OKE - ONEOK Buys Magellan Midstream Partners - Why I'm Bullish

2023-05-15 07:37:54 ET

Summary

- ONEOK is acquiring Magellan Midstream Partners.

- I believe this is a nice win for ONEOK shareholders. Providing diversification and growing free cash flow per share potential.

- ONEOK is determined to keep its dividend payout ratio at less than 85%, meaning that ONEOK's dividend will continue to grow unimpeded.

Investment Thesis

ONEOK ( OKE ) is a stock that is highly valued for above-average dividend yield. Meanwhile, over the weekend, ONEOK announced its intention to acquire Magellan Midstream Partners ( MMP ).

Here I discuss the details of the acquisition and how investors should think about the go-forward business.

As a recent ONEOK shareholder, I believe this is a compelling value add. Here's why.

Details of the Acquisition

ONEOK buying up Magellan will see the acquired company's share price jump. While in the coming days, I suspect that ONEOK's share price will be volatile as traders push down ONEOK's share price on the added leverage on its balance sheet and increasing share count.

Plus, once the acquisition completes post-Q3 2023, Magellan unit holders may sell out of their ONEOK position, leading to further volatility in ONEOK.

Moving on, the combined companies will now have an enterprise value of $60 billion, which starts to become significant for a natural gas pipeline company. The disadvantage here is that ONEOK will be even more leveraged, something we'll soon discuss in more detail.

The advantage, though, is that hedge funds seeking exposure to this section of the market will now migrate towards ONEOK as the "natural" go-to large and diversified midstream service provider.

Recall, ONEOK's business model is very compelling since it's predominantly driven by fee-based revenues.

Even though the business model is indirectly tied to natural gas demands, ONEOK's combined business makes its revenues from the volumes transported over its pipelines and processing facilities rather than from the price of natural gas .

Although the demand for volumes of natural gas is somewhat tied to the price of natural gas, ONEOK's go-forward business model is for the most part contingent on volumes through its pipelines .

Magellan unitholders will get about $25 in cash for every unit and 0.6670 shares of ONEOK's stock for each Magellan unit. Put another way, Magellan shareholders will get 37% cash and 63% stock in ONEOK per Magellan unit.

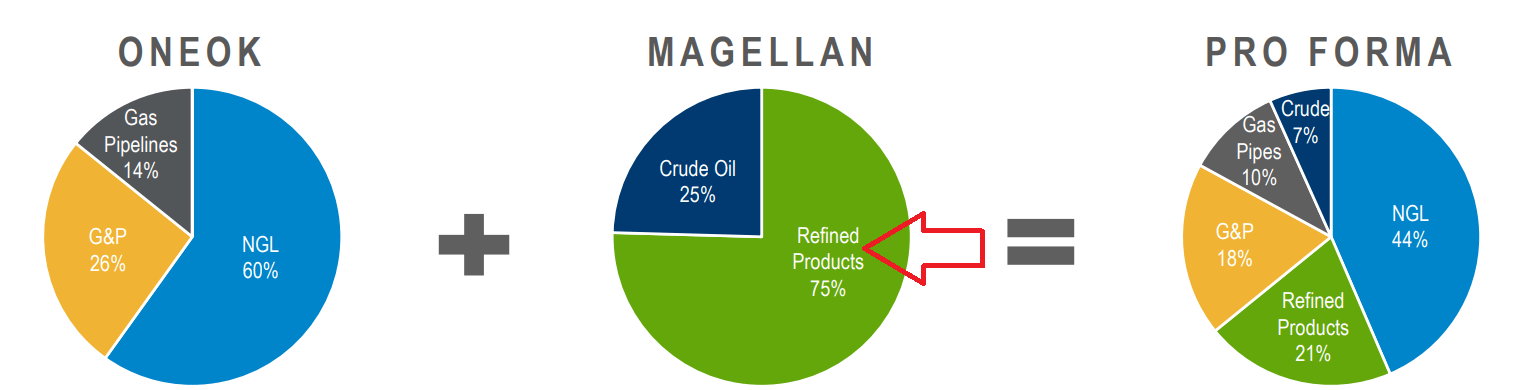

For ONEOK this brings two aspects. First is the diversification into refined products (see below).

{kind=link}

Secondly, this reduces ONEOK's dependency on Bakken, as part of its Natural Gas Liquids segment.

What the Future Holds for ONEOK?

ONEOK believes that both businesses together see potential synergies of $200 million. In other words, there are no significant synergies to this deal.

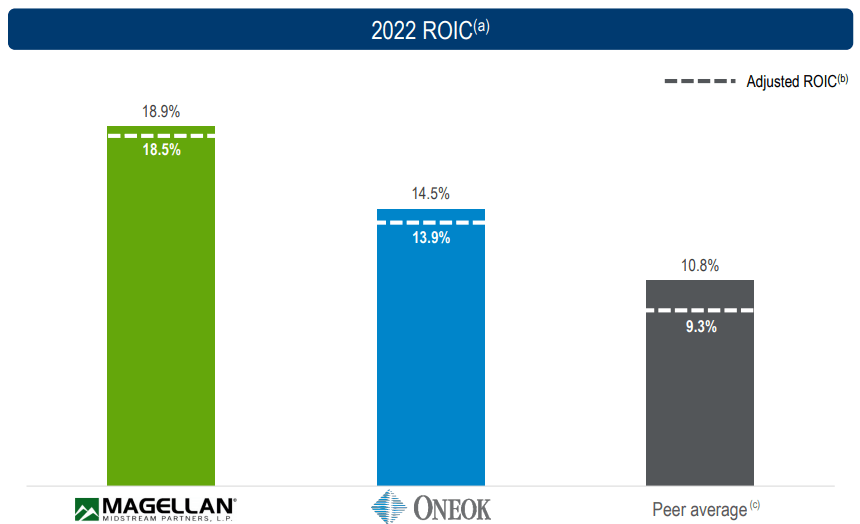

Rather, Magellan is a fast-growing business with high returns on invested capital that ONEOK believes will be accretive to its EPS figures in 2024, and accretive to its free cash flow figures in 2025.

{kind=link}

Thinking About its Valuation

As a rough estimate, Magellan was on target to report about $1.4 billion of EBITDA in 2023. While ONEOK was guiding for about $4.4 billion of EBITDA in 2023.

{kind=link}

Altogether, the combined companies plus the synergies should see around $6 billion of EBITDA in 2024.

Now, keep in mind that ONEOK had a one-off insurance settlement of $540 million that bolstered this year's EBITDA. Without this figure, ONEOK would probably be on target for approximately $4 billion of EBITDA.

Meaning that one way or another, the combined company should see around $6 billion of EBITDA in 2024. This leaves ONEOK valued very approximately at 10x enterprise value.

Although, the obvious bearish consideration is that ONEOK's balance sheet will end 2023 with more than 4x of net debt to EBITDA.

OKE and MMP acquisition

Meaning that if ONEOK wishes to return to 3.5x net debt to EBITDA over the next several years ONEOK will have its work cut out, to not only keep a growing dividend plus pay down its debt while also investing in its future growth opportunities.

The Bottom Line

ONEOK believes that, once the transaction closes, the combined business will see an average of annual $1 billion of free cash flow in the first four years. The downside here is that ONEOK's balance sheet will be seriously stretched, with net-debt-to-EBITDA of 4x.

ONEOK's shares outstanding will increase from about 447 million to 582 million, a 30% increase in the total number of shares outstanding. ONEOK will see EPS accretion of 3% to 7% per year from 2025 through 2027, meaning that, including the increase in shares, there's still around 5% CAGR to EPS coming from this deal.

With the share price at around $60, ONEOK's dividend yield has crossed slightly higher than 6% - something that I believe is very compelling.

For further details see:

ONEOK Buys Magellan Midstream Partners - Why I'm Bullish