OKE - ONEOK: A Lot More Than Its Dividend

2023-04-25 07:49:57 ET

Summary

- ONEOK pays a high dividend of 5.7%.

- Here I put forth the role of natural gas in the Future Energy transition and how natural gas' prospects are more than just a transition fuel.

- ONEOK's prospects are to a large extent immune to the natural gas cycle. The business model is more than 90% derived from fees associated with transporting and processing natural gas.

Investment Thesis

ONEOK ( OKE ) is a midstream player servicing the natural gas market.

I believe that since everyone reading this analysis already knows that ONEOK has a very attractive dividend yield of approximately 5.7%, rather than trudge over a well-beaten path, I find it more insightful to look beyond ONEOK's high dividend yield to other, possibly even more compelling, considerations to be bullish on ONEOK.

Natural Gas Liquids, More Than Just a Transition Fuel

ONEOK gathers and processes producers' natural gas. More specifically, its business is tied to the natural gas liquid volumes that flow through its processing facilities, rather than upstream natural gas producers which are directly tied to natural gas prices.

{kind=link}

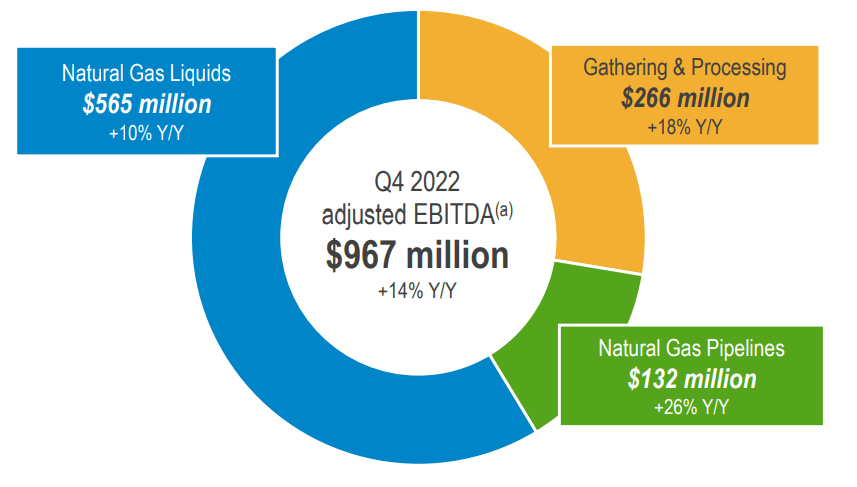

As you can see above, the biggest proportion of its EBITDA is tied to its Natural Gas Liquids segment. This segment is responsible for gathering, and fractionating unfractionated natural gas liquids.

In plain English this means, ONEOK takes raw natural gas from upstream producers which contain a mixture of Natural Gas Liquids components and seeks to remove the mixture of Natural Gas Liquids (the unfractionated natural gas liquids, "NGLs"), resulting in residue natural gas (primarily methane) and purity products.

These purity products are then sent to their customers, such as petrochemical companies, propane distributors, ethanol producers, and refineries.

Moving on, in the past 12 months, since the Russian invasion, the calls for the energy transition have picked up momentum. Today, citizens and all kinds of entities together call for the energy transition to gather momentum.

This means reducing our carbon-based energy supply down from approximately 60%, depending on the country, to around 20%.

The bulk of the energy transition will be supplemented by solar panels and wind turbines, with the remainder 20% being made up of natural gas and oil for freighting and transportation (particularly airplanes).

You may retort that my view of Future Energy is too quick to discount oil's dominance. And while I would fully acquiesce to that argument, my assertion here is not about oil's prospects. Rather, it's about natural gas' prospects as a key transition and destination fuel.

{kind=link}

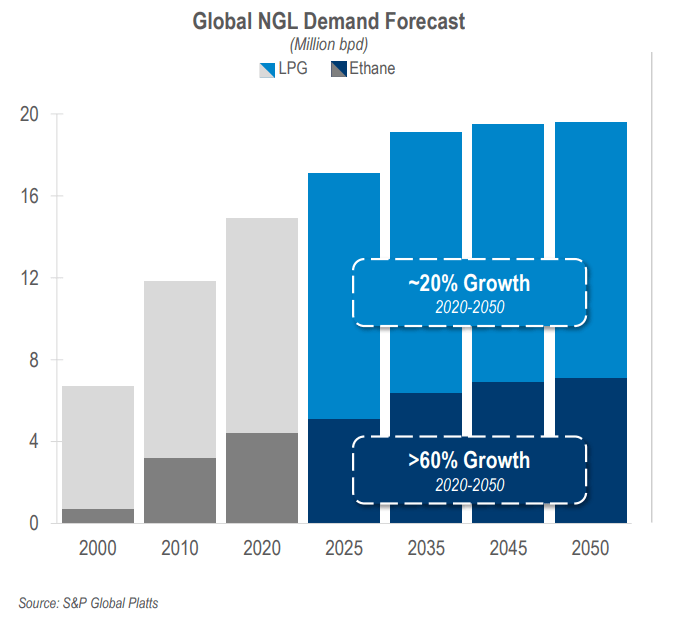

The graphic above echoes my assertion that prospects for ethane, a natural gas liquid, are expected to ramp up substantially in the coming decades.

Simplicity is the Key to ONEOK's Investment Thesis

{kind=link}

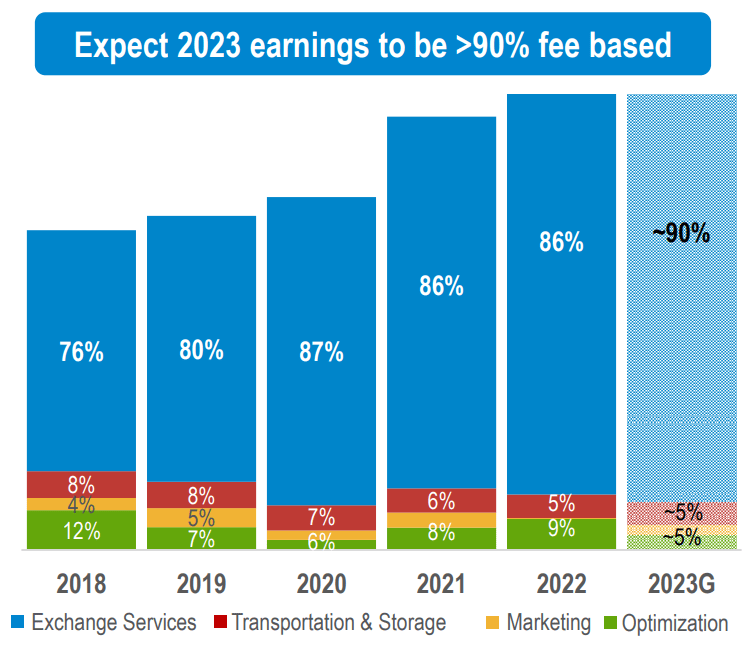

As you can see above, approximately 90% of ONEOK's earnings are fee-based. In practical terms, this means that the business's prospects are to a certain extent insulated from the vicissitudes of the natural gas market.

Indeed, given that right now natural gas prices are close to a 30-year low (after adjusting for inflation), this speaks to the strength of ONEOK's intrinsic value at present.

Next, let's turn our focus to 2023 as a whole.

{kind=link}

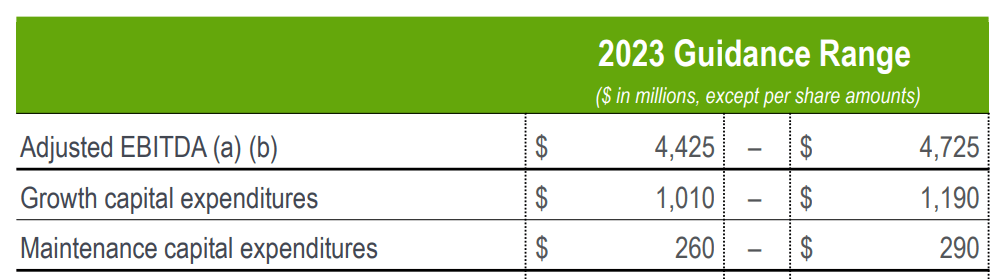

As you can see here, ONEOK's free cash flows are expected to come to around $3.3 billion, leaving the company priced around 9x forward free cash flows.

If I were to highlight one negative aspect of the investment it would be that ONEOK carries a significant amount of debt. Case in point, ONEOK is due to pay out nearly $1 billion of debt this year. That's roughly a third of its total free cash flow for 2023.

Accordingly, this leaves around $2.3 billion left over, with somewhere in the ballpark of $1.7 billion being used for its dividend payments, meaning that there's less than $500 million left to pay down the $12 billion of outstanding debt on its balance sheet.

Of course, I don't expect ONEOK to operate debt free. But it would be unwise not to at least discuss its leveraged position.

The Bottom Line

ONEOK is a midstream player that's very attractively priced considering natural gas' medium and long-term prospects.

The investment thesis is really straightforward, as it's about the fees ONEOK collects from committed volumes running through its pipelines. That's not difficult to understand.

The difficulty for investors lies in holding this stock. Case in point, despite the compelling long-term prospects of the company, not including its dividend yield, the stock really hasn't gone far in the past 12 months.

On the other hand, I'd rapidly retort that compared with nearly all other areas of the market tied to natural gas, the fact that this stock is relatively flat in the past 12 months is a massive win.

For further details see:

ONEOK: A Lot More Than Its Dividend