OKE - ONEOK: 25+ Years Of Uninterrupted Dividends From This Toll Road-Like Business

Summary

- ONEOK is a midstream player offering investors a solid dividend and fee-based profits that are largely insulated from commodity price volatility.

- The vast majority of its customers are investment-grade rated, providing further insulation from economic uncertainty.

- I also highlight the dividend, balance sheet, valuation, and other important points.

With all the talk about layoffs hitting office jobs, particularly in the tech sector, it's important to focus on one's own nest egg. That means being financially resilient in the event of a major life event such as a job loss.

That's why it pays to invest in toll-road like businesses that have steady revenue streams. In turn, they provide investors with dividend income that's less vulnerable to economic downturns.

This brings me to ONEOK ( OKE ), which is an energy midstream company that's great for investors who don't like dealing with Schedule K-1s come tax time.

The stock has done rather well since my last bullish take on it in late September, giving investors a 34% total return since then, and far surpassing the 11% return of the S&P 500 ( SPY ) over the same timeframe. Let's explore why OKE remains a good buy at present for income investors.

Why OKE?

ONEOK is a large midstream corporation that owns a premier collection of natural gas liquids systems, connecting suppliers in the Rocky Mountain, Mid-Continent, and Permian Regions of the U.S. to key markets.

It's also vertically integrated with an extensive network of gathering, processing, storage and transportation assets. This business model enables ONEOK to capture profits across the midstream value chain.

It also helps that the majority of OKE's earnings are fee based, and thereby not tied to swings in commodity prices. This ranges from 80% fee-based for OKE's natural gas gathering and processing segment to 90% and 95% for the natural gas liquids and natural gas pipelines business segments.

Plus, the vast majority (around 85%) of OKE's customers are investment grade rated, providing further insulation from economic uncertainty. OKE is also expected to generate significant amounts of free cash flow in this and the coming years, with which it could materially ramp up its share buybacks, as noted by Morningstar in its recent analyst report :

With the reduced capital program, Oneok is forecast to have material levels of excess cash flow in 2023, perhaps 24 months behind other U.S. midstream peers to buy back more stock. We estimate there could be up to $675 million in buybacks in 2023, though knowing Oneok's penchant for finding accretive growth projects, this is also equally likely to be plowed back into attractive growth assets.

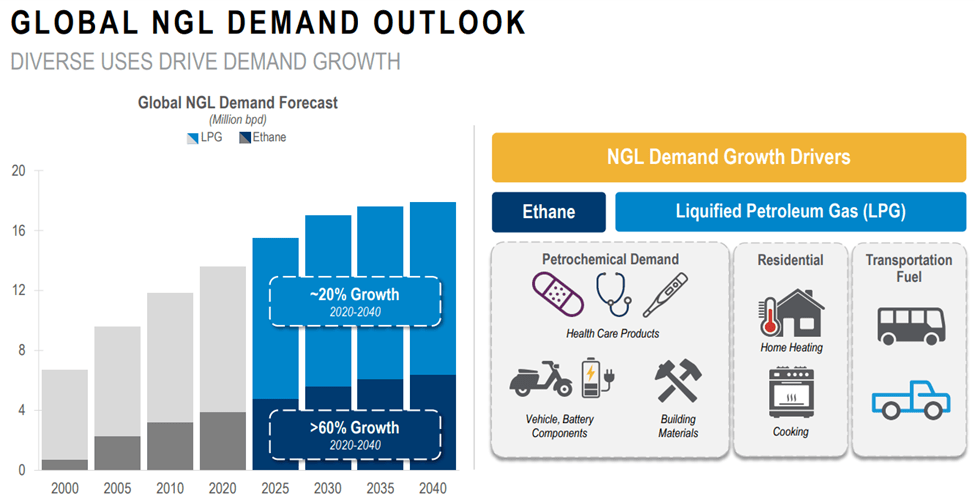

Looking ahead, OKE is well-positioned to benefit from strong global demand for NGL, which has a wide range of uses, ranging from petrochemicals to home heating and cooking. As shown below, both LPG and Ethane NGL products are expected to see continued growth through at least 2040.

{kind=link}

Notably, J.P. Morgan ( JPM ) recently upgraded OKE's shares from a price target of $71 to $75, seeing value in its Bakken shale exposure, as noted by their analyst below:

The Bakken's surprising 40-plus rigs point to steady production after the recent storms wane and winter slows down, according to JPM's Jeremy Tonet, adding Oneok "clearly possesses the highest Bakken-rich gas/NGL volume operating leverage, with significant torque to NGL volume growth and incremental ethane extraction."

Meanwhile, OKE carries a safe balance sheet with a net debt to EBITDA ratio of 3.8x, sitting below the 4.5x level that ratings agencies generally consider to be safe for midstream companies. Management also views getting down to the 3.5x level as being its long-term goal.

Importantly for dividend investors, OKE has paid an uninterrupted dividend (no cuts) for over 25 years, and recently raised its dividend by 2.1% last month (5-year dividend CAGR of 5.5%), resulting in a 5.7% forward yield. The new dividend also remains well-covered at a 67% payout ratio based on trailing 12 months' operating cash flow.

Lastly, OKE is not as cheap as it was when I last visited it in late September, but remains appealing at the current price of $67.26 with an EV/EBITDA of 13.3, especially after its recent drop from the $70 level.

{kind=link}

With potential for material improvement in free cash flow this year, OKE could return more capital to shareholders via buybacks or pursue accretive growth projects. Analysts have a consensus Buy rating with an average price target of $71.42 , which translates to a potential 12% total return over the next 12 months.

Investor Takeaway

ONEOK is an attractive midstream player, offering investors a safe dividend that's been uninterrupted for over 25 years, and fee-based profits, which are largely insulated from commodity price volatility. OKE also enjoys strong Bakken shale exposure, from which it could extract appealing value through its extensive gathering, processing, storage and transportation network. Lastly, while OKE is no longer cheap, it remains reasonably priced for potentially solid long-term income and growth.

For further details see:

ONEOK: 25+ Years Of Uninterrupted Dividends From This Toll Road-Like Business