OKE - ONEOK - Buying For The Dividend And The Growth

2023-07-22 08:56:26 ET

Summary

- ONEOK Inc is set to become one of the largest energy infrastructure companies in the US following its acquisition of Magellan Midstream Partners, a deal valued at $18.8 billion.

- The acquisition is expected to significantly increase ONEOK's cash flow, supporting a growing dividend and potentially increasing earnings per share by 3% - 7% annually between 2024 and 2027.

- Despite potential regulatory scrutiny and the need to efficiently leverage the acquisition, ONEOK is rated as a 'buy' due to its solid dividend, recent performance, and great outlook.

Investment Summary

ONEOK Inc ( OKE ) is making strong moves to solidify itself as one of the largest energy infrastructure companies in the entire country. With the announcement of one of the largest deals in the industry's history, the acquisition of the company Magellan Midstream Partners ( MMP ) will be a major tailwind and benefit to shareholders of OKE. The massive addition of cash flows to OKE will result in them being able to support a growing dividend.

With OKE having a 12% CAGR of their dividend the last 23 years, I think investors are in at a good price point here. OKE might be slightly higher than the sector's average p/e of 9, but buying into a quality business like OKE is worth that premium in my opinion. The deal will catapult OKE into a cash flow generating machine, and I am rating them a buy as a result.

The Magellan Deal

The announcement of the MMP deal shock the energy industry and the deal is set to make OKE one of the largest energy infrastructure companies in the country. The deal is valued at $18.8 billion in a stock-and-cash acquisition offer. The deal encompassed that OKE is also taking on the net debt of MMP, which is $5 billion currently. Once the deal is complete, this would mean that the OKE has a combined enterprise value of $60 billion.

On May 14 the announcement was made and OKE is paying a 22% premium for the company with a share price of $67.5 per share based on the closing price of May 12.

Revenue Growth (Seeking Alpha)

The rationale behind the acquisition from OKE's side is that the deal will help bring together two premier energy infrastructure companies, which will result in a company with a high ROIC and robust cash flows too.

MMP is naturally a demand-driven company that because of its low capital expenditures is able to generate strong cash flows. With the TTM levered FCF being over $1 billion, MMP has a levered FCF margin of over 29%. The addition is actually expected to yield quite immediate results for OKE as the services that MMP provides are easily integrated with OKE's own business model. The first results of the deal are expected to be seen in early 2024 and between 2024 and 2027 the OKE management sees the EPS growing 3% - 7% YoY due to the acquisition. For investors of OKE that is great news as it will mean higher cash flows and a higher return to shareholders. MMP had a solid 2022 with strong cash flows, and sound projections are that MMP will add $200 annually in cash flows to OKE between 2024 - 2027.

{kind=link}

The addition of $5 billion net debt seems fairly manageable on the side of OKE. It would result in a total net debt of just under $18 billion. With the combined TTM EBITDA of both OKE and MMP of around $5.5 billion, a net debt/EBITDA ratio of 3.2 is fine by me. It's just a little higher than the threshold of three I normally keep. But I have strong faith that EPS will continue to grow, and the ratio will decrease over time.

Quarterly Result

Looking at the performance of OKE in the last quarter, they did very well in my opinion. Net income landed at $1.05 billion, which translates to $2.34 per share. The result is also impacted by an insurance settlement for OKE. Despite natural gas prices not being where they used to be, and the same goes for oil in terms of last year's highs, seeing them growing like this is reassuring.

Growth History (Earnings Presentation)

Historically, OKE has done very well even through tough commodity cycles and has continually grown its EBITDA . With a track record like this, I think it's fair to have a higher premium for the company, you are essentially paying for the expertise and robust model of the business.

2023 Guidance (Earnings Presentation Q1)

Looking ahead at the remaining part of 2023, OKE seems well on its way to achieving the goals they set in place. Net income of $2.2 - $2.5 billion would be a massive improvement from 2022 when they had $1.7 billion in net income. Why OKE is able to achieve growth like this is the increased product they are pushing for. They have also noted they are able to put in place higher feeds as an impact of inflation-based escalators. It seems OKE is hedging quite well against the lower natural gas prices that were at the start of 2023, but with the outlook remaining positive and a possible upbeat to prices, I think OKE sits in a phenomenal place right now.

Risks

The major risk with OKE right now is that they will continue to face scrutiny from regulators as the fossil-fuel industry isn't looked upon very fondly right now, and honestly, I don’t think that sentiment will ever change. The switch towards renewables is too strong to stand against, but we also need to realize the importance of the energy infrastructure we have set in place, something that OKE is a part of and will continue to benefit from.

But the investment thesis right now also relies a little bit on the fact that they can leverage efficiently from the deal of acquiring MMP. If there is a clear lack of performance post-merger, then the current price might be overvalued. But seeing as MMP is a well-run company and the same can be said for OKE I don’t see this as enough to lower my rating of the company.

Valuation & Wrap Up

For investors seeking a solid dividend addition to their portfolio that is growing despite downturns in its industry, the OKE looks very promising. The company announced recently a major deal of acquiring MMP, which would net them an enterprise value of $60 billion in total. With the expected addition of $200 million in FCF annually post-merger, then shareholders will have the opportunity to benefit heavily here as OKE prioritizes diverting capital to shareholders.

{kind=link}

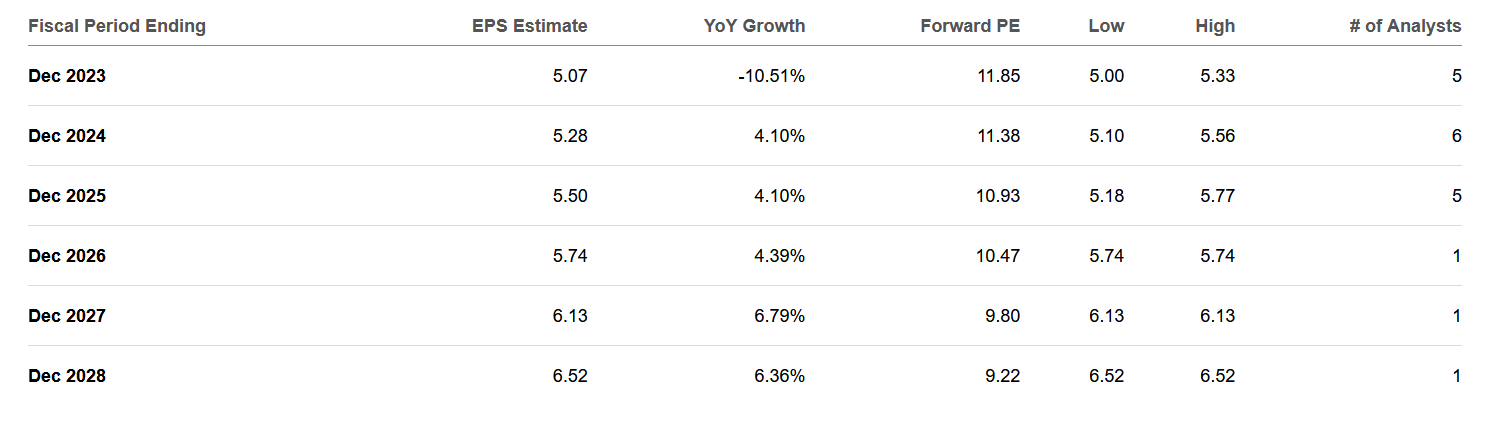

I think that with a company as solid as OKE you have to accept a little premium to the share price, and even with an FWD p/e of 12 compared to the sectors 9, I think OKE still offers plenty of potential here. I am rating them a buy based on the solid dividend and the recent performance of the business.

For further details see:

ONEOK - Buying For The Dividend And The Growth