OKE - ONEOK And Magellan May Be Stronger Together But Face Opposition From Unitholders

2023-06-21 09:00:00 ET

Summary

- Energy Income Partners opposes ONEOK's acquisition of Magellan Midstream Partners due to tax consequences and potential loss of value.

- The acquisition would create a larger energy infrastructure footprint in Middle America, making it more attractive for larger players.

- Despite opposition, the deal could benefit ONEOK shareholders by increasing margins and creating a stronger combined entity.

The energy infrastructure industry is one that I follow closely, and I have written articles on both ONEOK ( OKE ) and Magellan Midstream Partners (MMP). Before getting to the disclosures at the end of the article, I want to say that I am a share/unit holder of Energy Transfer (ET), Enbridge (ENB), Enterprise Products Partners (EPD), OKE, and Kinder Morgan (KMI). While I don't own units of MMP directly, I own them indirectly through the Alerian MLP ETF ( AMLP ) and InfraCap MLP ETF (AMZA).

Previously, in an article I had written on ET, I indicated that I felt the energy infrastructure industry would continue to consolidate and that smaller companies would need to merge to increase their economies of scale. On May 14th, news broke that OKE agreed to acquire MMP for $18.8 billion in a deal that consisted of $25 in cash and 0.667 in common shares of OKE for every 1 share of MMP. Units of MMP immediately increased from $54.87 to $62.61 per unit and have since settled at $60.10 roughly one month later. Since the news broke, shares of OKE have declined in value as analysts raised questions about the attractiveness of acquiring refined and crude assets when OKE has focused on natural gas and natural gas liquids (NGLs). The tax consequences to MMP holders had been previously discussed as being significant upon the news breaking, and now a new wrinkle has emerged. Energy Income Partners LLC is MMP's 4th larger unitholder, owing 3.12% of the corporation (6,315,186 units), and issued a letter to MMP's board stating that it intends to vote against the proposed acquisition at the special shareholder meeting in July.

In this article, I am going to examine the letter written to MMP's Board of Directors by Energy Income Partners, look at what the combined entity would look like, and provide an opinion on if I like the deal as a shareholder of OKE.

{kind=link}

The Energy Income Partners letter has become the latest obstacle for OKE

A copy of the Energy Income Partners letter can be read here ( letter ). Overall, I felt they made some very interesting points, and depending on how many unitholders it reaches, this letter could be a major obstacle for the acquisition. I will list what I felt were the key points and then examine some of Energy Income Partners statements:

- We believe the taxes paid by our funds and investors will exceed the premium offered by ONEOK and any potential benefits from the merger.

- We want to see Magellan remain as a stand-alone entity whose returns on invested capital are far superior to ONEOK.

- The longer the units are held, the more the tax basis declines and the higher the deferred tax liability. Most of this tax is due only when the units are sold, and this proposed transaction is a sale for tax purposes and prevents unitholders from further deferring that tax liability.

- We are urging the Board to direct management to include in the S-4 a full and detailed quantitative analysis of the tax consequences to Magellan unitholders of the proposed merger with ONEOK, as we believe you are required to do. This analysis also needs to feature prominently in all future communication by Magellan, as it was not done in either merger press release.

- Since the average Magellan unitholder has held their units longer than EIP, their tax bill would be higher on average. Such a tax bill paid by all 202 million units outstanding would amount to well over $2 billion

- This deal represents an enormous transfer of value from Magellan unitholders to the Internal Revenue Service and ONEOK shareholders.

- If EIP wanted to own an investment that is 77% ONEOK and 23% Magellan, which we do not, we can do that by purchasing more ONEOK on the open market without incurring this enormous tax liability.

Energy Income Partners has owned units of MMP since Q4 2006 , so to me, there is no surprise that they would cite tax consequences so much in their letter. I am not an accountant and do not have a CPA license, so I will not offer an opinion on MLPs and taxes. If you're interested in learning more about the tax implications of the MLP structure, I suggest you conduct your own research or speak with a CPA. You can get started by reading this page ( The benefits of master limited partnerships ).

Energy Income Partners cites that MMP has a larger return on invested capital than OKE, and they are correct. Return on invested capital [ROIC] is the net operating profit after tax ((NOPAT)) dividend by invested capital, which is the sum of all debt and equity on the balance sheet.

- Earnings before income taxes = $3,546,300,000.

- Effective tax rate = 23.6%.

- NOPAT = $2,709,373,200.

- Total Debt = $13,306,000,000.

- Total Equity = $7,132,000,000.

- ROIC = 13.26%.

- Earnings before income taxes = $1,069,100,000.

- Effective tax rate = 0.3%.

- NOPAT = $1,065,892,700.

- Total Debt = $5,126,900,000.

- Total Equity = $1,681,400,000.

- ROIC = 15.66%.

The deal is reflective of the May 12th closing prices, which place an implied value on MMP's units of $67.50. Since then, OKE's share price has declined and currently sits at $60.95. Based on today's prices, unitholders of MMP would receive $25 cash plus 0.667 shares of OKE for every 1 share, which is worth $40.85 for a total value of $65.65. I didn't see language that specifies the share distribution increasing if the share price of OKE declines in the deal papers, but I may have missed it. In the letter, Energy Income Partners specifically states that based on the average cost basis of their funds, they believe that the average tax liability would be between $10-$12 per unit for retail investors based on their marginal tax bracket compared to the $9 in premium offered by the OKE deal as of 6/6/23.

Based on this language, I may not have missed anything in the documentation I read. OKE traded at $59.31 on 6/6, so 0.667% of $59.31 is equivalent to $39.56. Then, when you add $25 in cash, the value is $64.56. MMP traded for $55.41 prior to the news of the acquisition, so if the deal were to close and shares of OKE were $59.31 as they were when this letter was written, the upside from the $55.41 share price would be $9.15 per share. If Energy Income Partners is correct in their tax assumptions, this could be the information that convinces other institutions and retail investors to vote no along with them at the special meeting.

Why ONEOK is going after MMP and if I like the deal as an OKE shareholder

Before going through the deal and looking at MMP's asset mix, I wanted to look at raw financials and what financial power MMP brings to the table.

{kind=link}

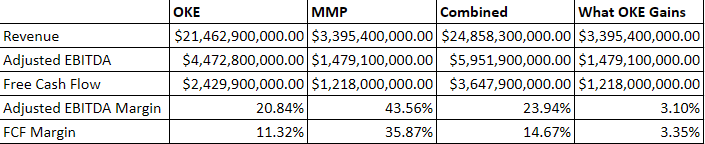

I used the TTM numbers for OKE and MMP . On paper, OKE is the larger company, as they generate more revenue, Adjusted EBITDA, and free cash flow [FCF] than MMP. On the other hand, MMP operates a higher margin business, as its Adjusted EBITDA margin is 43.56%, which is 22.72% larger than OKE, and its FCF margin is 35.87% which is 23.55% larger than OKE. By acquiring MMP, without accounting for synergies or economies of scale, OKE is adding $3.4 billion in revenue, $1.48 billion of Adjusted EBITDA, and $1.22 billion in FCF. When assets are combined with OKE, OKE will see its Adjusted EBITDA margin increase by 3.1% to 23.94% and its FCF margin increase by 3.35% to 14.67%.

{kind=link}

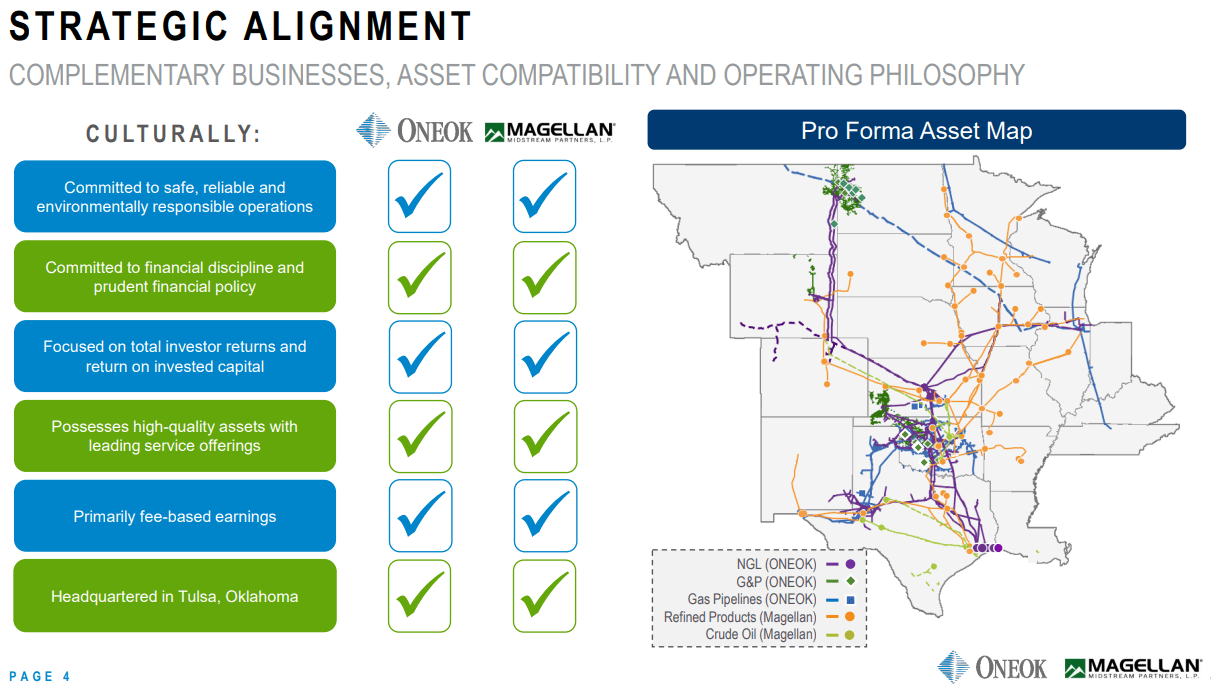

In addition to revenue, Adjusted EBITDA, FCF, and higher margins, OKE gains diversification and synergies. Both companies operate in what I consider Middle America, and MMP's assets strongly complement OKE's. In addition to positioning, it allows OKE to diversify away from natural gas and gain crude and refined products segments. From a financial perspective, OKE gains 3-7% of EPS accretion from 2025 - 2027, operating synergies of $200 million, which could be as much as $400 million in reduced expenses and $15 billion in tax deductions. The combined entity would generate $1 billion of annual FCF after dividends from 2024 through 2027.

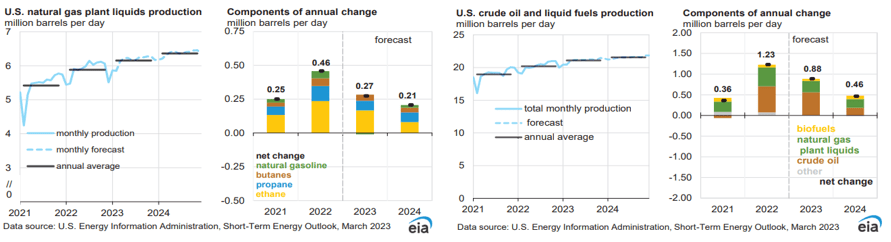

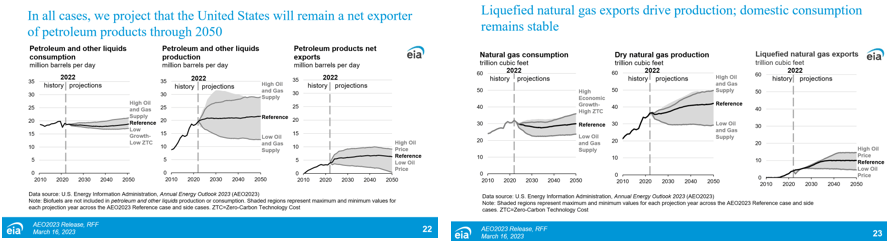

I like the deal from the perspective of an OKE shareholder. The Short-Term Energy Outlook from the EIA is clearly indicating that U.S. crude oil and liquid fuel production, in addition to natural gas production, will increase over the next two years. The reference case in the Annual Energy Outlook from the EIA projects that petroleum and other liquid production will slightly increase from now through 2050, and dry natural gas production will increase by roughly 20% through 2050. The EIA is also projecting that the United States will remain a net exporter of petroleum products and liquified natural gas [LNG] through 2050. The equation is simple, the more fossil fuels are produced, the need for transportation, storage, and refining will increase, and midstream operators will continue to see elevated needs for their services.

{kind=link}

{kind=link}

Conclusion

I like the deal from a shareholder perspective, ok OKE. I think the companies are stronger together, despite the individual margins. The acquisition will create one of Middle America's largest energy infrastructure footprints and make the combined entity that much more enticing for one of the larger players to acquire. I am not saying this will 100% occur, but I do think further consolidation will occur in the energy infrastructure space, and the combined entity is something that Kelcy Warren at ET would salivate over. I think EPD could also be interested to some degree, as it takes another chess piece off the table and further entrenches them into the Middle America market. Even if the new entity doesn't get acquired, I think the company is stronger together, and shareholders could see larger amounts of returned capital in the future as additional capital could be allocated toward the dividend. After reading the letter from Energy Income Partners, I think they have made some fair points and that there is a chance they gain traction opposing the deal or convince management to go back to the table with concessions in order to get the deal done.

For further details see:

ONEOK And Magellan May Be Stronger Together But Face Opposition From Unitholders