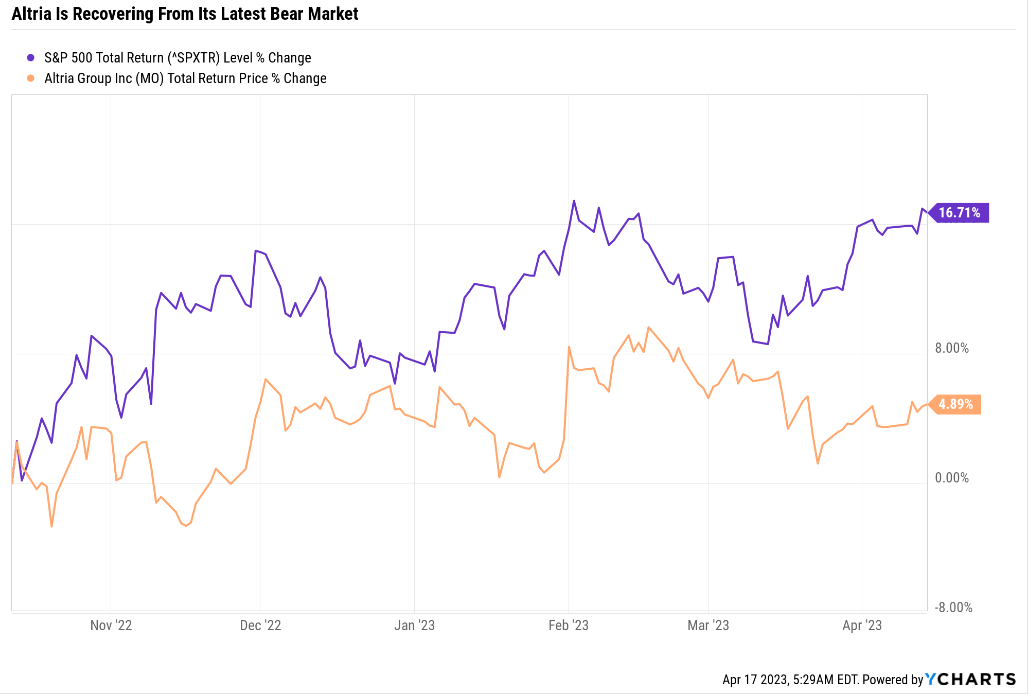

MO investors might not realize it, but MO's bear market ended in April 2022 when its total return price, including dividends, hit a new all-time high.

However, it then began a new bear market, falling up to 24% (so far) since May 2022.

{kind=link}

Since bottoming on October 12th, along with the rest of the market, MO has soared almost 17%.

Why is it in another bear market? Because MO has been flailing with its efforts at transitioning to a smoke-free future.

Its 2018 $13 billion investment in Juul was a disaster.

It paid 40 times EV/EBITDA for a company that was growing at 100% at the time, but which the FDA then cracked down on hard. The FDA is trying to ban Juul in the US, though a court has stayed that order for now.

MO took on $13 billion in debt to buy a 35% stake in Juul and has ended its partnership with the company, writing down the value of its investment to $250 million.

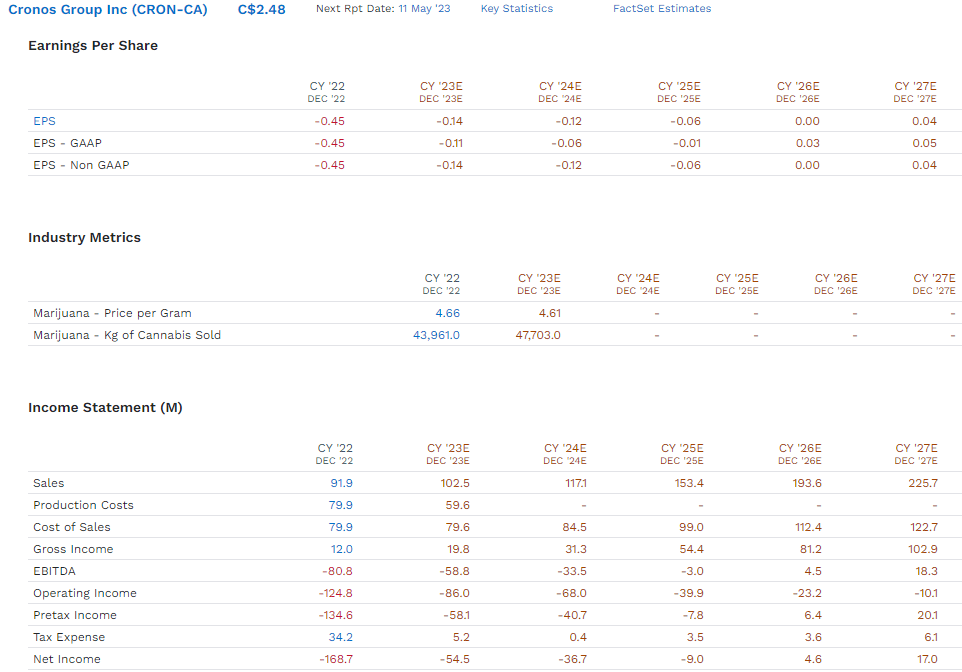

Its $1.8 billion investment in Cronos ( CRON ), which left it with 45% of the company, was also made at the top of that market (cannabis). MO recently declined to exercise its warrants to buy shares at a valuation of $10 billion.

- it's taking a $483 million write-down on Cronos

- likely not to be the last write-down.

{kind=link}

Cronos is a fast-growing company but isn't expected to turn a profit until 2026 and not turn a profit on an EPS basis until 2027.

In October 2022, MO and PM reached a deal in which it would give up its revenue share rights to iQos in the U.S. for $2.7 billion.

Instead, MO signed a joint venture with Japan Tobacco ( JAPAF ) to market its brand of heat sticks in the U.S. (MO will get 75% of that revenue).

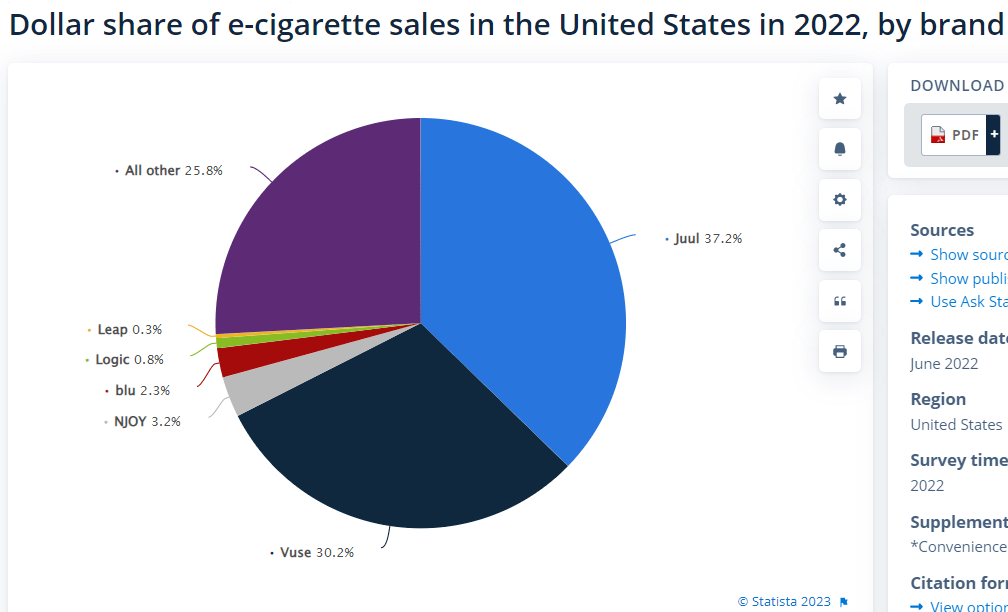

MO has also announced it's buying nJoy for $2.75 billion (using the PM buyout funds), the only vaping company to get FDA approval in the U.S. so far.

{kind=link}

The FDA has denied BTI's Vuse approval in the U.S. and is trying to get its products pulled from the market, the same as Juul.

- BTI is appealing.

If the FDA is successful, MO's NJOY will automatically become the #1 vaping brand in the U.S.

MO recently held an investor day outlining its long-term plan for 4% to 6% EPS and dividend growth partially driven by a return to international sales.

We believe the international smoke-free and non-nicotine categories combined represent multi-billion dollar opportunities for us. Our teams are evaluating these opportunities and expect to finalize strategies for these growth areas over the next 12 months. We intend to share specific goals for these areas once established."

Altria said those non-nicotine offerings could include cannabis and caffeine pouches." - Seeking Alpha .

I'll be covering MO's plans in-depth in an upcoming article.

- caffeine pouches are likely to fall flat though cannabis is indeed a popular growth market.

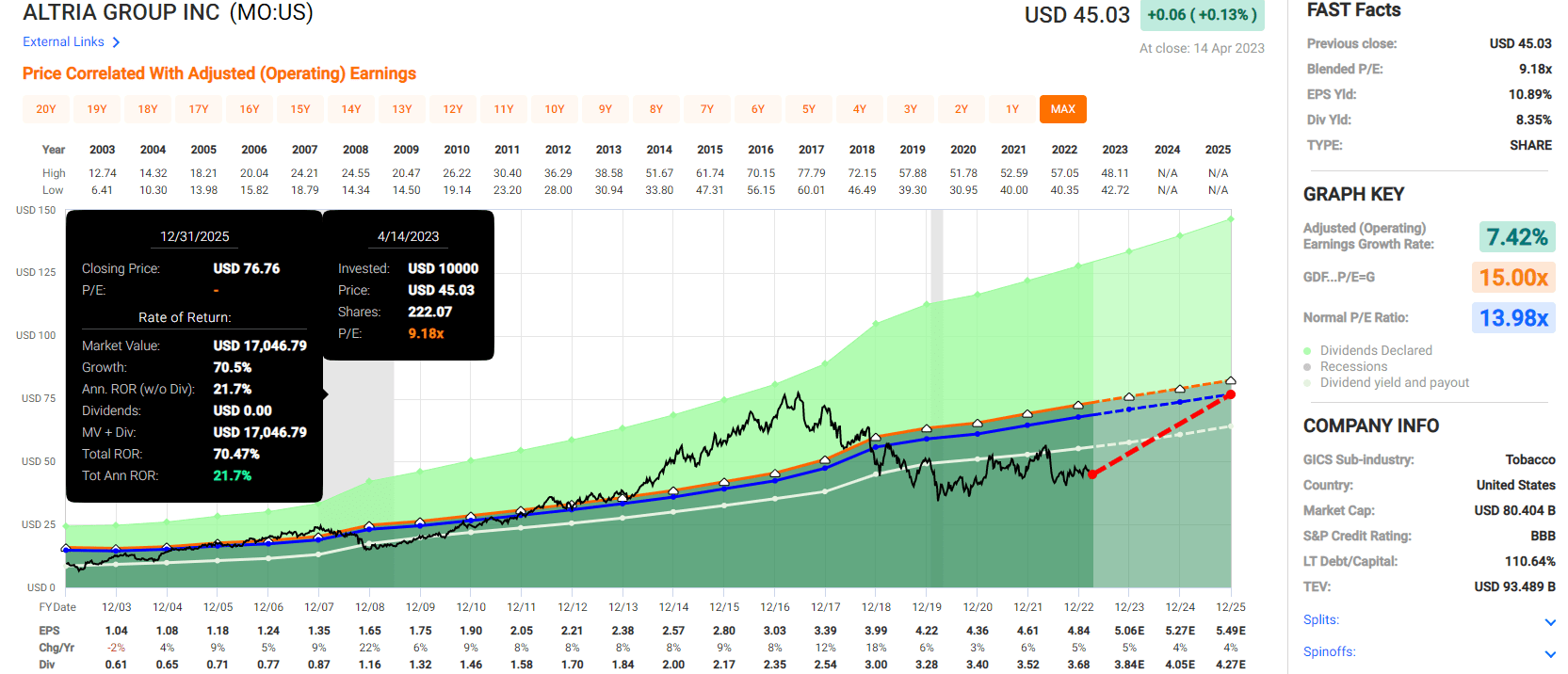

Summary Facts

- DK quality rating: 98% medium risk 13/13 Ultra SWAN (sleep-well-at-night) dividend king

- Fair value: $71.50

- Current price: $45.03

- Historical discount: 37%

- DK rating: potential Ultra Value buy

- Yield: 8.3%

- Long-term growth consensus: 5.5%

- Long-term total return potential: 13.8%.

{kind=link}

If MO grows as expected, a modest 4% to 5% in the coming years, and returns to historical market-determined fair value of 14 times earnings, it could deliver 70% total returns or 22% annually through 2025.

Altria's Best Bear Market Recovery Rallies Since 1985

| Time Frame (Years) |

| Annual Returns |

| Total Returns |

| 1 |

| 157% |

| 157% |

| 3 |

| 54% |

| 264% |

| 5 |

| 44% |

| 520% |

| 7 |

| 42% |

| 1056% |

| 10 |

| 30% |

| 1251% |

| 15 |

| 25% |

| 2668% |

(Source: Portfolio Visualizer Premium.)

Buying MO in a bear market is a great way to earn Buffett-like returns and change your life.

Bottom Line: Don't Buy Outrageously Overvalued Aristocrats When You Can Buy Screaming Bargain Aristocrats

Let me be clear: I'm NOT calling a top in NVO or bottom in ALB or MO (I'm not a market-timer).

Even Ultra SWANs can fall hard and fast in a bear market.

Fundamentals are all that determine safety and quality, and my recommendations.

- over 30+ years, 97% of stock returns are a function of pure fundamentals, not luck

- in the short term; luck is 25X as powerful as fundamentals

- in the long term, fundamentals are 33X as powerful as luck.

NVO is one of the world's best companies, an AA-rated ultra-swan that is wonderfully positioned to fight diabetes and obesity for years and decades to come.

But NVO is priced at 43X earnings, an almost 60% historical premium that is just asking for trouble.

Is it a defensive aristocrat? Yes, it's a drug maker.

Is it a historically low volatility stock? Yes.

Is it growing like a weed? Yes, earnings are expected to double in the next four years.

But all those wonderful attributes are already baked into the share price, and that's why anyone buying today might face negative returns over the next three years (along with a 30% to 50% crash in the coming market correction).

In contrast, ALB and MO are two of the most undervalued aristocrats you can safely buy today for the long-term.

ALB is literally the most undervalued aristocrat on Wall Street, 60% undervalued, the mirror image of NVO's outrageous premium.

And MO is once again in a bear market, after clawing its way out of the last one.

There are no risk-free stocks, not even undervalued Ultra SWAN aristocrats.

But buying MO at a 37% discount or ALB at a 60% discount is a wonderfully prudent way of putting your savings to work the smart way.

When the margin of safety is this high, a lot of bad news is already priced in.

Thus, by merely being terrible less than expected, aristocrats like Albemarle Corporation and Altria Group, Inc. offer the potential for 112% and 70% returns in the next three years.

That's literally Buffett-like return potential from aristocrat bargains hiding in plain sight.

For further details see:

One Dangerous Dividend Aristocrat To Ignore And 2 Potentially Set To Soar